Defying the Cost Tsunami: Why is Apple Daring to Cut Prices Amid Industry-Wide Hikes?

05/18 2026

05/18 2026

581

581

iPhone 17 Price Drop: Apple Shifts from Value Retention Myth to Price War

Author | Jin Yingshi

Click to listen to the podcast version of this article

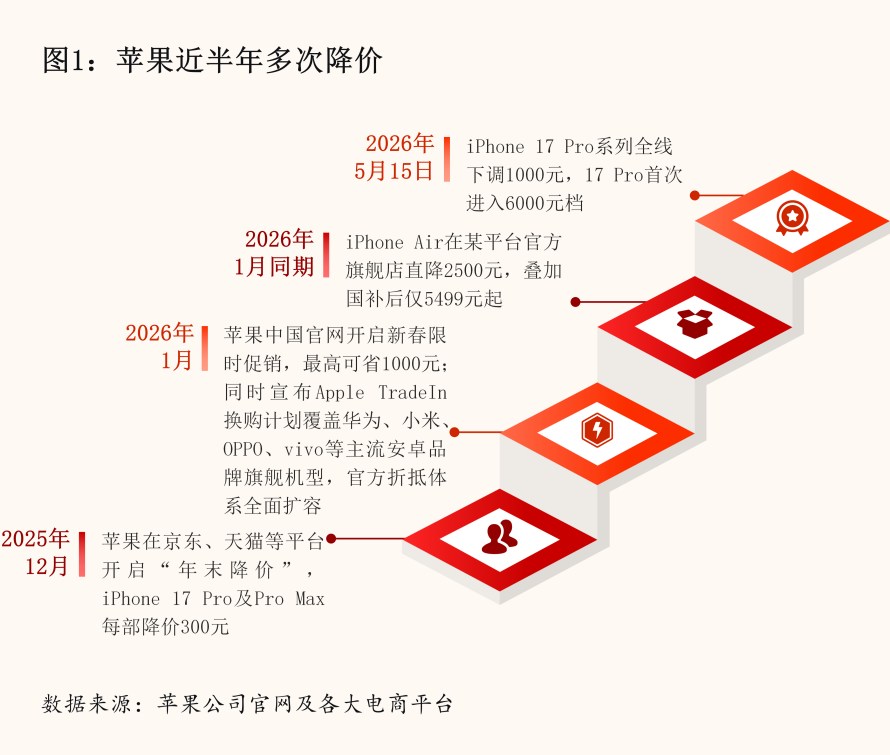

At midnight on May 15th, JD.com's Apple flagship store took the lead in adjusting prices, with the iPhone 17 Pro series seeing a uniform reduction of 1,000 yuan across the board. When combined with dual subsidies for trade-ins, savings could reach up to 2,000 yuan, bringing the final price to 6,999 yuan. The iPhone 17 Pro officially entered the 6,000 yuan price bracket, marking the lowest official channel price since the series' launch.

Simultaneously, Tmall's Apple Store official flagship followed suit, with the iPhone 17 seeing its first price drop post-launch. With multiple subsidies and trade-in offers, the final price reached just 4,499 yuan.

Authorized resellers also received official notifications, initiating a comprehensive price adjustment spanning both e-commerce and offline channels.

The reason this event sent shockwaves through the industry lies not only in the staggering 1,000 yuan price drop itself but also because it occurred during an extremely 'abnormal' time window. Global memory chip prices have surged for several consecutive quarters, prompting Android brands to raise prices to pass on costs. The entire smartphone industry is undergoing a supply chain-driven price reshaping.

Amidst widespread cost anxieties across the industry, why would the world's highest-valued tech company choose a pricing path no one anticipated?

Memory Price Hikes and the 'Matthew Effect' in the Smartphone Industry

The most critical variable in the 2026 smartphone industry is the explosive surge in memory chip prices. The capacity battle ignited by AI computing power demand is reshaping profit distribution across the entire industrial chain.

According to TrendForce's latest survey, mobile DRAM contract prices continued to rise sharply in Q2 2026, with LPDDR4X average selling prices (ASP) increasing by at least 70%-75% quarter-on-quarter, while LPDDR5X saw a 78%-83% quarterly increase.

This upward trend has persisted for several quarters. UBS estimates that by Q4 2026, memory costs' share in mid-to-low-end smartphone BOMs will rise from 22% in Q4 2024 to 34%, with per-unit memory costs increasing by approximately $16 year-on-year.

Shortages and price surges in DRAM and NAND chips have become one of the most severe supply chain crises in the smartphone industry in recent years, with cascading effects deeply embedded in terminal market pricing systems.

Faced with this 'cost tsunami,' smartphone brands have adopted starkly different strategies: Huawei and Apple have chosen not to raise prices or even cut them, relying on supply chain bargaining power and brand premium to absorb cost pressures; Xiaomi has proactively reduced shipments, strategically 'cutting volumes' to avoid direct competition; while OPPO and Vivo have adopted a middle ground, moderately raising prices on mid-to-low-end models to maintain profits.

In response to cost-side price hikes, the industry landscape is rapidly differentiating. Omdia data shows that Q1 2026 smartphone shipments in mainland China reached only 69.8 million units, down 1% year-on-year, with the market in a consolidation phase. IDC recorded 69.01 million units, a 3.3% year-on-year decline.

Against a backdrop of market pressure, the Matthew Effect has intensified, with leading brands' anti-cyclical capabilities contrasting sharply with smaller manufacturers' survival struggles.

The Pricing Logic After a 28% Surge

To understand Apple's pricing confidence, we must start with an exceptionally strong financial report.

In Q2 FY2026 (ending March 28), Apple achieved total revenue of $111.184 billion, up 16.6% year-on-year, setting a new historical high for the same period. Net profit reached $29.578 billion, up 19.4% year-on-year, surpassing last year's $24.77 billion and significantly exceeding Wall Street's expected $26.7 billion; gross margin stood at 49.3%, with a net margin of 26.6%.

All business segments performed strongly, with iPhone revenue contributing $56.994 billion, up 21.68% year-on-year, accounting for 51.26% of total revenue; services revenue reached $30.976 billion, up 16.25% year-on-year; Mac and iPad businesses also achieved steady growth.

Globally, Greater China's performance was particularly outstanding, with regional revenue reaching $20.497 billion in the quarter, surging 28.09% year-on-year and becoming Apple's fastest-growing market among all regions.

Against this backdrop of high growth and rising market share, choosing to cut prices now is clearly not a passive response to 'weak sales.' The prevailing industry interpretation is that this represents a proactive strategic positioning, using short-term price concessions to secure greater market share and deeper user loyalty during an industry downturn.

Why Can Apple Afford to Cut Prices?

Apple's core confidence in defying market trends lies in its far superior profitability and strong supply chain bargaining power.

Apple's profit efficiency advantage becomes clear when viewed from a global market perspective. According to Counterpoint, in Q1 2026, Apple captured 48% of industry revenue with approximately 21% of global shipment share—nearly half the market. Samsung ranked second with 18% of revenue share, while Xiaomi, OPPO, and Vivo accounted for just 6%, 5%, and 4% respectively.

The foundation of this pattern (pattern) lies in the gap in average selling prices (ASPs). In Q4 2025, Apple's iPhone ASP exceeded $1,011 (about 7,028 yuan) for the first time, while OPPO's ASP was $258, Samsung's $249, Vivo's $233, and Xiaomi's just $155 during the same period. The combined ASPs of these four Android manufacturers still fell short of Apple's alone.

Counterpoint notes that Apple has long commanded over 80% of global smartphone market profits through brand premium and product portfolio optimization.

This 'high-margin' profit structure gives Apple ample pricing flexibility when memory chip prices surge and competitors raise prices to survive. While others raise prices for survival, Apple cuts prices to capture market share. The profit efficiency gap dictates fundamentally different strategic choices.

Memory chip price hikes hit hardest manufacturers with thin margins and weak bargaining power, while Apple's supply chain management system has become its most robust defensive moat in pricing strategy.

According to tech media Wccftech, Apple is aggressively purchasing available mobile DRAM at premium prices, even sacrificing short-term operating profits to secure full-year production and inventory safety. This strategy aligns with previous analysis by Tianfeng Securities analyst Ming-Chi Kuo: amid memory market turbulence, Apple can completely absorb high memory costs, lock in supplies early, and squeeze competitors' inventory space to gain a superior long-term competitive position.

Tim Cook's statements during the earnings call corroborate this, noting that memory costs were already higher in Q2 than Q1 and expected to rise further in Q3. However, the company had partially offset these impacts by digesting existing memory inventory stockpiled in advance. This 'early lock-in and hoarding' supply chain strategy has bought Apple valuable breathing room.

Counterpoint analysis suggests that unlike Xiaomi's struggles with smartphone profitability, Apple's gross margins can withstand memory price increases primarily due to the 'blood reserves' built under its premiumization strategy. Relying on this profitability confidence and supply chain foresight, Apple can pursue pricing paths most contrary to industry trends during periods of widespread price hikes.

From Value Retention Myth to Proactive Offensive

This price cut represents a microcosm of Apple's broader pricing strategy shift in China.

Reviewing recent developments:

From 'indirect promotions' to 'direct official price cuts,' from 'channel concessions' to 'unified official pricing,' and from 'annual price reductions' to 'four rounds in six months,' Apple's pricing approach has undergone a dramatic transformation. This shift closely relates to strategic adjustments by Apple's senior management team.

Bloomberg reports indicate that newly appointed core Apple managers have adopted a more aggressive operating style, gradually moving away from overly cautious previous strategies.

Bank of America analysts also note that Apple is intentionally expanding its price bands—extending downward to boost market share while raising prices on ultra-premium models to maintain industry-leading profit levels. This 'price tiering' strategy bears strong similarity to Samsung's high-growth model between 2009-2013, when its global market share surged from 4% to 32%.

Analysts at Hua Nan Yong Chang Securities believe that price cuts across the iPhone 17 series may stimulate a new sales peak, helping further solidify Apple's market position in China. Meanwhile, reports predict that if the iPhone 18 Pro series maintains current pricing instead of raising prices by the end of 2026, locking in high-end sales volumes early could sustain market performance similar to the iPhone 17 Pro. Apple may also expand into higher price tiers with a foldable iPhone Ultra to capture additional profits.

Counterpoint Research forecasts that despite continued market weakness in 2026, memory chip shortages may persist until late 2027, prompting OEMs to shift from pursuing shipment volumes to prioritizing product value enhancement.

Amid narrowing profit margins industry-wide, Apple's price cut sends a more profound signal—not an inability to raise prices, but a strategic choice to 'advance by retreating' within a higher-dimensional framework.

Conclusion

When the company with the industry's highest brand premium begins 'proactively cutting prices,' the rules of the game have fundamentally changed.

Through this price cut, Apple has demonstrated its pricing confidence to the market with exceptional financial performance and profit margins, backed by a robust supply chain management system to lock in costs. Simultaneously, frequent price adjustments have reshaped Chinese premium market perceptions of Apple's 'pricing inertia.'

It's foreseeable that future competition in China's premium smartphone market will unfold simultaneously across two dimensions: innovative product iteration and dynamic price competition. Apple's aggressive participation in the 618 shopping festival with its deepest discounts yet may merely signal the beginning of a larger transformation. When industry giants no longer cling to price redlines, the entire market's profit structure and competitive landscape will be thoroughly reshaped.

References

[1] Apple Inc. FY2026 Q1 and Q2 Financial Reports

[2] IDC China Smartphone Market Tracker Report, Q1 2026

[3] Omdia Global Smartphone Shipment Report Q1 2026 & China Smartphone Market Tracker Report Q1 2026

[4] Counterpoint Research Global Smartphone Market Report

[5] TrendForce Mobile DRAM Report

[6] 'Apple Aggressively Purchasing Mobile DRAM at Premium Prices,' Wccftech Tech Report

[7] RD Observation's Continuous Tracking Data on iPhone 17 Series Domestic Sales (Through W18, May 2026)

THE END

Copyright and Disclaimer

1. Content Copyright: Except for quoted public data, policies, and cases, all content is original. Professional data derives from authorized databases and government websites, with cases compiled from real events.

2. Image Licensing: Some images are proprietary materials or officially licensed, with others AI-generated. For network images without clear copyright attribution, rights remain with original creators and will be removed upon notification.

3.Reprinting specifications: Reprinting is prohibited without permission; if reprinting, the complete source and author must be retained.

4.Disclaimer: This article is a business figure observation and industry commentary compiled by the author based on publicly available information. The content is for reference only and does not constitute professional advice. Any risks arising from its use shall be borne by the user. The Industrial Association reserves the right of final interpretation of this article.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle