China’s Smart Box Market: Scale Hits Rock Bottom; Breakthroughs Seen in Gaming, Learning, and AI Integration

04/29 2026

04/29 2026

520

520

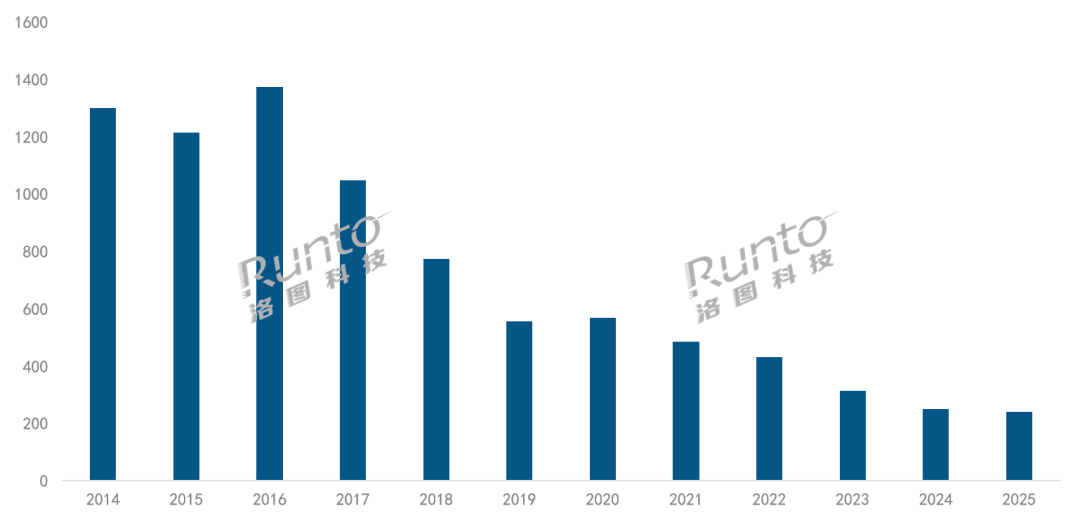

Over the past decade, China’s smart (OTT) box market has undergone significant transformation. After a period of rapid expansion from 2011 to 2016, the market peaked at nearly 14 million units before experiencing a downturn, with current sales falling below 2.5 million units.

According to Runto data, total channel sales in China’s smart box market (excluding operator and broadcast-specific boxes) are projected to reach 2.406 million units in 2025, marking a 3.4% year-on-year decline.

China Smart Box Market Total Channel Sales Volume (2014–2025)

Data Source: Runto, Unit: 10,000 units

In China, the penetration rate of smart TVs has plateaued, with built-in features becoming increasingly comprehensive. This has significantly reduced the need for external boxes. Over time, broadcasters and operators have been promoting set-top-box-free solutions, replacing external devices with direct coaxial connections and software-based terminals. Meanwhile, the widespread adoption of affordable screen-mirroring tools has further diverted casual users. Additionally, ongoing policy efforts to encourage "built-in set-top boxes" and integrated terminals have further constrained the growth potential of standalone boxes.

However, as the saying goes, “the worst is behind us.” Despite the continued market contraction, the rate of decline has slowed considerably, suggesting that the industry is approaching a stabilization phase. The market is nearing its lowest point, with specific demand segments beginning to sustain the foundational market.

Brand Landscape:

Tencent, Xiaomi, and Tmall Magic Box Lead the Market

Currently, traditional e-commerce platforms like Tmall and JD.com dominate China’s smart box sales. According to Runto, online channel sales reached 1.299 million units in 2025, remaining relatively stable compared to 2024 and accounting for 56.3% of the total market.

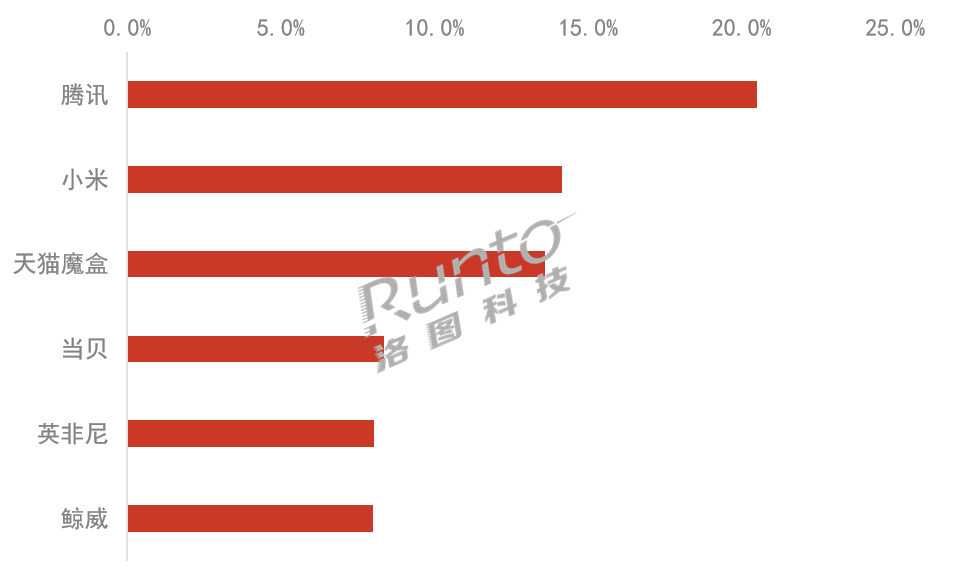

In 2025, the competitive landscape among leading smart box brands on mainstream e-commerce platforms underwent significant changes. Industry resources increasingly flowed toward mainstream brands with strong content ecosystems, product innovation capabilities, and channel advantages, while smaller brands and white-label products saw their market shares decline or exit entirely. Runto’s online monitoring data reveals that Tencent maintained its top position in sales for the year, with Xiaomi overtaking Tmall Magic Box for second place. Jingwei, which ranked fourth in 2024, fell out of the leading group and was replaced by Dangbei.

