Kunlunxin's IPO: Is Baidu's Pricing Dilemma Lurking Beneath?

05/13 2026

05/13 2026

572

572

Written by Ning Chengque

Source: Bowang Finance

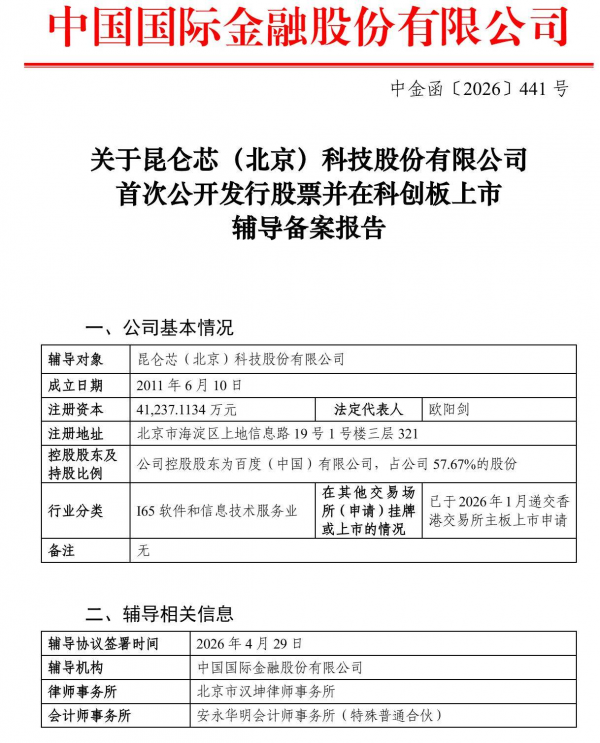

In 2026, a notification on the official website of the China Securities Regulatory Commission (CSRC) brought Baidu's 15-year capital strategy into the limelight. Kunlunxin (Beijing) Technology Co., Ltd. officially embarked on IPO coaching for listing on the STAR Market, with CICC serving as its advisor. Just four months prior, this AI chip company had submitted an application for a mainboard listing to the Hong Kong Stock Exchange through a confidential filing.

Li Yanhong's third listed entity is on the horizon, pursuing a dual-track "A+H" listing strategy.

Since rumors of Kunlunxin's listing began circulating in late 2025, Baidu's market value has soared by tens of billions of Hong Kong dollars, with its stock price hitting a new peak since 2023.

However, amidst this IPO, valued at over 21 billion yuan, a stark contradiction arises: According to market sources, Kunlunxin, with approximately 2 billion yuan in revenue in 2024, is valued at just 21 billion yuan. In contrast, Cambricon, with comparable shipment volumes, once saw its market value soar past 800 billion yuan.

A vast chasm exists between the two. Is Li Yanhong's third IPO truly worth this valuation?

01

"Born into Affluence": Growth Propelled by the AI Computing Boom

Kunlunxin's journey began in 2011.

At that time, a modest FPGA AI accelerator project was quietly initiated within Baidu. Over the years, Baidu's FPGA deployment scale expanded continuously. At the international top-tier chip conference Hot Chips, Baidu unveiled its self-developed Kunlun XPU architecture for the first time.

2018 marked a pivotal turning point. That year, China's AI industry entered its first computing power boom cycle, with the GPU server market experiencing explosive growth. The escalation of Sino-U.S. tech competition propelled "domestic substitution" to the forefront of the industry. Baidu's "Kunlun 1" chip officially debuted in the same year, utilizing Samsung's 14nm process and delivering 260 TOPS of computing power.

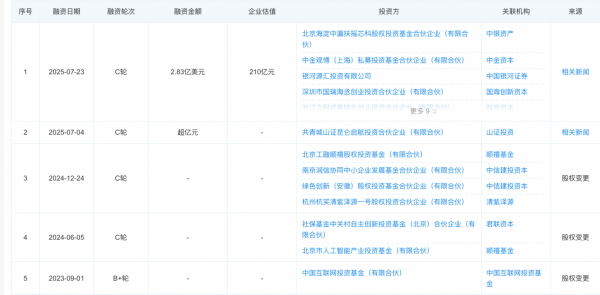

Subsequently, the entire domestic AI chip industry began to flourish. Alibaba's T-Head was officially established, while startups like Biren and Moore Threads emerged as the "Four Little Dragons of GPUs." In 2021, Baidu formally spun off Kunlunxin as an independent entity, with chief chip architect Ouyang Jian assuming the role of CEO and an initial valuation of 13 billion yuan.

Financial data underscores Kunlunxin's confidence. According to market sources, Kunlunxin generated approximately 2 billion yuan in revenue in 2024, with a net loss of around 200 million yuan. Its full-year revenue for 2025 is expected to surpass 3.5 billion yuan, potentially achieving break-even, with over half of its income derived from clients outside Baidu.

Multiple brokerage research reports project revenue could reach 6.5 to 8.3 billion yuan in 2026. In terms of shipment volume, IDC's latest data shows that Kunlunxin shipped 116,000 AI accelerator cards in 2025, ranking third domestically alongside Cambricon.

These figures indicate that Kunlunxin has successfully navigated the entire process from design and tape-out to mass production, with its product stability and reliability validated by the market, securing its position in the industry.

Breakthroughs in external orders are even more significant. In China Mobile's AI server procurement for 2025-2026, Kunlunxin secured 70% to 100% of the shares in the "CUDA-like ecosystem" segment, ranking first overall with orders worth billions of yuan.

Ouyang Jian revealed in an interview that the company has engaged with nearly 100 clients, including China Merchants Bank, China Southern Power Grid, Geely Automobile, and Vivo, with delivery scales ranging from dozens to tens of thousands of cards.

From being a "Baidu internal supplier" to generating over half of its revenue externally, Kunlunxin has achieved a rare feat among domestic AI chip companies in terms of revenue generation.

02

A 30-Fold Valuation Disparity: Where Does the Issue Lie?

However, in stark contrast to its revenue scale, Kunlunxin's valuation continues to lag behind its peers.

Cambricon's market value stood at just 25.7 billion yuan during its initial public offering in 2020, but its pure and scarce AI chip concept quickly attracted significant passive capital from Sci-Tech Innovation Board (STAR Market) and chip ETFs.

Coupled with a performance turnaround driven by the AI computing boom—Cambricon reported 6.497 billion yuan in revenue in 2025, a year-on-year increase of 453.21%, with a net profit of 2.059 billion yuan—its stock price once surged to 1,966 yuan, with a market value exceeding 800 billion yuan.

Performance continued to accelerate in the first quarter of 2026, with revenue reaching 2.885 billion yuan, a year-on-year increase of 159.56%, and a net profit of 1.013 billion yuan. Single-quarter performance approached half of the full-year total for 2025, making high growth throughout the year highly probable.

In contrast, Kunlunxin's latest funding round, completed in July 2025, valued the company at only 21 billion yuan post-investment, a fraction of Cambricon's market value at the time.

With comparable shipment volumes and rapidly narrowing revenue gaps, where does this disparity originate?

The disappearance of scarcity is an unavoidable and harsh reality.

Analysts point out that the valuation premium enjoyed by Cambricon stems from its long-standing "uniqueness"—for an extended period, Cambricon was the only pure AI chip stock on the A-share market, attracting significant passive allocation from numerous ETFs. Holdings from ETFs alone supported its market value surpassing 100 billion yuan despite its unprofitable status.

Today, the A-share market boasts multiple AI chip listed companies, including Moore Threads and MetaX, while Biren Technology is pursuing a listing in Hong Kong. Kunlunxin no longer holds a first-mover advantage, making it virtually impossible to replicate Cambricon's legendary valuation path.

A deeper constraint lies in the capital market's established pricing model for "Baidu-affiliated" enterprises.

Tianyancha data reveals that Baidu remains the majority shareholder of Kunlunxin with a 57.67% stake following its IPO. This ownership structure appears relatively closed within the chip industry, which is characterized by high barriers to entry and heavy investment, and relies on venture capital mechanisms to attract diverse local funding and industrial resources.

The market clearly understands the valuation logic of "following Baidu's lead." However, as the narrative of domestic substitution returns to rationality, an AI chip company backed by a major corporation, yet to fully demonstrate ecological independence and commercialization capabilities, naturally cannot command the same premium as an "independent vanguard."

Shortcomings in the software ecosystem are equally hard to ignore. Ouyang Jian himself acknowledges this—when discussing Kunlunxin's "CUDA-like" programming model, he admits, "We have a programming model very close to CUDA, with better performance and cost-effectiveness than competitors, but in terms of versatility, programmability, and ecosystem, we do lag behind the leading competitors."

03

Under NVIDIA's Shadow: How Long Can Kunlunxin Sustain Its "Home Field Advantage"?

Beyond the valuation gap, Kunlunxin faces significant uncertainty due to fierce competition across the entire industry sector.

According to IDC's latest data, total AI accelerator card shipments in the Chinese market reached approximately 4 million units in 2025, with NVIDIA firmly dominating the market with around 2.2 million units shipped, accounting for a 55% market share. Although this represents a significant decline from its earlier overwhelming dominance of over 90%, NVIDIA's ecological advantage in high-end training products remains virtually unchallenged.

Among domestic players, Huawei holds the second-largest overall market share in China and the top position domestically, with 812,000 units shipped, accounting for approximately 20% of the market. Alibaba's T-Head ranks second domestically with 265,000 units shipped, representing about 6.6% of the market. Kunlunxin and Cambricon tie for third place domestically, each shipping around 116,000 units.

Kunlunxin's approach of offering "comprehensive AI server solutions" initially sidestepped the complexity of software adaptation for clients, making it highly attractive to government, enterprises, and telecom operators. However, the long-term scalability of this strategy remains untested.

"Comprehensive solutions" imply a product form closer to "software-hardware integration," yielding higher gross margins than selling standalone cards. However, this approach also places Kunlunxin in direct competition with system-level players like Huawei and Inspur.

During the window of domestic substitution, Kunlunxin leveraged "localized orders" from telecom operators, government agencies, and financial institutions to gain an early lead. However, as penetration rates in these sectors gradually saturate, maintaining high growth will require Kunlunxin to compete head-on with NVIDIA and Huawei in broader commercial markets.

CUDA's entrenched software ecosystem and Huawei Ascend's full-stack solution of "chips + MindSpore + CANN" represent formidable obstacles Kunlunxin must overcome.

The significance of the spin-off becomes nuanced in this context. From Baidu Group's perspective, Kunlunxin's independent listing effectively alleviates Baidu's financial burden—chip development is a capital-intensive, long-cycle sector, and Kunlunxin's past losses directly dragged down Baidu's profitability. After the spin-off, external financing will no longer be consolidated in Baidu's financial statements, significantly reducing pressure on the group's R&D expenditures.

Baidu recognizes this as well. The spin-off announcement openly states that independent listing would, on one hand, attract investor groups focused on AI computing chips, and on the other hand, enhance Kunlunxin's image among clients, suppliers, and potential strategic partners, strengthening its negotiating position to secure more business.

However, while proclaiming "independent development," Kunlunxin remains a subsidiary with 57.67% of its shares firmly controlled by Baidu. The market likely sees through this rhetoric.

04

The Market's Eyes Are Clear: The AI Chip IPO Boom Faces Its True Test

For investors, the suspense surrounding Kunlunxin's IPO extends far beyond its pricing alone. Investment banks have set conflicting targets: BOC International's research team has valued Kunlunxin at 100 billion Hong Kong dollars. Goldman Sachs estimates that if the market grants Kunlunxin a valuation multiple similar to Cambricon's, Baidu's approximately 57.67% stake in Kunlunxin would be worth up to 22 billion US dollars, equivalent to 45% of Baidu's current market value.

However, given current circumstances, this optimistic assumption is unlikely to materialize. After listing, shares of Moore Threads and MetaX both experienced significant declines from their peak values. For Kunlunxin, with shipments of 116,000 units, replicating the thousand-billion-yuan market value miracle of Moore Threads and MetaX will require far more than imagined.

Market scrutiny of domestic AI chip companies has evolved from merely assessing "domestic origin" to a comprehensive evaluation encompassing technological autonomy, client structure, ecological barriers, and profitability. Any deficiency in these areas will be penalized by secondary market investors.

Kunlunxin's dual "A+H" capital strategy may provide a unique buffer—the Hong Kong Stock Exchange offers international financing and brand endorsement, while the STAR Market focuses on high valuations and pricing power for hard technology. A dual listing ensures financing certainty while balancing valuation and market image.

This pragmatic capital allocation, capable of "advancing or retreating," represents Kunlunxin's response to its current valuation gap.

The most critical move by a Chinese internet company in the AI era hinges on Baidu's third bell-ringing ceremony.

However, as the frenzy of capital celebration subsides, the questions facing Kunlunxin and Li Yanhong remain sharp: Amidst the domestic camp's aggressive advance and complex capital narratives, a company's greatest challenge has never been "how to go public," but rather "how to survive after going public."

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!

-

![]()

AI Agent Smartphones: The Next Competitive Edge Transcends Large Models

-

![]()

Over 880 Million Yuan Worth of Orders Unveiled, Bidding Launched for Shenzhen Eastern Public Transport

-

![]()

Tesla's Robotaxi Hits the Road: A Monumental Gamble with an Uncertain Future