Kuaishou’s Q1 Report: The Strategic Imperative of Spinning Off Kling

06/04 2026

06/04 2026

518

518

Source | Bohu Finance (bohuFN)

Half a month ago, news broke that Kuaishou is planning to spin off Kling for an independent listing, sending ripples across the industry. Multiple media outlets reported that Kling’s valuation has surpassed $20 billion, roughly two-thirds of Kuaishou’s current market cap of approximately $30 billion.

What truly astonished outsiders was not Kuaishou’s decision to spin off Kling, but the fact that Kling—an AI business established less than two years ago and nurtured within Kuaishou—is now valued nearly on par with its parent company.

This development has placed Kuaishou at a pivotal crossroads between legacy and innovation, though the solution to this dilemma appears to be taking shape.

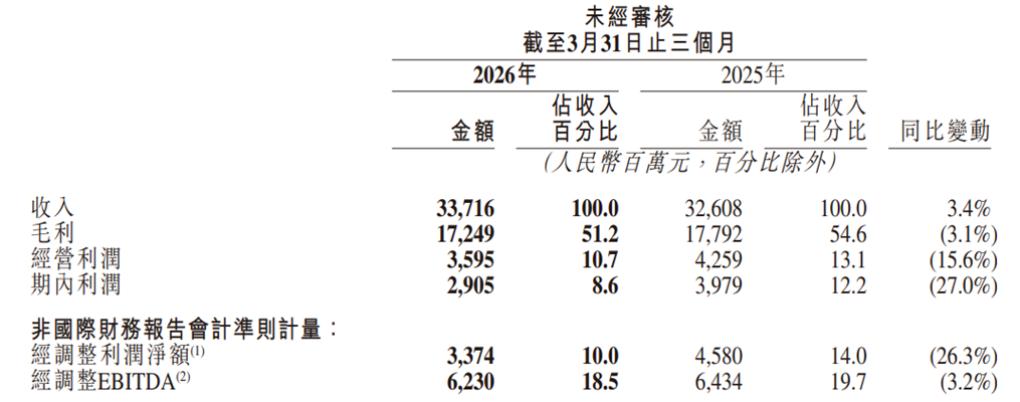

Recently, Kuaishou released its Q1 2026 financial report, revealing total revenue of RMB 33.716 billion, marking a modest year-on-year increase of 3.4%—the slowest growth rate since its listing. Adjusted net profit stood at RMB 3.374 billion, reflecting a significant year-on-year decline of 26.3%, as ongoing AI investments continue to weigh on profitability.

More concerning is the underperformance across Kuaishou’s three core businesses: advertising, live streaming, and e-commerce. Notably, revenue from live streaming—the segment most familiar to its user base—plummeted by 13.5% year-on-year, with its share of total revenue continuing to shrink.

Kuaishou’s traditional businesses are facing a midlife crisis. The true catalyst for market excitement lies with Kling AI, but the substantial investments in AI are eroding the company’s profits. Caught between legacy and emerging businesses, Kuaishou has limited options.

To “rewrite its destiny,” Kuaishou must bet on Kling’s ability to successfully pivot its business trajectory.

01 The Decline of the ‘Three Pillars’

Kuaishou’s Q1 2026 performance was under significant pressure.

The overall business landscape showed a clear divergence: traditional operations weakened, while new AI ventures surged. However, the high-cost AI segment also caused sharp declines in net profit and gross margin, perpetuating a trend of revenue growth without corresponding profit improvements.

A closer look at the financials reveals that each of Kuaishou’s “three pillars” faces unique challenges.

