The World is Re-evaluating China's Chips

05/11 2026

05/11 2026

590

590

Author|Liu Jingfeng

The global semiconductor industry is standing at a historic peak.

The Philadelphia Semiconductor Index has surged 65% since the beginning of the year, outperforming all expectations.

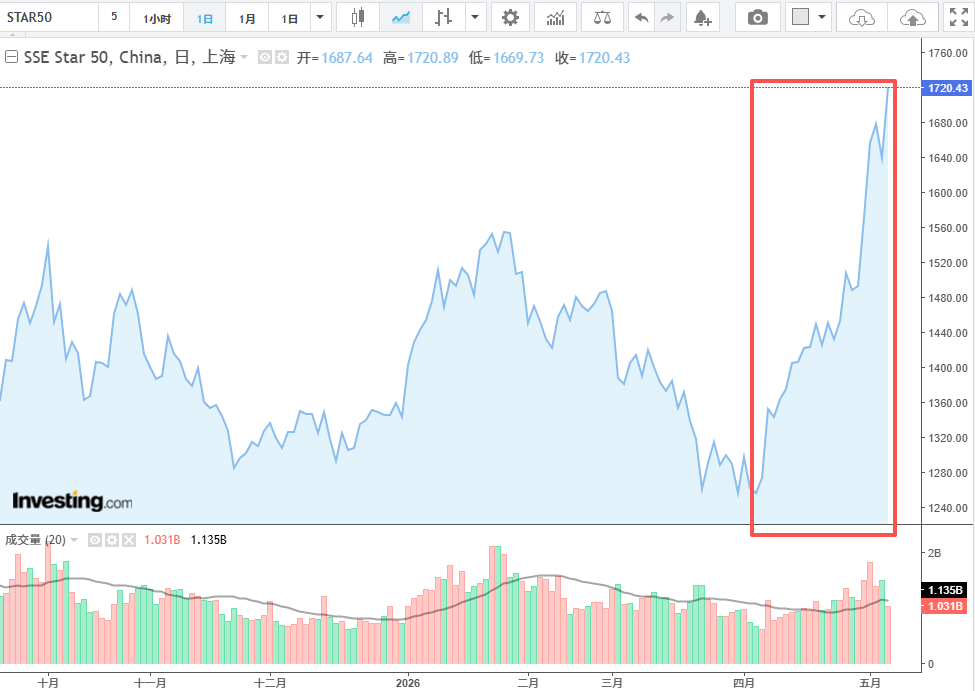

In Asia, this growth is equally remarkable: South Korea's Composite Stock Price Index, which rose 75% last year, has climbed another 76% this year, hitting a new high of 7,816 points today. In China, the K-line of the Science and Technology Innovation 50 Index is following a steep upward trajectory, gaining 35% in a month, with countless AI and semiconductor companies experiencing multiple consecutive trading days of limit-ups or sharp increases.

Figure Caption: Data Flow Chart of China's Science and Technology Innovation 50 Index

The stock market's performance is just the beginning. Beyond it, China's memory chips and AI inference chips are transitioning from domestic substitution to international expansion, with China's integrated circuit export volumes hitting record highs for three consecutive months, surging 84.92% year-on-year in March.

Faced with these changes, overseas markets are displaying a complex mix of awe and fear towards China's chips: Two renowned investment banks, Morgan Stanley and Goldman Sachs, have recently expressed optimism about China's AI computing power industry, asserting that China's AI chips are on the rise. Meanwhile, the deep integration of DeepSeek V4 with Huawei's Ascend has raised concerns for NVIDIA, the global leader in AI chips.

It should be noted that in the traditional global semiconductor division of labor, China's chip industry has long been confined to low-end manufacturing and passive constraints, with 'choke points' becoming a deeply ingrained label for the industry. However, standing at the dawn of a new industrial cycle, this landscape has been completely rewritten: China's chip industry is rising strongly, seamlessly integrating into and leading the global chip market's upward trend, standing shoulder to shoulder with Europe, the United States, Japan, and South Korea at the center of global semiconductor competition.

A wave of Chinese chip exports, triggered by an explosion in AI computing power demand, is on the horizon.

Before this round of stock market surges, some 'unusual' events were already unfolding. The first involves several sets of data.

In April of this year, China's General Administration of Customs released foreign trade data: from January to February, China's integrated circuit exports reached $43.3 billion (approximately RMB 304.6 billion), soaring 72.6% year-on-year, far exceeding the overall Chinese export growth rate of 21.8% during the same period. By March, this growth rate reached a new high, surging 84.92% year-on-year, setting a recent monthly growth record. Among them, ASEAN has become China's largest direct export market for chips, accounting for 29.7% from January to February 2026, with a growth rate as high as 128%. Emerging markets such as the Middle East, Latin America, and Africa have become significant sources of incremental demand for China's chip exports, with growth rates exceeding 89% from January to February 2026.

Over the past few years, integrated circuits have been one of China's key export commodities, but growth rates have been relatively stable: In 2023, affected by a downturn in the global chip industry, China's integrated circuit export value was $135.97 billion, down 5% year-on-year. In 2024, as the chip market recovered, domestic integrated circuit exports rebounded to $159.55 billion, up 17.4% year-on-year. In 2025, this figure rose to $201.9 billion, up 26.8% year-on-year.

A closer look reveals that the significant increase in integrated circuit export value was driven not by export volume but by average price. According to data released by the General Administration of Customs, China's integrated circuit export volume increased by only 13.7% in the first two months of this year, but the average unit price rose by 52%.

'Increasing volume and price' is the most direct market language of industrial upgrading, a signal that has rarely appeared in China's chip export data over the past five years.

Of course, behind the price increases, on the one hand, overseas markets are experiencing a shortage of memory and AI chips; on the other hand, and more importantly, Chinese chips have begun to gain competitiveness overseas. This, in turn, indicates that China's chip exports have made substantive progress in transitioning from 'low-price, high-volume' to 'high-value-added output.'

The second event comes from a technical document.

On April 24, the domestic large-scale model DeepSeek released its V4 version. In the official technical report, there was a seemingly mild statement: 'We have validated the fine-grained EP (Expert Parallelism) scheme on both NVIDIA GPUs and Huawei Ascend NPUs.'

This understated remark sounded the clarion call for domestic chips to enter the AI large-scale model arena. On the day of DeepSeek V4's release, multiple domestic chip manufacturers, including Huawei Ascend and Cambrian, completed efficient adaptation of the V4 model and open-sourced the adaptation code to the GitHub community. Among them, Huawei Ascend's entire line of super node products supports the V4 series models, while Cambrian completed Day 0 adaptation of two versions of the V4 model based on the vLLM inference framework.

Over the past decade, the 'hardware validation list' for global top-tier AI models has been an unspoken power ranking—with NVIDIA always at the top and Chinese companies either absent or listed at the very bottom. This time, Huawei Ascend and NVIDIA were written side by side in the same line.

Previously, Reuters reported on this, revealing a more symbolically significant detail: Before releasing V4, DeepSeek did not follow the usual practice of prioritizing adaptation windows for NVIDIA and AMD but instead gave the opportunity to Huawei weeks in advance. The report was brief but forceful: 'breaking from standard industry practice'—breaking industry norms.

DeepSeek even previewed in a footnote that after the batch launch of Ascend 950 super nodes in the second half of the year, the price of V4-Pro would be 'significantly reduced.'

This implies that domestic chips are not just 'usable' but 'highly effective' in large-scale model inference.

As early as the end of 2025, Wang Jian, CEO of Huawei Korea, announced that in 2026, AI computing power products centered around the Ascend 950 would be exported to South Korea—a global semiconductor powerhouse home to 86 semiconductor-related enterprises, including Samsung and SK Hynix. This move prematurely pull open (lākāi, meaning 'kicked off') the international expansion of Ascend chips.

The third event comes from two reports.

On the evening of April 29, Cambrian released its Q1 2026 financial report: revenue reached RMB 2.885 billion, up 159.56% year-on-year; net profit was RMB 1.013 billion, up 185.04% year-on-year. Subsequently, a series of financial reports from Hygon Information and the memory sector were released, placing the profitability of the domestic computing power chain in black and white for all to see.

Just before Cambrian's financial report, on April 26, Morgan Stanley released an 82-page in-depth report titled 'China's AI Accelerators—Who Will Stand Out,' systematically covering three leading domestic AI chip companies—Cambrian, Iluvatar CoreX, and MetaX—for the first time, providing clear ratings and target prices, and outlining the ultimate roadmap for the localization of China's AI computing power over the next four years: by 2030, domestic AI chip self-sufficiency will reach 86%, with a potential total market size of $67 billion.

Morgan Stanley believes that with the global explosion of AI agents, inference computing power will become the absolute mainstay, with inference demand 4.5 times that of training, accounting for over 70% of overall computing power demand. Chinese chips already have advantages in inference energy efficiency and cost per token.

In 2025, the global inference chip market size exceeded $80 billion, with China accounting for nearly 40%. Among this, the domestic market share of domestic AI chips rose from 35% in the first half of 2025 to 46% in the second half, and is expected to exceed 50% in 2026, while domestic AI chips will also officially embark on large-scale international expansion.

A week later, renowned investment bank Goldman Sachs released two research reports on Cambrian and Inspur Information, stating that the domestic AI chip supply chain is transitioning from catching up with foreign products to independently meeting the demands of domestic internet giants. This signifies its recognition of the judgment that 'domestic AI chips are rising' in China.

When Wall Street starts to change its tune, this story is no longer just about China.

Stock market surges and investment bank reports can easily be dismissed as market sentiment.

But sentiment cannot explain changes in industrial data. The export of Chinese chips is primarily supported by three categories: memory chips, AI peripheral chips, and automotive chips.

Global memory chips are the key to understanding this transformation.

Over the past year or so, the global memory market has undergone a structural dislocation.

In early 2025, DeepSeek's overnight success sparked a new global competition in AI large-scale model applications. Model applications triggered an explosion in inference demand, leading to strong demand for high-bandwidth memory (HBM) in AI servers, causing giants like Samsung and SK Hynix to shift production capacity towards high-end products, creating a supply vacuum for consumer-grade memory (such as DRAM and NAND flash memory used in smartphones and PCs).

Subsequently, global memory chip prices began a crazy (fēngkuáng, meaning 'frenzied') round of price hikes. According to data from semiconductor research firm TrendForce, DRAM contract prices surged 80%-90% quarter-on-quarter in Q1 2026, while NAND flash memory contract prices rose 55%-90% quarter-on-quarter.

At this precise moment, domestic memory chip manufacturers ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies Co. (YMTC) crossed the technical yield threshold (with CXMT's DDR5 and YMTC's 3D NAND yields both exceeding 85%), enabling large-scale shipments and allowing them to capitalize on the global memory chip price surge, further expanding their global market presence. By the end of 2026, CXMT's production capacity is expected to cover 15% of global DRAM memory demand, while YMTC's global NAND market share has already reached 13%.

Thus, this is not merely luck but rather a precise alignment of timing—technology was ready just as the market needed it.

Beyond memory chips, the AI peripheral chip sector is quietly becoming a major business.

In the grand narrative of AI chips, the global spotlight is fixed on NVIDIA's H200 and B200, and TSMC's 3nm process, as if controlling high-end GPUs alone could lock down China's AI chip progress. However, an AI server requires not just top-tier computing chips but also hundreds of power management chips, high-speed interface chips, and signal transmission chips. These chips are not on export control lists but are indispensable parts of AI infrastructure—every additional AI server increases demand for such supporting chips.

Chinese manufacturers have quietly achieved global substitution in these areas.

For example, according to a May 6 report by Jiemian News, a large number of overseas AI power and optical communication companies are mass-procuring domestic MCU chips to meet surging demand for computing power and AI power supplies. In the discrete semiconductor device sector, China has become a global manufacturing base and the largest market for discrete semiconductors. In data transmission, domestic company Montage Technology's DDR5 memory interface chips and PCIe Retimers now stand alongside U.S.-based Rambus and Japan's Renesas in a tripartite market balance.

The international expansion of automotive chips has adopted the most covert 'embedded' approach. In Q1 of this year, China's automotive chip exports surged 67%. Behind this, on the one hand, the international expansion of new energy vehicles is driving automotive chip exports; on the other hand, overseas automakers are increasingly collaborating with Chinese automotive chip companies. For instance, Japanese automakers, which have long relied solely on their own or Western chips, announced in April that they would adopt Horizon Robotics' ADAS chips in their main models, with these vehicles being sold in markets such as Europe, the U.S., and Southeast Asia. Starpower Semiconductor's IGBT chips are penetrating the supply chains of traditional European automakers, replacing Infineon—a testament to recognition deeper than just price, given the typically stable nature of automotive supply chains.

This raises the biggest question: Over the past few years, China's mainland chip industry has been under constant external pressure and 'choke points,' so why has it suddenly succeeded?

It should be clarified that overseas, particularly U.S., 'choke points' on Chinese chips target two areas: advanced-node chips (7nm/5nm/3nm, high-end AI training chips) and key equipment (EUV lithography machines, advanced photoresists, etc.). These areas, heavily dependent on technological breakthroughs, remain weaknesses in China's mainland chip industry.

However, in mature-node chips, China's mainland has manufacturing advantages. Its production capacity for mature nodes (28nm and above) already accounts for 33% of the global total, with the localization rate of equipment for 28nm and above exceeding 40%.

This breakthrough is essentially China's mainland leveraging its 'ultra-large-scale market + full industrial chain resilience + institutional advantage of concentrating resources to accomplish major tasks' to establish a 'moat' in mature nodes, open up 'new tracks' in AI/memory/automotive chips (the aforementioned memory chips, automotive chips, MCUs, and power management chips all fall into this category), and 'circumbendibly catch up' in advanced nodes, ultimately forming a balanced pattern (géjú, meaning 'landscape') of 'you suppress yours, I develop mine.'

Judging from the reactions of overseas institutions and media, this revaluation is real, but it has clear boundaries.

In fact, at the end of last year, Liu Jinjin, Goldman Sachs' chief China equity strategist, and his team expressed a change in attitude in their report, stating that China's major indices still have a 38% upside potential by the end of 2027, and Chinese tech companies still have room to enhance their valuations and earnings by focusing on AI applications—this represents a starkly different analytical logic from the past framework of 'Chinese stock market being policy-driven and valuations being unreliable.'

However, the boundaries are also clearly defined. Paul Triolo, a partner at the U.S. think tank Albright Stonebridge Group, made an intriguing remark in a CNBC report: U.S. export restrictions have added 'rocket fuel' to China's chip demand.

The implication of this statement is that today's prosperity of China's chip industry is largely driven by sanctions—if Nvidia's chips were available, Huawei Ascend and Cambricon might not have the market space they enjoy today. He also pointed out that 'China is the only country attempting to rebuild almost the entire semiconductor supply chain, which is naturally extremely complex and will require more time to surpass export controls in key areas.'

However, it is worth noting that the global semiconductor industry is currently entering a collective frenzy. The Wall Street Journal pointed out that the Philadelphia Semiconductor Index has surged 54% since the end of March, marking its strongest 25-trading-day performance since the peak of the 2000 dot-com bubble. Goldman Sachs analysts noted that the index has exceeded its 200-day moving average by approximately 50%, representing the most extreme deviation level since 2000; Morgan Stanley has classified semiconductors as one of the 'most historically overbought' sectors.

This also means that the rise in Chinese chip stocks and the surge in exports are occurring amid this global tidal wave—it is currently difficult to precisely distinguish how much of the gains are due to industrial revaluation and how much are due to emotional resonance.

The reality is that China's technological ceiling in high-end chip manufacturing and equipment remains real. Without EUV lithography machines, chip manufacturing at nodes below 7nm can only rely on hard-grinding with multi-patterning techniques, with yields and costs unable to compete head-on with TSMC. This is not a gap that can be bridged in the short term. SMIC has also admitted that breakthroughs in advanced processes 'will take time' under current tool restrictions.

The risk of intense competition in mature processes is accumulating. It is understood that dozens of domestic wafer fabs are set to commence production between 2026 and 2027. If demand growth fails to keep pace with capacity expansion, price wars could erupt at any time—the historical scenario of 'winning market share but losing profits' in the solar and display panel industries could potentially repeat in the semiconductor sector.

The threat of trade barriers is escalating. In early April this year, bipartisan lawmakers in the U.S. Congress jointly proposed the 'Multilateral Alignment for Coordinated Technology Hardware (MATCH) Act,' attempting to fundamentally cut off China's access to key equipment for building advanced semiconductor manufacturing capabilities by mandating coordinated actions with allies. This legislative move marks a comprehensive escalation and paradigm shift in Congress's strategy for semiconductor export controls toward China.

Additionally, overseas markets are also accelerating the construction of their chip industries. Southeast Asia, in particular, is emerging as a new semiconductor landscape: Singapore and Malaysia form the first tier, with the former focusing on institutions and R&D platforms and the latter advancing into front-end manufacturing and advanced packaging; the Philippines, Vietnam, Thailand, and Indonesia constitute the second tier, establishing advantages in areas such as packaging and testing, wafer manufacturing, and automotive chips. China's capabilities in mature-process chips and breakthroughs in AI inference chips are forming a new symbiotic and complementary ecosystem with these developments.

In the past, the world habitually perceived Chinese chips as 'low-cost imitations'—low-end, cheap, functional but not of high quality. This impression is now being revised.

The revision is slow, but the direction is clear.

Jensen Huang once said that his greatest concern was Chinese companies finding a way to bypass Nvidia. Judging from these signals in the spring of 2026, that path is no longer just a possibility but is being paved brick by brick into reality.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!