Ride-Hailing Giant Earns Less Than One Cent Per Order: What Story Does T3 Go Out Tell as It Prepares for IPO?

06/05 2026

06/05 2026

634

634

A Business Deal Among the Elite

Original content from Digit Economy Studio

Author | Uncle You

T3 Go Out, the third-largest ride-hailing platform in China, has officially launched its IPO process, with its operating entity, Nanjing Lingxing Technology Co., Ltd., submitting a prospectus to the Hong Kong Stock Exchange. T3 Go Out boasts a star-studded shareholder lineup, including three major state-owned enterprises (SOEs)—FAW Group, Dongfeng Motor, and Changan Automobile—as well as two internet giants, Tencent and Alibaba.

This company, seen as the "national team" in the travel sector, reported a profit of RMB 7.44 million for FY2025 (the year ending December 2025) in its prospectus, marking its first annual profit. However, this modest profit masks a heavy reliance on traffic from aggregation platforms and structural challenges in its business model. Now, as it seeks to ride the wave of smart travel, whether it can capitalize on the capital market remains uncertain.

A Business Deal Among the Elite

More than a decade ago, the wind of mobile internet transforming the real economy blew into the travel market. Ride-hailing platforms such as Yidao, Didi, and Kuaidi were established one after another. After the "thousand-team battle" in the ride-hailing market, Didi merged with Kuaidi and acquired Uber China, officially becoming the leader in the Chinese ride-hailing market.

Subsequently, major automotive OEMs also entered the ride-hailing market, giving rise to platforms such as UCAR, Caocao Mobility, Shouqi Limousine & Chauffeur, Enjoy Travel, OnTime, and T3 Go Out, solidifying the second-tier echelon of China's ride-hailing market. Their logic was straightforward: ride-hailing could serve as a primary sales channel for new energy vehicles under OEMs; moreover, the long-term operational business value significantly outweighed one-time sales—each ride-hailing service could bring the automotive brand closer to users.

Among these, T3 Go Out was established the latest but boasted the most prestigious shareholder background.

In 2018, facing the "Four Modernizations" trend of electrification, intelligence, connectivity, and sharing in the automotive industry, as well as the dominance of platforms like Didi in the travel market, three major automotive SOEs—FAW Group, Dongfeng Motor, and Changan Automobile in Chongqing—realized that a single enterprise would struggle to cope with industry changes. They needed to jointly build a smart travel platform belonging to the "national team" to achieve a strategic transformation from manufacturing cars to providing travel services.

Cui Dayong, who had worked at FAW for over two decades, led a core team of about nine people in closed-door preparations in Changchun, formulating a differentiated strategy of "Internet of Vehicles + B2C self-operation." The core logic was to use customized vehicle telematics (central control screens) to receive orders, combined with facial recognition technology, to fundamentally address safety hazards of "mismatch between person and vehicle"; simultaneously, starting with a heavy-asset model of self-owned vehicles and employed drivers to ensure service standardization.

In April 2019, the three automotive SOEs, along with renowned internet companies such as Tencent, Alibaba, and Suning, formally signed a joint venture agreement in Nanjing to establish T3 Go Out, with a planned total investment of RMB 9.76 billion.

This shareholder structure of "automotive SOEs" plus "internet giants" established significant resource advantages and industry barriers in the fiercely competitive travel market at the time. Among them, the three automotive SOEs provided strong vehicle and hardware support for T3 Go Out, while Tencent and Alibaba could offer crucial and stable technological, traffic support, and operational empowerment through their Tencent Travel and Gaode Maps, respectively. It is no exaggeration to say that T3 Go Out was born with a "golden spoon" in its mouth.

In July 2019, T3 Go Out officially launched in Nanjing with an initial fleet of customized new energy vehicles. In its early stages, Cui Dayong insisted on a high-profile approach, utilizing vehicle telematics technology to achieve full-trip monitoring and emergency intervention, emphasizing safety as a key selling point.

With the collective support of its major shareholders, T3 Go Out emerged as a latecomer to become the third-largest ride-hailing giant in the industry. By the end of 2025, T3 Go Out operated in 194 cities across China, with over 234.5 million registered users and 797.2 million orders.

Reliance on Aggregation Platforms Exposes Structural Risks

Between 2020 and 2023, the ride-hailing market experienced its first wave of IPOs, with Dida Chuxing, OnTime, and Caocao Mobility going public. Given its strong shareholder backing and prominent market position, why did T3 Go Out only initiate its IPO this year?

Industry insiders believe that T3 Go Out's consortium-style origin and overly prestigious shareholder list lack a true decision-maker. The board's excessive checks and balances and lack of a final arbiter, combined with insufficient cohesion with Cui Dayong's management team, often led T3 Go Out to choose the safest and most conservative path when facing market trend changes. This characteristic is also reflected in T3 Go Out's business style.

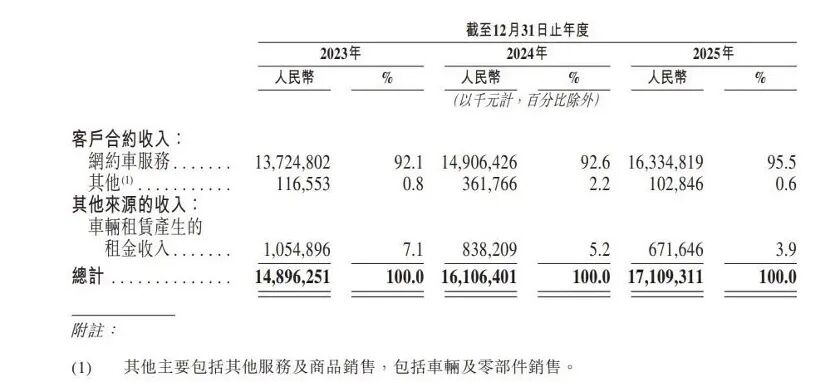

According to the prospectus, from 2023 to 2025, the company's total revenue grew from RMB 14.896 billion to RMB 17.109 billion, with a compound annual growth rate of 8.8%, but the growth rate slowed down—8.1% year-on-year in 2024 and 6.2% in 2025. From its revenue structure, T3 Go Out currently heavily relies on ride-hailing services, with concentration continuing to increase. From 2023 to 2025, the proportion of revenue from this business to total revenue rose from 92.1% to 92.6% and reached 95.5% in 2025.

Image source: Prospectus

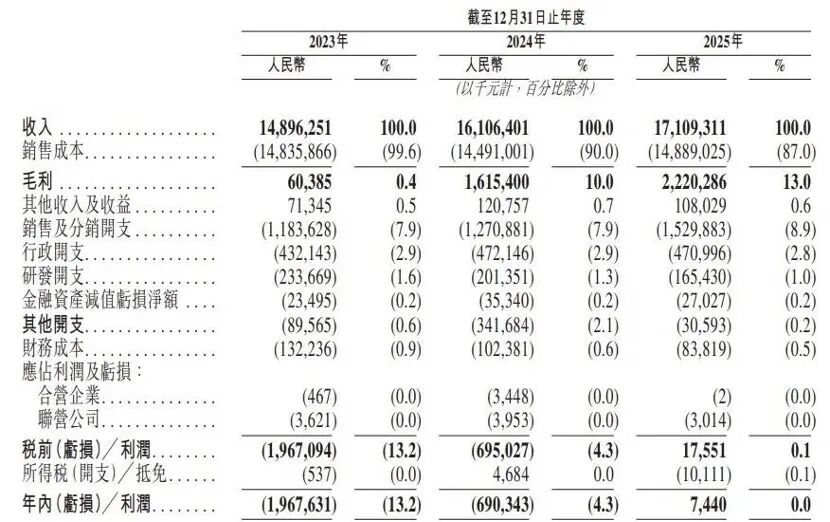

Despite its business scale, the company's profitability is astonishing: net profit was only RMB 7.44 million in 2025.

A net profit of RMB 7.44 million corresponds to RMB 17.109 billion in revenue, with a net profit margin of only 0.04%—less than 5 cents of profit per RMB 100 of revenue. Based on an annual order volume of 797 million, the profit per order is only about RMB 0.009. This set of data reveals a reality: T3 Go Out's profitability does not stem from breakthrough growth in its core business but rather from cost compression and expense control.

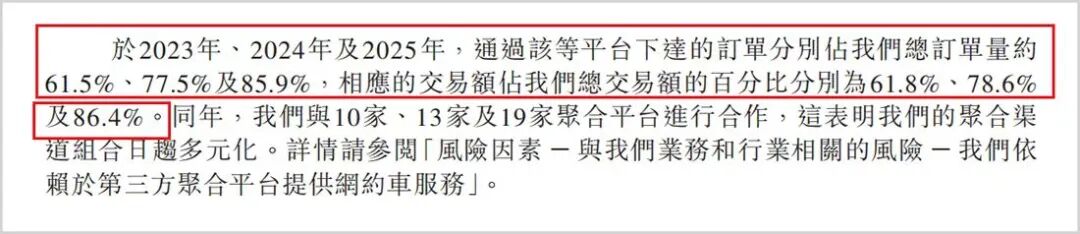

Deep reliance on third-party aggregation platforms is a structural risk that T3 Go Out cannot ignore. The prospectus shows that from 2023 to 2025, the proportion of orders from aggregation platforms (such as Gaode and Tencent Travel) surged from 61.5% to 85.9%, and the proportion of transaction volume rose from 61.8% to 86.4%. This means that out of every RMB 100 of transaction volume, more than RMB 86 was completed through third-party portals. The resulting channel service fees amounted to RMB 1.388 billion, accounting for 90.7% of sales and distribution expenses, equivalent to RMB 0.81 being taken away by third-party platforms for every RMB 100 of revenue.

Operating Performance Excerpted from Prospectus

Critically, aggregation platforms hold the power of traffic allocation while collaborating with multiple ride-hailing platforms. T3 Go Out's "lifeline is in others' hands," and its bargaining power is inevitably limited. The prospectus states that if aggregation platforms raise commissions or terminate cooperation, it will have a significant adverse impact on order volume and profit margins.

Moreover, compliance concerns at the operational end are equally significant. The prospectus discloses that due to violations related to transportation permits and ride-hailing driver certificates, T3 Go Out was fined RMB 2.5 million, RMB 10.6 million, and RMB 21.4 million in 2023, 2024, and 2025, respectively. The total fines of RMB 21.4 million in 2025 are nearly three times the net profit for the same period.

More worryingly, as of December 31, 2025, T3 Go Out was still in a state of insolvency with net debt of RMB 448 million and a net current liability of RMB 976 million. The company admitted in the prospectus that it primarily relies on bank loans and shareholder contributions to fund its operations. With such a balance sheet, there are differing views in the market as it rushes toward the capital market.

If the IPO is successful, it will enhance T3 Go Out's market competitiveness while alleviating its debt pressure.

What's the Trump Card for Riding the Smart Travel Wave?

The ride-hailing market is vast and continuously growing, but competition is fierce. Led by Didi and Gaode, T3 Go Out is followed by a host of competitors vying through differentiated strategies.

Caocao Mobility focuses on customized ride-hailing to enhance service capabilities, Enjoy Travel emphasizes the business travel market, while OnTime, Shouqi Limousine & Chauffeur, and Enjoy Travel all highlight their penetration in core markets. Especially with Gaode's introduction of the ride-hailing aggregation model, it has completely transformed the competitive landscape. Didi and Gaode have formed a dimensionality reduction strike against second-, third-, and fourth-tier ride-hailing operators.

Choosing to go public at this moment, T3 Go Out is likely trying to catch the wave of smart travel. When describing its competitiveness, the company states that T3 Go Out possesses the industry's first and only vertically integrated large model, "Lingxing Qianmo," which has passed dual accreditation. Simultaneously, it is the first platform to integrate manned and Robotaxi fleets for mixed capacity scheduling.

Facing the profit ceiling of traditional ride-hailing services, T3 Go Out has bet its IPO proceeds and future narrative on Robotaxi, attempting to brand itself with the "AI + Travel" technology label.

Unlike Didi and Baidu Apollo Go's choice of a "self-operated" heavy-asset model, T3 Go Out has opted for an "operating platform + technology partner" model: T3 does not independently develop core autonomous driving technology but leverages its travel operation network as a foundation, introduces external top-tier AI technology, and then uniformly dispatches manned and unmanned driving capacity through its unique mixed scheduling platform to achieve efficient commercialization.

Although this model can quickly integrate resources and avoid heavy-asset investments, its institutional barriers and coordination costs are exceptionally high. The three parties—automakers, technology companies, and operating platforms—have different objectives: automakers focus on vehicle sales, technology companies pursue algorithm validation, and platforms prioritize operational efficiency. Reaching consensus on core issues such as technology route selection, data ownership, and profit distribution is far more challenging than internal corporate decision-making.

At this critical stage of technological breakthroughs, major smart travel giants are increasing their investments. From 2023 to 2025, T3 Go Out's sales and distribution expenses continued to rise, but R&D investment decreased year by year to RMB 234 million, RMB 201 million, and RMB 165 million, accounting for 1.6%, 1.3%, and 1.0% of revenue, respectively. It is unclear why T3 Go Out is cutting its R&D investment.

Conclusion

The ride-hailing industry has reached its current stage, with the market landscape taking shape: aggregation platforms, as traffic gateways, are profitably stable, while ride-hailing companies and drivers providing services complain about diminishing earnings.

Against this backdrop, the Hong Kong stock market has become cautious toward travel platforms in recent years. Dida Chuxing (HK2559) fell 22.5% on its debut in 2024, and as of June 4, 2026, its stock price had dropped to HKD 1.14 per share. OnTime (HK9680) has remained sluggish since its listing. Against the backdrop of fragile profitability and frequent compliance issues, investors' valuation filters for ride-hailing platforms have shattered.

Despite the challenges in the ride-hailing sector, T3 Go Out has played its IPO card of autonomous driving and smart travel. With the continuous reduction in the cost of core hardware such as LiDAR and chips, unmanned vehicles in some cities have achieved Bicycle profitability (per-vehicle profitability), and in the long run, the per-kilometer operating cost is significantly lower than that of manned ride-hailing services and taxis.

For ride-hailing platforms, this is an highly attractive commercial sector, and large-scale deployment will become a future trend. If ride-hailing drivers can be attracted to invest in and purchase unmanned vehicles while enjoying profit sharing, it could represent a socially cost-controlled "holistic transformation."

Can it catch the smart travel wave? THE END

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek