Sports Events Whistle Blows, TV Panel Prices Rise: Is the Boom Cycle Restarting?

05/03 2026

05/03 2026

424

424

Panel manufacturers enjoy price hike dividends, while TV brands face a cost nightmare.

Author|Jin Yingshi

Click to listen to the podcast version of this article

The FIFA World Cup in the United States, Canada, and Mexico in June is the most anticipated event for football fans worldwide this summer.

As countless eyes watch star players dominate the field, people may not realize that the screen in front of them is also stirring up dynamics in China's panel industry.

The "warm-up" from the Milan Cortina Winter Olympics has already given the market a taste of sweetness.

As early as the first quarter of this year, the sports consumption boom driven by the Winter Olympics ignited TV sales, with "January sales up 20% from December last year, and February sales up another 15% from January."

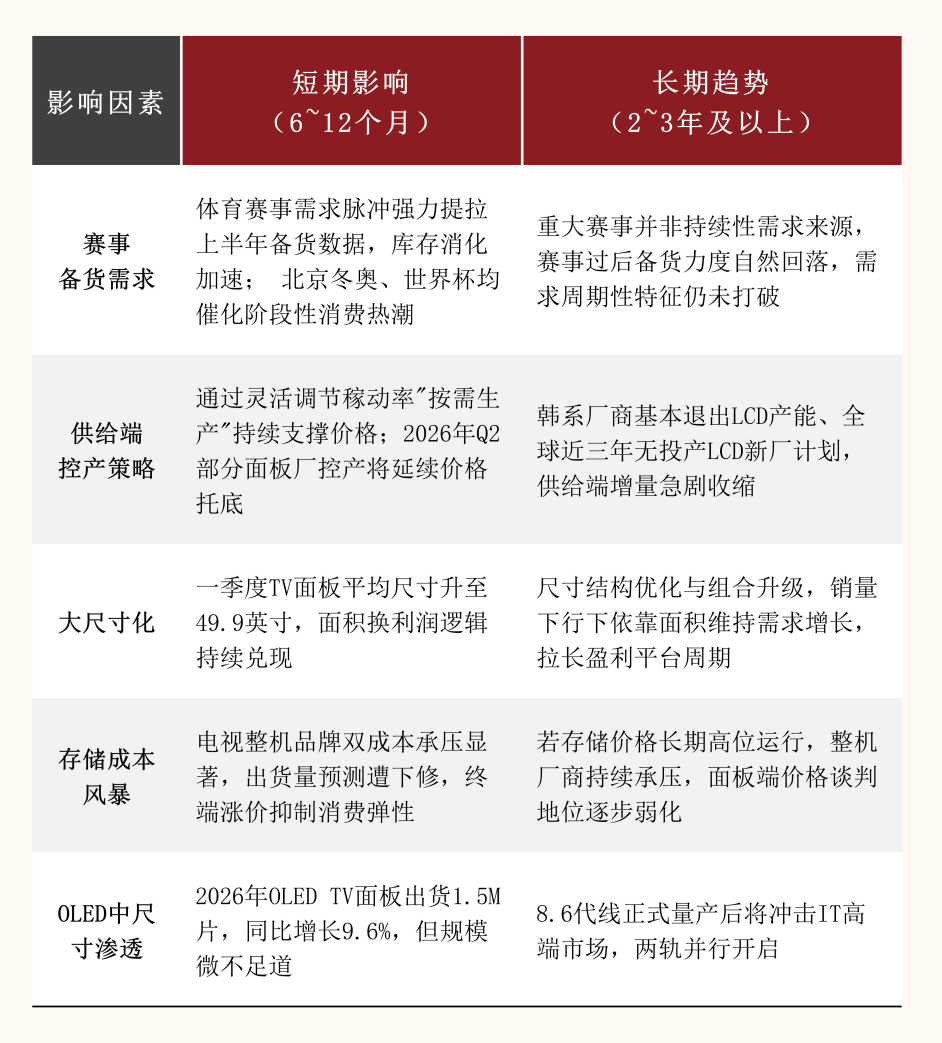

The combination of sports viewing enthusiasm and national subsidy policies has sustained a moderate rise in LCD TV panel prices during what should have been the off-season, creating a rare "off-season that doesn't feel like off-season" market trend. Following closely is the FIFA World Cup in the United States, Canada, and Mexico, starting in June, with the number of participating teams expanded to 48, matches increased to 104, and the tournament extended to 40 days. This "largest-ever" event will undoubtedly further catalyze global consumption of large-size TVs.

Panel manufacturers have already sensed the opportunity. TCL Technology's management clearly predicted in late 2025 that 2026, as a major year for sports events, "both the Winter Olympics and the FIFA World Cup in the United States, Canada, and Mexico will drive TV consumption, especially large-size TV consumption." They thus expect TV panel demand to increase by 1% to 2%, and with the trend toward larger sizes, overall demand area could grow by more than 5%.

Behind the sports event-driven momentum, the market is quietly shifting. How will the cost chain, already strained by rising memory chip prices, evolve further? What kind of performance have panel manufacturers truly delivered behind the impressive first-quarter price data?

Behind the Broad-Based Price Increases

On the surface, panel manufacturers seem to be collectively entering a "honeymoon period." According to AVC Revo data, global TV panel shipments in the first quarter of 2026 reached 63.6 million units, down 2.7% year-on-year.

Especially in terms of prices, since the beginning of 2026, LCD TV panel prices across all sizes from 32 to 65 inches have risen across the board. According to BOE's judgment in an investor conference call, three main factors are driving this price increase: consumer demand stimulated by sports events, pre-stocking driven by cost risks, and industry self-restraint in "production according to demand."

However, when we zoom in on financial report data, a more complex panel ecosystem emerges. Despite being in the same price hike trend, manufacturers' performance has diverged significantly.

BOE A (000725.SZ) reported revenue of 51.001 billion yuan in the first quarter, up 0.80% year-on-year; net profit was 1.707 billion yuan, up 5.78% year-on-year—a "moderate growth" result. Meanwhile, the company's inventory situation improved significantly, with first-quarter inventory at 25.5 billion yuan, down 8% quarter-on-quarter (based on comprehensive estimates from research institutions), indicating enhanced demand-side absorption capacity.

TCL Technology demonstrated stronger growth elasticity, with total revenue of 43.454 billion yuan, up 8.43% year-on-year; net profit was 1.556 billion yuan, up a remarkable 53.71% year-on-year. Its semiconductor display subsidiary, TCL CSOT, contributed particularly outstandingly, closely tied to its strong pricing power in the large-size TV panel segment.

Performance among Taiwan's panel giants also diverged. Innolux reported first-quarter revenue of 66.7 billion yuan, up 17.47% quarter-on-quarter, with March revenue rebounding to 25 billion yuan, up 27.82% month-on-month and 33.1% year-on-year. Chairman Hong Jinyang attributed this to customer pre-stocking and cost increase expectations, with first-half order demand exceeding expectations. In contrast, AU Optronics reported first-quarter revenue of 69.03 billion yuan, down 1.6% quarter-on-quarter and 4.3% year-on-year. Chairman Peng Shuanglang expects market conditions to clarify only in the second half of the year.

From a capital market perspective, the panel (Shenwan) index has risen 6.36% since April, with Rainbow Corporation (Chengdu rainbow Electronics) surging 44.36% and BOE A up 5.63%, showing a pattern of "leading stocks rising but with varying strength, with high-elasticity stocks leading the gains."

This pattern hints at a deeper issue: if terminal consumer demand cannot sustainably absorb price increases, the release of this round of "price hike dividends" may only be a "feast" for a few leading manufacturers.

TV Brands' "Dilemma" Amid Rising Memory Chip Prices

While panel manufacturers are enjoying "dividends" from price hikes, TV brands are experiencing a "cost nightmare."

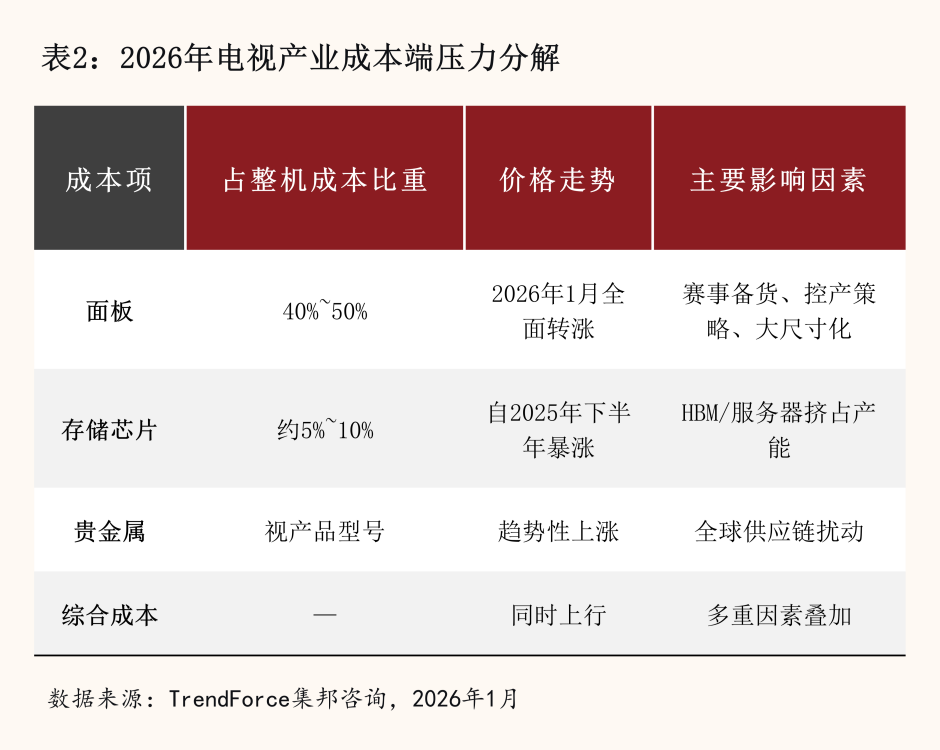

Panels account for 40% to 50% of a TV's total cost, and their price increases have directly pushed up TV production costs. Even more challenging is the "skyrocketing" price of TV memory chips, which have risen far more sharply than panels.

Take 4GB DDR4 memory, commonly used in 4K TVs, as an example. Its price has surged more than fourfold since the second half of 2025, driven by deeper structural factors: HBM (High Bandwidth Memory) and server applications have taken up a large share of DRAM production capacity, leading to severe supply shortages of traditional TV memory chips.

TV manufacturers now face a "double squeeze" from rising upstream costs and limited downstream pricing power due to highly competitive consumer markets. According to TrendForce's analysis, the TV industry faces the severe challenge of simultaneous price increases for memory chips, panels, and precious metals in 2026, leaving brands caught between "protecting profits" and "maintaining market share."

Data supports this judgment. TrendForce has further revised down its 2026 global TV shipment forecast from a previous annual decline of 0.3% to a decline of 0.6%, to about 194.81 million units, directly reflecting a darkening industry outlook.

This shift also imposes reverse constraints on the panel industry. If annual TV shipments continue to decline, terminal brands will inevitably pass on some cost pressures to panel manufacturers. After all, "no TV brand is willing to be a 'cost sponge' for panels."

How Does the "Production According to Demand" Strategy Support Prices?

Amid demand uncertainty, panel manufacturers are using a key strategy to stabilize the market: flexibly adjusting production line utilization rates.

According to CINNO data, the average utilization rate of domestic TFT-LCD panel factories was 83% in the first quarter of 2026 and is expected to drop to around 80% in the second quarter; some panel factories even plan to implement production holidays in May to control output. The core of this strategy is to use "controlled production declines" to secure "anticipated price floors." Reducing production is not just about responding to the market but about "guiding" it to create a tight balance between supply and demand.

Looking at specific timelines, the "active production cuts" during the 2026 Chinese New Year period serve as a model. The three major LCD TV panel manufacturers—BOE, TCL CSOT, and HKC—suspended operations at their back-end module factories for 5 to 10 days around the Chinese New Year, with synchronized production cuts at front-end lines. Overall LCD TV panel utilization rates are expected to drop by 3.5 percentage points quarter-on-quarter. This move perfectly aligned with the first-quarter stocking cycle, successfully pushing prices into a broad-based upward trend.

CITIC Securities judges that "panel price hikes have been the core driver of rapid improvement in LCD TV profitability over the past three years." From the industry low in 2022 to the fourth quarter of 2025, TV panel prices have risen by a cumulative 35% to 58%. By this measure, the improvement in net profit for LCD-focused leading companies' display businesses in a single quarter has exceeded 5 billion yuan. This shows that the strategy of controlling production to raise prices continues to play a role in allocating profits across the supply chain.

However, production control is a "double-edged sword." When terminal demand remains weak, brands will actively reduce orders because they cannot pass on costs. At that point, if panel manufacturers still strictly control capacity, utilization rates will fall below 80%, eroding their own scale effects and cost advantages and significantly reducing the positive impact of "production control to support prices."

Korean Manufacturers' Exit and the Global "No New Factory" Trend

Looking at the industry over a longer period, a more profound transformation emerges. The most significant long-term change in the LCD panel industry is the gradual "exit" of Korean manufacturers and the global "no new factory" trend in capacity expansion.

Samsung fully exited LCD panel manufacturing in 2022, and LG Display has been continuously downsizing its LCD business and fully shifting its Guangzhou production line to OLED after sale. This "Korean retreat, Chinese advance" industry restructuring further increased China's global panel market share to over 70% by 2025, with the top three companies—BOE, TCL CSOT, and HKC—accounting for nearly 60% market share combined.

In terms of new capacity expansion, the industry has shown rare "self-discipline." According to industry research, "LCD panel factory expansion has clearly stalled, with no new LCD panel factories or capacity expansion plans globally in 2026." This means supply-side capacity will remain largely locked in the medium term. Although Tianma's 8.6-generation line in Xiamen, which ramped up in 2025, still has some impact, the overall industry supply-demand balance remains stable within a controllable range.

This capacity structure has a decisive impact on industry trends. As CITIC Securities points out, the logic of LCD panel supply has been continuously validated, with "supply-demand fundamentals continuously improve (continuously improving)"; as industry competition turns more benign, profit release is expected to accelerate, and valuation methods for the sector will gradually shift from the traditional PB (Price-to-Book) perspective to PE (Price-to-Earnings) logic, releasing significant valuation repair momentum.

From a longer-term perspective, Chengtong Securities' "buy" rating for BOE A is directly based on supply-side changes: "Large-size LCD, as BOE's core business, now operates in a highly concentrated market." The company is leveraging its high-generation line capacity to continuously consolidate its LCD market position while developing AMOLED as a new growth driver.

Large-Size Trend: Trading Volume for Profit Through Area

If production control for price stability is the industry's "short-term spear," then the large-size trend is its "long-term shield."

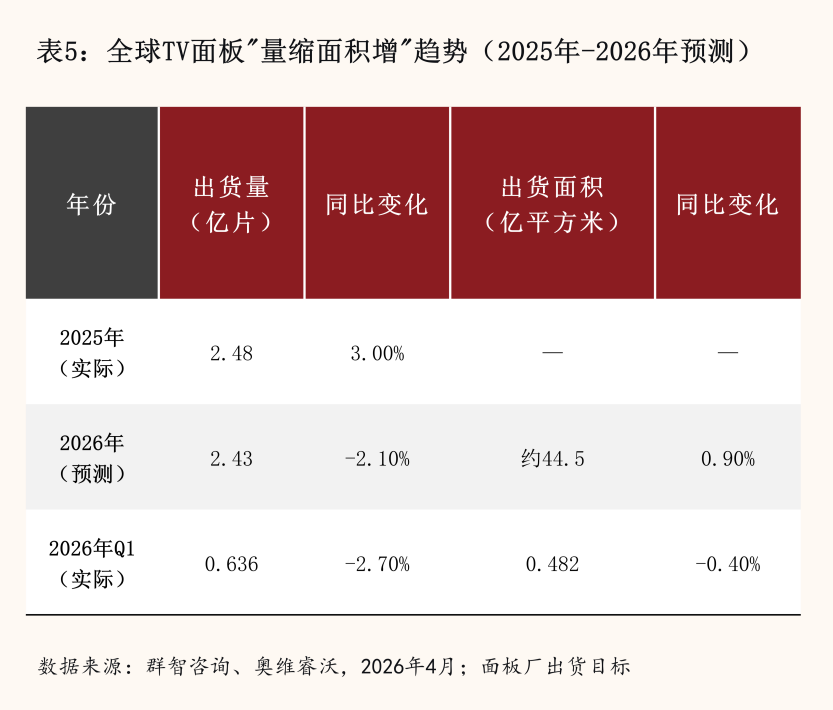

Against a backdrop of stagnant total TV shipments, "selling fewer but larger units" has become panel manufacturers' survival philosophy. According to AVC Revo data, the global average TV panel size reached 49.9 inches in the first quarter of 2026, with the large-size trend continuing to climb. Sigmaintell predicts that while TV panel shipments for the full year of 2026 are expected to decline by 2.1% year-on-year to 243 million units, shipment area could still grow by 0.9% year-on-year due to the large-size trend, achieving structural optimization of "volume decline but area stability."

BOE has also aligned with this structural trend, setting its 2026 shipment target at around 65.32 million units, with over 50% being mid-to-large-size products of 50 inches or above. TCL CSOT has even more explicitly focused its business strategy on large-size shipments and profitability improvement. Meanwhile, Sigmaintell cautions that growth in extra-large panels may slow due to weaker marginal demand and high base effects, with the industry now emphasizing "size structure optimization" over "mere size expansion."

The profit implications of this structural shift are significant. Chengtong Securities notes that in a highly concentrated competitive landscape with limited new capacity, the large-size trend has a profound impact on the panel industry by flattening past industry cycle fluctuations caused by capacity expansion. A pattern of simultaneous improvement in leading companies' profit levels and market share is taking shape. CITIC Securities calculates that leading manufacturers' LCD TV net profit margins reached over 15% during the 2025 peak sales season (Q2 and Q3), a rare profit level in the global electronics manufacturing industry.

OLED's "Mid-Size Breakthrough": Who Will Disrupt LCD's Market Share?

While focusing on LCD market achievements, we must also confront a long-standing question: Will OLED technology erode LCD's market space as "infiltrating Spring Rain (spring rain)"?

The answer hinges on "size segments."

In the large-size TV sector, OLED remains unlikely to substantially replace LCD in the short term. According to AVC Revo market monitoring, global OLED TV panel shipments reached 1.5 million units in Q1 2026, up 9.6% year-on-year, but this absolute figure represents just 2.4% of LCD TV shipments (62.1 million units). OLED TVs currently cannot match LCDs in cost, yield rates, or production scale.

The real threat emerges in the mid-size market: IT device panels are undergoing a profound "technology transition." BOE's 8.6-generation AMOLED production line successfully achieved early ignition by the end of 2025, with formal mass production expected in H2 2026. Meanwhile, Visionox and TCL CSOT are constructing OLED panel lines based on ViP and printing technologies, respectively. As OLED rapidly penetrates IT device and automotive display markets, the display panel industry is forming a new "dual-track" paradigm: OLED dominating high-end mid-size products while LCD maintains mainstream large-size shipments.

Chengtong Securities analyzes BOE's growth strategy as a "dual-drive" model combining LCD's high-barrier foundational business with AMOLED's new growth engine. This presents LCD manufacturers with strategic implications: LCD development must go beyond "excellence" to "depth," requiring sharper sensitivity in expanding technological and commercial boundaries. For example, leading players like TCL Technology are accelerating layout (deployment) of printing OLED and other new technologies to secure advantageous positioning before OLED's substitution inflection point (inflection point) arrives, ensuring multi-layered advantages in technology iteration and product roadmaps.

Conclusion

Looking back from late April 2026, the display panel industry is undergoing a complex interplay of "growth and decline, offense and defense."

However, three uncertainties remain to be decoded in this "short-term gains, long-term stability" roadmap:

First, with the Winter Olympics concluded and the FIFA World Cup opening in June, the "hot-then-cold" catalytic effect of sports events follows a clear industry pattern. Post-Olympics/World Cup, terminal brands' motivation for large-scale restocking significantly declines. If production capacity cannot be effectively controlled, panel prices may repeat the "rise-then-fall" scenario.

Second, panels account for 40-50% of total display device costs, limiting brands' ability to pass price increases to consumers. CITIC Securities assesses that "memory costs represent a relatively small portion of TV BOMs, so memory price hikes have limited impact," but if storage chips and other raw materials rise too rapidly, substitution consumption expectations will weaken, intensifying brands' bargaining demands on upstream suppliers. Currently, major home appliance brands have raised prices by 5-30% across categories, with TV price hikes controlled at 4-15% (based on aggregated public reporting of multiple brands' adjustments), insufficient to offset anticipated declines in overall shipment volumes.

Third, whether the industry's medium-to-long-term valuation can shift from cyclical pricing to PE-based pricing depends on the speed and magnitude of sustained profit release, which in turn requires maintaining dynamic cost-price balance without disruption from unforeseen events. Securities firms uniformly advocate "steady progress and value restoration" as the overarching direction, but history repeatedly shows that display industry recoveries are easily interrupted by sharp changes in either supply or demand variables.

Just as every world championship whistle signals both climax and natural conclusion, the true champions in display's "arena" will be those companies that outpace cycles by defining value through technological and scale-based negotiations.

As football fervor fades and Olympic torches extinguish, public enthusiasm for event-driven consumption will naturally stabilize. However, the supply chain optimization and pricing influence accumulated by Chinese panel manufacturers through years of global competition have solidified into industrial "hard power" capable of transcending cyclical fluctuations. This resilience may prove more enduring than any single World Cup, as a new phase of global display industry competition begins without fanfare.

References

[1] AVC Industry Chain - Global TV Panel Production, Sales, and Inventory Monthly Report, AVC Revo

[2] Global TV Panel Market Annual Outlook Report, Sigmaintell

[3] Global TV Shipment Survey January 2026 Edition, TrendForce

[4] Domestic Panel Manufacturers' Utilization Rate Monthly Tracking Report, CINNO

THE END

Copyright and Disclaimer

1. Content Copyright: Except for quoted public data, policies, and cases, all content is original. Professional data derives from authorized databases and government websites; cases are compiled from real events.

2. Image Licensing: Some images are proprietary or officially licensed, with AI-generated content; uncredited network images retain original authors' copyright and will be removed upon notification.

3. Republication Guidelines: Unauthorized reproduction is prohibited; full attribution and author credit must be preserved.

4. Liability Disclaimer: This article represents the author's commercial observations and industry commentary based on public information. Content is for reference only and does not constitute professional advice. Risks arising from use are assumed by the user. Duokong Xiangxian reserves final interpretation rights.

-

![]()

NVIDIA Partnership Fuels Luxshare Precision's Stock Surge to Record Highs, But Why Does Its Profit Margin Lag Behind Peers?

-

![]()

Alibaba Adjusts Prices Late at Night: Unveiling the Strategic Move

-

![]()

Insta360 Financial Report: Stellar Growth, Profit Under Strain—Where Lies the Turning Point?

-

![]()

Labor Day in the AI Era: The Dilemma of Perplexed Programmers

-

![]()

Sports Events Whistle Blows, TV Panel Prices Rise: Is the Boom Cycle Restarting?

-

![]()

From Philosophical Concept to Technological Concept, and Then to Economic Concept: The Past and Present of Token

-

![]()

When DeepSeekV4 and Meituan LongCat Simultaneously ‘Surpass One Trillion Parameters,’ What Signals Are Being Sent?

-

![]()

Chinese Home Appliances Should Not Indulge in the False Victory of 'Defeating Foreign Brands'