From 'Selling Cloud' to 'Selling Tokens': Operators Fully Join the AI Battlefield

06/01 2026

06/01 2026

647

647

Musk once predicted that Tokens would be consumed like data traffic in the future.

Viewed today, this statement is not just an imagination of AI usage but an early description of a new industrial measurement logic. When shifting the focus from operators' 'self-reconstruction' to the broader market, a new industrial landscape driven by Tokens is unfolding.

Author | Dou Dou

Editor | Pi Ye

Produced by | Industry Observer

AI cloud is approaching a milestone turning point.

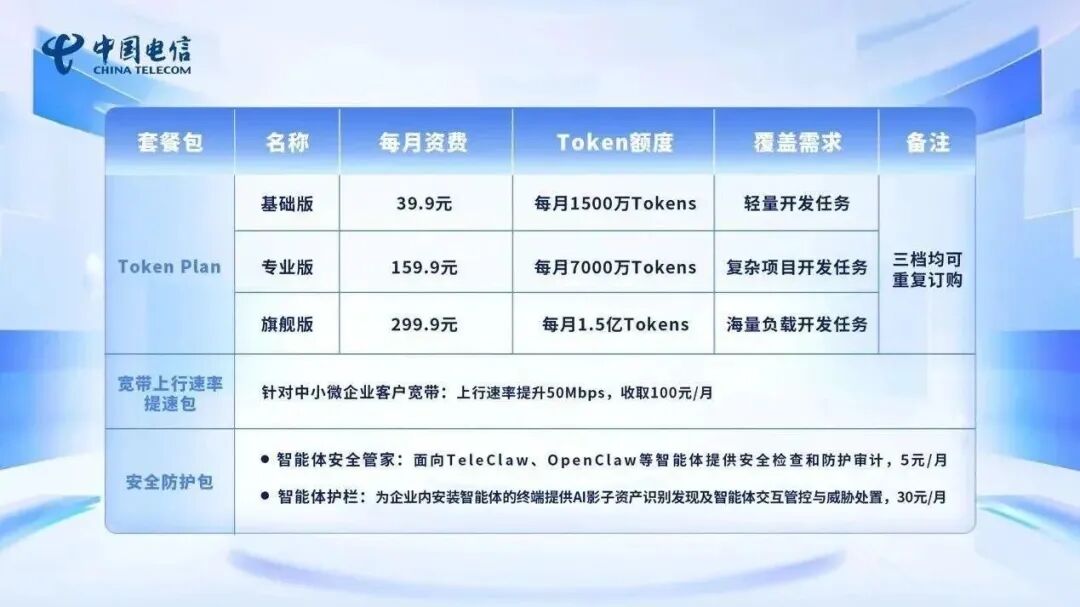

On May 17, China Telecom announced the trial launch of commercial Token packages nationwide. For individuals and families, the lowest package starts at 9.9 yuan/month, including 10 million tokens; for developers and small, medium, and micro enterprises, three tiers are set at 39.9 yuan, 159.9 yuan, and 299.9 yuan, corresponding to 15 million to 150 million tokens per month.

This means that Tokens are succeeding voice, SMS, and data traffic as the fourth fundamental communication service measurement unit for the three major operators. From 'selling data traffic' to 'selling Tokens,' operators are striving to reshape themselves into the 'State Grid' of the AI era.

Behind this transformation lies operators' second identity reconstruction in three decades. The first leap occurred during the cloud computing era, where operators entered the top tier of government and enterprise clouds by leveraging 'controllability, security, and national team' advantages; the second leap is happening now, as they reshape from 'government and enterprise cloud providers' into 'total integrators of AI access services.'

As the curtain rises, a series of ultimate questions about the industry's fate emerge: What game are operators playing? What underlying logic compels their self-revolution? What changes are needed to shift from 'selling cloud' to 'selling Tokens'? How should these changes be implemented? Where will this role reconstruction, rooted in three decades of foundation, ultimately lead operators?

I. Operators Collectively Renovate the 'AI Gateway'

Over the past three decades, operators' trump card has been integrating communication resources. Facing the AI era, this logic is upgrading to integrating AI resources and selling Tokens. To truly implement complex AI capabilities, traditional communication gateways can no longer suffice; they must be renovated into a new entry point through Token packages.

Notably, all three operators have entered the fray, reorganizing their AI service entry points around Token packages.

China Telecom bundles Tokens, connectivity, and security, offering personal and family packages starting at 9.9 yuan/month while setting independent tiers for developers and small and medium-sized enterprises. User entry points are no longer limited to traditional cloud platforms; they can be accessed via the Tianyi Cloud official website, China Telecom App, or the Tianyi AI Cloud Computer with built-in intelligent agents.

China Mobile advances simultaneously at local and group levels. Beijing Mobile launches a 5.99 yuan per-use package and a 24.99 yuan/month package for 10 million Tokens; Shanghai Mobile partners with Tencent to launch the WorkBuddy intelligent agent workstation, where 1 yuan buys 400,000 Tokens, payable directly via phone bills. At the group level, China Mobile releases MoMA, integrating over 300 models and reducing unit Token costs by about 30% through intelligent routing, caching, and Token compression.

China Unicom further upgrades its Token Plan into a combination of 'MaaS + tools + computing power.' Unicom Cloud and Yuanjing provide access to models like DeepSeek and MiniMax for individual users, adopting Credits flexible billing for team versions, serving R&D teams, government and enterprise offices, and industry solutions.

What drives this grand migration from 'connectivity resources' to 'computing power and model resources?'

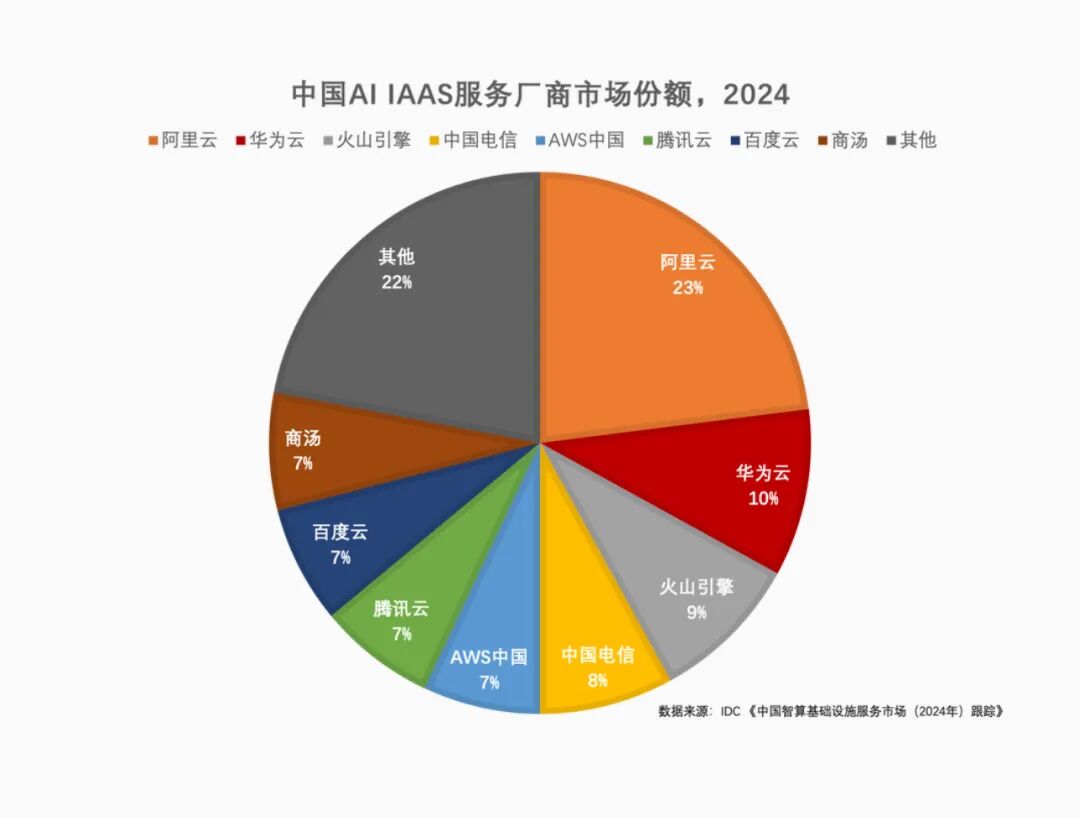

First, consider market positioning. IDC's 2024 China AI IaaS market share shows Alibaba Cloud at 23%, Huawei Cloud at 10%, Volcano Engine at 9%, China Telecom at 8%, and Tencent, Baidu, AWS China, and SenseTime at 7% each. While operators have entered the Top 5, they still lag significantly behind the top tier.

According to Omdia's 'China AI Cloud Market, 1H25,' by the first half of 2025, market share further concentrates among leading cloud providers. Alibaba Cloud leads with 35.8%, followed by Volcano Engine at 14.8%, Huawei Cloud at 13.1%, Tencent Cloud at 7%, and Baidu Intelligent Cloud at 6.1%. Operators have dropped out of the Top 5, meaning their AI cloud market share will continue to dilute unless they develop 'operator-exclusive track' capabilities.

More critically, internet giants have already packaged model services into user-friendly, purchasable plans. For example, Alibaba Cloud's BaiLian offers Token Plans, using Credits to uniformly offset consumption across multiple models; Tencent Cloud's Large Model Token Plan provides four tiers—Lite, Standard, Pro, and Max—with 39 yuan/month buying 35 million Tokens; Baidu Qianfan's Coding Plan offers 40 yuan and 200 yuan subscription tiers.

This indicates that Token packaging is not just a billing method for the developer market but a universal packaging approach for AI services entering the mass market.

Beyond external pressures, operators themselves face a necessary transition.

Data shows that in 2025, China Mobile's revenue reached 1,050.2 billion yuan, up 0.9% year-on-year; China Telecom's operating revenue was 529.6 billion yuan, roughly flat; China Unicom's revenue was 392.2 billion yuan, up 0.7% year-on-year. While the three operators' fundamentals remain robust, growth elasticity is diminishing.

Meanwhile, computing power and intelligent services are emerging as new growth drivers. China Mobile's intelligent computing service revenue surged by 279%, China Unicom's AI business revenue grew over 140%, and all three operators' computing power investment ratios exceeded 30% by 2026. Growth is shifting from traditional communication services to computing power, models, and intelligent applications.

The problem is that AI cloud competition now extends beyond data centers, dedicated lines, and GPUs. It hinges on model capabilities, computing power scheduling, inference costs, developer ecosystems, industry applications, and service responsiveness. If operators remain stuck in the 'resource-selling' phase, they will face simultaneous pressure from internet cloud providers, model companies, and industry software vendors.

Thus, operators must build a new gateway—supporting large models at the top, mobilizing computing power resources at the bottom, and connecting users, developers, and enterprises in the middle through Token packages.

II. From Cloud to AI: What Are Operators Changing?

What does the blueprint for this 'new gateway' entail? For operators, transitioning from 'selling data traffic' to 'selling Tokens' requires integrating which complex industrial elements?

The answer depends on evolving customer needs.

Previously, when enterprises adopted cloud services, they purchased servers, storage, and networks from operators. Now, as enterprises implement AI, they seek not just an isolated model interface but a complete system covering model invocation, computing power scheduling, application access, and unified billing. This compels operators to upgrade from 'cloud shelves vendors' to 'total integrators of AI gateways.'

First, models must be integrated. Multiple general-purpose, industry-specific, self-developed, and third-party models must converge into a unified entry point, enabling enterprises to invoke, switch, and manage models via a single API or platform.

Second, computing power must be integrated. AI computing power is more complex than cloud resources, involving intelligent computing centers, domestic chips, GPU resources, heterogeneous scheduling, cross-regional networks, and inference cost control. Operators must transform computing power scattered across regions, chips, and platforms into a schedulable, billable, and guaranteed computing power network.

Third, applications and intelligent agents must be integrated. Enterprises adopt AI not just to invoke models but to transform business processes. Customer service, marketing, R&D, production, operations, approvals, risk control, and knowledge management are the true endpoints. Models are merely foundational capabilities; only when encapsulated into industry-specific intelligent agents, toolchains, and Skills packages can they integrate into enterprises' daily systems. Thus, operators must provide not just model interfaces but application foundations tailored to government, state-owned enterprises, energy, transportation, finance, healthcare, and education sectors, helping enterprises solve 'how AI truly integrates into business' challenges.

Fourth, billing and operations must be integrated—this is where Token packages truly add value.

Different models, computing power levels, and intelligent agent tasks are difficult to price uniformly. A Q&A session, code generation, document processing, or intelligent agent execution all consume different models and computing power. For enterprises, purchasing, settling, and managing each item separately would raise usage thresholds. Operators must simplify complex resources into straightforward packages, enabling users to focus on quota limits, applicable scenarios, and overage billing without grasping the underlying complexities, thus helping enterprises solve 'whether AI can be scaled operationally' challenges.

In essence, this 'renovation' represents operators' method of reconstructing AI services: using models to open capability gateways, computing power to support foundational supply, intelligent agents to address business scenarios, packages to close commercial loops, and security compliance to uphold government and enterprise clients' trust.

III. Operators: Positioned as the 'Scaffolding' of the AI Era

Deconstructing top-level logic is just the first step. When ideals meet reality, more industry-specific implementation challenges arise: How should operators navigate the vast ecosystem of computing power, models, and applications?

Operators are constructing an end-to-end 'five-layer scaffolding' encompassing model, computing power, application, billing, and security compliance layers.

At the model layer, the core is controlling entry points.

Operators recognize that solely relying on self-developed models cannot fully catch up with leading internet giants, nor is it necessary. Thus, they adopt a 'self-developed foundation + external model aggregation' strategy. China Telecom's Xingchen, China Mobile's Jiutian, and China Unicom's Yuanjing ensure industry adaptability and autonomy; simultaneously, mainstream models like DeepSeek, Tencent Hunyuan, Alibaba Tongyi Qianwen, ByteDance Doubao, Zhipu GLM, and Kimi are integrated into unified platforms.

Take China Mobile's MoMA as an example: Its 'model federation + intelligent routing' shields users from perceiving which model is invoked behind the scenes, with the system automatically distributing tasks based on cost and performance. Essentially, all models are distributed through operators' gateways.

For models to circulate, underlying computing power support is essential. The computing power layer is where operators have the greatest opportunity to build moats.

Operators control East-to-West Computing nodes, backbone networks, dedicated lines, government and enterprise networks, and long-term computing power network construction capabilities—advantages difficult to replicate shortly. This positions them favorably in unified cross-hub, cross-chip scheduling. Operators are connecting heterogeneous resources from domestic chips, existing NVIDIA inventories, and multiple computing power enterprises into a network, forming formidable barriers, exemplified by Tianyi Cloud's 'One Cloud' and China Mobile's 'Xingluo' computing network brain.

Above computing power lie applications and intelligent agents.

To enable customer service, office, marketing, R&D, operations, approvals, and risk control processes to function, operators are standardizing intelligent agent frameworks like MobileClaw, TeleClaw, and Uniclaw, paired with industry-specific Skills packages. This creates an 'AI App Store' for state-owned enterprises and government clients, rapidly integrating AI capabilities into existing office and production systems, thus solving 'how AI enters business' challenges.

For applications to circulate and high frequency (high-frequency), complex invocations to be accounted for clearly, operators leverage their three-decade expertise in billing (Billing) and CRM systems. They introduce mechanisms like 'Tianyi Token Coins,' abstracting consumption across different models and computing power into unified billing units, seamlessly transitioning from 'data traffic packages' to 'Token packages.' This is why Token packages can rapidly roll out nationwide overnight.

The final step in closing the commercial loop is trust.

As 'national teams,' operators naturally dominate state-owned enterprises' computing power pools. Through layered reinforcements of classification protection, indigenous innovation, and trusted data spaces, they fortify 'government and enterprise-reserved tracks' that internet vendors struggle to penetrate.

Today, based on this 'scaffolding,' operators have broadly expanded their capabilities.

For instance, by the end of 2025, China Telecom boasted 43 EFLOPS of self-owned intelligent computing power, 110+ industry large models, 350+ intelligent agents, serving 37,000 clients with an 85% AI penetration rate among central enterprises; China Mobile's intelligent computing scale reached 61.3 EFLOPS, with its MoMA platform aggregating 300+ models and reducing unit Token costs by ~30%; China Unicom is advancing toward 45 EFLOPS, with AI revenue surging 147% year-on-year.

IV. Operators Go All-In on AI in the Token Economy

Musk once predicted that Tokens would be consumed like data traffic.

Viewed today, this statement transcends imagination about AI usage; it anticipates a new industrial measurement logic. When shifting focus from operators' 'self-reconstruction' to the broader market, a Token-driven new industrial landscape is emerging.

Over the past two years, the AI industry's mainstay has been model competition. Larger parameters, stronger inference, and more complete multimodal capabilities attracted market attention. However, as AI enters industrial implementation, competition priorities are shifting. Enterprises now care less about a model's intelligence and more about its ability to integrate into existing systems, process business stably, clarify costs, and enable auditing and management.

The challenge lies in transforming models into daily-usable, continuously purchasable, and risk-controllable production capabilities for enterprises. Low-threshold, purchasable, and quantifiable intelligent capabilities will become essential.

The door refurbished by the operators happens to integrate models, computing power, networks, security, and billing into a single entry point, enabling enterprises to procure intelligent capabilities as easily as purchasing communication services or cloud resources, without the need to re-understand a complex AI technology stack. This is the true industrial value of the Token package. On the surface, it appears as a credit limit, but behind the scenes, it may become the unit of measurement, settlement, and operation for AI services.

It is foreseeable that today's Token resembles a general-purpose package, but in the future, it is likely to further differentiate into an office package for employee efficiency, a developer package for R&D teams, an exclusive model package for central state-owned enterprises and government scenarios, and industry-specific intelligent agent packages for finance, energy, transportation, healthcare, and education.

However, although the prospect of 'buying Tokens as easily as topping up phone credit' is appealing, there is still a long way to go before it truly becomes a reality. Operators still face several tough challenges, such as whether the model performance is good enough, whether the intelligent agents can stably complete tasks, whether the inference costs can continue to decline, whether customers are willing to pay for long-term use, and whether these investments can ultimately translate into substantial revenue.

Therefore, the key to success for operators does not lie in who is the first to launch a Token package or how low the package price is, but rather in whether they can transform 'AI access' into a telecom-grade service that is measurable, billable, operable, and guaranteed. If this step is achieved, operators will no longer be merely sellers of cloud resources, dedicated lines, or computing power pools in the AI industry; instead, they will become trusted infrastructure providers in the process of industrial AI implementation.

By then, AI may no longer be a new technology that requires repeated justification for enterprises; instead, it will become a factor of production that can be accessed, billed, and continuously used, just like water, electricity, and networks.

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek