Alibaba’s Trillion-Yuan Revenue Struggles to Mask Decline as Profits and Cash Flow Tumble

05/28 2026

05/28 2026

657

657

On May 13, Alibaba Group Holding Limited unveiled its financial results for the fourth quarter and the full fiscal year ending March 31, 2026.

Image Source/Company Financial Report

This financial performance report reflects a landscape of both growth and pressure.

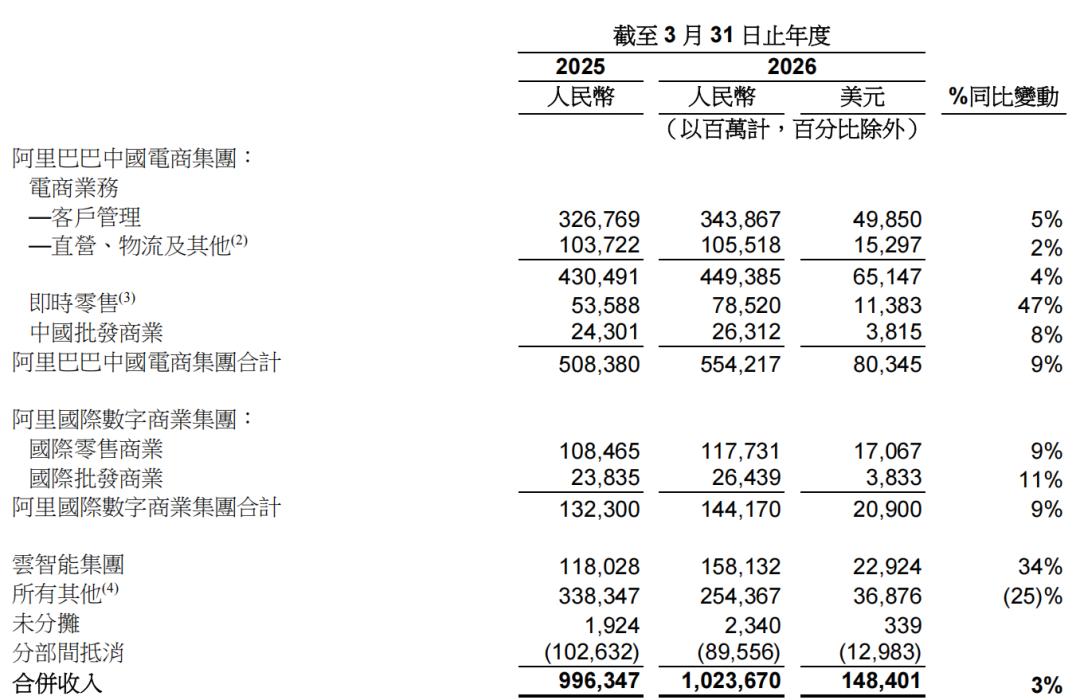

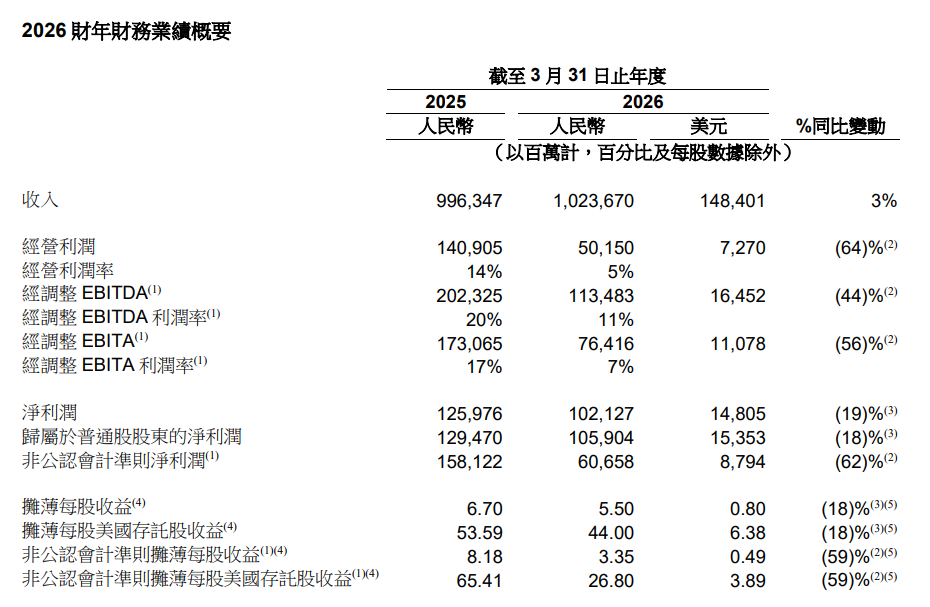

According to the financial report, Alibaba Group's annual revenue for FY2026 surpassed RMB 1 trillion for the first time, reaching RMB 1,023.67 billion. However, net profit for the same period dropped by 19% year-on-year to RMB 102.1 billion.

Net cash generated from operating activities was RMB 76.213 billion, marking a 53% decrease from RMB 163.509 billion in FY2025. Free cash flow shifted to a net outflow of RMB 46.609 billion, in contrast to a net inflow of RMB 73.870 billion in FY2025.

Image Source/Alibaba Official Website

Behind these figures lie a mix of high business growth, driven by instant retail and AI+cloud initiatives, and challenges such as profit compression, talent fluctuations, and intensified competition due to significant investments.

At this crucial juncture of strategic investments, the key focus of external attention is balancing Alibaba's long-term strategic layout with short-term performance.

1 Trillion-Yuan Revenue: Profit and Cash Flow Under Pressure

Alibaba's overall performance in FY2026 faced substantial pressure, with financial challenges including sluggish revenue growth, declining net profit, and cash flow issues.

Financial data indicates that while the company's annual revenue reached RMB 1,023.67 billion, it only grew by 3% year-on-year. Excluding the disposed businesses of Sun Art Retail and Intime, revenue increased by 11% on a like-for-like basis.

Specifically, throughout FY2026, revenue from China's e-commerce group was RMB 554.217 billion, up 9% year-on-year. Revenue from the Cloud Intelligence Group was RMB 158.132 billion, up 34% year-on-year. Revenue from Alibaba International Digital Commerce Group was RMB 144.170 billion, up 9% year-on-year.

Additionally, revenue from all other businesses (including Hema, Cainiao, Alibaba Health, Hujing Entertainment Group, Gaode, Lingxi Interactive Entertainment, DingTalk, and others) was RMB 254.367 billion, down 25% year-on-year. This decline was primarily due to the disposal of Sun Art Retail and Intime businesses, along with a decrease in Cainiao's revenue.

Image Source/Company Financial Report

The growth of China's e-commerce group, the company's core business, is closely tied to the rapid development of instant retail.

In FY2026, Alibaba's instant retail business revenue was RMB 78.520 billion, up 47% year-on-year, primarily driven by increased order volumes from Taobao Flash Sales, launched at the end of April 2025.

The company stated that from January to March this year, the overall order volume of instant retail was 2.7 times that of the same period last year, with non-dining retail reaching 3 times.

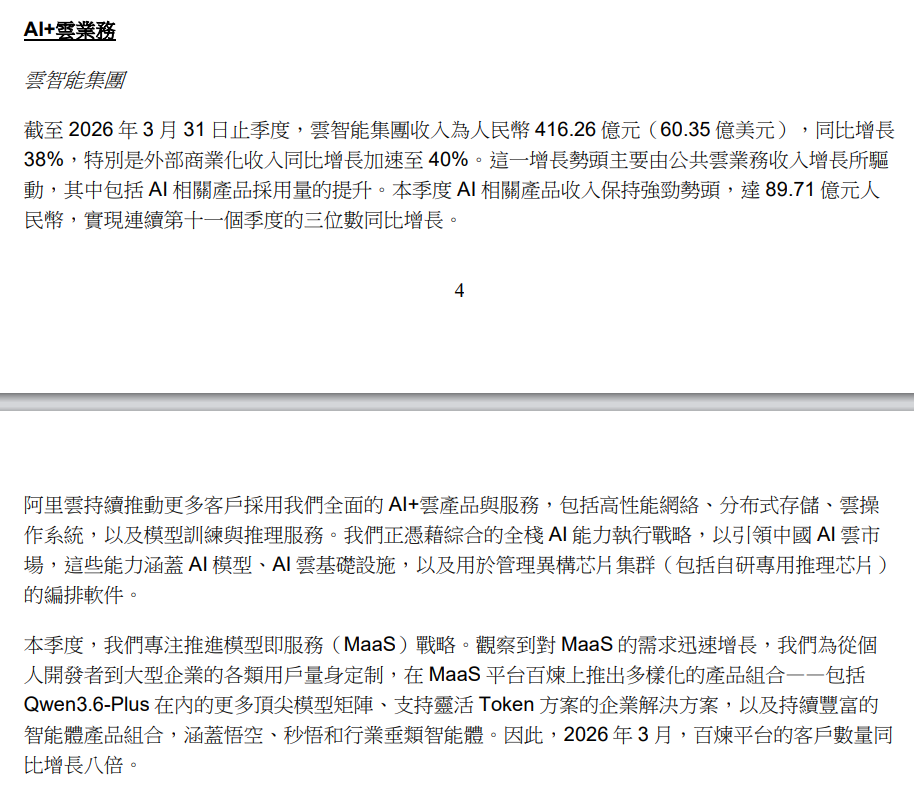

The Cloud Intelligence Group, powered by AI, emerged as Alibaba's fastest-growing business segment in FY2026.

Image Source/Company Financial Report

Financial reports show that as of the fourth quarter of FY2026, revenue from AI-related products remained robust, reaching RMB 8.971 billion, marking the eleventh consecutive quarter of triple-digit year-on-year growth, with annualized revenue exceeding RMB 35.8 billion.

In terms of progress, the company's full-stack AI technology includes T-Head's self-developed chips at the foundational level, MaaS model services in the middle, and the implementation and monetization of AI applications for B-end and C-end at the upper level.

Wu Yongming also predicted that in the quarter ending June, the annualized recurring revenue (ARR) of AI models and application services, including the BaiLian MaaS platform, would exceed RMB 10 billion, and RMB 30 billion by the end of the year. "The high-profit margin advantage of this revenue stream is gradually becoming apparent and will be a pillar of our healthy and high-quality revenue growth in the future."

However, the growth of these two major businesses is underpinned by substantial investments by Alibaba.

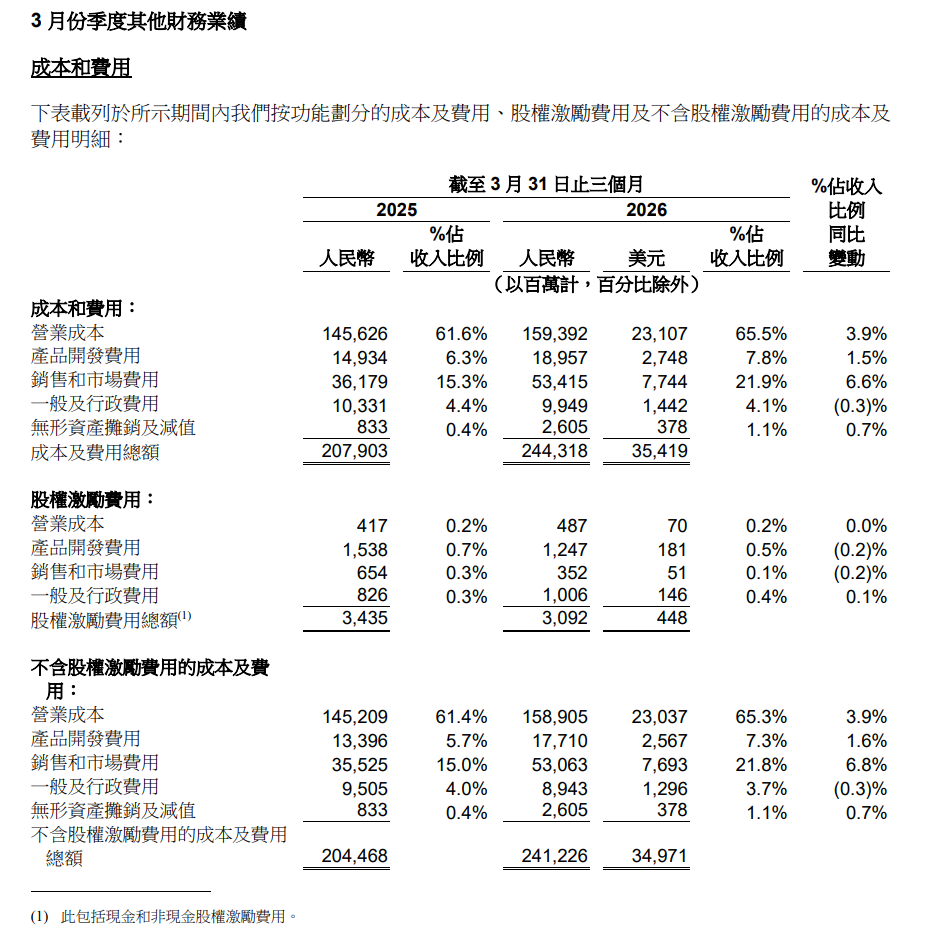

In FY2026, Alibaba's selling and marketing expenses reached RMB 245.023 billion, up approximately 70.13% year-on-year, with the proportion of revenue increasing from 14.5% in the same period of FY2025 to 23.9%.

Image Source/Company Financial Report

Among these, selling and marketing expenses in the fourth quarter were RMB 53.415 billion, up approximately 47.6% year-on-year. The financial report attributed this to investments in user acquisition for instant retail and QianWen APP.

Moreover, when releasing the second-quarter results of FY2026 in November 2025, the group stated that over the past four quarters, Alibaba's capital expenditures in AI+cloud infrastructure were approximately RMB 120 billion.

Under these massive investments, Alibaba's profits were significantly compressed, and cash flow came under pressure.

Financial reports show that in FY2026, Alibaba's net profit attributable to ordinary shareholders was RMB 105.904 billion, down 18% year-on-year. Non-GAAP net profit was RMB 60.658 billion, down 62% from RMB 158.122 billion in FY2025.

Image Source/Company Financial Report

Annual net cash from operating activities was RMB 76.213 billion, a significant year-on-year decline of 53%. Operating cash flow in the fourth quarter fell 66% year-on-year. Free cash flow turned from a net inflow of RMB 73.870 billion in the previous year to a net outflow of RMB 46.609 billion, with a single-quarter net outflow of RMB 17.300 billion, indicating a significant cash burn trend.

2 Dual-Wheel Drive Strategy: High Investments for Growth

After becoming an e-commerce giant, Alibaba's e-commerce business growth slowed, and the company urgently needed new businesses and strategies to stimulate traditional e-commerce growth and boost performance.

After some exploration, Alibaba's solution was to implement a "dual-wheel drive" strategy centered on instant retail, AI, and cloud. On one hand, it upgraded consumer service capabilities, using instant retail to create a closed-loop consumption experience across all time slots and scenarios. On the other hand, it strengthened its self-developed technological foundation, driving the commercialization of AI and cloud technologies.

In April of the previous year, Alibaba launched Taobao Flash Sales and positioned it as a primary entry point on the Taobao homepage, along with a large-scale subsidy plan for direct consumer subsidies, logistics development, merchant incentives, and technological investments.

At the same time, the company focused on its AI business, developing the entire AI value chain.

At the AI infrastructure level, the company self-developed T-Head AI chips to provide high-quality computing power support for cloud computing infrastructure and MaaS inference platforms.

In terms of foundational models, it developed the QianWen large model and iterated three versions in nearly three months, while accelerating the layout of specialized models, launching the open-world model HappyOyster for real-time interactive creation and the multimodal model HappyHorse focused on cross-modal understanding and generation.

This inevitably requires substantial financial investments.

According to Xinhuanet, in July 2025, Taobao Flash Sales initiated a subsidy plan worth RMB 50 billion, expected to be used within 12 months for direct merchant subsidies such as store subsidies, product subsidies, delivery subsidies, and commission reductions, as well as consumer benefits through large red envelopes, free order cards, and officially subsidized fixed-price products.

The AI business is also capital-intensive.

Last year, Alibaba mentioned that the company was actively advancing RMB 380 billion in AI infrastructure construction, and in the first quarter of this year, it stated that the RMB 380 billion capital expenditure was conservative and might increase further in the future.

In FY2026, Alibaba's free cash flow significantly decreased due to investments in instant retail and cloud infrastructure, turning from a net inflow of RMB 73.870 billion in FY2025 to a net outflow of RMB 46.609 billion.

Image Source/Company Financial Report

Alibaba has indeed achieved certain returns through such significant investments.

After the release of the FY2026 financial report, Xu Hong, Alibaba Group's Chief Financial Officer, stated, "Our strategic investments continue to translate into business growth. Revenue from the Cloud Intelligence Group continues to accelerate, and AI-related product revenue has achieved triple-digit growth for eleven consecutive quarters. Customer management revenue from China's e-commerce segment grew by 8% quarter-on-quarter on a like-for-like basis, with steady improvements in unit economics and average order value for instant retail. Looking ahead, we are confident in our business and will continue to invest in AI+cloud to strengthen our strategic advantages."

However, it is also evident that the company's performance has been affected.

Due to massive investments in instant retail, user experience, and technology businesses, Alibaba's adjusted EBITA for FY2026 fell by 56% year-on-year to RMB 76.416 billion.

Image Source/Company Financial Report

Even so, Alibaba remains committed to these strategic investments.

Media reports stated that at an internal meeting in early 2026, Alibaba's core management encouraged the team to continue boldly pursuing Flash Sales and not to bear the burden of losses for three years.

Whether the AI business can achieve revenue greater than costs as soon as possible remains uncertain, and the industry faces multiple challenges in terms of competition and talent stability.

3 Intensifying AI Competition and Core Talent Departures

Since 2026, Alibaba's AI core technology team has experienced frequent and far-reaching personnel changes, with a concentrated loss of key personnel from the core R&D team of the Tongyi QianWen large model, compounded by a technical architecture reorganization at the group level, becoming a significant variable in Alibaba's AI strategy advancement.

On March 4, 2026, Lin Junyang, the technical leader of Alibaba's QianWen (Qwen) and Alibaba's youngest P10-level technical expert, announced his departure on social media.

Lin Junyang (File Photo)

Public information shows that Lin Junyang made outstanding technical contributions to Tongyi QianWen, such as leading the development of models like Qwen3.0, which outperformed Llama2-70B, pioneering a multimodal Agent framework to enhance visual/voice understanding capabilities, and promoting the construction of the largest open-source model ecosystem in the Chinese community. His departure is regarded by the industry as a "technical earthquake" for Alibaba's AI team.

Following Lin Junyang, several core members announced their departures, including Yu Bowen, the post-training leader of Qwen, and Kaixin Li, a core contributor to Qwen3.5/VL/Coder. Previously, Hui Binyuan, the head of Qwen Code, had already left and joined Meta in January.

Personnel changes in the core technology team have raised industry concerns about the sustainability of R&D.

On the other hand, although Alibaba has established a full-stack AI layout from chips, computing power, and large models to industry applications, and achieved some revenue feedback, its AI business still lags behind in the face of industry competition.

At the market competition level, although Alibaba Cloud maintains a leading position in the overall AI cloud market, it has been surpassed by competitors in the core incremental track of enterprise-level MaaS.

According to IDC data, Volcano Engine occupies nearly 50% of the market share in terms of public cloud large model Token calls, significantly ahead of Alibaba Cloud. Industry competition has shifted from traditional IaaS infrastructure to fierce competition in model services and application implementation.

This means that Alibaba Cloud faces increasing pressure to catch up in terms of model iteration speed, user experience, and ecosystem activity. At the same time, industry price wars and homogeneous services are squeezing profit margins, making the issue of increasing revenue but not profits in the AI business more prominent.

Moreover, at the business level, the synergy between Alibaba's AI applications and its core e-commerce ecosystem remains at the tool level. Products such as AI shopping assistants and merchant agents have not yet brought significant monetization improvements, and the actual boost of AI technology to the main business's revenue and profits is limited. C-end AI products like the QianWen App are still in the stage of burning money to acquire users.

Alibaba also clearly stated that B-end enterprises have stronger payment willingness, and most inference resources are invested in the commercialization field. C-end businesses, including user acquisition for the

For Alibaba, the fiscal year 2026 marked a pivotal year for strategic decision-making, wherein it opted to prioritize long-term growth over short-term profits. The advent of instant retail has unlocked fresh consumption scenarios, while the integration of AI and cloud computing has fortified its technological bedrock. Nevertheless, the financial strain, core team turnover, and intense competitive pressures within the industry, all stemming from substantial investments, will persist in challenging Alibaba's strategic determination and operational efficiency.

The crux of the matter lies in whether this dual-wheel-driven approach can genuinely transform into sustainable profits and cash flow in the future, thereby breaking free from the cycle of "high investment, low return." The outcome will be instrumental in shaping Alibaba's growth trajectory and industry standing in the ensuing phase.

Source: Consumer Daily - Jinzhao News

Image: Courtesy of Alibaba

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek