Apple’s Performance and Market Value Soar to New Heights: How Did It Get There?

05/12 2026

05/12 2026

338

338

Introduction: Under Tim Cook’s leadership, Apple has evolved from a 'hardware seller' to a 'user operator.'

Author: Li Ping | Produced by: Leestone Business Review

1

The Strongest Quarterly Report in History

'We’ve just had the best March quarter (second fiscal quarter) ever, with double-digit growth in every region,' Tim Cook announced at Apple’s recent financial results briefing.

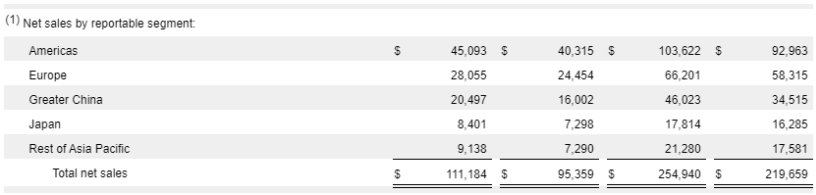

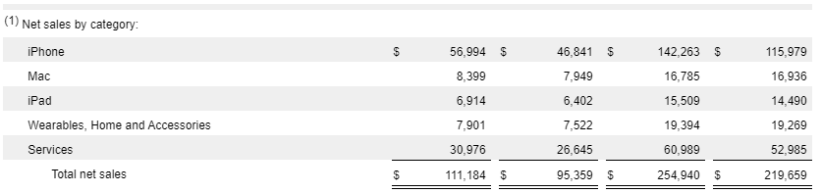

According to the financial data, in the second quarter of FY2026 (ending March 28, 2026), Apple’s total revenue reached $111.184 billion, marking a 17% year-on-year increase. Net profit stood at $29.6 billion, up 19.4% year-on-year. Diluted earnings per share were $2.01, a 22% year-on-year rise, all surpassing market expectations and setting new records for the second quarter in previous years.

In terms of business segments, Apple’s hardware business generated total revenue of $81.206 billion, a 16.7% year-on-year increase. Driven by strong demand for the iPhone 17 series, iPhone revenue reached $56.99 billion, up 21.7% year-on-year, becoming the core driver of the company’s overall hardware growth. The strategy of offering 'more for the same price' was pivotal to the global success of the iPhone 17 series. Reportedly, the new iPhone 17 series phones upgraded storage to a minimum of 256G, while maintaining the price at 5,999 yuan. Additionally, they qualified for government subsidies in China.

According to IDC data, in the first quarter of 2026, global smartphone shipments were 289.7 million units, a 4.1% year-on-year decline, breaking a ten-quarter growth streak since mid-2023, primarily due to shortages and cost increases of DRAM and NAND storage chips. Among them, Apple’s global market share was 21.1%, a 1.5 percentage point year-on-year increase. Regionally, smartphone shipments in the Chinese market in the first quarter were approximately 69.01 million units, a 3.3% year-on-year decrease. Among them, Apple’s smartphone shipments reached 13.1 million units, a 33.3% year-on-year increase, ranking first in growth.

Beyond the strong sales of the iPhone series, Apple’s other hardware products also experienced positive growth. Mac business revenue reached $8.4 billion, a 6% year-on-year increase, primarily due to the concentrated release of the MacBook Air, MacBook Pro, and the more affordable MacBook Neo during this fiscal quarter. iPad business revenue reached $6.91 billion this quarter, an 8% year-on-year increase, mainly due to increased sales of the M5 Pro and A16 models.

Compared to traditional hardware businesses, Apple’s software services performed even more impressively. Financial results showed that Apple’s software services revenue reached $31 billion this quarter, a 16% year-on-year increase. This marks the second consecutive quarter that Apple’s services revenue has exceeded the $30 billion mark. In essence, even without considering its vast hardware portfolio, Apple has become one of the world’s largest software companies.

Based on the strong sales of the iPhone 17 series, Apple restored double-digit growth in the Chinese market, alleviating external concerns about a 'decline in the Chinese market' to some extent. Data shows that Apple’s revenue in Greater China reached $20.497 billion this quarter, a 28.09% year-on-year increase, setting a record for the second fiscal quarter in previous years and far exceeding market expectations.

In addition to the Chinese market, Apple’s sales performance in other regions was also impressive. Revenue in the Americas region was $45.093 billion, an 11.85% year-on-year increase, accounting for more than 40% of total revenue. The United States remains Apple’s largest market. Revenue in the Europe region reached $28.055 billion, a 15% year-on-year increase, accounting for 25.2%, reflecting the popularity of the iPhone 17 series in the European market. Additionally, the year-on-year growth rates in other Asia-Pacific regions and Japan were 25% and 15%, respectively.

Based on the strong financial performance, Apple’s stock price rose 3.24% the day after the financial report was released, and its market value surged by over $100 billion overnight. As of the close of the most recent trading day, Apple’s total market value stood at $4.3 trillion, setting another all-time high.

2

Gross Margin Reaches New All-Time High

In fact, since the second half of 2025, the surge in demand for AI, data centers, and other applications has led to an expanding market for storage products, with price increases for memory modules and hard drives sweeping the entire market. As the global shortage of memory chips continues to spread, the consumer electronics industry, including smartphones and PCs, has been significantly impacted. Against this backdrop, Apple’s performance in this fiscal quarter was not well-regarded by the outside world, and the company’s stock price began to decline in December 2025, losing its $4 trillion market value.

However, external concerns about Apple’s cost side did not materialize. Financial results showed that Apple’s gross margin reached an all-time high of 49.3% this quarter, a 2.2 percentage point year-on-year increase. Among them, the gross margin of the hardware business was 38.7%, a 2.8 percentage point year-on-year increase, and the gross margin of the software business rose to 76.7%, a 1.4 percentage point year-on-year increase.

It is evident that despite the pressure of rising memory costs across the entire consumer electronics industry, Apple’s hardware business gross margin has increased instead of decreased, mainly due to economies of scale and product mix optimization. On the one hand, the significant increase in iPhone shipments has brought about strong economies of scale, effectively diluting unit fixed costs. On the other hand, Apple’s products are primarily targeted at the mid-to-high-end market, and the impact of rising storage costs is relatively smaller compared to competitors. Additionally, the increased proportion of high-margin products like the Pro series has also contributed to the company’s gross margin improvement.

Furthermore, Apple’s strong supply chain management advantages are also a key factor in its gross margin improvement against the trend. Under Tim Cook’s leadership, Apple has successfully implemented a global supply chain layout, dispersing the production of core components to the most cost-effective regions and using stringent process management to minimize inventory cycles, greatly reducing the occupation of company funds by inventory. At the same time, Cook has pushed Apple to sign long-term exclusive agreements with core suppliers and even prepay funds to lock in upstream production capacity, which is also a key factor in Apple’s hardware product gross margin being 'insensitive' to storage price increases this fiscal quarter.

However, the potential impact of the escalating memory price increase on Apple’s future cost side cannot be ignored. In this regard, Cook himself admitted during Apple’s FY2026 second-quarter financial results conference call that the reason Apple was able to maintain high profit margins in the previous two quarters (ending December 2025 and March 2026) was mainly due to significant stockpiling in advance, locking in lower memory costs. However, starting in June, this protection will gradually lose effectiveness, and the stockpiled DRAM and NAND flash memory inventories will begin to be depleted, forcing Apple to purchase new components at the current soaring market prices.

As usual, Apple will prepare for the mass production and release of the iPhone 18 series in the second half of this year, which coincides with the point where its memory inventory runs out. Prior to this, there have been rumors in the market that Apple will keep the pricing of the iPhone 18 unchanged. However, given the shortage of memory chips, the sustainability of this strategy is clearly questionable.

Some analysts also believe that based on the strong market performance of the iPhone 17 series, Apple may make significant adjustments to its product release schedule, with the most notable being a significant extension of the production cycle of the iPhone 17 standard model, while the iPhone 18 standard model originally scheduled for release this autumn may be absent.

3

Services: The 'Money Printing Machine' in Full Swing

In addition to supply chain advantages, the increase in the revenue share of service software is also a key factor in the continuous improvement of Apple’s gross margin, which is also attributed to Cook’s leadership. Since 2014, Cook has successfully transformed the services business into Apple’s second growth engine through a series of forward-looking strategic layouts.

In fact, because Steve Jobs preferred that 'good products should be bought outright' and opposed subscription-based user binding, during Jobs’ era, the Apple Store was only a supplement to hardware, with its main goal being to enhance the iOS ecosystem and make the iPhone more powerful and irreplaceable, rather than to generate major revenue from app distribution.

Under Cook’s leadership, Apple has successfully deeply integrated services such as Apple Music, iCloud, and AppleCare, thereby constructing a complete 'User Lifetime Value (LTV) System'. Based on this strategy, users continue to pay for music subscriptions, cloud storage, in-app purchases, etc., after purchasing hardware, forming a new dual-drive business model of 'hardware driving services, services feeding back into hardware'.

Thus, Apple has transformed the originally low-frequency hardware transactions into high-frequency, high-stickiness, and high-margin continuous service revenue through ecological synergy, achieving a commercial transformation from 'selling devices' to 'operating users'.

Data shows that in FY2015, Apple’s services business revenue was less than $20 billion. In FY2025, Apple’s services business revenue reached $109.16 billion, surpassing the $100 billion mark for the first time, accounting for approximately 26.2% of the company’s total revenue. Additionally, from a gross margin perspective, Apple’s services gross margin has consistently been above 75%, more than double that of its hardware business.

In the second quarter of FY2026, Apple’s software services revenue reached $31 billion, a 16% year-on-year increase, accounting for 28% of revenue, far exceeding market expectations. At the same time, with the continuous increase in Apple’s global active device base, the gross margin of Apple’s services business rose to 76.7%, setting another all-time high. From the perspective of gross profit contribution, although Apple’s software services revenue accounts for less than 30%, it contributes 43% of Apple’s gross margin, making the services business the 'ballast' of Apple’s profit side.

It is worth mentioning that Apple is currently actively expanding its advertising business within its services ecosystem. It is reported that Apple has added advertising slots to its App Store search results and plans to launch ads focusing on local businesses in Apple Maps in the United States and Canada this summer. Due to the extremely high profit margins of the advertising business, the increase in its revenue share is expected to continue to drive the gross margin of Apple’s entire services sector, meaning that Apple’s services business will continue to operate in 'money printing machine' mode.

In April of this year, Apple officially announced a leadership transition. Current CEO Tim Cook will step down as CEO on September 1 and become Executive Chairman, with John Ternus, Senior Vice President of Hardware Engineering, succeeding him as Apple’s CEO. This marks the official end of Tim Cook’s 15-year tenure at the helm of Apple.

Overall, Apple not only achieved 'full bloom' in its hardware and software businesses in the second fiscal quarter but also achieved double-digit growth in all major markets, indicating that the company’s sales breakthrough was not reliant on a single market or product but on global demand resonance. For Cook, who is about to step down as CEO, this is undoubtedly a nearly perfect report card.

-

Ali and DeepSeek: Mere Neighbors in the AI Landscape of Hangzhou

-

![]()

World Models: The Top Technical Narrative in Embodied AI

-

Kunlunxin, Backed by Baidu, Aims for Dual A+H Share Listing Amid RMB21 Billion Valuation Challenges

-

![]()

Apple’s Performance and Market Value Soar to New Heights: How Did It Get There?

-

![]()

Exploring the Distinctions Between Alibaba and ByteDance in AI-Driven E-commerce: The Comprehensive Integration of Qianwen with Taobao

-

![]()

Qianwen Revolutionizes Taobao: Alibaba's Bold Self-Transformation

-

![]()

What’s the Real Story? China Leads in 5G Patents but Pays More in Royalties!

-

![]()

8 Auto Companies Unanimously Deny 'Summons for Talks' Rumors, but OTA Battery Locking is Real