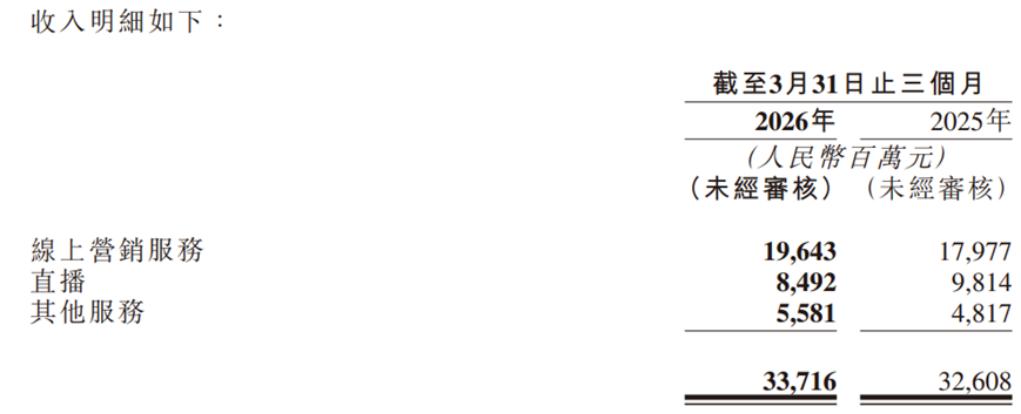

Live streaming revenue was RMB 8.492 billion, a sharp 13.5% year-on-year drop. Over the past year, growth in this segment has continuously slowed, from a 14.4% year-on-year increase in Q1 2025 to negative growth by Q4.

Over the long term, live streaming’s share of Kuaishou’s revenue has also diminished, from 95.3% in 2017 to 38.2% in 2021, and further down to 25.2% in Q1 2026. Live streaming is no longer the platform’s primary growth engine.

Online marketing services (advertising) have emerged as the new pillar business, with Q1 revenue of RMB 19.643 billion, up 9.3% year-on-year. Domestic online marketing revenue grew by over 10%, accounting for 58.3% of total revenue.

However, while advertising revenue exceeded expectations, the growth rate still showed a noticeable slowdown compared to the 12.5% increase for the full year of 2025. The loss of advertisers is becoming a concern that cannot be ignored.

Other services (including e-commerce and Kling AI) generated RMB 5.58 billion in revenue, up 15.9% year-on-year. However, Kuaishou announced that starting from Q1 2026, it would no longer disclose quarterly or annual e-commerce GMV separately, citing alignment with industry practices.

The rationale sounds plausible, but the underlying implication is clear: amid e-commerce sluggishness, if any platform were excelling, it would surely flaunt its GMV.

Moreover, Kling AI generated over RMB 650 million in revenue in Q1, up more than 300% year-on-year. Yet, under this context, revenue from other services still declined compared to RMB 6.295 billion in Q4 2025, indicating even greater pressure on the e-commerce business.

In fact, e-commerce revenue growth has slowed from 78% in 2021 to 15% in 2025. Market analysts believe that GMV growth for Kuaishou’s e-commerce segment in 2026 may drop to the 5%-10% range.

(Figure: Kuaishou’s Q1 2026 financial report)

Behind the slowdown in traditional businesses lies a shakeup in Kuaishou’s core user base.

In Q1 2026, Kuaishou’s average daily active users (DAU) reached 412.7 million, up about 1.2% year-on-year; average monthly active users (MAU) reached 771.7 million, a net increase of approximately 60 million year-on-year.

While the user base is still expanding, growth alone is not enough—the key is whether these new users can be retained and become active.

However, Kuaishou’s DAU grew by only 1.2% in Q1, effectively stalling compared to 410 million users in Q4 2025. The DAU/MAU ratio slipped from 55.0% in Q4 2025 to 53.5%, indicating declining user engagement with the app.

The core of the “Old Railway Economy” (a term referring to Kuaishou’s loyal user base) is a Familiarity Community Culture—an acquaintance-based community culture built on emotional and trust-based connections. However, frequent scandals involving top streamers keep eroding this trust, compounded by tightening regulations on live streaming and a cap on tipping revenue.

For Kuaishou, live streaming, e-commerce, and advertising are highly interdependent. Its loyal user base drives traffic, and once traffic starts to loosen, e-commerce and advertising—both reliant on traffic monetization—will naturally slow down.

Moreover, Kuaishou faces fierce competition from rivals like Douyin, Bilibili, and WeChat Channels, all vying for user attention and advertiser budgets.

Douyin’s e-commerce GMV surpassed RMB 4 trillion in 2025, still growing at over 20%. Bilibili’s advertising revenue jumped 30% year-on-year in Q1 2026, with DAU reaching 115.2 million, up 8% year-on-year. WeChat Channels saw user engagement grow by over 20% year-on-year in 2025.

Telling the “Old Railway Economy” story is becoming increasingly difficult for Kuaishou.

02 The ‘Fire and Ice’ of AI

Against the backdrop of weakening traditional businesses, AI has become the brightest spot in Kuaishou’s financials.

In Q1 2026, Kling AI generated over RMB 650 million in revenue, up more than 300% year-on-year. Additionally, as of March 2026, its ARR (Annualized Recurring Revenue) approached $500 million, up from $300 million in January.

Kling has finally turned a profit, becoming Kuaishou’s new growth narrative amid the decline of the “Old Railway Economy.” But the faster Kling grows, the greater the profit pressure on Kuaishou.

In Q1 2026, Kuaishou’s profit for the period was RMB 2.905 billion, down 27% year-on-year; adjusted net profit was RMB 3.374 billion, a 26.3% year-on-year decline; gross margin contracted to 51.2% from 54.6% a year earlier.

(Figure: Kuaishou’s Q1 2026 financial report)

Where did the profits go? Kuaishou made it clear in its financials.

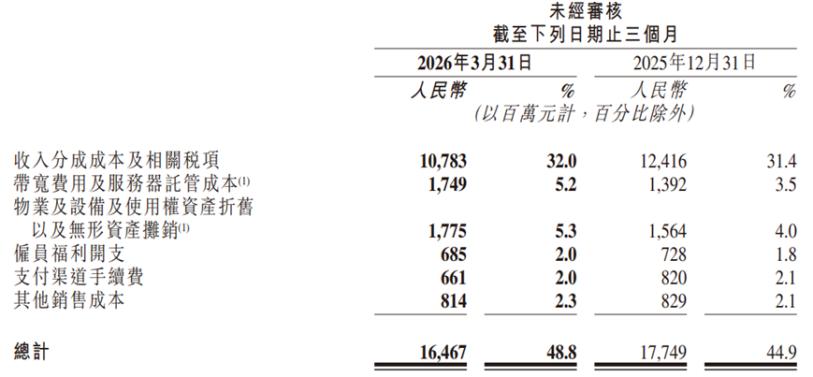

First, on the cost side, sales costs rose 11.1% year-on-year in Q1, far outpacing the 3.4% revenue growth. Bandwidth and server costs, along with asset depreciation, surged—a cost burden from Kling’s aggressive global expansion.

(Figure: Kuaishou’s Q1 2026 financial report)

Additionally, AI investments continue. Q1 R&D expenses were RMB 3.6 billion, up 9.8% year-on-year. Capital expenditures for 2026 are expected to reach RMB 26 billion, an increase of RMB 11 billion from 2025.

While this still lags behind the hundreds of billions in capital expenditures by Alibaba and ByteDance, Kuaishou’s adjusted net profit for 2025 was only RMB 20.6 billion. Before the profits even grow cold, they are fully reinvested into AI, making Kling a true “money pit.”

Understanding why Kuaishou is eager to spin off Kling becomes easier.

First, to ease financial pressure.

Kuaishou’s traditional businesses remain under pressure, but AI is a new story it must tell. It is foreseeable that the stronger the AI business becomes, the more it will erode overall company profits.

Thus, spinning off Kling into a self-sustaining, independently funded entity can satisfy secondary market expectations while allowing Kuaishou to focus limited resources on traditional businesses, benefiting both sides.

Second, Kuaishou and Kling operate on two entirely different narratives and should not be forced into the same basket.

Kuaishou tells a mobile internet story, targeting content consumers in lower-tier markets and pursuing traffic effects. Kling, however, is an AI model company, with 70% of its revenue from overseas markets, primarily serving B-end enterprise clients and P-end professional creators. Their product positioning and user profiles are completely different—they do not share the same ecosystem.

Therefore, Kling must stand alone for capital markets to price it independently of Kuaishou’s influence. At that point, the market will evaluate not just how Kling empowers Kuaishou, but its potential as a large AI model enterprise.

Finally, Kuaishou cannot afford to fall behind in the AI race.

Whether to retain AI talent or secure a better valuation amid a wave of AI company listings, with Minimax and Zhipu having already set precedents, Kling’s listing should happen sooner rather than later.

However, after spinning off Kling, how will Kuaishou tell its next story?

03 Kuaishou Seeks a ‘New Identity’

The most critical variable is whether Kling, as an independent large model company, can justify its $20 billion valuation.

In an optimistic scenario, Kling’s ARR could continue growing and achieve profitability, acquiring a base of highly engaged, high-paying users.

At that point, Kling could become Kuaishou’s greatest asset in its transformation.

In the mobile internet era, the marginal cost of content delivery is low, allowing platforms to rapidly scale and form winner-takes-all ecosystems—a reality that has kept Kuaishou in Douyin’s shadow.

But in the AI era, serving each DAU incurs significant costs. The competitive logic shifts from “how to capture user attention” to “who can complete tasks with the highest engineering efficiency,” presenting an opportunity for Kuaishou to overtake rivals.

For Kuaishou, spinning off Kling for an independent listing means it is no longer just an internal tool empowering Kuaishou’s ecosystem but a content creation platform capable of running a full AI video supply chain in global workflows.

This is the capability content creators value most. Whoever can fully integrate the video production chain, building an industrial ecosystem from creative input to output, holds the true “productivity” that matters in the AI era.

Currently, Kuaishou is charging full speed in this direction. Recently, Kling debuted at the Cannes Film Festival and announced three theatrical-level collaborations, showcasing its industrial-grade delivery capabilities through native 4K output and efficient AI-human collaboration.

Kling’s competitor, Seedance, follows a similar path, leveraging ByteDance’s film and television production tools like Jimeng, Jianying, and Xiaoyunque AI, along with content platforms like Hongguo and Fanqie Novels, to form a complete content ecosystem loop.

However, Kuaishou’s ambitions are grander. It not only has a vast video content ecosystem to support AI video output and implementation but also aims to position Kling as a widely usable “productivity engine,” selling the scarcest productivity asset in the AI era. This is a crucial step in Kuaishou’s transition from a “short-video content platform” to an “AI video infrastructure provider.”

Of course, challenges remain. The biggest concern is whether Kling can break through in the fiercely competitive AI video generation sector. After all, ByteDance has Seedance, Alibaba has HappyHorse, and numerous vertical players are in the mix—the market never lacks competitors.

If so, Kling’s commercialization will remain heavily dependent on Kuaishou’s ecosystem. While AI does drive business growth—for example, Kuaishou’s AI comic drama marketing spend surged over 100x year-on-year in Q1—this alone is unlikely to justify a higher valuation.

Thus, before Kling can truly stand on its own, Kuaishou’s ability to stabilize its core “three pillars” businesses will determine whether it has sufficient resources to wage this prolonged battle.

Regardless, Kling represents a rare opportunity for Kuaishou to “rewrite its destiny.”

Looking back at Kuaishou’s Q1 report, the message extends beyond performance—it clearly tells the market: Kuaishou is ready to adopt a “new identity” and gamble on a future with greater imagination.

Whether the market buys it will determine how much room Kuaishou has to transform.

The cover image and illustrations in this article are owned by their respective copyright holders. If the copyright owners believe their works are unsuitable for public browsing or should not be used without compensation, please contact us promptly, and our platform will make immediate corrections.

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek