How Can Chinese Small Home Appliances Conquer Southeast Asia Through 'Dimensional Competition'?

07/02 2026

07/02 2026

326

326

While home appliance giants are aggressively targeting the high-end markets in Europe and America, Chinese small home appliances are launching a 'flanking war' in Southeast Asia. By avoiding direct competition and leveraging agility and precise positioning, they have secured a foothold and grown rapidly in the vacuum left unattended by the giants.

Original Content by New Entropy, New Consumption Team

When Midea made its PortaSplit split-type air conditioner a hot commodity in Europe, prompting foreigners to drive 200 kilometers just to snag a second-hand unit at double the price, everyone hailed the reverse takeover of European and American markets by Chinese manufacturing—with Midea, Haier, and other overseas self-owned brands accounting for 40%–90% of the market share, marking a historic leap from 'Made in China' to 'Brand China.' Yet, few noticed that in the tropical regions with year-round high temperatures, a fiercer 'flanking war' was already underway. Avoiding direct clashes with the big players in the European and American markets, Chinese small home appliance companies have shifted their focus to Southeast Asia. Without the heavy burden of transformation, these brands, which have been squeezed out in China, have found a new haven in the heat and humidity of Southeast Asia with their Ultimate cost-performance ratio (ultimate cost-effectiveness), rich functionality, and lightweight, portable designs.

Small Home Appliances Struggle to Survive in China, Turn to Southeast Asia

Looking back at 2020, internet-famous small home appliances like air fryers, sandwich makers, and blenders capitalized on the 'stay-at-home economy' during the pandemic, filling the gaps in young people's lives with precisely targeted scenarios. During that unique period, for young people living alone and renting, traditional home appliances costing thousands of yuan seemed bulky and uneconomical, while affordable, stylish, and portable small home appliances became instant emotional comforts that required little thought to purchase. Most of these brands started as unbranded factories in industrial belts, relying on the Ultimate cost-performance ratio (ultimate cost-effectiveness) of direct-from-manufacturer sales to execute a brilliant blitzkrieg in the gaps before home appliance giants could penetrate the lower-tier markets.

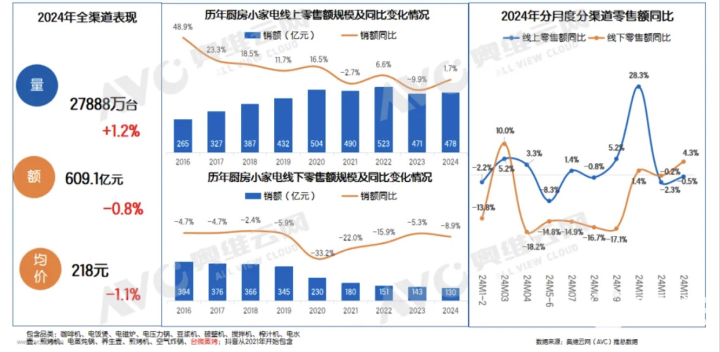

But the tide receded faster than expected. By the 2023 618 shopping festival, growth in the small home appliance sector had already shown signs of slowing. Data from Aowei Cloud was more straightforward: In 2024, the total retail volume of small home appliances in China was approximately 279 million units, a slight year-on-year increase of 0.3%, but retail sales reached 60.9 billion yuan, a year-on-year decline of 0.8%. Volume was up, but prices were down, and the pressure of intense internal competition was mounting.

▲Figure/Aowei Cloud

Worse still, the survival pressure on small home appliances came not only from the market penetration of the giants but also from high-dimensional ecological competition. As Midea built its 'MevoX Self-Evolving Intelligent Agent,' Robam Appliances deepened its 'ROKI Digital Kitchen System,' and Dreame's sub-brand MOVA targeted the whole-house smart ecosystem, the wars among home appliance giants had long transcended the logic of selling individual products to selling system ecosystems.

When Midea and Haier redefined family scenarios with whole-house smart ecosystems, the niche scenarios that small home appliances relied on for survival were completely devoured. Your power outlets, your data, and your interaction entry points were either absorbed by the giants or completely eliminated. Moreover, even Pop Mart, a company known for selling trendy toys, wanted a piece of the pie: As early as August 2025, Pop Mart began recruiting talent related to small home appliances; by April 2026, IP-derived small home appliance products were officially launched, covering kitchen appliances like electric kettles and coffee makers, as well as limited-edition Labubu coolers.

The intention was clear: to create 'lifestyle' products centered around IP.

When small home appliances are no longer just life tools but are bundled into emotional consumption and ecosystem memberships, brands that rely solely on aesthetics and cost-effectiveness to break through will see their survival space further squeezed. Apart from established players like Bear Electric Appliance and Buydeem, which have some brand momentum and can seek transformation, most small and medium-sized players without brand heritage, technological accumulation, or financial strength have no choice but to find alternative paths—avoiding both the low-price competition in China and direct clashes with home appliance giants in the European and American markets, and instead targeting the emerging Southeast Asian market.

Striking Gold in Southeast Asia: Precisely Harvesting the 'Tropical Dividend'

A wave of Chinese small home appliance 'guerrilla forces' has risen prominently in Southeast Asia. Gaabor, a new brand founded in September 2021, achieved sales exceeding 230 million yuan and shipped 1.82 million units within just one year, with its air fryer alone selling over a million units annually, consistently ranking first in multiple Southeast Asian countries on Shopee and TikTok's small home appliance categories. In just four years, it has joined the ranks of billion-yuan sellers.

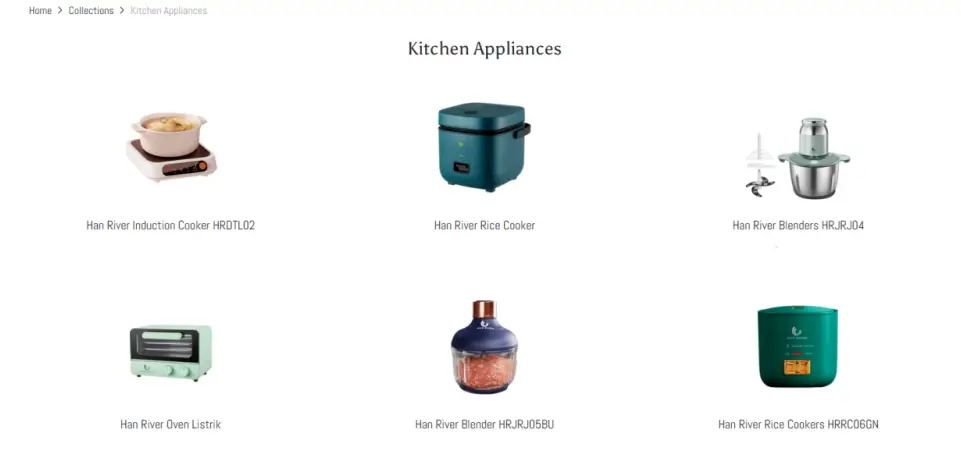

Another small home appliance brand from Chaoshan, Guangdong, Han River, had already become a top seller in Shopee Indonesia's home appliance category by 2020 and ranked among the top four sellers in Southeast Asia. According to relevant data, its annual revenue exceeded 150 million yuan in 2025, with some individual products selling over 20,000 units per month, generating 2.34 million yuan in sales.

▲Figure/Han River

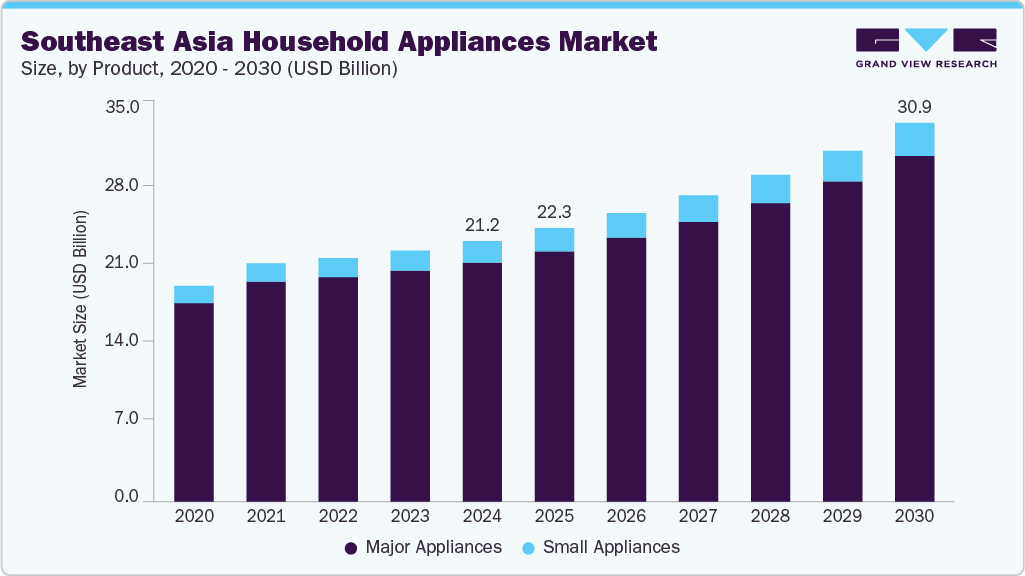

Bear Electric Appliance, which has deep roots in the Vietnamese market, customized electric stew pots and air fryers for local steaming and boiling dietary habits, seeing a 26.66% year-on-year increase in export revenue in 2024 and ranking second in market share for online air fryers in Vietnam. According to Grand View Research, the Southeast Asian small home appliance market reached $22.3 billion in 2025 and continues to grow at a compound annual rate of 6.7%.

On one hand, there is rapidly growing demand; on the other, Chinese small home appliances are thriving overseas. This begs the question: Why has Southeast Asia become such fertile ground for Chinese small home appliances to go global?

▲Figure/Grand View Research

First, the perfect alignment of demographic dividend and demand matching. Although Southeast Asia has a total population of only 660 million, 70% are under 35. As an emerging market in the midst of economic acceleration, local young consumers have a strong willingness to consume online, eager to improve their quality of life while being highly price-sensitive. Chinese small home appliances, with their stylish designs, multifunctionality, and low prices, precisely meet market demands.

Second, precise positioning of niche demands. The hot and humid climate in Southeast Asia leads to a prevalence of small households, with local users preferring lightweight, wireless, and multifunctional small home appliances. From a scenario perspective, high temperatures and humidity have created strong demand for handheld fans and dehumidifiers; multigenerational family structures have amplified the market for multifunctional food processors; and the local enthusiasm for social gatherings and cold drinks has driven broad growth for kitchen appliances like air fryers and ice makers.

Third, the 'short-circuit economy' enabled by e-commerce infrastructure. Shopee and Lazada have deep roots in the region, while TikTok Shop has ignited content e-commerce in Indonesia, Vietnam, and elsewhere. Cross-border logistics and overseas warehousing systems are becoming increasingly mature, allowing Chinese brands to bypass the heavy barriers of traditional offline distribution and directly reach consumers. For example, Gaabor Sharp capture (keenly captured) the market characteristics of Southeast Asia, where 'local celebrities have strong influence and live commerce conversion rates are high,' and built a marketing system combining 'local celebrity endorsements + mid-tier influencer recommendations,' directly converting traffic into sales.

As of now, Gaabor's exposure on social media platforms like Facebook, Instagram, and TikTok has exceeded 100 million, growing far faster than its competitors during the same period. Fourth, the ultimate supply chain advantage. As the world's largest manufacturer of small home appliances, China accounts for approximately 60%–70% of global production capacity. The rapid prototyping, extreme cost control, and agile functional iteration capabilities of industrial clusters in the Pearl River Delta and Yangtze River Delta represent formidable barriers that Southeast Asian local brands find difficult to overcome. This supply chain advantage gives Chinese small home appliance brands an absolute 'quality-to-price ratio' advantage when facing the fragmented Southeast Asian market.

From 'Selling Goods' to 'Taking Root': Three Hurdles to Overcome

However, Southeast Asia is far from a paradise for gold prospectors. While it may seem like a land of opportunity, it is fraught with hidden reefs. Data shows that over 70% of small home appliance brands that go overseas fail to survive a year there. In a highly fragmented market landscape, transitioning from 'selling goods' to 'taking root' requires overcoming three critical challenges.

The first is extreme market fragmentation: Southeast Asia consists of 11 countries with vast differences in language, culture, and religion. For example, Vietnamese consumers prefer low-priced and practical products, while Indonesians favor high-end and intelligent ones. Domestic 'one-size-fits-all' strategies are doomed to fail. Therefore, the ability to execute refined local operations is the primary challenge for all brands entering Southeast Asia.

Take Gaabor as an example. Its ability to break through within a year is attributed to its ultimate “ localization ” (extreme localization) in product design, marketing strategies, and even team management: For the air fryer alone, multiple versions were developed to suit local conditions. For multigenerational households in Thailand and the Philippines, it launched a 6.5L Giant capacity (jumbo-sized) model; for the small household pain point in Vietnam, it focused on 3L-4.5L compact models. Not to mention features like low-temperature fresh-locking and steam-tender frying optimized for local dietary preferences.

▲Figure/Gaabor

In marketing, Gaabor also refused a one-size-fits-all approach. For core markets like the Philippines, Indonesia, Vietnam, Thailand, and Malaysia, it built independent localized accounts and developed differentiated content. This 'one country, one policy' refined operation is not just a test of patience but an ultimate filter for cultural insight.

Han River, on the other hand, offers an alternative approach: Instead of rushing to expand across the board, it first deepened its presence in Indonesia, becoming a top seller there before gradually radiating to Malaysia, Vietnam, and Thailand. At the same time, it expanded from cleaning appliances to multiple categories like kitchen and personal care, building a brand matrix.

▲Figure/Han River

The second challenge is breaking free from the low-price quagmire: In Southeast Asia, numerous unbranded products flood the market with $9.9 shipping-inclusive deals, compressing the industry's average gross margin to below 10%. Coupled with China's highly mature industrial belt, where product functionality is easily replicated, mere feature stacking is no longer a winning strategy. Failing to escape the price war will quickly lead to a replay of the brutal internal competition seen in the domestic market.

The third challenge is bridging the brand gap: Under the fast-moving consumer goods model, brand loyalty among Southeast Asian consumers is less than 15%, with over 70% of purchases being impulsive. Traffic comes and goes quickly, leading most brands to remain stuck in cross-border dropshipping modes, lacking local after-sales, warehousing, and operational systems. Additionally, the fragmented logistics and inconsistent after-sales standards across Southeast Asian countries result in inefficient product repair and return processes, uneven consumer experiences, and difficulty in improving repurchase rates and reputation. Notably, some leading companies have already begun seeking breakthroughs by moving production capacity overseas.

Midea and Haier have established production bases in Thailand and Indonesia; leading OEM companies like Xinbao and Biyi have also followed suit with their own layout (layout). This is not just about shortening delivery cycles but also about building brand trust through localized production, avoiding trade barriers, and truly transforming from outsiders to local players. The rise of Chinese small home appliances in Southeast Asia is essentially a form of 'dimensional competition.'

In China, they are the underdogs squeezed by the ecosystems of industry giants; in Southeast Asia, however, they have become the dominant players armed with mature supply chains, advanced e-commerce operation experience, and agile product iteration capabilities—those things considered 'basic skills' in China have become powerful weapons to outcompete local brands here. Additionally, Southeast Asia is highly fragmented, and home appliance giants often focus on the more brand-premium-driven European and American markets, inadvertently leaving a vacuum that allows Chinese small home appliances to secure early positions and thrive rapidly. However, this does not mean they can rest easy.

Southeast Asia today closely resembles the Chinese market twenty years ago: wild, vibrant, full of opportunities, yet fraught with pitfalls. Ultimately, the ones that survive may not necessarily be the fastest runners but rather those willing to Squat down (squat down) and understand every inch of the land, those willing to shift from a sales-oriented mindset to a brand-building one, and those capable of turning short-term traffic into long-term trust—the few who dare to be different.

- END -

-

![]()

Behind the Release of Its First Self-Developed Chip, Is OpenAI's Full-Stack Ambition on Display?

-

![]()

Has Anthropic Targeted Chinese Users? Is a New Era of AI-Driven Racial Discrimination Emerging?

-

![]()

MathWorks: Generative AI Holds Great Potential, Yet a Trusted Toolchain is Essential for Flawless Operation

-

![]()

Small Earphones, Big Business

-

![]()

Volkswagen Slashes 100,000 Jobs, Mercedes-Benz Axes Year-End Bonuses: What’s Ailing German Auto Titans?

-

![]()

Doubao Can No Longer Offer Free Services to 345 Million Users: China's Era of Free AI Is Drawing to a Close

-

![]()

How Can Chinese Small Home Appliances Conquer Southeast Asia Through 'Dimensional Competition'?

-

![]()

Why are top intelligent driving players betting on reinforcement learning?