NVIDIA Partnership Fuels Luxshare Precision's Stock Surge to Record Highs, But Why Does Its Profit Margin Lag Behind Peers?

05/03 2026

05/03 2026

450

450

Produced by | Bullet Finance

Art Design | Qianqian

Reviewed by | Songwen

On April 27, Luxshare Precision's stock price quickly climbed to RMB 72.60 per share after the market opened, reaching a new all-time high. The stock price fluctuated at a high level throughout the day and eventually closed at RMB 71.97 per share, up 9.05%, with a total market capitalization reaching RMB 524.4 billion.

From April 1 to April 28, the company's stock price has surged by over 41%, making it one of the most closely watched tech stocks in the A-share market.

The immediate catalyst for this round of stock price increases was a research report released on April 27 by analyst Ming-Chi Kuo of TF International Securities. Kuo stated in the report that OpenAI plans to develop its own smartphones and is collaborating with MediaTek and Qualcomm to develop mobile processors. Luxshare Precision is the exclusive system co-design (collaborative design) and manufacturer, with mass production expected in 2028.

Regarding this rumor, "Bullet Finance" has sent an interview request to Luxshare Precision for verification but has not yet received a response as of the time of publication.

OpenAI CEO Sam Altman previously posted, "It feels like a good time to seriously rethink how we design operating systems and user interfaces," which the market interpreted as an indirect response to plans for AI-powered smartphones.

If this rumor proves true, Luxshare Precision will upgrade from a traditional consumer electronics contract manufacturer to the core partner for the world's first AI smartphone, gaining a first-mover advantage in the AI terminal hardware wave.

Beyond the short-term catalyst of the OpenAI rumor, the core logic supporting Luxshare Precision's long-term stock price strength lies in its solid financial performance and the growth potential brought by its "pursuit of light" business. So, setting aside market enthusiasm, what is the company's actual operational performance?

1. Market Attention Driven by the "Pursuit of Light"

Financial report data shows that in 2025, Luxshare Precision achieved total revenue of RMB 332.344 billion, up 23.64% year-on-year; net profit attributable to shareholders was RMB 16.6 billion, up 24.20% year-on-year. Revenue and net profit growth remained synchronized, both reaching new historical highs.

On April 28, Luxshare Precision released its 2026 first-half earnings forecast, projecting net profit attributable to shareholders of RMB 7.84 billion to RMB 8.11 billion for the first half of 2026, up 18% to 22% year-on-year.

Against the backdrop of overall pressure in the consumer electronics industry, these results are particularly impressive.

Currently, Luxshare Precision has three main businesses: consumer electronics, communications and data centers, and automotive electronics. Against the backdrop of the AI infrastructure boom, investors are clearly more focused on the communications and data center segment.

In the communications and data center field, the company focuses on core components and complete machine assembly (complete machine assembly) for communication base stations and AI servers, covering key areas such as high-speed electrical connections, optical connections, thermal management, power management, server systems, and 4G/5G RF antennas.

What truly ignited market enthusiasm was the company's recent Intensive release (intensive release) of signals about its "pursuit of light."

The company stated on an interactive platform that it continues to deepen its research into data center optical interconnect technologies such as CPO and NPO. Subsequently, in its latest investor relations activity record, the company revealed that at the OFC exhibition, it was the only manufacturer to demonstrate a Demo of an XPO switch-level interconnect and thermal dissipation integration solution.

It further stated that the company began its layout (layout) with relatively near-term NPO technology and has made good progress, with clear opportunities for implementation. In the 800G and 1.6T optical module segments, progress with domestic and international clients has been smooth, and these areas are expected to become one of the core drivers of future growth.

(Image / Luxshare Precision Announcement)

A series of business developments, combined with the high growth prospects of the AI computing power sector, have made Luxshare Precision a key focus for institutional investors.

According to a report by China Securities Journal, as of April 20, 291 listed companies had been visited by institutions in April. Luxshare Precision ranked first, with 279 institutional visits.

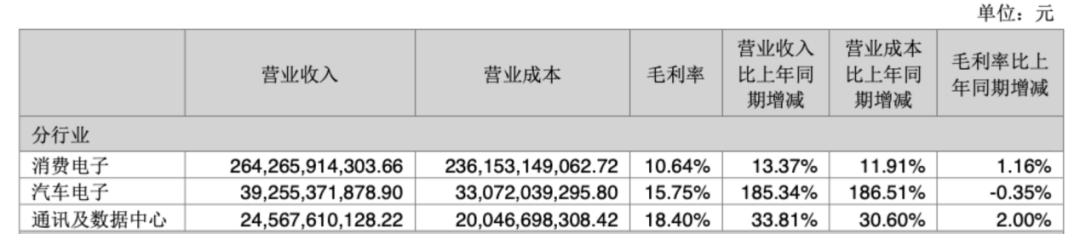

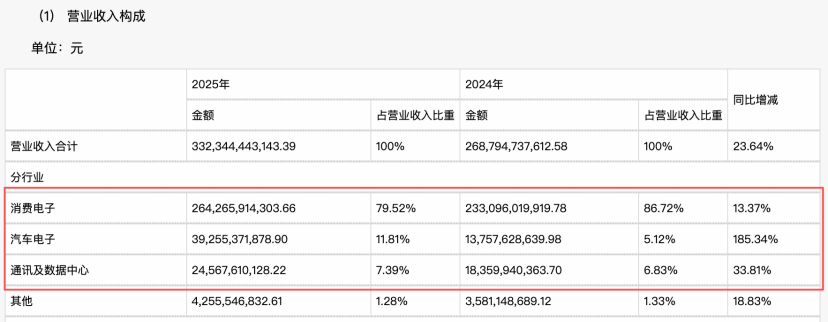

So, how does Luxshare Precision's business in this area perform specifically? Data shows that in 2025, its communications and data center business achieved revenue of RMB 24.568 billion, up 33.81% year-on-year, with a gross margin of 18.4%, significantly higher than the company's overall gross margin of 11.9%, becoming a key driver of improved profitability.

(Image / Luxshare Precision Financial Report)

It is worth mentioning that despite the rapid rise of new businesses, consumer electronics remain the core stabilizer for Luxshare Precision. In 2025, the company's consumer electronics business achieved revenue of RMB 264.266 billion, up 13.37% year-on-year, with its revenue share declining to 79.52%, down about 7 percentage points from 2024, indicating a weakening reliance on a single business.

(Image / Luxshare Precision Financial Report)

2. Significant Differences in Gross Margins Compared to Industry Peers

How does Luxshare Precision's "light" business perform when compared to the broader industry?

In reality, Luxshare Precision's optical business is closer to optical communications. Optical communications refer to the use of lasers as information carriers and optical fibers as transmission channels, forming a vast system that supports high-speed data transmission such as AI computing power. The market's highest expectations lie in optical modules, which are key devices responsible for the bidirectional conversion of electrical and optical signals in optical communication systems. They are the "conversion hub" closest to orders and with high cost proportions within the system.

In addition to optical modules, Luxshare Precision is also involved in NPO and CPO "packaging technologies" and supplies supporting products such as high-speed copper cables, power management, and liquid cooling solutions. In this model, Luxshare Precision primarily adopts a joint development (JDM) or customized design (ODM) approach with major clients, where product specifications and technical routes are mainly driven by clients, and the company leverages its advantages in precision manufacturing and large-scale delivery.

Its positioning is to provide customers with integrated "copper-optical-electrical-thermal" solutions, with barriers more be reflected in (reflected) in manufacturing than in technology.

(Image / Luxshare Precision Financial Report)

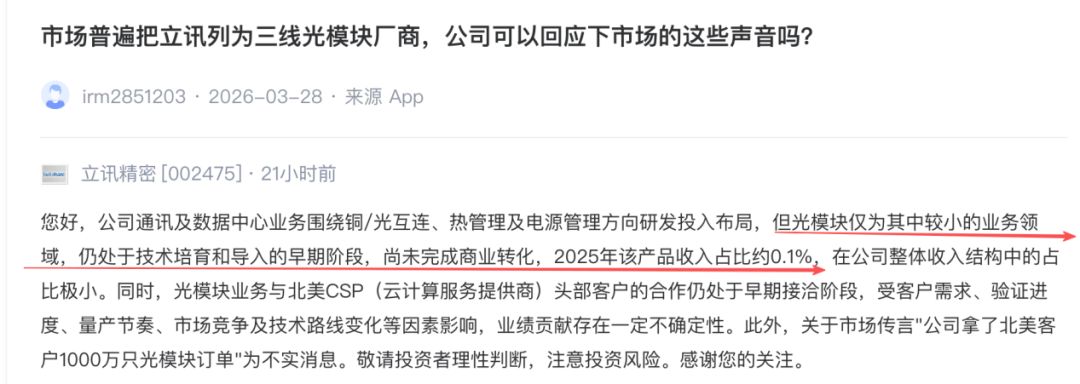

According to the latest response from Luxshare Precision's board secretary on April 28, the company's communications and data center business focuses on R&D and layout (layout) in copper/optical interconnects, thermal management, and power management. Optical modules are only a smaller part of this business and remain in the early stages of technology development and adoption, with no commercial conversion yet achieved. In 2025, revenue from this product accounted for about 0.1% of the company's total revenue, a negligible share in the overall revenue structure.

(Image / Shenzhen Stock Exchange Interactive Easy)

Currently, the core players in the global optical module market include companies such as InnoLight, Eoptolink, and Tianfu Communication. Among them, InnoLight and Eoptolink are absolute leaders in the global optical module industry, with a highly focused main business—in 2025, optical module business revenue accounted for over 97% of InnoLight's total revenue, while nearly 100% of Eoptolink's revenue came from optical interconnect products.

Both InnoLight and Eoptolink adopt a "self-developed design + branded sales" model, holding product definition rights and core pricing power. It is precisely this difference in positioning that directly leads to differences in profitability between Luxshare Precision and its industry peers.

In 2025, the overall gross margin of Luxshare Precision's communications and data center business was 18.4%, while InnoLight's optical module business gross margin was 42.61% and Eoptolink's optical interconnect business gross margin was as high as 47.81%, showing a significant gap.

This indicates that Luxshare Precision's optical module business is still primarily focused on manufacturing and system integration, with core technologies and high-value-added segments mainly controlled by professional optical module manufacturers and upstream chip companies.

3. Can It Break Free from Path Dependency?

The business model in the optical module segment is essentially consistent with the consumer electronics business that Luxshare Precision relied on to grow. Starting from single components and gradually expanding to multi-category full-stack solutions, this cooperative approach closely resembles the company's "routine" of entering Apple's supply chain with connectors and later securing orders for complete device assembly.

While this approach helps it quickly enter the market with the help of major clients, it also sow (sows) some underlying concerns.

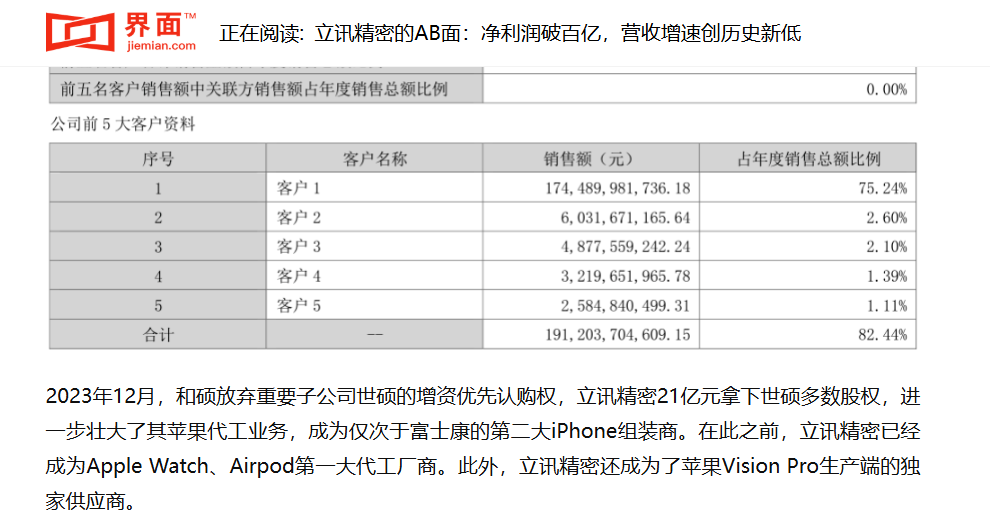

For a long time, its deep bind (binding) with top giant Apple has been an advantage for Luxshare Precision's scale expansion but has also become a shackle limiting its profitability. Financial report data shows that in 2025, revenue from its largest client still accounted for as high as 56.68% of the total. Although this is a significant decline from the previous two years, having over half of its revenue concentrated in a single top client remains extremely high in the manufacturing industry.

(Image / Luxshare Precision Financial Report)

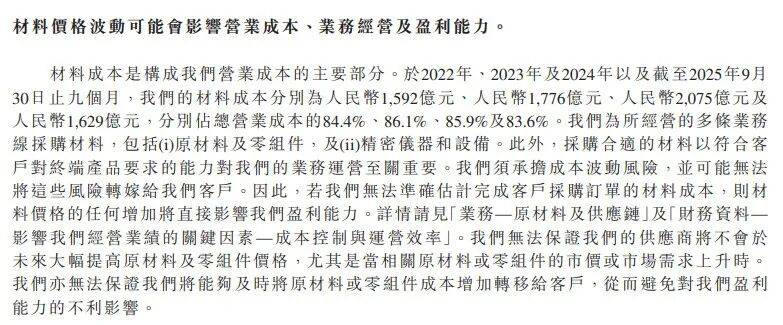

Positioned in the middle of the "upstream core components monopolized, downstream terminal giants dominate the rules" industrial chain, Luxshare Precision has long been in a weak bargaining position.

According to its prospectus submitted to the Hong Kong Stock Exchange, from 2022 to the first nine months of 2025, material costs consistently accounted for about 85% of operating costs—a typical cost structure for contract manufacturers. Core raw materials such as upstream chips and precision components mainly come from global giants, leaving little room for bargaining. Meanwhile, downstream top clients control product definitions, technical routes, and procurement rules, naturally holding stronger bargaining power.

(Image / Luxshare Precision Prospectus)

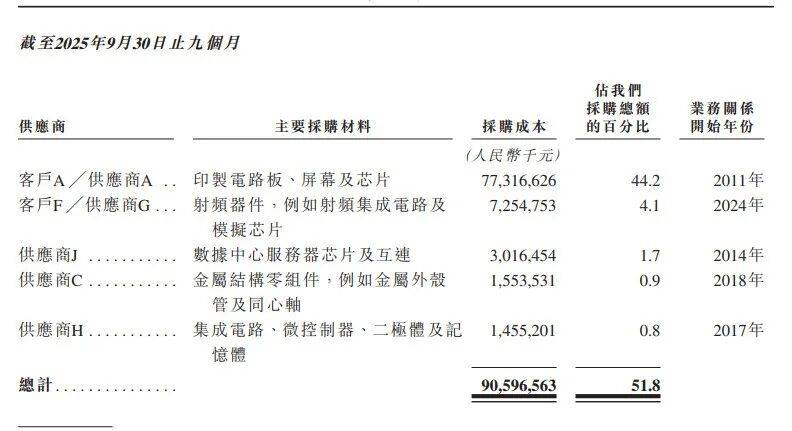

It is worth mentioning that to control the entire procurement process as well as the cost and quality of raw materials, some of the company's core clients require Luxshare Precision to purchase certain core components from themselves or their designated suppliers. The prospectus shows that in the first three quarters of 2025, the company's largest client A overlapped with supplier A, and client F overlapped with supplier G, resulting in the company's bargaining power being controlled by core clients in both upstream and downstream.

(Image / Luxshare Precision Prospectus)

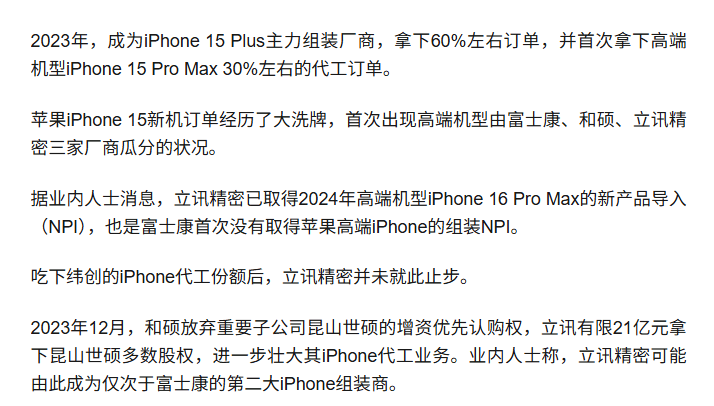

According to media reports, since entering the iPhone assembly business in 2020, Luxshare Precision has continuously increased its share, securing assembly orders for the high-end iPhone 15 Pro Max model for the first time in 2023 and becoming the second-largest contract manufacturer after Foxconn in the same year. To consolidate its position in Apple's supply chain, Luxshare Precision has continuously expanded production capacity and optimized its cost structure. Industry consensus suggests that it has adopted a more competitive pricing strategy to secure more orders and gain market entry.

(Image / Media Reports)

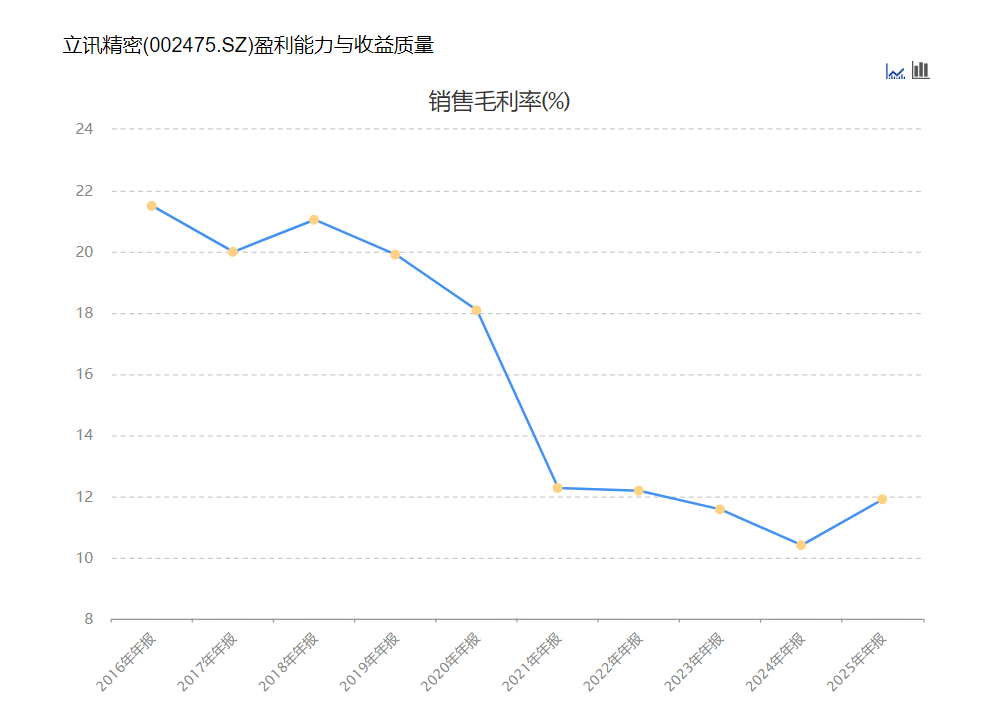

The company's own gross margin trends also reflect this. In 2018, Luxshare Precision's overall gross margin was 21.05%, declining to 12.28% in 2021, further slipping to 10.41% in 2024, and maintaining at 11.92% in 2025.

(Image / East Money)

Now, the market's highly anticipated new optical module business seems to be following a similar logic.

Research content from industrial chain surveys conducted by leading securities firms such as China Merchants Securities and CITIC Construction Investment in the first quarter of 2026 shows that NVIDIA is a core client for Luxshare Precision's communications and data center business.

However, unlike self-research-driven professional optical module manufacturers such as InnoLight and Eoptolink, Luxshare Precision still relies on joint development, customized contract manufacturing, and system integration delivery as its core model in NVIDIA's supply chain.

Product specifications, technical standards, interface protocols, and even iteration rhythms are primarily driven by downstream major clients, with the company mainly responsible for large-scale production, multi-category integration, and delivery implementation. Its core technological barriers are concentrated in manufacturing and integration rather than upstream core areas such as optical chips and high-speed signal processing, with product pricing power and final solution definition rights mainly held by downstream major clients.

Additionally, it is worth noting that with the explosion in AI computing power demand, the high-speed optical module industry has already entered a phase of rapid capacity expansion and accelerated product iteration. According to China Economic Times, even for core components like 800G high-speed optical modules, market prices have dropped from $800 in 2024 to $350 since mass production began.

Meanwhile, 1.6T products remain priced between $1,200 and $2,000 due to supply bottlenecks in core components such as optical chips. Industry consensus expects that as 1.6T capacity gradually releases in the second half of 2026, prices will also enter a downward trajectory.

For professional optical module companies with core optical chips, self-developed architectures, and proprietary brands, they can offset selling price declines through technological iteration, yield optimization, and self-developed cost reductions to maintain stable high margins.

However, for manufacturers like Luxshare Precision, which focus on customized contract manufacturing and supporting integration, upstream core material costs are beyond their control, while downstream product selling prices decline in tandem with industry and major client procurement systems, leaving less room for technological premiums and pricing buffers.

Undeniably, the cooperation model of bind (binding) with global top tech giants allows Luxshare Precision to quickly enter high-growth sectors, unlock new growth spaces, and rapidly deploy its optical module and AI computing power businesses in a short time.

However, in the long run, a development model that relies on custom OEM for major clients and lacks pricing power over core technologies will struggle to escape the fate of operating below the industry's gross profit margin.

While the market is immersed in the valuation speculation and stock price surge driven by the AI optics business, whether Luxshare Precision can break free from its inherent path dependence in new markets, move beyond its pure manufacturing support role, and establish its own technological barriers and product influence will directly determine the ceiling for its long-term growth.

*The featured image in the article is from: Shitu.com, based on the VRF protocol.

-

![]()

NVIDIA Partnership Fuels Luxshare Precision's Stock Surge to Record Highs, But Why Does Its Profit Margin Lag Behind Peers?

-

![]()

Alibaba Adjusts Prices Late at Night: Unveiling the Strategic Move

-

![]()

Insta360 Financial Report: Stellar Growth, Profit Under Strain—Where Lies the Turning Point?

-

![]()

Labor Day in the AI Era: The Dilemma of Perplexed Programmers

-

![]()

Sports Events Whistle Blows, TV Panel Prices Rise: Is the Boom Cycle Restarting?

-

![]()

From Philosophical Concept to Technological Concept, and Then to Economic Concept: The Past and Present of Token

-

![]()

When DeepSeekV4 and Meituan LongCat Simultaneously ‘Surpass One Trillion Parameters,’ What Signals Are Being Sent?

-

![]()

Chinese Home Appliances Should Not Indulge in the False Victory of 'Defeating Foreign Brands'