Insta360 Financial Report: Stellar Growth, Profit Under Strain—Where Lies the Turning Point?

05/03 2026

05/03 2026

479

479

By Yang Xuejian

From Node Finance

On April 28, Insta360 (688775.SH) unveiled its financial results for the full year of 2025 and the first quarter of 2026. The report reveals that Insta360 achieved a revenue of RMB 9.741 billion in 2025, marking a 74.76% year-on-year increase, and secured a 66% global market share in panoramic cameras and a 57% share in thumb cameras. The growth momentum persisted into the first quarter of 2026, with revenue reaching RMB 2.481 billion, up 83.11% year-on-year. However, despite the revenue surge, Insta360's net profit attributable to shareholders declined to RMB 929 million in 2025 and further dropped to RMB 84.62 million in the first quarter of 2026.

"Why did profits decline despite revenue growth?" Before external doubts surfaced, Liu Jingkang, the founder of Insta360, addressed this in a heartfelt open letter, penned "without the aid of AI."

"2025 was Insta360's fastest and most comprehensive growth year since inception. It was an extraordinary year: listing on the STAR Market in June 2025, embarking on a new journey; launching a panoramic drone at year-end, achieving differentiated growth amidst industry giants; and successfully resolving a two-year lawsuit with the pioneer of action cameras earlier this year. Storms have never been absent, but we have consistently navigated through them," Liu wrote in the open letter.

High-Intensity Strategic Investment Dilutes Profit Margins

"Revenue growth exceeded 70% for both 2025 and Q1 2026, while R&D expenses surged by over 95% year-on-year in both periods," Liu highlighted.

A review of Insta360's financial report by Node Finance reveals that, from a business structure perspective, Insta360's growth remains heavily reliant on its core action imaging segment. New product categories have yet to contribute revenue, resulting in high business concentration. Subsequent growth stability hinges on the successful launch of new products and market expansion efforts.

In the imaging market, sustaining high growth requires triple support from product iteration, market presence, and distribution channels. Short-term growth may rely on marketing and channel expansion, but breaking through long-term growth ceilings depends on business boundary expansion and sustained user reputation.

Thus, Insta360 is aggressively expanding its business, most notably reflected in its R&D expenditure.

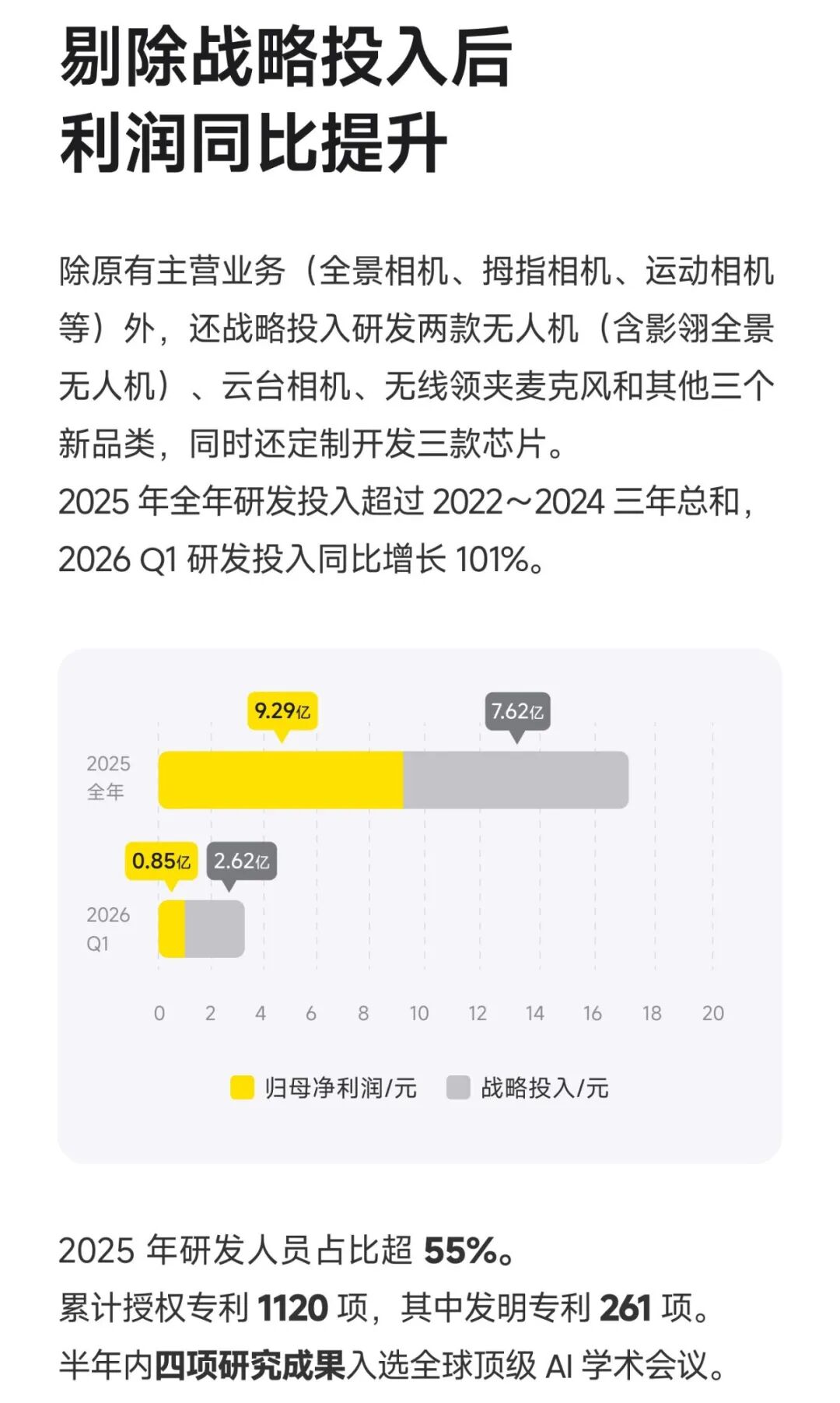

Node Finance observed in the financial report that Insta360's R&D investment reached RMB 1.53 billion in 2025, nearly doubling year-on-year and surpassing the total of the previous three years. In the first quarter of 2026, R&D investment reached RMB 465 million, up 101% year-on-year, with R&D growth consistently outpacing revenue growth. R&D personnel accounted for over 55% of the workforce, with a cumulative total of 1,120 authorized patents. R&D resources are concentrated on core technologies and new businesses.

From the perspective of R&D funding allocation, Insta360 focuses on three key areas:

1. New product category development, including gimbal cameras, wireless lavalier microphones, and drones, planned for launch within the year;

2. Core hardware self-development, with simultaneous custom development of three chips to reduce external supply chain dependencies;

3. AI and cutting-edge technology deployment, advancing the development of "photography robots" and panoramic vision technology. In 2025 and the first quarter of 2026, strategic investments reached RMB 762 million and RMB 262 million, respectively.

"High-intensity strategic investments support the company's long-term development layout but also lead to a decline in short-term profit metrics," Liu stated.

Indeed, Insta360's approach aligns with the tech industry's pattern of prioritizing long-term technological barriers over short-term profits, a proactive choice made by most "long-termist" companies. However, in Node Finance's view, Insta360 must still balance the commercialization progress of its heavily invested new products with the pace of profit recovery.

Aggressive Bet on "Hardware-Software + AI"

Such aggressive R&D investment in new product categories stems from Insta360's market development judgment. The imaging market's size is driven by technological and product innovation, with photography robots representing one of the future directions.

Liu revealed that six years ago, the company made a prediction: "Will there come a time when everyone has a portable 'photography robot,' like a professional photographer hired during travel group events, automatically moving through space, finding angles, and capturing those wonderful moments?"

Therefore, over the past six years, Insta360 has iteratively developed the "eyes," "torso," and "brain" of photography robots through various R&D efforts.

Insta360 clearly outlined its long-term technological direction in its financial report and shareholder letter: to create a "photography robot" with autonomous perception, automatic shooting, and intelligent editing capabilities. The company defines camera hardware as the "eyes," drones and gimbals as the "limbs," and AI algorithms as the core "brain," driving product upgrades from imaging tools to intelligent imaging assistants.

From this, it is clear that in Insta360's vision, future cameras will deeply integrate shooting and editing, with industry competition shifting from pure hardware to overall capabilities of "hardware + software + data."

Simultaneously, Insta360's technological boundaries extend into the field of embodied intelligence, collaborating with multiple embodied intelligence companies to provide panoramic data collection and visual training support for model development. Imaging devices are poised to become AI industry infrastructure, opening up new growth avenues. Self-developed chips aim to enhance product performance, optimize costs, ensure supply chain security, and strengthen foundational technological competitiveness.

Since 2017, when action camera giant GoPro declined, Insta360's development steps seem to have precisely aligned with user demand for differentiation. For example, it addressed pain points of traditional action cameras in snowboarding, diving, and other sports scenarios, such as difficult framing, shaky footage, and selfie sticks appearing in shots. Later, as trends for running and cycling selfies emerged, it launched thumb cameras to solve portability and lightweight equipment needs. With the rise of city walks, street photography, and social media check-ins, it swiftly introduced the Ace series with flip-screen functionality.

In Node Finance's view, amid the mainstream technological trend of AI, Insta360 has once again integrated technology with its positioning, targeting the photography robot segment and collaborating with embodied intelligence companies to develop related intelligent models, exploring future business directions and demonstrating a proactive approach to differentiated competition.

Overall, reviewing Insta360's financial data and strategic layout for 2025 and the first quarter of 2026, its core development path becomes clear. For example, it maintains revenue fundamentals and market share in the short term through traditional core products. Long-term growth potential is pursued through expanding business boundaries with new product categories, AI, and embodied intelligence collaborations, enabling sustainable development.

For capital markets, Insta360 is currently in a typical tech company development stage of "high growth, low profitability, and high investment." For the imaging industry, Insta360 retains the ability to maintain leading scale and sustain significant R&D investments to expand the market, embodying a long-termist capability.

"Competing with giants is an unavoidable growth path for every company. The imaging market is highly diverse in terms of user demographics, scenarios, and demands. Combined with our relentless pursuit of innovation, we have ample space for differentiated innovation in competing with giants," Liu confidently stated in his open letter.

However, Node Finance believes that in the AI era, industry development directions will converge, with every company aspiring for long-term growth targeting "hardware-software + AI" capability reserves. In this context, Insta360's challenges and the competition to break through homogeneous development will persist. Therefore, balancing profit efficiency with high-intensity investments and proving that technological innovation can still create incremental value will require time to validate.

In Node Finance's view, 2026 will be a critical window for validating Insta360's strategy. The launch timing of three major new products—gimbal cameras, wireless lavalier microphones, and drones—competition with powerful rivals, and profit performance in subsequent quarters of 2026 will directly influence capital market confidence in Insta360.

"Improvements in R&D and marketing efficiency, product design, and supply chain integration will yield significant cost savings. More importantly, the three new product categories—gimbal cameras, microphones, and drones—are expected to launch within the next year, transitioning from 'investments' to 'revenue' and boosting profits," Liu expressed confidence in the new product launches.

As Insta360 pursues its development, it will also face industry-wide price wars and marketing battles. Whether it can successfully break through, transitioning from a single imaging hardware provider to an AI-era intelligent imaging ecosystem platform, will be crucial in the next 9-12 months.

-

![]()

NVIDIA Partnership Fuels Luxshare Precision's Stock Surge to Record Highs, But Why Does Its Profit Margin Lag Behind Peers?

-

![]()

Alibaba Adjusts Prices Late at Night: Unveiling the Strategic Move

-

![]()

Insta360 Financial Report: Stellar Growth, Profit Under Strain—Where Lies the Turning Point?

-

![]()

Labor Day in the AI Era: The Dilemma of Perplexed Programmers

-

![]()

Sports Events Whistle Blows, TV Panel Prices Rise: Is the Boom Cycle Restarting?

-

![]()

From Philosophical Concept to Technological Concept, and Then to Economic Concept: The Past and Present of Token

-

![]()

When DeepSeekV4 and Meituan LongCat Simultaneously ‘Surpass One Trillion Parameters,’ What Signals Are Being Sent?

-

![]()

Chinese Home Appliances Should Not Indulge in the False Victory of 'Defeating Foreign Brands'