Eight Departments and One Pair of Glasses: China Writes the 'Next Gateway' into National Policy Documents

06/24 2026

06/24 2026

340

340

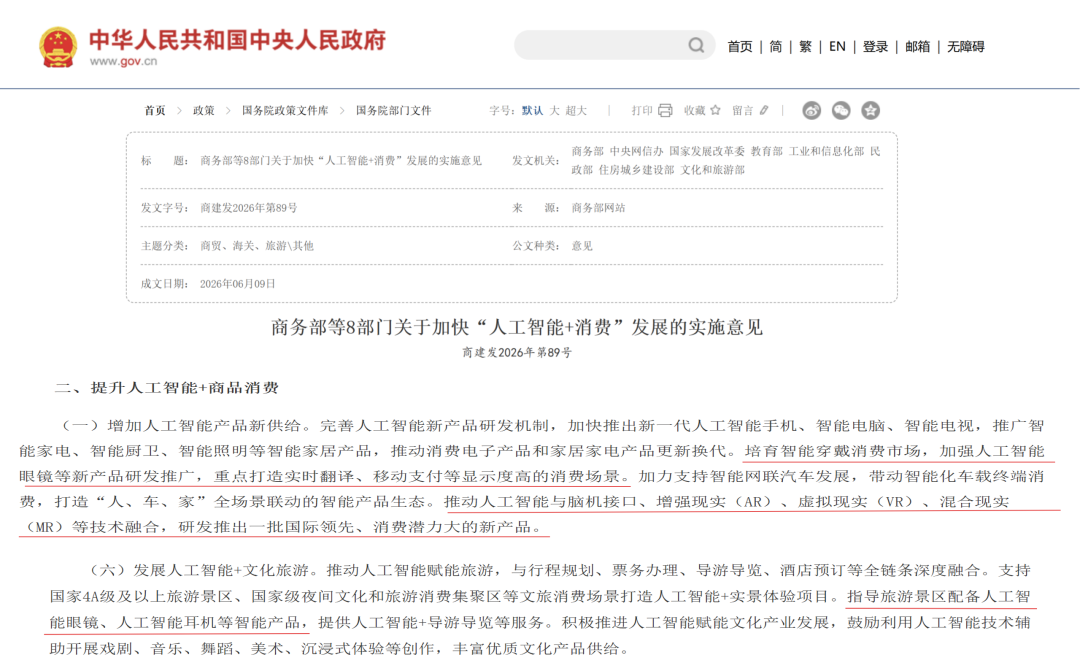

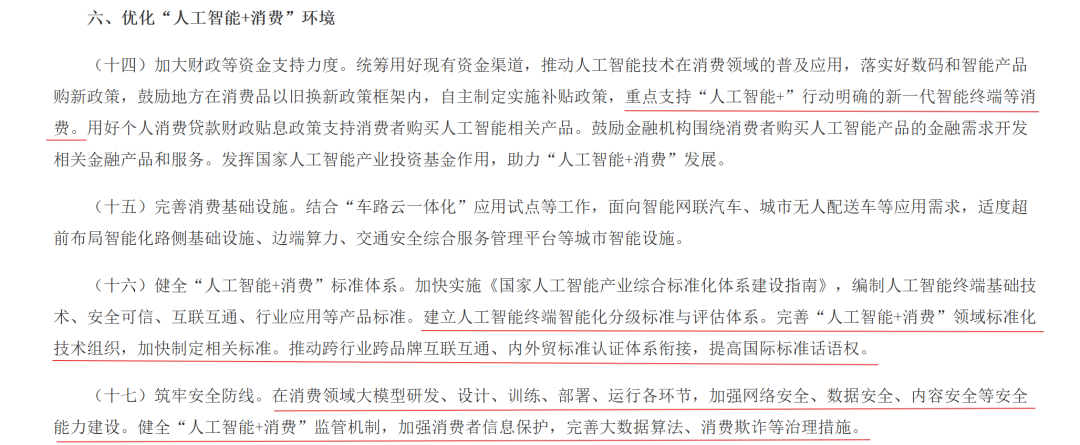

On June 18, 2026, the 'Implementation Guidelines for Accelerating the Development of 'AI + Consumption' by the Ministry of Commerce and Eight Departments' (Shang Jian Fa [2026] No. 89), dated June 9 and jointly issued by the Ministry of Commerce and seven other departments, was officially made public. In this national policy document covering commodity consumption, service consumption, and commercial innovation, smart glasses were explicitly mentioned—twice.

The eight co-signing departments are: Ministry of Commerce, Cyberspace Administration of China, National Development and Reform Commission, Ministry of Education, Ministry of Industry and Information Technology, Ministry of Civil Affairs, Ministry of Housing and Urban-Rural Development, and Ministry of Culture and Tourism. Such high-level cross-departmental collaboration in the consumer electronics sector is rare.

Article (I), 'Increasing New Supply of AI Products,' explicitly states: 'Cultivate the smart wearable consumption market, strengthen R&D and promotion of new products like AI glasses, and focus on creating high-visibility consumption scenarios such as real-time translation and mobile payments.' Another mention appears in Article (VI), 'Developing AI + Cultural Tourism,' which requires: 'Guide tourist attractions to equip with smart products like AI glasses and AI earphones, providing services such as AI-powered tour guiding.'

Implementation Guidelines for Accelerating 'AI + Consumption' by Eight Departments, Source: Chinese Government Website

The two mentions—one unlocking consumption scenarios, the other anchoring specific implementation channels—represent not just 'encouragement of a new function' but 'national-level policy anchoring of a new gateway.'

Placing this moment in a broader context, the smart glasses sector in 2026 stands at a critical inflection point.

According to IDC's Q1 2026 market tracker, global smart glasses shipments reached 3.566 million units, up 130.1% YoY; China's AR/VR category shipments grew 86.2% YoY. Ministry of Commerce data showed a 183.5% YoY increase in online retail sales of smart glasses from January to February 2026, with key platforms reporting a 2.8x YoY sales surge by May. During 618, JD.com's smart glasses sales tripled YoY.

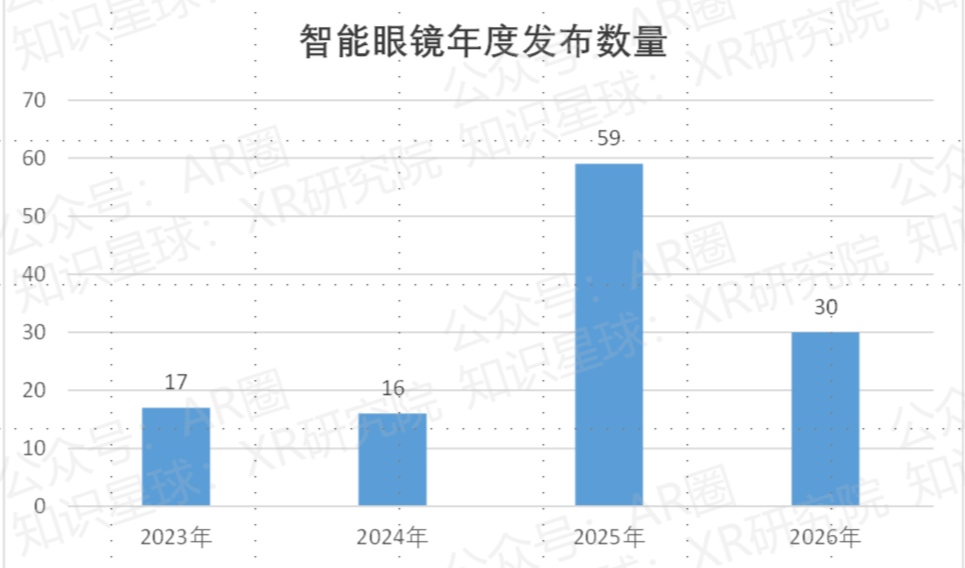

Per the 'Smart Glasses Market Tracker (June 2026 Edition)' by AR Circle and XR Research Institute, 167 smart glasses models were available as of June 2026, with 30 new launches in H1 2026 across 83 brands—a sector rapidly reaching saturation.

Document No. 89 officially confirms this acceleration through policy.

As of June 2026, 167 smart glasses models are available, with 30 new launches in H1 2026 across 83 brands, Source: AR Circle

01 Why Glasses, Not Phones or Earphones?

A notable detail in Document No. 89: 'Real-time translation' and 'mobile payments' are assigned to smart glasses, not phones or earphones.

'Policy selects form factors not based on strongest functionality, but on which best represents next-gen interaction,' Zhu Dianrong, XR Research Institute founder, told AR Circle. 'Glasses' advantage—a consensus in the industry—lies in their ability to simultaneously handle first-person perception, hands-free operation, and real-time information enhancement. Document No. 89 confirms, rather than creates, this reality.'

Form factor differences are clear: phones rely on screens and require active use; earphones handle audio but lack visual output; glasses, worn on the face, accept voice/image inputs and provide audio/visual outputs. First-person perception + hands-free + real-time enhancement—a native closed loop (closed loop) on glasses, unmatched by other consumer electronics.

Inquiry about Rokid AI glasses' World Cup score prediction and display, Source: Rokid

The document's 'real-time translation' and 'mobile payments' exemplify two high-visibility consumer touchpoints for this closed loop .

Phones already offer translation, but the process—'pull out phone → open app → hold up to speaker'—disrupts conversation flow and creates social distance. Glasses translate differently: hearing sound, delivering translation directly to ears/vision without screen interaction. The difference lies not in efficiency but interaction style—shifting from 'I use a device to help' to 'I naturally understand.'

Qianwen AI glasses' real-time translation display, Source: Qianwen

Payment logic is more direct: glasses enable hands-free transactions when phones are inaccessible.

Yet translation and payments are merely two high-visibility policy-selected scenarios. AI glasses' potential spans: first-person filming (phones capture 'quality,' glasses capture 'opportunity'), ambient information streams (navigation, messages, schedules—no screen/hand occupation), AI assistant interaction (voice-activated, natural dialogue), and industrial/research hands-free assistance.

Each scenario contains elements phones/earphones cannot fully address. Document No. 89 bets on glasses as the AI gateway: portable, unobtrusive, always-on.

02 Timing Is No Coincidence

Prior to Document No. 89, the sector had already sent strong signals.

Domestically, H1 2026 saw entry density reminiscent of the smartphone wars. Alibaba, Huawei, Xiaomi, and Li Auto launched smart glasses—internet giants, phone makers, and automakers converging on the sector. H1 2026 marked a clear inflection point: from niche experimentation to big-tech positioning.

Capital accelerated too: Rokid, Thunderbird Innovation, VITURE, and others secured new funding rounds in H1 2026. VITURE alone raised over $200 million in six months—rare amid cautious hardware financing.

Global players persisted: Meta enhanced Ray-Ban series with AI/display features; Google partnered with Samsung/Qualcomm on Android XR; Snap unveiled SPECS AR glasses at AWE 2026; Bloomberg reported ongoing Apple R&D; Kering and traditional eyewear giants also entered.

Snap SPECS AR glasses, Source: 36Kr

From domestic to global, consumer to professional—the breadth of players and scenarios is unprecedented. Glasses' AI gateway potential is being validated simultaneously by diverse actors.

Policy does not create inflection points; it confirms them. Document No. 89's release endorses sectoral changes and signals the window's countdown.

03 What Document No. 89 Offers—and Demands

Document No. 89 impacts smart glasses via four layers:

Layer 1: Demand stimulation. It mandates 'implementation of digital/smart product purchase incentives,' encouraging local subsidies within trade-in frameworks and supporting AI product purchases via personal loan interest subsidies. For smart glasses priced between $150–$1,500, subsidies will significantly boost adoption.

Layer 2: Scenario expansion. It designates tourist sites, elderly care facilities, and cultural venues as key deployment areas—TO G/B scenarios previously hard for consumer brands to penetrate, now opened by policy.

Layer 3: Standardization. It calls for 'AI terminal intelligence grading standards and evaluation systems.' A double-edged sword: weaker players face elimination, while technically robust firms gain clearer competitive frameworks.

Layer 4: Technical direction. It urges 'fusion of AI with BCI, AR, VR, MR to launch globally leading, high-potential products.' 'Globally leading' sets a high bar—domestic players now compete globally.

Together, these layers elevate smart glasses from a 'sector' to a 'national priority.'

Implementation Guidelines for Accelerating 'AI + Consumption' by Eight Departments, Source: Chinese Government Website

04 Four Strategies, Four Critical Questions

Post-policy, success hinges on execution. Domestically, four distinct paths emerge:

Path 1: Ecosystem Binding—Alibaba Qianwen. Launched in March 2026, Qianwen AI glasses (G1: screenless lite, S1: binocular flagship) integrate Tongyi Qianwen LLM and Alibaba core services (Taobao, Alipay, Fliggy). Voice commands enable food orders, shopping, and travel bookings—LLM + ecosystem brings AI assistants from cloud to wearables.

Key question: Can ecosystem-driven value extend beyond Alibaba's own services to broader consumption?

Path 2: Open Ecosystem—Rokid. Rokid glasses support four global AI LLMs, including native Google Gemini integration. Its YodaOS open-source system, with 30,000+ developers, powers smart agent stores spanning automotive, home appliances, and professional tools.

Rokid AI glasses integrate four global AI LLMs, Source: AR Circle

Key question: Can developer scale translate into 'must-have' user scenarios during the policy window?

Path 3: Full-Scenario Matrix—Thunderbird Innovation. Thunderbird offers Air (cinema AR), GT, V (AI filming), and X (full-function waveguide AR) series, spanning $150–$1,500 price points. It pursues both MicroOLED and MicroLED displays, with two R&D/manufacturing bases operational.

Key question: Can matrix breadth yield a 'category-defining' flagship to convert width into brand momentum?

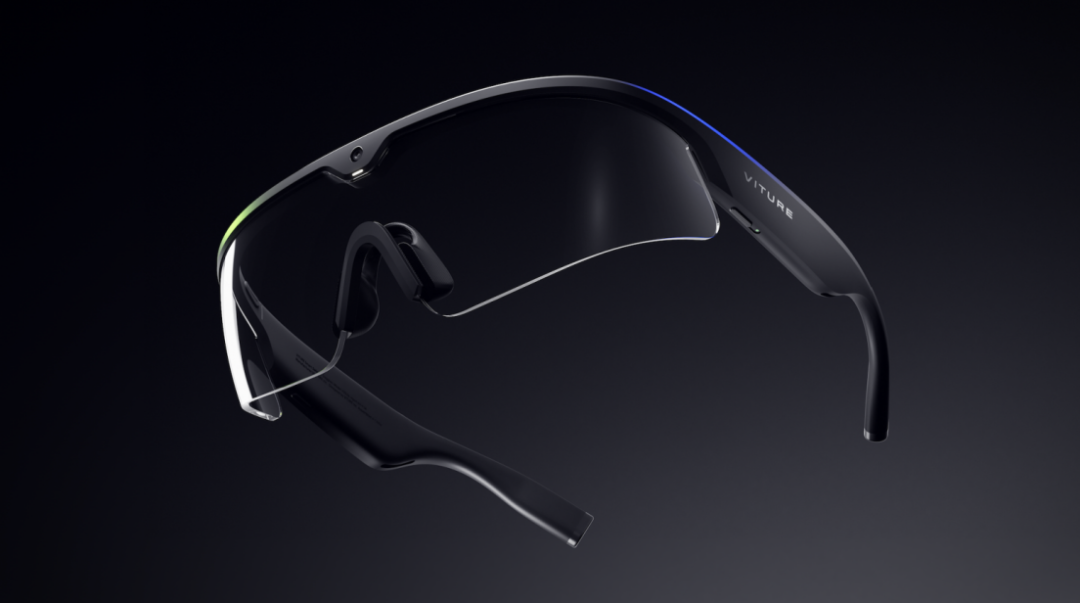

Path 4: Industrial AI Gateway—VITURE. At AWE 2026, VITURE launched Helix, the first industrial AI glasses on NVIDIA XR AI platform, operating independently of phones for scientific research (scientific research), medical, and compliance-driven production lines. It bypasses crowded consumer AI glasses, betting on physical AI's perception hardware gateway.

VITURE Helix AI glasses, Source: VITURE

Key question: Q1 2027's initial Helix deployment compliance will test industrial AI gateway viability.

All paths are valid but challenging. The policy window demands answers: ecosystems must define boundaries, open systems must scale, matrices need focus, and industrial routes require commercialization pace. First to solve their puzzle secures the next round.

Four strategies converge on one choice: in the national policy window, who solidifies the 'AI gateway' position first?

05 After the National Document

The Ministry of Commerce-led eight-department joint policy embedding 'smart glasses' in consumption documents—such cross-departmental consumer electronics collaboration is rare.

Meanwhile, an increasing number of players from various industries at home and abroad are entering this arena in their own ways: mobile phone manufacturers, internet giants, automotive companies, traditional eyewear giants, vertical AR companies, and industrial-grade new forces.

The moment the term 'smart glasses' was written in Document No. 89, all players in the arena heard the starting gun.

The remaining question is no longer 'Will the smart glasses category take off?', but rather—in two years, who will secure their position in front of this national-level opportunity.

END

-

Why is CATL Partnering with Octopus Energy to Build a Battery-Swapping Network for Heavy-Duty Trucks in the UK?

-

![]()

Research on New Trends and User Value in China's Public Charging Consumption Market

-

【Insight】NPO (Near Package Optics) as a Transitional Solution for CPO, Industry Development Embraces Opportunities

-

![]()

Charging Industry Shifts from Quantity to User Experience as New Benchmark

-

![]()

Qianli Technology Aims for Autonomy from Geely's Sphere: Why Does BAIC Initiate the Alliance First?

-

![]()

Three Major New Policies Come into Force on the Same Day, Revolutionizing the Growth Dynamics of China's Auto Market

-

![]()

The Complete Blueprint of Tsinghua-Affiliated Embodied AI 'Startup Dream Team': 7 Companies, 25 Billion in Funding, and the Dawn of an Era

-

![]()

The Ministry of Industry and Information Technology Forces Auto Companies to 'Self-Examine and Rectify,' Banning Unsafe Old Electric Vehicles from the Roads