Memory Chip Price Surge: Can the Handheld Smart Imaging Device Industry Weather the 'Cost Storm'?

03/03 2026

03/03 2026

671

671

SHEN MOU

Original Source: Shenmou Finance (chutou0325)

The 'butterfly effect' unleashed by AI is now making its presence felt in the realm of handheld smart imaging devices.

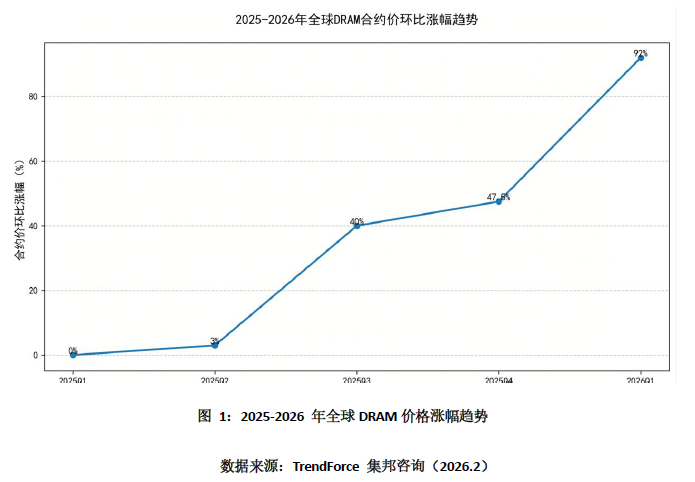

At the dawn of 2026, a fresh wave of global DRAM memory chip price increases was set in motion. TrendForce's February 2026 data reveals that the cumulative spot price surge for memory chips over the preceding three months has surpassed 300%.

Behind this dramatic spike lies the AI industry's voracious appetite for memory production capacity. Memory chip manufacturers have been redirecting their consumer-grade memory chip production towards high-bandwidth memory (HBM) and server-side memory, both in high demand for AI computing. This shift has led to a dwindling supply of consumer-grade memory chips and a consequent price explosion, exerting immense cost pressure on the entire consumer electronics supply chain.

Compared to general consumer electronics, handheld smart imaging devices are particularly vulnerable to fluctuations in memory chip prices. Moreover, their significantly smaller procurement volumes compared to smartphone and PC manufacturers result in even higher procurement costs.

This confluence of factors presents a formidable challenge to the profitability of the handheld smart imaging industry during this memory chip price hike cycle, casting a pall over its future profit prospects.

01

Advanced Process Capacity Shift to HBM Fuels DRAM Price Increase

The global DRAM memory chip price surge is not an isolated incident; it is propelled by a profound reconfiguration of upstream capacity allocation logic by the AI industry.

Currently, the global DRAM market is dominated by three giants: Samsung, SK Hynix, and Micron, collectively commanding over 90% of the market share.

This concentration of power gives them significant sway over capacity allocation. With the burgeoning demand for AI computing power, these manufacturers have been hastening the shift of their advanced process capacity towards HBM and server-side memory products since 2025.

According to publicly available information, Samsung has reallocated 30% of its advanced consumer-grade DRAM capacity to HBM3, SK Hynix has shifted 40%, and Micron has also redirected 25% of its capacity.

This round of capacity adjustments has directly slashed the effective global consumer-grade DRAM capacity by approximately 20%, effectively rewriting the capacity allocation playbook of upstream memory manufacturers.

The capacity structure adjustment is immediately reflected in prices. Monitoring data from multiple agencies, including TrendForce, Goldman Sachs, and UBS Securities, indicates that global DRAM contract prices soared by 90%–95% quarter-over-quarter in the first quarter of 2026. For handheld smart imaging device manufacturers, this translates to escalating memory chip procurement costs, potentially becoming a key factor affecting profitability.

From a supply-demand perspective, a Goldman Sachs report highlights a roughly 15% supply-demand gap in the global DRAM market in 2026, with AI-related scenarios consuming over 40% of the high-end DRAM capacity at once. TrendForce predicts that the global DRAM supply-demand gap will narrow to 5% in the fourth quarter of 2026 and reach equilibrium in the first quarter of 2027.

In essence, the AI-driven supply crunch in consumer-grade DRAM is unlikely to abate in the near term, continuing to test the cost control prowess of the handheld smart imaging industry.

02

Why Are Handheld Smart Imaging Devices More Vulnerable to Memory Price Hikes?

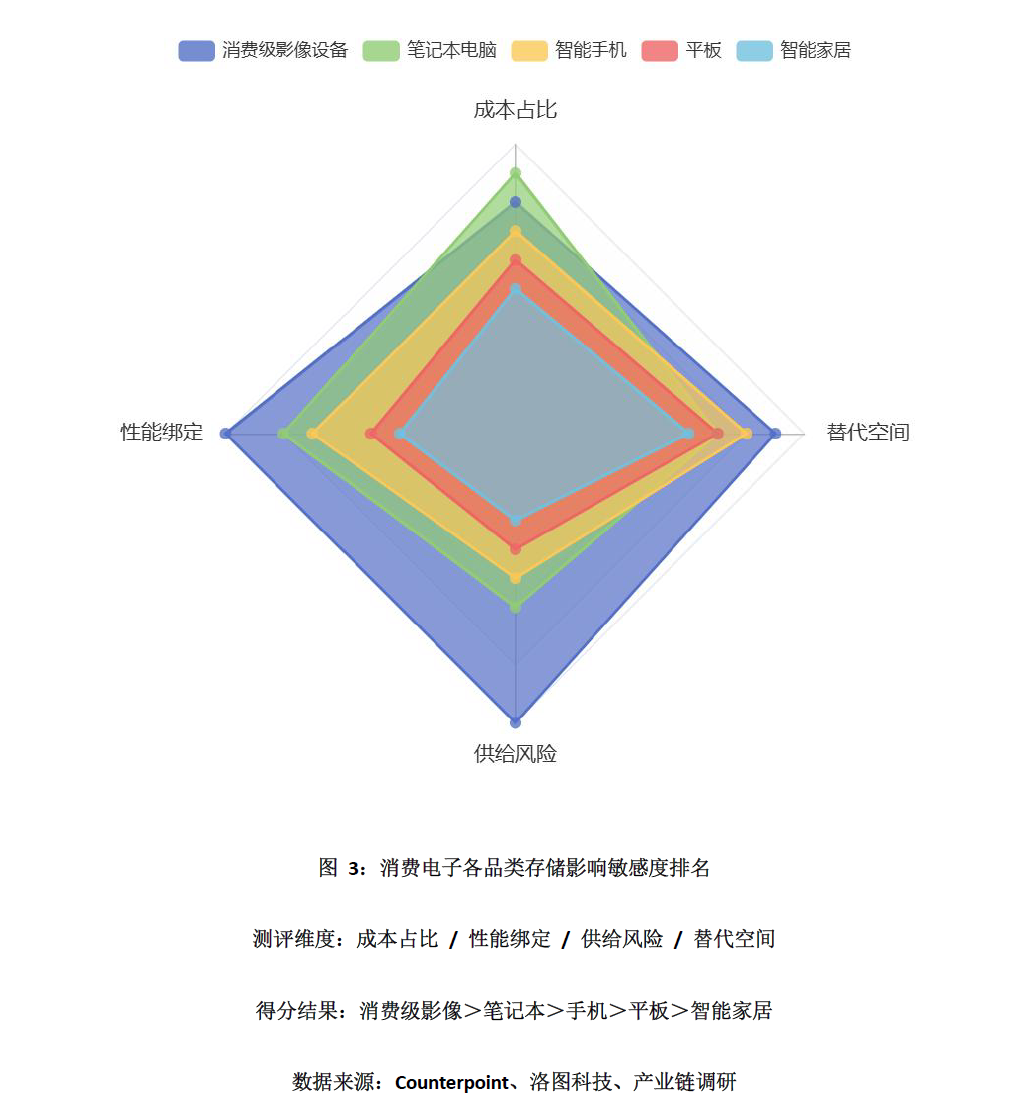

Among consumer electronics, why do memory price hikes hit handheld smart imaging devices harder than smartphones and PCs? This stems from both the technical nature of the products themselves and the varying bargaining power of different market segments within the supply chain.

The impact of memory price hikes on handheld smart imaging devices can be attributed to two primary factors.

On one hand, consumer electronics products with highly specialized functions (single-core scenarios) have their user experience entirely dictated by the upper and lower limits of the imaging system.

The imaging system comprises lenses, sensors, processors, algorithms, and memory. In this closed-loop system, performance bottlenecks in any single component can lead to a decline in overall imaging performance.

Among these components, memory chips play a pivotal role as the conduit for high-throughput data flow, significantly influencing key functions such as panoramic stitching, electronic image stabilization, and video quality.

Take panoramic cameras as an illustration: insufficient memory performance can result in stitching artifacts, failed image stabilization, or increased noise, directly compromising the basic user experience of the product. Hence, memory performance carries more weight in handheld imaging devices compared to general consumer electronics.

On the other hand, at the supply chain level, the relatively modest procurement scale of handheld smart imaging devices further exacerbates cost pressures.

According to IDC data, smartphone shipments reached 1.26 billion units in 2025, personal PC shipments stood at 280 million units, and global wrist-worn device shipments hit 150 million units in the first three quarters. In contrast, annual shipments of handheld smart imaging devices hover around tens of millions of units.

Compared to major smartphone and PC manufacturers like Apple, Samsung, and Lenovo, which boast large procurement volumes and long-term supply agreements with manufacturers and are thus prioritized in capacity allocation, handheld smart imaging device manufacturers have relatively modest procurement scales. Most of them can only secure supplies through distributors, resulting in higher procurement prices. Some manufacturers even need to pay additional premiums to secure the required DRAM products, naturally amplifying cost pressures.

03

Rising Costs Amidst Market Competition: Further Squeezing Industry Profit Margins?

If the previous analysis remained at the level of theoretical deduction, specific supply chain data now renders the impact of this round of cost shocks more tangible.

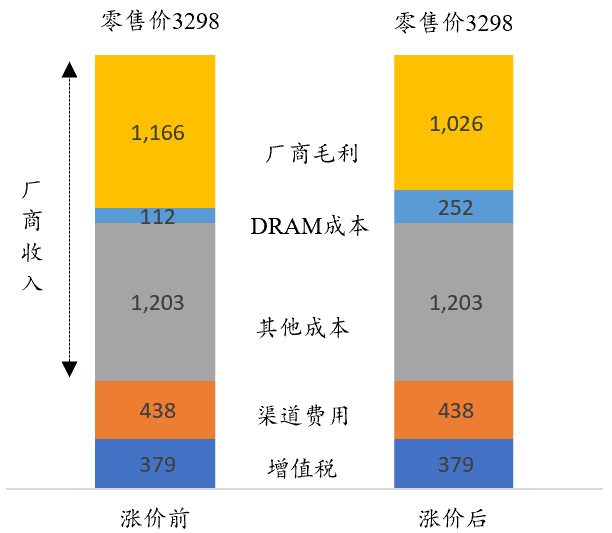

Take a flagship panoramic camera from a certain manufacturer as an example: it utilizes two Micron LPDDR5 2GB memory chips. The price per chip in the agency channel has surged from a low of $8–$10 in the fourth quarter of 2025 to $16–$18 currently (spot price: $25–$30).

Through straightforward calculations, the gross profit margin of this flagship panoramic camera has plummeted by nearly 6 percentage points.

Notes

1: The retail price is based on JD.com's self-operated price. Value-added tax is calculated at 13% in accordance with tax law. Channel fees are set at 15% based on supply chain research. The gross profit margin is estimated at 47% based on a certain listed company's Q3 gross profit margin. DRAM costs are calculated at $8 and $18 per chip before and after the price hike (spot price: $25–$30).

Note 2: ① JD.com retail price: 3,298 RMB; retail price excluding VAT: 3,298/1.13 = 2,919 RMB; after deducting 15% channel commission: 2,919 * 0.85 = 2,481 RMB; ② Revenue confirmed by the manufacturer per unit sold = 2,481 RMB; price increase for two 2GB chips (from $8 to $18) = 2 * (18 - 8) * 7 = 140 RMB; ③ Impact on gross profit margin: 140/2481 = 5.64%.

Note 3: Spot price source: DRAMeXchange.

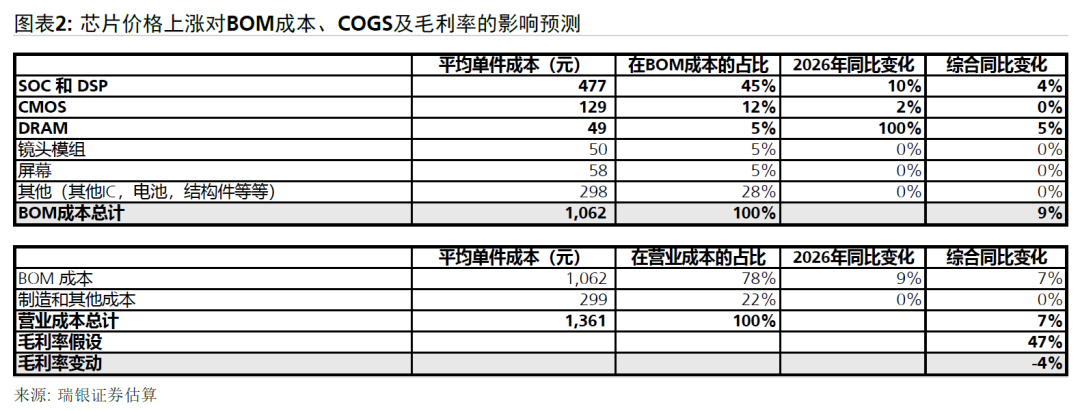

UBS Securities also highlighted in a research report on Insta360 released on February 6 that, affected by the shortage and price hikes of memory chips, Insta360's product costs are expected to rise by about 6% in 2026, with a potential decline in gross profit margin of 4 percentage points.

Meanwhile, major manufacturers of handheld smart imaging devices, such as DJI, Insta360, and GoPro, all plan to expand their market shares in 2026, leading to increased product line overlap and intensified market competition.

Under the dual onslaught of rising costs and heightened competition, there is limited scope for product price increases, and the gross profit levels of new products are also under duress, potentially impacting the overall profit performance of the industry.

In conclusion, the current round of memory chip price hikes is driven by the structural adjustment of production capacity resulting from the AI industry's evolution. In the short term, the tight supply of consumer-grade DRAM is likely to persist.

For the handheld smart imaging device industry, factors such as small procurement scales, highly specialized functions, intensified market competition, and limited room for product price increases are squeezing profit margins from both ends. If cost pressures continue to mount while terminal prices fail to adjust effectively, some companies within the industry may face losses in 2026.

* Images sourced from the internet. Please contact us for removal if there is any infringement.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan