China Mobile: Navigating Tax Reform Impact—Will Dividend Payouts Stay Consistent?

03/27 2026

03/27 2026

555

555

On March 26, 2026, Beijing time, following the close of the Hong Kong market, China Mobile (600941.SH/00941.HK) unveiled its 2025 annual report and fourth-quarter financial results (as of December 2025). Here are the key highlights:

1. Operating Data: Revenue Growth and Steadily Rising Operating Profit

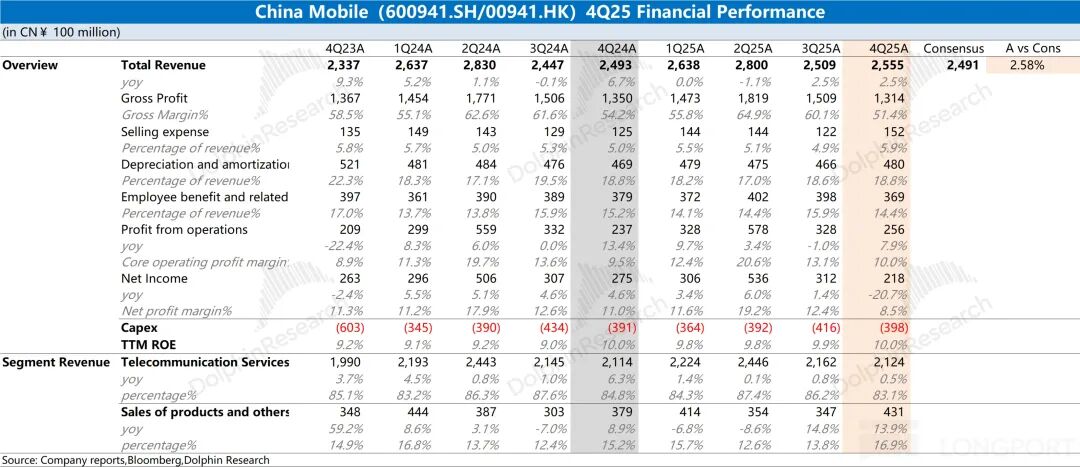

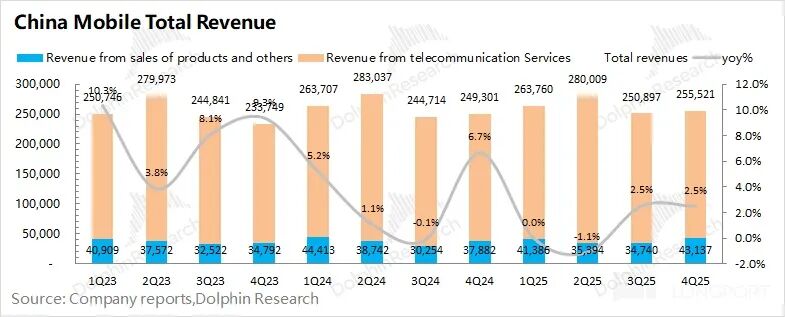

China Mobile's total revenue for the fourth quarter of 2025 reached RMB 255.5 billion, marking a 2.5% increase year-on-year. Communication services revenue saw a slight uptick year-on-year, while product sales and other businesses experienced a 14% year-on-year growth for two consecutive quarters. Operating profit for the same period stood at RMB 25.6 billion, up 8% year-on-year, largely driven by a decrease in operating expense ratios.

2. Core Business Performance: Data Traffic Drives Growth Amidst Price Cuts, Broadband Expands Steadily

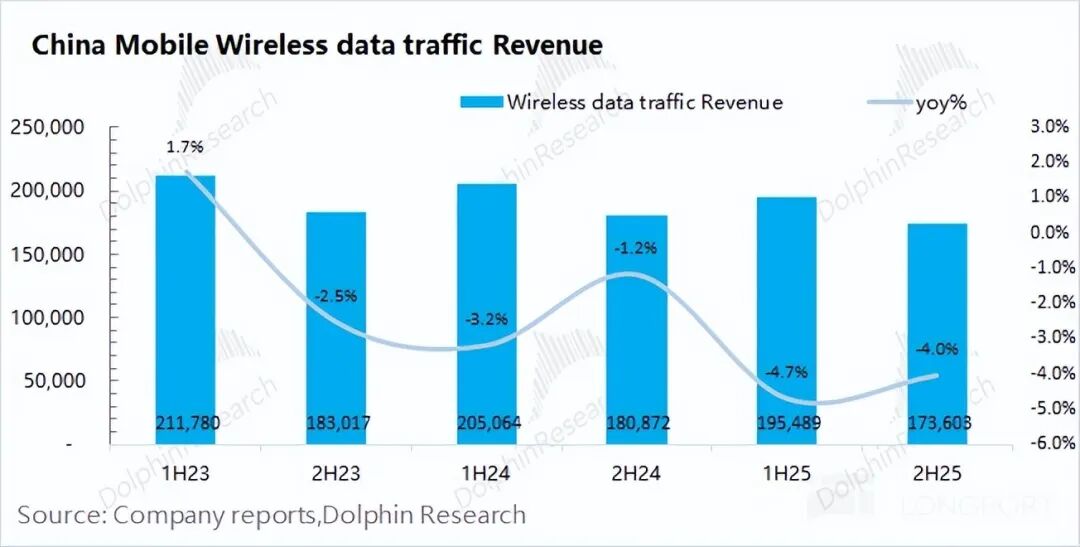

a) Data Traffic Business: The largest revenue contributor, accounting for 40% of total revenue. Data traffic revenue in the second half of 2025 was RMB 173.6 billion, down 4% year-on-year. Despite a 10% increase in data usage volume, the average data tariff dropped by 13% as the company continued its strategy of reducing fees to attract users.

b) Broadband Business: Showed steady growth. Broadband revenue in the second half of 2025 was RMB 73 billion, up 8.6% year-on-year, fueled by an increase in broadband subscribers and higher average monthly revenue per user.

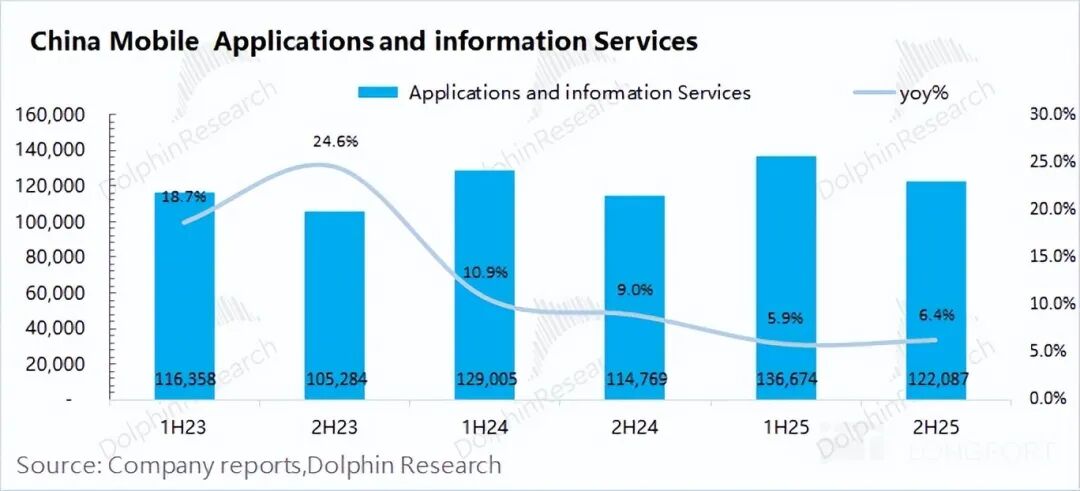

c) Other Businesses: Voice and SMS services declined, while information services maintained growth.

3. Capital Expenditures: Shift from Communication Networks to Computing Power

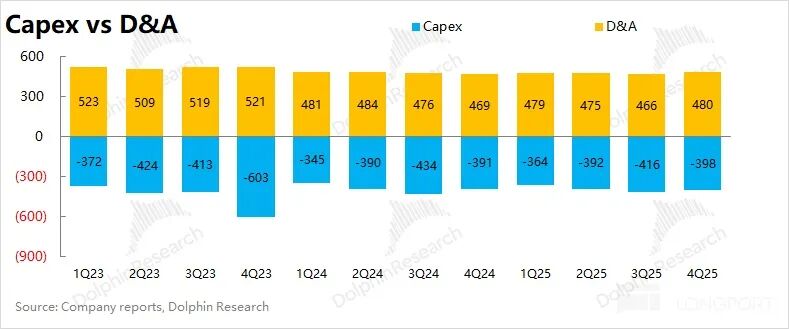

China Mobile's (600941.SH) capital expenditures in the fourth quarter of 2025 were approximately RMB 39.8 billion, roughly flat year-on-year. Looking ahead, the company anticipates capital expenditures of RMB 136.6 billion in 2026, a decrease of RMB 15-20 billion year-on-year. The reduction will primarily target communication network investments, with continued increases in computing power network investments (around RMB 37.8 billion).

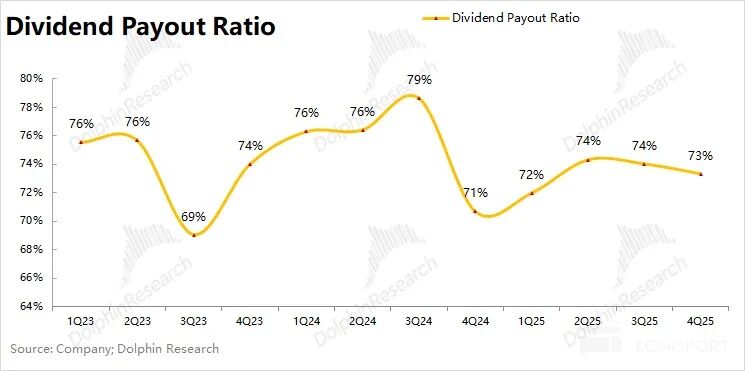

4. ROE and Dividend Payouts: Stable ROE and High Dividend Payout Ratio

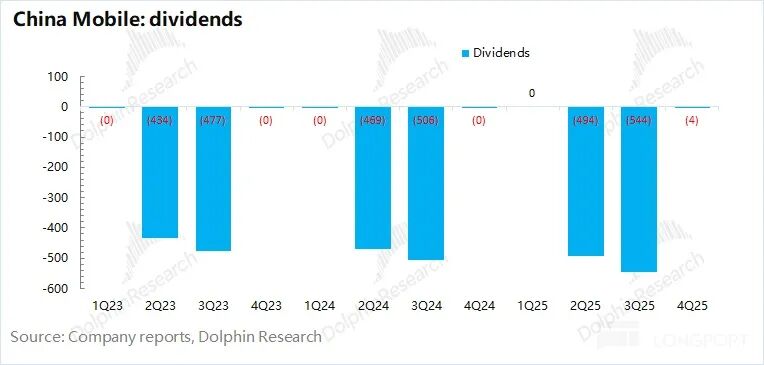

The company's trailing twelve months (TTM) ROE for the quarter was 10%, flat year-on-year. Dividends and share buybacks in the second and third quarters totaled RMB 104.2 billion, with the current dividend payout ratio remaining above 72%.

Dolphin Research's Overall View: High Dividends Persist Despite Tax Hikes, Computing Power Fuels Growth Hopes

China Mobile's performance this quarter largely met expectations, with revenue growth primarily driven by product sales, while core communication services experienced slight growth. The significant decline in profit was mainly influenced by other income, while operating profit increased by 8% year-on-year.

Breakdown of Business Performance:

① Data Traffic Business: Continued its strategy of reducing fees to drive traffic, with average data tariffs falling by 13% in the second half of the year, while mobile subscribers saw slight growth.

② Broadband Business: Maintained around 8% growth in the second half of the year, driven by increases in both subscribers and tariffs.

③ Other Businesses: Information services and product sales grew, primarily driven by computing power services.

While business data remained steady, the market focused on the following aspects:

a) Capital Expenditures: The company's capital expenditures in the quarter were RMB 39.8 billion, roughly flat year-on-year. For 2026, the company plans to spend RMB 136.6 billion, a 9.5% year-on-year decline. The focus will shift from communication networks to computing power networks (around RMB 37.8 billion).

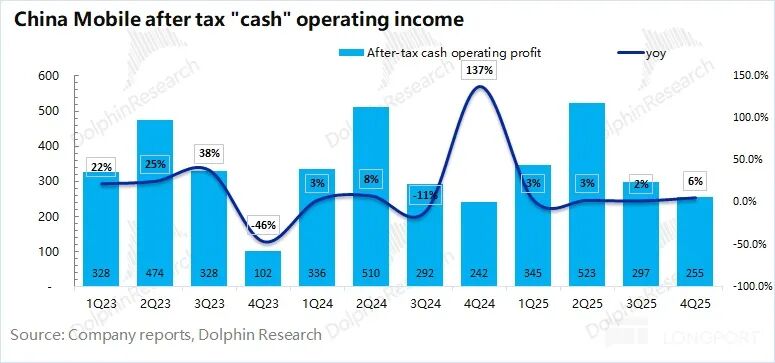

As the high-investment phase of 5G concludes, China Mobile's capital expenditures have significantly decreased. Given the gradual reduction in capital expenditures and still-high amortization and depreciation, the company's cash operating profit will be higher than reported operating profit, indicating greater profitability. Dolphin Research estimates the company's after-tax cash operating profit for the quarter at RMB 25.5 billion, up 6% year-on-year.

b) Dividend Payouts: Typically paid in the second and third quarters, total dividends for 2025 were approximately RMB 104.2 billion, with the estimated dividend payout ratio remaining above 72%.

Overall, China Mobile's operating performance remained stable this quarter, with the decline in net profit primarily influenced by other gains and losses. Considering the impact of the new value-added tax (VAT) policy starting in 2026 (effective January 1, 2026), which upgrades data traffic, SMS, and MMS services from 'value-added telecom services' to 'basic telecom services,' the corresponding VAT rate will increase from 6% to 9%.

Given the proportion of data traffic, SMS, and MMS services in the company's revenue, market expectations suggest the VAT increase will impact total revenue by approximately 1-2%. Under the current strategy of reducing fees to drive traffic, it remains challenging to pass these costs on to downstream consumers, with a profit impact of around 5-7%.

In this financial report, the company continued to reduce capital expenditures, steadily improved ROE, and maintained a relatively high dividend payout ratio. The company retains its attributes of 'stable performance' and 'high dividends.' The VAT adjustment will affect all three major telecom operators (China Mobile, China Telecom, and China Unicom) as an 'industry-wide impact,' posing a 'one-time' shock to 2026 earnings growth and slightly weakening the company's dividends (by around 5%).

As a data traffic provider, China Mobile continues to see steady growth in annual data usage, indicating a stable business. The VAT increase is an industry-wide issue for telecom operators, moderately weakening performance but remaining manageable. Before significant growth in data centers and AI, even with a partial reduction in dividend payouts, China Mobile still offers a dividend yield above 6%, making it a viable option for 'dividend stock' investors.

Below is a detailed analysis:

I. Operating Data: Steady Growth

1.1 Revenue

China Mobile's total revenue in the fourth quarter of 2025 was RMB 255.5 billion, up 2.5% year-on-year. Breaking it down, revenue from communication services was RMB 212.4 billion, up 0.5% year-on-year, while revenue from product sales and others was RMB 43.1 billion, up 14% year-on-year.

The company's communication services revenue saw slight year-on-year growth this quarter, with personal communication services declining by 4% while home and enterprise services maintained around 9% growth.

For personal communication services, which account for over half of total revenue:

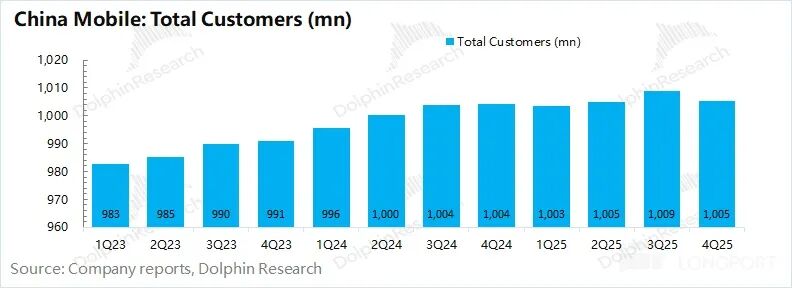

① Mobile Subscribers: The company's total user base remained above 1 billion, with a slight sequential decline.

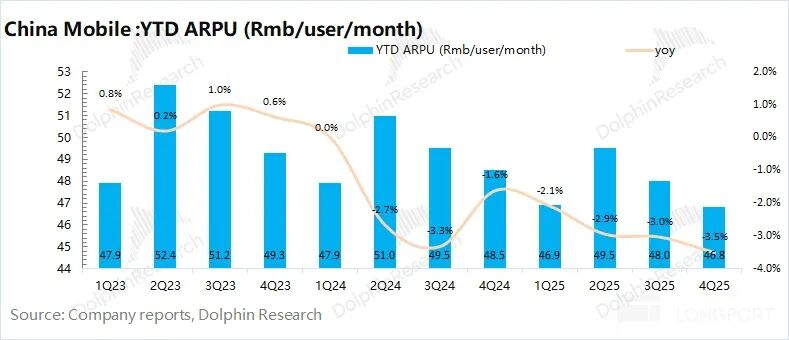

② Mobile ARPU: The average monthly revenue per user was RMB 43.2 this quarter, down 4.5% year-on-year. Over the past year, the average monthly revenue per mobile user has shown a declining trend.

2.2 Gross Margin

China Mobile's gross margin in the fourth quarter of 2025 was 51.4%, down 3.8 percentage points year-on-year. Dolphin Research categorizes 'network operations and support costs' and 'product sales costs' as operating costs to calculate gross profit and margin.

Compared to product sales, the company's communication services have a relatively high gross margin. However, the increased proportion of product sales-related businesses this quarter 'dragged down' the overall gross margin.

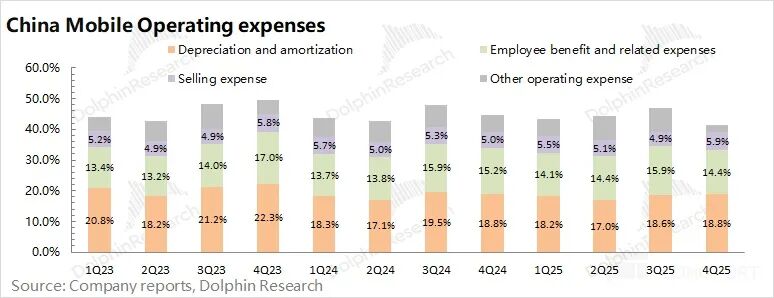

2.3 Operating Expenses

China Mobile's operating expenses in the fourth quarter of 2025 were RMB 105.9 billion, down 4.9% year-on-year. Dolphin Research includes 'sales expenses,' 'employee compensation expenses,' 'depreciation and amortization,' and 'other operating expenses' in operating costs.

1) Sales Expenses: RMB 15.2 billion this quarter, up 21.5% year-on-year. The company increased marketing investments in existing operations and customer service.

2) Employee Compensation Expenses: RMB 36.9 billion this quarter, up 2.2% year-on-year, with increased focus on core talent and frontline staff.

3) Depreciation and Amortization: RMB 48 billion this quarter, down 2.7% year-on-year. With the conclusion of the 5G investment peak, the company's capital expenditures have gradually declined, leading to a sustained reduction in depreciation and amortization.

2.4 Net Profit

China Mobile's net profit in the fourth quarter of 2025 was RMB 21.8 billion, down 21% year-on-year, primarily influenced by other gains and losses. Due to the impact of the VAT increase starting in 2026, the company made 'adjustments to package revenue splitting for tax purposes' this quarter.

Given that the company's depreciation and amortization exceed capital expenditures, from a cash flow perspective, the company's after-tax cash operating profit for the quarter was RMB 25.5 billion (excluding non-operating factors), up 6% year-on-year.

II. Business Segment Performance: 'Reducing Fees to Drive Traffic' Remains the Primary Strategy

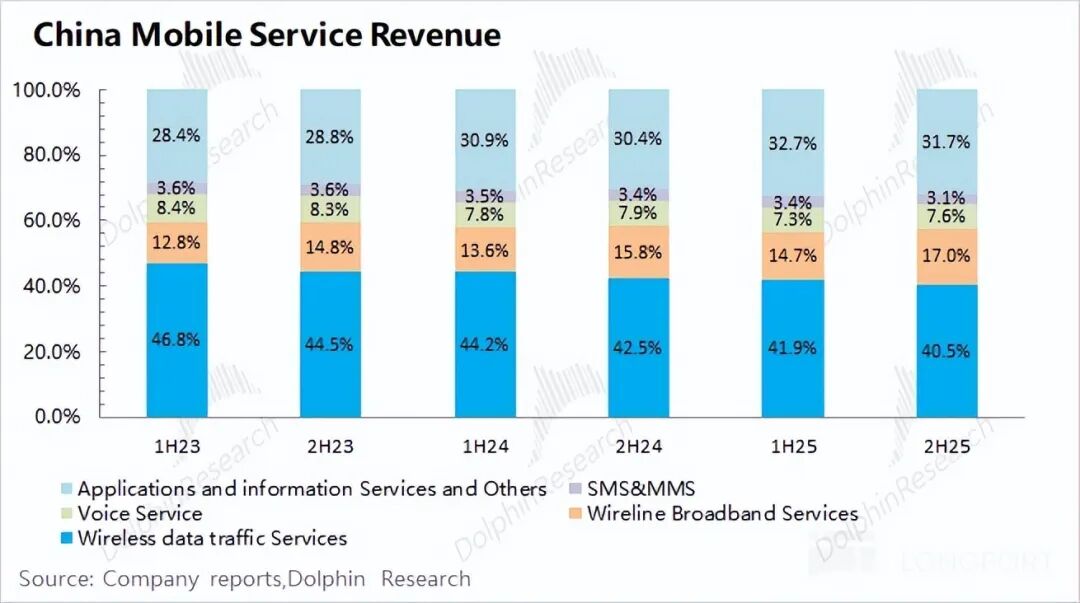

China Mobile's revenue primarily comes from communication services and product sales, with communication services accounting for over 80% long-term. Therefore, changes in revenue and business performance are mainly driven by communication services.

Within communication services, wireless data traffic services currently contribute the most revenue, at 40.5%. Under the strategy of reducing fees to drive traffic, the revenue share of data traffic services has shown a declining trend. Other segments include broadband services, voice services, SMS services, and application and information services.

2.1 Wireless Data Traffic Business

China Mobile's data traffic revenue in the second half of 2025 was RMB 173.6 billion, down 4% year-on-year. Driven by demand for short-form video, data usage continued to increase, but unit tariffs declined, leading to a further decline in data traffic revenue.

Breaking it down, total wireless data traffic usage by China Mobile users in the second half of the year reached 96.1 billion GB, up 10.3% year-on-year, while the average data tariff was RMB 1.8/GB, down 13% year-on-year. Despite sustained growth in data demand, the company continued to reduce user data tariffs.

2.2 Broadband Business

China Mobile's broadband revenue in the second half of 2025 was RMB 73 billion, up 8.6% year-on-year. The company's broadband business continued to grow, primarily driven by an increase in market share.

As of the end of December 2025, the company's broadband subscriber base grew to 324 million, up 3% year-on-year. This implies an average monthly revenue per broadband user of RMB 37.6, up 4.6% year-on-year.

- END -

// Reprint Authorization

This article is an original work authored by Dolphin Research. Any reprinting is strictly prohibited without prior authorization.

// Disclaimer and General Disclosure Notice

This report is crafted exclusively for general data reference and is intended for the use of readers affiliated with Dolphin Research and its associated institutions. It does not consider the unique investment goals, preferences for investment products, risk tolerance levels, financial circumstances, or particular needs of any individual recipient. Investors are advised to consult with independent professional advisors before making any investment decisions based on the content of this report. Any investment decisions made based on the information provided herein are undertaken at the investor's own risk. Dolphin Research disclaims any direct or indirect liability or losses that may result from the utilization of the data contained in this report. The information and data presented in this report are sourced from publicly available materials and are provided solely for reference purposes. While Dolphin Research endeavors to ensure the reliability, accuracy, and completeness of the relevant information and data, it does not provide any guarantees in this regard.

Under no circumstances shall the information mentioned or views expressed in this report be considered or construed as an offer to sell securities, an invitation to buy or sell securities, or as advice, solicitations, or recommendations regarding relevant securities or related financial instruments in any jurisdiction. The information, tools, and materials contained in this report are not intended for distribution to, or use by, any person in any jurisdiction where such distribution, publication, provision, or use would contravene applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliated companies to any registration or licensing requirements in that jurisdiction.

This report solely reflects the personal opinions, insights, and analytical methods of the relevant authors and does not represent the official stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is exclusively owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to any other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving