Shifting 'Multi-Brand' Leftward, 'Multi-Category' Rightward: Is Aux's Trajectory Echoing Gree's?

04/29 2026

04/29 2026

392

392

Editor: Liu Zhicheng

Reviewer: Xu Xu

The recent public spat between Gree and Hisense air conditioners has certainly grabbed attention, with both sides trading barbs, leaving many observers to remark:

It seems high-stakes business battles still rely on the most direct tactics!

Indeed, this clash between the two industry titans has a certain raw, unrefined quality.

While their dispute may appear fierce at first glance, the 'intensity' of this business war pales in comparison to past confrontations—remaining largely confined to media statements and verbal jousts, devoid of any real, direct clashes.

It's worth noting that in the annals of air conditioning industry conflicts, the decade-long patent and trade secret litigation between Aux and Gree stands out.

The two sides escalated from exchanging accusatory letters to court battles demanding compensation in the millions, eventually reaching claims as high as 225 million yuan, and culminating in appeals at the Supreme People's Court...

The ferocity of that relentless struggle far surpasses today's mere verbal skirmishes.

However, as time marches on, Aux, in contrast to Gree's enduring fighting spirit, has adopted a much more restrained approach.

It wasn't until last year that Aux finally achieved its long-held aspiration of listing on the Hong Kong Stock Exchange.

But unexpectedly, the newly capital-market-listed Aux Electric recently released a disappointing 2025 performance report, swiftly shifting the investment market's focus...

Growth 'Slowdown': Aux Awaits Its Next Move

Indeed, it was quite unexpected. Prior to going public last year, Aux's performance was impressive.

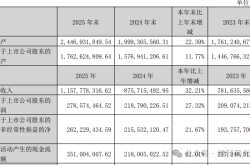

The prospectus revealed that from 2022 to 2024, Aux Electric's revenue stood at approximately 19.528 billion yuan, 24.832 billion yuan, and 29.759 billion yuan, respectively, with year-on-year growth rates of 27.2% and 19.8% in 2023 and 2024.

Corresponding net profits attributable to the parent company were 1.442 billion yuan, 2.487 billion yuan, and 2.910 billion yuan, with year-on-year growth rates of 72.5% and 17.0% in the latter two years.

In the first quarter of 2025, Aux Electric's revenue reached approximately 9.352 billion yuan, up 27.0% year-on-year; net profit stood at 924.5 million yuan, up 23.01% year-on-year.

However, post-IPO, Aux's first annual report revealed that in 2025, its revenue growth rate plummeted to 0.97%, and the growth rate of net profit attributable to the parent company turned negative, dropping to -23.20%.

The corresponding gross profit margin also fell from 20.97% at the end of 2024 to 18.84%, and the net profit margin dropped from 9.78% to 7.44%.

This was primarily due to intensified market competition, rising raw material prices, and increased uncertainty in the global economic environment.

Of course, this performance should be viewed dialectically.

Although Aux's performance 'changed dramatically' post-IPO, conversely, one might marvel at the timing of Aux's listing, its sharp vision, and its clear grasp of market trends amidst such a stark contrast.

However, a closer look at the 2025 annual report reveals some puzzling aspects of Aux's operations.

On one hand, perhaps to cope with the pressure of rising raw material costs and shrinking profits, Aux Electric implemented certain cost-control measures last year.

For instance, significantly reducing its workforce.

Financial reports indicate that as of December 31, 2025, the group had a total of 15,631 employees, a net decrease of 4,163 compared to the end of 2024 (19,794), representing a reduction of over 21%.

Additionally, according to the prospectus, as of March 31, 2025, Aux actually had 22,408 full-time employees, including 21,792 in China and 616 overseas.

Based on this data, Aux optimized 6,777 employees in nine months last year.

Curiously, in 2025, Aux's total salary costs were approximately 2.3588 billion yuan, compared to 2.3609 billion yuan in 2024.

This means that despite optimizing over 20% of its workforce, Aux only saved about 2.1 million yuan in salary costs.

Did they give raises to existing employees, or were the laid-off employees extremely inexpensive?

On the other hand, in terms of expenses, even though Aux faced significant pressure on performance growth last year, its 'sales and distribution expenses' and 'administrative expenses' still increased by 25.5% and 6.0% year-on-year, reaching 1.603 billion yuan and 1.087 billion yuan, respectively.

This was mainly due to business expansion, increased expenses from new overseas sales companies, heightened promotional spending, and higher warehousing, logistics, and depreciation costs for new bases.

From the 2026 operational guidance in the financial report, this increase in expenses aims to further improve the overseas market layout and enhance future revenue growth, representing Aux's attempt to break through by trading time for space.

As for the remaining R&D expenses, they might have been considered for cost reduction and efficiency improvement.

In 2024, Aux's R&D expenditure was approximately 688.7 million yuan, down 3.0% year-on-year from 710 million yuan in 2023.

This was mainly due to optimizing the R&D personnel structure, which improved innovation efficiency and resource allocation.

However, this has led to some new issues in the business market:

First, compared to Gree, Haier, and Midea, Aux has a significant gap in R&D investment scale and R&D expense ratio.

For example, Tianyancha APP shows that in 2025, Haier Smart Home and Midea Group's R&D expenses reached 10.10 billion yuan and 17.79 billion yuan, respectively.

As for Gree Electric Appliances, its R&D expenses in the first three quarters of last year were 5.622 billion yuan, up 5.03% year-on-year.

But now, Aux is further reducing its R&D expenditure. Will this affect the long-term competitiveness of its brand products? Could it be a case of being penny-wise and pound-foolish?

Moreover, against this backdrop, Aux announced price hikes for its products this year, such as a 3%-8% increase in home air conditioners and home central air conditioners starting from January 19...

So, with no significant improvement in brand and product strength, will consumers pay for Aux's price hikes?

The verdict may need more time.

Fortunately, after successfully obtaining listing financing, Aux's asset-liability pressure has significantly reduced, leaving more room for trial and error.

The prospectus showed that from 2022 to the first quarter of 2025, Aux's asset-liability ratios were 88.3%, 78.8%, 84.1%, and 82.5%, respectively, far exceeding those of industry giants like Gree and Midea.

Now, Aux's asset-liability ratio has dropped to 68.3%, and its cash and bank balances have increased from 2.908 billion yuan at the end of 2024 to 6.879 billion yuan, providing a thicker financial cushion.

However, one criticism is that with such a high asset-liability ratio in the past, in 2024 (the year before going public), Aux still used 'cash and bank balances' to declare a one-time dividend of 3.7935 billion yuan to shareholders.

Most of this dividend went to the founding family of Zheng Jianjiang.

Immediately after, in the use of proceeds from the capital raising, Aux mentioned 'will be used for working capital and general corporate purposes.'

Although this 'dividend first, then list to replenish funds' approach is not a violation of regulations, from an investment perspective, major shareholders cash out early, while post-listing operational risks and financial pressures are shared with new shareholders. Coupled with the sudden performance decline, it raises concerns:

When Aux knocked on the door of the Hong Kong Stock Exchange, how much of the blueprint described in the prospectus was for long-term operations, and how much was just for the sake of going public?

The Era of Major Diversification: Go Overseas, but Also Diversify?

From a business perspective, Aux now faces the same dilemma as its 'old rival' Gree—a relatively single business structure.

In 2025, Aux's sales revenue from air conditioning products (home air conditioners + central air conditioners) was approximately 29.52 billion yuan, accounting for a staggering 98.24% of total revenue.

However, unlike Gree, which is actively expanding overseas while also trying to diversify its product lineup, Aux has not made many moves to expand its product categories.

The remaining 'other' revenue segment mainly comes from group scrap and raw material sales, as well as brand licensing fees.

Overall, it's still largely a one-legged operation.

So, how does Aux plan to break out of this?

There are two main actions: First, as mentioned earlier, ramping up efforts in overseas markets, a path already validated by Haier, Midea, and TCL Smart Home.

Objectively speaking, this route is full of potential, but for Aux, the uncertainties and challenges remain significant.

At first glance, Aux's overseas market revenue is now as high as 14.7411 billion yuan, accounting for 49.06% of total revenue, seemingly reaping substantial rewards.

However, Aux Electric's overseas business is mostly based on the low-margin ODM model.

According to the prospectus, from 2022 to 2024, its ODM business revenue in overseas markets was approximately 6.881 billion yuan, 8.503 billion yuan, and 11.937 billion yuan, respectively, accounting for about 80% of total overseas revenue.

More worryingly, affected by external factors such as tariff trade wars, Aux's overseas market revenue in Europe and North America fell by 6.3% and 30.7% year-on-year in 2025, respectively, while South America only grew by 0.1%. Only Asia (excluding mainland China) saw revenue grow by 11.8% year-on-year, representing minimal overall growth.

Against this backdrop of slowing overseas market growth, how well is Aux's brand accepted overseas? How are its consumer channels performing?

When will its proprietary brand business step up to drive growth?

The second action is to opt for a multi-brand matrix rather than first focusing on diversifying its product categories.

In addition to its main brand Aux AUX, it has launched the cost-effective sub-brand Huasuan, the youth-oriented brand AUFIT, and the high-end brand ShinFlow, aiming to tap into niche market segments for brand growth.

This is Aux's most differentiated choice, but also the most debatable.

After all, past experience shows that Gree fell significantly behind Haier and Midea in terms of revenue scale and valuation because it failed to promptly and firmly pursue a diversified product strategy.

The contrast between advancement and retreat is stark.

Moreover, the air conditioning industry is now highly mature. From Xiaomi's challenge for the second-place spot in online air conditioner sales last year to the current public sparring among Hisense and others, it can be seen as a shock and shakeup to the traditional air conditioning industry landscape led by Gree.

If even the industry leader struggles to maintain an independent trajectory, why should Aux stubbornly focus on a single air conditioning category, and even build a multi-brand matrix at this time, further dispersing brand momentum and consumer attention?

Furthermore, let's be blunt: Gree has a unique cost and technological moat, so even though its growth is under pressure, its overall gross profit margin and profitability remain strong.

From 2022 to 2024, Gree Electric Appliances' gross profit margins were 26.04%, 29.43%, and 29.43%, respectively; net profit margins were 12.18%, 13.59%, and 17.11%.

What about Aux, known for its cost-effectiveness?

During the same period, its gross profit margins were 21.25%, 21.84%, and 20.97%; net profit margins were 7.38%, 10.01%, and 9.78%.

In 2025, they were 18.84% and 7.44%, respectively, with a clear gap between the two.

From this perspective, in addition to going overseas, Aux also needs to make second-tier preparations in advance to find its own path to diversification...

Of course, this means Aux will need to further increase its R&D expenditure, and its net profit may continue to suffer for a considerable time.

But honestly, just like its current counter-cyclical increase in sales expenses, this is itself a strategic investment in the future. You can't catch the wolf without risking the cubs.

Moreover, judging by its 2026 operational priorities, Aux has officially proposed implementing a 'multi-category expansion' layout.

Since the trend is unstoppable, why not give Aux a bit more time to see if it can forge its own path amid the winds and waves?

After all, the business world is never short of stories of rapid advancement. What is truly scarce is the resolve to stay on course amid slowdowns and controversies.

The road is long, the wind has not stopped, and we hope Aux can carry that unyielding entrepreneurial spirit, turning lows into accumulation and slowdowns into gear shifts.

Like a true long-termist, daring to quietly sow the seeds of future success at unpopular junctures...

Disclaimer: This article is based on legally disclosed company information and publicly available data, and expresses opinions. However, the author does not guarantee the completeness or timeliness of this information. Additionally, the stock market carries risks, and caution is advised when entering. This article does not constitute investment advice; investment decisions should be made independently.

-

![]()

Shifting 'Multi-Brand' Leftward, 'Multi-Category' Rightward: Is Aux's Trajectory Echoing Gree's?

-

![]()

Revenue Soars for Five Straight Years! Unveiling the Wealth Secrets in FuJing Technology's Annual Report

-

New Regulations Set the Tone: Farewell to Ineffective Involution in L3, L4 is the Ultimate Goal for Autonomous Driving Commercialization

-

![]()

Let's Imagine: What If DeepSeek and Kimi Merged?

-

![]()

Why Are Young People Choosing 'Reverse Car Upgrades'?

-

![]()

Who 'Killed' the Profits of Cars in the Era of Intelligent Electric Vehicles?

-

![]()

China’s Smart Box Market: Scale Hits Rock Bottom; Breakthroughs Seen in Gaming, Learning, and AI Integration

-

![]()

70.06 Million Yuan in Subsidies Lead to First-Quarter Profitability, Moore Threads Continues to Await Commercialization Turning Point