Tencent continues to dominate the mainstream e-commerce market with a 20.5% share, thanks to its robust content ecosystem and superior product offerings. Leveraging resources from its video platform, cloud services, and gaming content, Tencent’s boxes create a closed-loop ecosystem for content distribution and user engagement. Additionally, by integrating cutting-edge technologies such as 8K ultra-high definition, Dolby Vision, Dolby Atmos, HDR Vivid, and DTS, Tencent has established a strong competitive edge.

The Tencent Aurora Box, developed in collaboration with Xiaopai Technology, has seen increased investment in ultra-high-definition product resources. The partnership has built a technological advantage in core areas like AI-enhanced audio-visual experiences and Tencent’s Hunyuan multimodal large models. In 2025, the jointly launched Tencent Aurora Box 7 series broke away from low-end price competition, capturing nearly half of the premium market segment (priced above 500 yuan).

Xiaomi’s strength lies in its IoT ecosystem and brand reputation, holding a 14.1% share of the mainstream e-commerce market in 2025. The Xiaomi Box 5, launched in May 2025, became the brand’s second-best-selling model, contributing 22.5% to its annual sales.

Tmall Magic Box capitalizes on the home-court advantage of Taobao’s e-commerce platform, holding a 13.6% market share. By 2025, the product had evolved to its eighth generation, with significant improvements in performance, system fluidity, and interactive experience. The brand often leverages e-commerce promotions and penetration into lower-tier markets, succeeding through cost-effectiveness and channel efficiency.

Market Share of Major Brands in China’s Traditional Mainstream E-commerce Smart Box Market (2025)

Data Source: Runto Online Monitoring Data, Unit: %

Product Highlights:

Gaming, Learning, and AI Large Models Drive Innovation

After more than a decade of development, smart box hardware has matured, with 4K resolution and quad-core processor penetration exceeding 95%. In 2025, gaming capabilities, educational applications, and AI integration have emerged as key innovation areas for mainstream manufacturers.

First, gaming capabilities have been enhanced. With advancements in cloud gaming technology and network infrastructure, manufacturers like Tencent have introduced cloud gaming platforms, improved controller compatibility, and optimized system performance, enabling console-like gaming experiences on TVs. This expansion of use cases has boosted device engagement and usage rates.

Second, educational applications have gained traction. Amid sustained demand for home-based learning, smart boxes have evolved from entertainment hubs to educational tools by integrating children’s education content, picture book reading, synchronous classrooms, and enrichment programs. Large-screen eye protection, remote control functionality, and AI tutoring features directly address parents’ needs for healthy and efficient screen time.

A more transformative shift comes from AI large model integration. With generative AI advancements, smart boxes now offer more than basic voice-activated content requests. They can understand semantic meaning, engage in multi-round dialogues, provide personalized recommendations, and execute cross-application tasks.

At the application level, some models support deep integration with AI platforms like DeepSeek, enabling Q&A, translation, and content explanation functions. The Tencent Aurora Box, in particular, led the industry by deploying the OpenClaw AI agent tool, enabling automated management of schedules, documents, and smart home devices. It also pioneered AI-driven picture book generation on set-top boxes, allowing users to create personalized content via voice commands.

Market Forecast:

Moderate Decline Expected, with 2.3 Million Units Projected for 2026

Looking ahead, Runto believes that China’s smart box market is unlikely to return to growth in the short term but is also no longer poised for a significant decline. Over the next two to three years, the market will experience moderate fluctuations.

From a demand perspective, limited new user growth makes substantial market expansion unlikely, but replacement demand and niche-scenario needs will provide basic support. Scenarios such as upgrading older devices and catering to specific user groups (e.g., elderly users and families with children) still offer growth potential.

From a competitive standpoint, market consolidation will intensify. As ecosystem capabilities become increasingly critical, manufacturers with strong content, system, or AI offerings will expand their advantages, while brands lacking core resources will gradually exit.

From a product evolution perspective, AI will be a decisive factor shaping the industry’s future. If large model capabilities can be effectively implemented in OTT scenarios and deliver tangible user value, smart boxes could be redefined as essential household gateways rather than peripheral devices.

However, challenges remain, including computational costs, interactive experiences, and content adaptation. If these issues persist, AI’s impact on market growth may remain limited to conceptual advancements.

Runto forecasts that China’s smart box market will continue to decline, reaching approximately 2.3 million units in 2026, a 4% year-on-year decrease.

-

New Regulations Set the Tone: Farewell to Ineffective Involution in L3, L4 is the Ultimate Goal for Autonomous Driving Commercialization

-

![]()

Let's Imagine: What If DeepSeek and Kimi Merged?

-

![]()

Why Are Young People Choosing 'Reverse Car Upgrades'?

-

![]()

Who 'Killed' the Profits of Cars in the Era of Intelligent Electric Vehicles?

-

![]()

China’s Smart Box Market: Scale Hits Rock Bottom; Breakthroughs Seen in Gaming, Learning, and AI Integration

-

![]()

70.06 Million Yuan in Subsidies Lead to First-Quarter Profitability, Moore Threads Continues to Await Commercialization Turning Point

-

![]()

Momenta's Ambitions for 'Physical AI' Must Overcome the Challenge of 'Momenta Quotient'

-

![]()

China’s Former Color TV Titan Now Faces Delisting Crisis