Launching the Capacity Battle! NVIDIA Secures $3.2 Billion Deal with Corning

05/11 2026

05/11 2026

590

590

Recently, NVIDIA and Corning announced a multi-year strategic collaboration in both business and technology.

According to the disclosed information, NVIDIA's total investment in Corning is capped at $3.2 billion, divided into two parts: an initial $500 million investment through pre-financed warrants, acquiring 3 million shares of Corning common stock; and a traditional warrant granting the right to purchase up to an additional 15 million Corning shares at $180 per share in the future, corresponding to a potential additional investment of up to $2.7 billion.

NVIDIA CEO Jensen Huang also revealed that, in addition to the equity investment, NVIDIA has paid Corning billions of dollars in advance to secure optical fiber capacity construction. In return, Corning has committed to increasing its optical connection product manufacturing capacity in the United States by 10-fold, expanding optical fiber production by over 50%, and constructing three new advanced manufacturing facilities in North Carolina and Texas.

This collaboration is not an isolated event but a continuation of NVIDIA's systematic optical layout over the past few months. Two months ago, NVIDIA had already invested $2 billion each in Lumentum and Coherent, totaling $4 billion. Previously, NVIDIA had also made multi-billion-dollar procurement commitments to Marvell, a core supplier of optical DSPs. Thus, NVIDIA has completed an end-to-end optical supply chain closed loop (closed loop) covering optical devices, core chips for optical modules, and fiber optic cables.

Following the announcement, Corning's pre-market stock price surged over 20% and closed up 12%, with year-to-date gains exceeding 107%.

To understand why NVIDIA is placing such a heavy bet on optics, one must first recognize the structural impact of AI computing power demand on optical connection infrastructure.

Unlike traditional data centers, AI computing centers handle 'east-west traffic' for parameter synchronization among GPUs, requiring a 1:1 non-blocking network architecture. This has led to an exponential increase in optical fiber consumption. According to CRU data, optical fiber demand in AI data centers has grown by 75.9% annually, with the supply-demand gap widening from 6% to 15%. Optical fiber prices have surged more than threefold in a few months.

From the optical module perspective, LightCounting's latest forecast in March 2026 indicates that the global optical module market will maintain high growth of about 60% in 2026, with 800G optical module shipments more than doubling again. 1.6T module shipments will grow from a small base in 2025 to tens of millions of port levels, and the global optical module market size will approach $60 billion by 2031.

Additionally, Dell'Oro Group data shows that global data center capital expenditures will grow by 57% in 2025 due to accelerated AI deployments, with full-year spending expected to exceed $1 trillion in 2026.

However, the rapid demand growth has encountered rigid supply-side constraints. The optical fiber industry follows a strict 'preform-fiber-cable' pyramid structure, with preform manufacturing accounting for about 70% of industry costs and profits. Production involves complex chemical vapor deposition processes, with impurity levels needing to be controlled at the parts-per-billion level. The complete expansion and yield ramp-up cycle takes 18 to 24 months, making it difficult for manufacturers to quickly release new capacity despite significant price increases.

Corning's newly expanded capacity is expected to gradually commence production by the end of 2027 and reach full production in 2028, with little significant increase in global effective supply in the short term.

Against this backdrop of worsening supply-demand mismatch, NVIDIA has chosen to bypass traditional spot procurement models and directly secure upstream exclusive capacity through multi-billion-dollar long-term agreements, front (front-loading) its ultimate computing power demands to the material manufacturing stage.

As JPMorgan pointed out in its latest research report, this collaboration not only provides financial support but, more importantly, offers Corning's photonics business confirmation of its technology roadmap and long-term demand visibility.

The impact of this event on the optical industry will be profound and multidimensional. From a supply chain model perspective, NVIDIA's move marks a structural shift in the optical communication supply chain from passive matching to proactive capacity locking.

Traditionally, the optical communication industry has stocked inventory based on industry standards, mass-produced, and then matched orders, operating relatively passively with demand highly dependent on telecom operators' investment cycles. However, with the wealthiest end customers now directly involved in upstream capacity construction, deep binding of AI chip manufacturers with upstream optical material capacity is likely to become the new norm, potentially reshaping the competitive landscape between supply and demand.

From an industry landscape evolution perspective, this trend will accelerate the concentration of optical industry profit pools and influence toward the top. Companies like Corning, Coherent, and Lumentum that have secured 'tickets to the giant (giants') ecosystem' will gain long-term orders and capacity expansion funding, while small and medium-sized manufacturers will see significant gaps widen in capacity, yield, and long-term agreement orders.

From a technological impact perspective, NVIDIA is systematically transforming optical products from generic industry components to NVIDIA-defined, partner-exclusive models through capital means. This will profoundly influence the direction of next-generation AI network hardware standards. In the future, optical module and connector manufacturers may face a strategic choice of 'integrating into the NVIDIA ecosystem or being marginalized' at the highest-value core layers of AI networks.

As the scale and number of AI factories continue to rise, optical connections are no longer an underestimated supporting element in data center infrastructure but are becoming a key strategic resource determining the expansion speed of AI infrastructure.

Jensen Huang stated in an interview that NVIDIA will expand the application of optical technology on an unprecedented scale, candidly admitting that no optical company has ever operated at such a scale.

This total investment of $3.2 billion, combined with the previous $4 billion in collaborations with Coherent and Lumentum, is propelling the global optical industry into a new era of strategic competition characterized by long-term capacity locking, deep binding, and joint technological research.

-

AI's Richest Person Revealed: A Native of Zhanjiang!

-

No one dares to bet big on Seres' financial report

-

Standing at a Distance, Behind Xiaomi's Phone Slowdown and Layoffs", "Xiaomi Phone, Declining Sales, Offline Stores, Product Strategy, Comprehensive Ecosystem of People, Vehicles, and Homes", "Accordi

-

![]()

ByteDance Enters Physical AI, Igniting the Second Wave of 'Feast'?

-

![]()

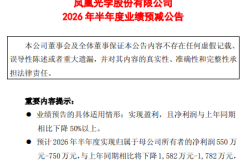

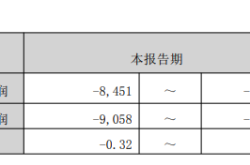

Phoenix Optics Forecasts a Nearly 70% Drop in First-Half Net Profit, Yet Optical Business Profit Shows Growth!

-

![]()

A Staggering 50.16% Reduction in Losses Projected! COST's Interim Report Signals a Pivotal Moment

-

![]()

Nearly 19% of National Total! Guangdong Boasts 164 Registered Large Models as New AI Personification Regulations Take Effect

-

![]()

BYD’s Baosha, Sought After by Australians, Makes a Triumphant Return to China