Has the Smartphone Era Embraced Price Hikes? Is Pausing New Releases the Optimal Strategy?

03/20 2026

03/20 2026

691

691

Author | Wuzi

In 2026, the mobile phone industry witnessed its most significant "black swan" event: a dramatic surge in memory prices.

Counterpoint's Memory Price Tracking Report reveals that DRAM prices skyrocketed by over 50% quarter-on-quarter in the first quarter of 2026, while NAND prices soared by more than 90%. Memory prices are projected to continue climbing by approximately 20% in the second quarter.

Faced with relentless pressure from escalating memory costs, smartphone manufacturers such as OPPO, Vivo, and Honor have responded by raising product prices, with hikes ranging from several hundred to over a thousand yuan.

While transferring cost pressures to consumers can temporarily alleviate operational strains for smartphone makers, it may also dampen consumer purchasing enthusiasm. Counterpoint senior analyst Jeongku Choi observes, "For terminal manufacturers, this is a double whammy—rising component costs coupled with diminishing consumer purchasing power. As the quarter progresses, demand is likely to decelerate."

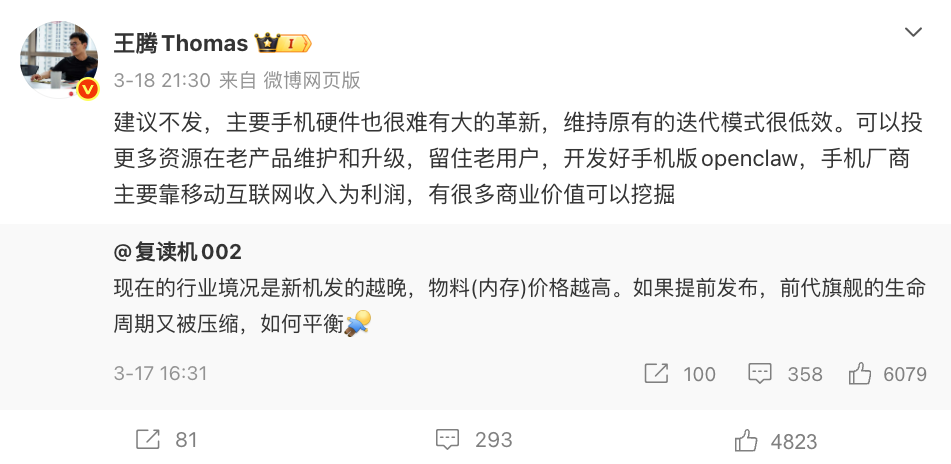

Image source: Wang Teng

As an outsider to the current predicament, Wang Teng, former General Manager of Xiaomi China's Marketing Department and head of the REDMI brand, suggests that manufacturers refrain from launching new devices amid soaring memory prices. He argues that significant hardware innovations are scarce, rendering the existing iteration model inefficient.

Wang Teng believes smartphone makers should channel more resources into maintaining and upgrading older products to retain users and develop a robust mobile version of OpenClaw (an AI agent framework). "Smartphone manufacturers primarily profit from mobile internet revenue, and there's substantial commercial value to unlock," he asserts.

This raises the question: Is Wang Teng's advice sound? What growth opportunities exist at the smartphone system level? If hardware investment yields diminishing returns, why are manufacturers still eager to launch new products?

01

Memory Price Hikes Normalize "Price Increases and Reduced Configurations"

While the rapid rise in memory prices is widely acknowledged, what's the actual impact on the cost of a single smartphone? At MWC 2026 in early March 2026, Lu Weibing, Partner and President of Xiaomi Group, as well as President of Xiaomi's Mobile Phone Division and General Manager of the Xiaomi Brand, provided a clear quantitative breakdown of recent memory price hikes.

Lu Weibing revealed that in the first quarter of 2026, memory quotes were nearly four times higher than the same period last year. "A 12GB+256GB memory combination, which cost about $30 (approximately 207 RMB) at its lowest, now costs around $120 (approximately 826 RMB)—quadruple the previous cost."

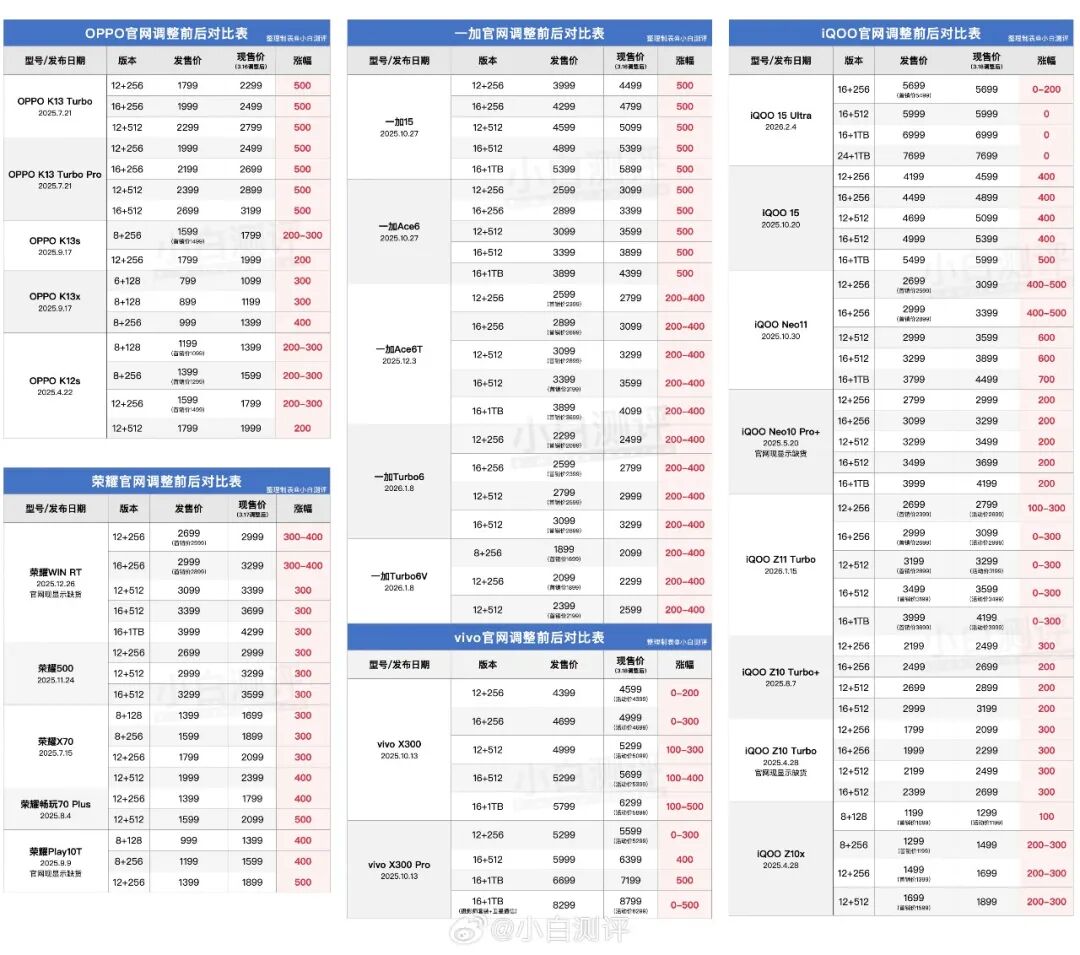

Image source: Xiaobai Reviews

Based on Lu Weibing's data, the memory cost for a 12GB+256GB smartphone has surged by approximately 619 RMB. However, smartphone manufacturers have not fully passed these cost increases onto consumers. Data compiled by Xiaobai Reviews indicates that recent price hikes for several smartphone models range from 200 to 500 RMB.

The reason is that smartphone makers recognize that indiscriminate price hikes could significantly curb consumer demand. Thus, they aim to absorb some cost pressures through internal efficiencies.

In early March 2026, Lei Jun, Founder, Chairman, and CEO of Xiaomi, stated in an interview, "(Memory price hikes) have exerted significant pressure on our mobile phone and related businesses. We may need to digest these cost pressures through internal efficiency improvements as much as possible. We'll explore various ways to minimize consumer difficulty."

However, it's crucial to note that due to intense homogenized competition in the smartphone industry, only Apple can secure substantial profits through differentiation. Many smartphone brands operate on razor-thin margins.

Take Xiaomi as an example. In the first half of 2025, its smartphone business had a gross profit margin of 11.95%. During the same period, the average selling price of Xiaomi smartphones was just 1,142.1 RMB, with an average gross profit of only 136.48 RMB per unit. With extremely limited profit buffers for entire devices, smartphone manufacturers like Xiaomi struggle to respond flexibly to severe cost shocks.

Given this, many smartphone makers are not only raising prices but also eager to make "reductions" in hardware configurations.

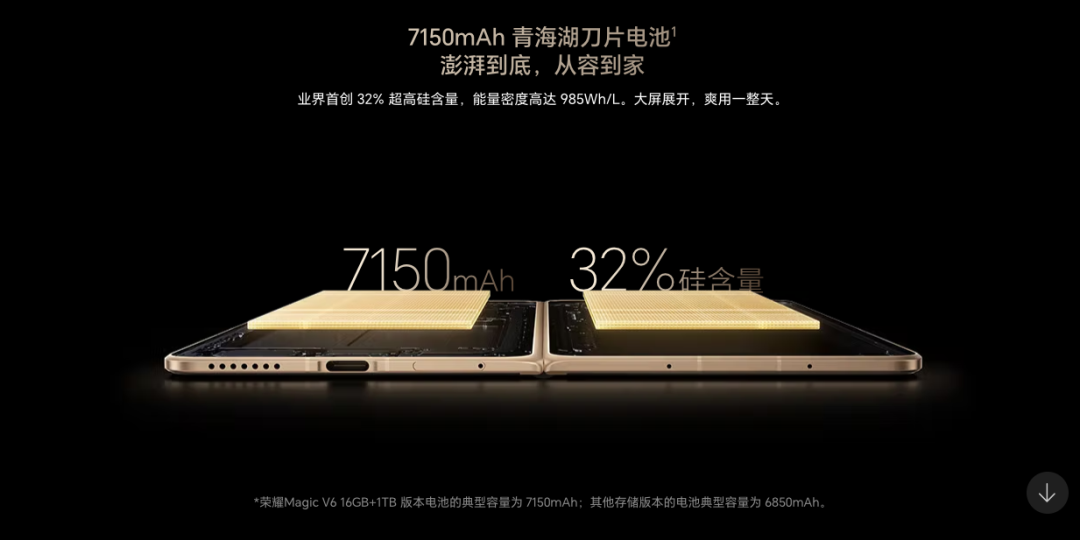

Image source: Honor

For instance, the Honor Magic V6, released on March 10, is priced between 8,999 RMB and 11,999 RMB, with a 1,000 RMB price increase for the large-memory version. Although marketed as a "foldable screen grand slam," the Honor Magic V6's imaging hardware configuration saw little improvement, with only the 16GB+1TB top-tier model featuring a 7,150mAh battery and support for Beidou satellite messaging.

More notably, according to renowned tech blogger "Digital Chat Station," current mid-range and low-end new devices are "regressing," testing mainstream screen configurations from around 2019—90Hz waterdrop screens.

Given the high prices and limited upgrades of new smartphone models, consumers are beginning to hold onto their money and vote with their feet. Data disclosed by "RD Observation" shows that in the first three days of sales, the Honor Magic V6 sold only 75% as many units as the Honor Magic V5 during the same period.

Thus, Wang Teng's recent suggestion that smartphone manufacturers refrain from launching new devices does hold some reasonableness.

Although smartphone makers are adopting proactive strategies to cope with rising memory prices, the severity of the increases makes price hikes and reduced configurations for new devices unavoidable. This shift not only makes consumers cautious about new smartphone releases but also reduces the marginal returns of the new device-driven sales model that smartphone manufacturers have long relied on.

Against a backdrop of diminishing returns from acquiring new users, smartphone manufacturers indeed need to turn their attention to existing users.

02

The AI Era Arrives: Manufacturers Must Win the Access Point Battle

Unlike traditional terminals, which have relatively limited post-transaction engagement with platforms, smartphones, as mass computing platforms, continue to provide services such as app distribution, finance, and gaming long after the initial sale. Manufacturers maintain long-term connections with users and generate revenue through these channels.

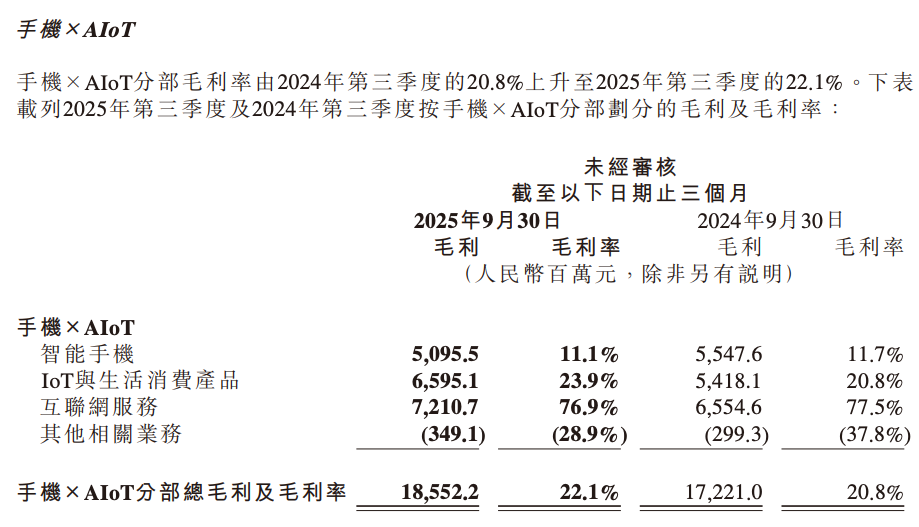

Image source: Xiaomi's Q3 2025 financial report

Take Xiaomi as an example. Although it is a smartphone manufacturer, its primary revenue comes from internet services. Financial reports show that in Q3 2025, Xiaomi's internet services had a gross profit margin of 76.9%, generating 7.211 billion RMB in gross profit—accounting for 38.87% of the total gross profit of the Mobile × AIoT division, far exceeding the smartphone business.

Against the backdrop of sustained memory cost increases, if smartphone manufacturers allocate more of their limited resources to engaging existing users—improving the smoothness of older models, expanding new system compatibility, and strengthening software capabilities—they could enhance user stickiness and generate revenue, providing a stable path through the downturn.

More importantly, as technology matures, the smartphone industry is on the verge of entering the AI era. This new market environment places new demands on smartphone manufacturers.

Since 2026, driven by OpenClaw, the tech industry has seen a surge in "shrimp farming" (a metaphor for AI agent development). In the future, AI agent tools like OpenClaw could become core access points for smartphones. To avoid losing control over primary access points, manufacturers must develop their own "lobster" (AI agent) ecosystems.

Image source: Xiaomi

Currently, many smartphone manufacturers are intensifying their efforts in OpenClaw-related businesses. For example, on March 6, Xiaomi launched "Xiaomi Miclaw," a mobile agent product, and began closed beta testing. On March 10, Honor introduced the "Lobster Universe," allowing Honor smartphone users to interact with YOYO and "Lobster." On March 11, Huawei released the "Xiao Yi Claw" Beta version, capable of handling tasks such as document editing, PPT creation, and email replies.

However, unlike traditional software, which can dilute usage costs through economies of scale, OpenClaw consumes massive amounts of tokens during task execution, resulting in high costs. To encourage users to adopt "lobster" habits, manufacturers must invest heavily in subsidies to educate the market.

Image source: Xiaomi

For instance, at Xiaomi's Spring 2026 product launch on March 19, Lei Jun announced that Xiaomi is embracing the AI era and will invest over 60 billion RMB in AI over the next three years. For context, Xiaomi's net profit in 2024 was just 23.578 billion RMB. This massive AI investment will place significant pressure on the company's cash flow in the coming years.

Clearly, for smartphone manufacturers, amid rapidly rising upstream memory costs, leveraging software services to unlock the "residual value" of existing users is a more rational choice. As AI technology matures, manufacturers aiming to secure a place in the AI era must allocate limited resources to software development and user subsidies.

03

Caught in a "Prisoner's Dilemma," New Device Releases Cannot Stop

Although Wang Teng's suggestion holds some merit, smartphone manufacturers have not adopted a defensive posture. Instead, they are rushing to launch new products.

Since 2026, Samsung, Honor, OPPO, and other manufacturers have released products such as the Galaxy S26, Magic V6, and Find N6. Brands like Vivo, OnePlus, and iQOO are set to launch new models such as the X300 Ultra, OnePlus 15T, and iQOO Z11.

The primary reason smartphone manufacturers continue to release new devices, rather than following "rational economic" logic and halting launches, is that they are caught in a "prisoner's dilemma."

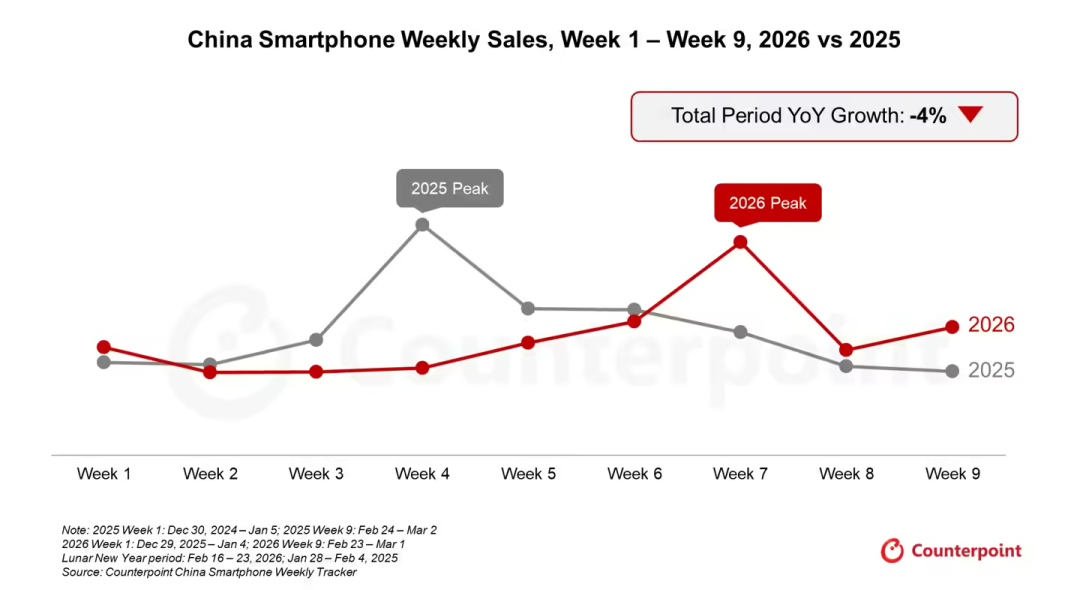

Image source: Counterpoint

Due to soaring memory prices, consumer demand has been severely suppressed, leading to a significant contraction in the smartphone market. Counterpoint data shows that in the first nine weeks of 2026, smartphone sales in China fell by 4% year-on-year. IDC forecasts that global smartphone shipments will decline by 12.9% year-on-year in 2026.

Against this backdrop, while the return on investment for smartphone manufacturers is far from ideal, the shrinking market size means intensified internal competition. If a manufacturer halts new device releases, its market share will be eroded by competitors, potentially leading to a "death spiral."

However, it is worth noting that amid memory price hikes, manufacturers are not pursuing their previous "flood the market" strategy but are instead targeting the high-end segment. For example, the Honor Magic V6 and OPPO Find N6 have starting prices as high as 8,999 RMB and 9,999 RMB, respectively, aligning with the iPhone 17 Pro series.

The rationale behind manufacturers' focus on high-end flagship models is twofold: First, flagship phones command higher prices, providing ample buffer space for cost increases. Second, manufacturers hope to use high-end models as a platform to drive the adoption and application of AI technologies.

As mentioned earlier, driven by OpenClaw, smartphone manufacturers are actively "farming shrimp" (developing AI agents). However, given the sensitivity of private data on smartphones, manufacturers must also address privacy and security concerns when integrating "lobster" (AI agents). Lei Jun stated, "The main concern now is the upload process to the cloud, where many security factors are inadequate. We aim to process highly private information locally."

Due to limitations in physical space and cooling, smartphones have a clear performance ceiling. Currently, only more energy-efficient flagship processors can provide sufficient on-device AI processing capabilities.

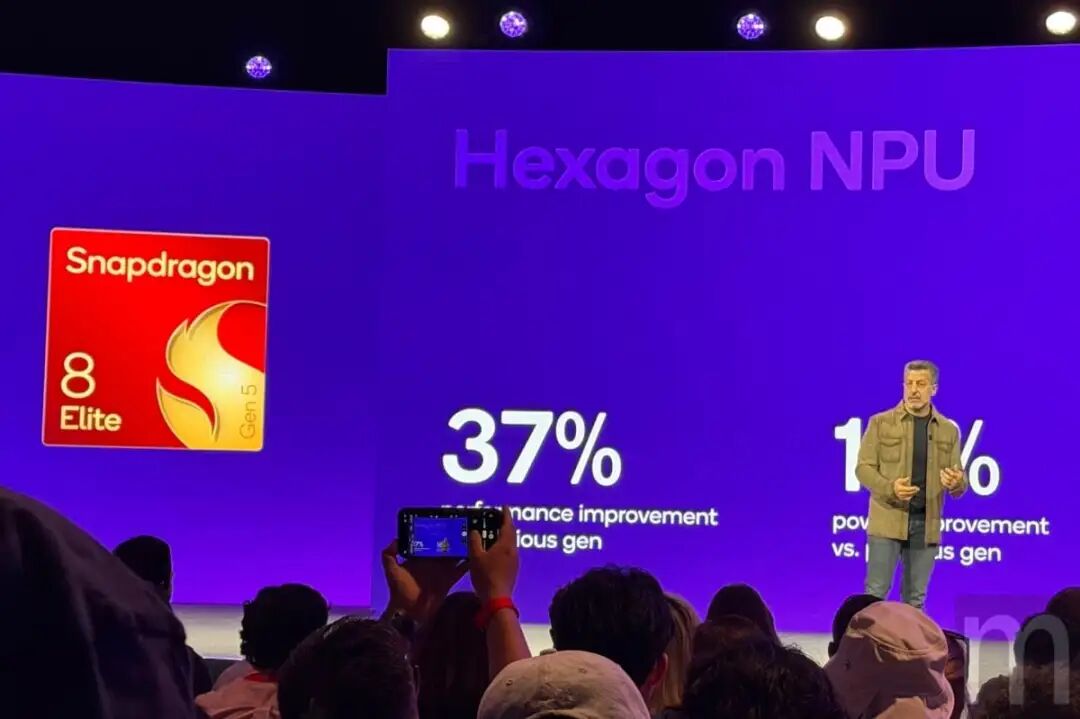

Image source: Qualcomm

For example, the fifth-generation Snapdragon 8 Elite features a new-generation Qualcomm Hexagon NPU, delivering a 37% improvement in AI performance. It can run 3 billion-parameter large models on-device at a speed of 220 tokens per second and adds support for INT2 and FP8 quantization precision.

Clearly, while older models can receive OTA updates for new software, hardware performance bottlenecks make it difficult for them to run the latest AI features optimally. Therefore, for smartphone manufacturers, launching new devices with stronger computing power is essential to keep pace with the AI technology wave.

In summary, amid sustained memory price increases, if smartphone manufacturers choose to halt new device releases and focus on internet services, they may offset cost pressures in the short term. However, over the longer term, this strategy amounts to voluntarily surrendering their position in product innovation, weakening their brand and technological evolution capabilities, and ultimately undermining future competitiveness.

From the vantage point of industry evolution, the smartphone sector is rapidly advancing into the age of artificial intelligence (AI). Smartphones are no longer confined to being mere hardware gadgets; instead, they have evolved into pivotal conduits for on-device intelligence and gateways to expansive ecosystems. The deployment of AI agent tools, exemplified by OpenClaw, hinges on the relentless iteration and validation processes facilitated by next-generation hardware platforms.

Within this dynamic landscape, the introduction of flagship products emerges as a crucial strategy for smartphone manufacturers. It not only serves as a potent mechanism to sustain their market clout but also as an indispensable pathway to capitalize on AI entry points and forge distinctive capabilities.

What remains unequivocal is that only those smartphone manufacturers who steadfastly adhere to the dual-pronged approach of technological innovation and product excellence amidst cyclical downturns can transcend the transient challenges posed by escalating memory prices. By doing so, they can seize the reins of initiative in the AI era and orchestrate a transformative leap from 'scale-based competition' to 'capability-driven competition'.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving