Countdown to SpaceX's IPO: Musk's Ultimate Vision Unveiled

06/05 2026

06/05 2026

474

474

Is the $2 trillion valuation a leap of faith or a gateway to a new era of space exploration?

The world's financial markets are riveted on a 'spacecraft' poised to enter Earth's IPO orbit.

This isn't a scene from a sci-fi movie but the most significant capital event of 2026. Elon Musk's SpaceX, the pioneering space exploration technology company, has discreetly filed its IPO documents, with plans to list on NASDAQ in June.

The figures are as bold as Musk himself: an anticipated valuation of $1.75 to $2 trillion and a funding target of $75 billion. If successful, it would surpass Saudi Aramco to become the largest IPO in history. This 'spacecraft' not only carries Musk's dreams of space but also a collective wager by global capital on the 'space economy.'

Image source: Internet

SpaceX has evolved from a fledgling rocket company with a few desks and a wild dream in 2002. Earlier this year, Musk orchestrated a brilliant asset reshuffle: SpaceX officially merged with xAI. The prospectus now showcases an unprecedented business structure—three distinct segments, each telling a unique story:

One handles rocket launches, another sells satellite Wi-Fi, and the third builds large models and social media platforms. Musk has interwoven these elements with the grand narrative of 'humans becoming a multi-planetary species + AI infrastructure,' all packaged into a single prospectus.

Image source: Internet

Is this a 'vertically integrated space empire' or a strategic bundling of money-losing ventures with profitable ones for a joint listing? The answer depends on your perspective.

Denmark's pension fund Akademiker Pension has already announced its intention to blacklist SpaceX, with Chief Investment Officer Anders Schelde stating bluntly: "The company's reasonable valuation should not exceed $1 trillion, yet the market starts at $1.8 trillion." Michael O'Rourke, Chief Strategist at Jonestrading, was even more direct: "This is what you see at the market top and in a bubble."

From Near Bankruptcy to Space Monopolist

All discussions about 'why it's worth $1.75 trillion' must trace back to the starting point—Elon Musk, who had just $3 million left in his pocket on Christmas Eve 2008.

SpaceX's early days were marked by three 'near-death experiences' that forged its survival instincts.

The first crisis occurred on March 24, 2006, when the Falcon 1 prototype 'Demonstrator' exploded on the launch pad before takeoff. On March 21, 2007, it failed again, disintegrating due to uncontrolled spin. These back-to-back failures pushed the company's cash flow to the brink. Investors gave Musk an ultimatum: succeed on September 28, 2008, or face liquidation.

That afternoon, after the rocket's third stage separated, the control center fell silent. Until the 'orbit confirmation' signal arrived, Musk dared to look up and said, "Thank God." SpaceX survived, but only temporarily.

Image source: Internet

The second crisis struck on June 28, 2015. SpaceX's 'lifeline'—the Falcon 9 rocket carrying out its seventh International Space Station resupply mission—disintegrated two and a half minutes after launch in full view of the world. This was NASA's first time entrusting critical cargo to a commercial company, and the failure nearly severed all future government contracts for SpaceX, forcing Musk to cover damages out of pocket.

Image source: Internet

The third crisis occurred on September 1, 2016, when another Falcon 9, loaded with a Facebook communications satellite, exploded during a static fire test. The satellite was reduced to dust, the launch pad severely damaged, and operations halted for six months. At the time, SpaceX had over $10 billion in backlogged orders, with each delay incurring exorbitant penalty fees.

Image source: Internet

Three explosions pushed SpaceX to the edge three times. But each time, Musk chose to double down rather than walk away. This obsessive commitment laid the foundation for everything that followed. Musk adheres to first principles, returning to the essence of the problem: if it's theoretically possible, it must be made real in practice.

Traditional rocket launches cost hundreds of millions of dollars. SpaceX's reusable rockets can reduce single-launch costs to the tens of millions—not a marginal improvement but a 90% reduction. While Blue Origin was celebrating its first successful recovery, SpaceX was already mass-producing reusable rockets. By 2025, SpaceX completed 167 orbital launches, capturing 85% of the U.S. market. Its monopoly wasn't enforced by administrative orders but won through cost advantages.

The audacity of Starlink lies in its initial perception as another 'PPT dream' by Musk. Proposed in 2015, it aimed to deploy 12,000 satellites in low Earth orbit. At the time, the global total of in-orbit satellites was just over 2,000.

But Musk saw a different opportunity: rocket launches are low-frequency, high-ticket services. To excite Wall Street, he needed a high-frequency, cash-flow-generating 'money printer.' Starlink was the answer.

In 2020, Starlink began offering test services. By 2025, it contributed $11.387 billion in revenue with a 63% profit margin. Today, over 9,600 satellites orbit the Earth, covering 164 countries with over 10 million users. SpaceX is no longer just a company that sends things into space but a global telecom operator directly selling 'signals' to the ground.

Image source: Internet

The final chapter of the story is 'AI + Space.'

In February 2026, SpaceX acquired xAI in an all-stock deal. Many found this move puzzling: Why would a rocket company buy an AI firm?

Musk's logic: Starlink has already woven a 'space internet' covering the globe. The ultimate value of this network is to become the world's largest distributed computing platform. Imagine data centers not built on crowded, power-hungry ground but in low Earth orbit—solar energy nearly infinite, radiative cooling venting into the depths of space.

Image source: Internet

SpaceX's vision is to transform low Earth orbit into humanity's first 'space data center.' Rockets handle transportation and construction, while satellites manage connectivity and computing power distribution. From 'space transportation' to 'space computing,' the valuation imagination has fully opened.

Don't Ignore the 'Elephants in the Room'

SpaceX has indeed achieved 'what no one else has': it's the only aerospace company to turn rocket recovery into an assembly line, Starship iteration into software updates, and satellite internet into a profitable business. These advantages are real, structural, and difficult to replicate. But 'what no one else has' doesn't automatically equate to 'worth $2 trillion.' Against a backdrop of 5% risk-free rates, engineering advantages must rapidly convert into cash flow; otherwise, 'what no one else has' is just another way of saying 'expensive for a reason.'

The strongest pillar supporting SpaceX's valuation is undoubtedly Starlink.

But the numbers don't lie: $11.387 billion in revenue in 2025, up nearly 50% year-over-year; operating profit of $4.423 billion, up 120% year-over-year; adjusted EBITDA margin of 63%. Among global tech companies, only a few top SaaS firms can match this profitability. With 10.3 million subscribers across 164 countries and 9,600 in-orbit satellites accounting for over half of global active satellites—all self-designed, manufactured, launched, and operated—this is a cash-printing machine with a proven business closed loop.

Image source: Internet

However, the challenge lies in ARPU. Starlink's average revenue per user (ARPU) is visibly declining:

2023: ~$99/month

2025: ~$81/month

2026 Q1: ~$66/month

A 33% drop in three years. SpaceX attributes this to global expansion, penetration into Asian, African, and Latin American markets, and promotion of low-cost plans—an inevitable cost.

This explanation holds merit but implies a critical assumption: user growth must consistently outpace ARPU decline. Currently, Starlink's user base grows 105% year-over-year, outpacing the decline. But where will ARPU bottom out? The prospectus doesn't say. If the steady-state ARPU stabilizes at $40–50, the revenue model needs recalculating.

At a $1.8 trillion valuation, Starlink's implied price-to-sales (PS) ratio exceeds 100x. Even based on EBITDA, it's over 30x. This isn't pricing for an 'excellent company' but for 'inevitably ruling Earth'—implying most of humanity will use Starlink. Is that possible?

If Starlink anchors SpaceX's valuation floor, the AI segment represents the ceiling—and the greatest uncertainty.

In Q1 2026, the AI segment posted a quarterly operating loss of $2.469 billion, nearly double Starlink's same-period $1.188 billion profit. In 2025, the AI segment lost $6.355 billion for the year. Meanwhile, SpaceX's total net loss in 2025 was $4.937 billion—meaning SpaceX would have been profitable without the AI segment's money pit.

More striking is the capital expenditure. In Q1 2026, SpaceX's total capex was $10.107 billion, with 76% allocated to AI—primarily for Grok large model training and computing infrastructure. At this rate, annual AI capex will exceed $30 billion.

How much does the AI segment earn? $818 million in Q1 2026. The gap between revenue and capex spans nearly an order of magnitude. This is a classic 'arms race' model: you must burn cash to build computing power to avoid obsolescence, but when and how this computing power will monetize remains unclear.

Image source: Internet

SpaceX's IPO filings reveal a core bottleneck in scaling its Starorbit AI plan: GPU supply shortages. Its current single-procurement model offers weak risk resistance, and the jointly built TeraFab chip factory lacks legally binding agreements, leaving project success rates uncertain.

Now, new variables emerge: Musk has begun leasing computing power. On the morning of May 7, 2026 (Beijing Time), Musk announced this collaboration on X, confirming that the entire computing power of the Memphis Colossus1 data center would be provided to Anthropic.

On May 20, 2026 (local time), SpaceX formally submitted its S-1 prospectus to the U.S. Securities and Exchange Commission (SEC), detailing contract terms, amounts, and rights/obligations with Anthropic. This will partially alleviate the AI segment's cash burn, but expecting it to stop burning money—let alone consistently generate profits—remains unrealistic.

Image source: Internet

First, let's clarify one point: XAI has not been abandoned by Musk or seen its importance downgraded. The leasing of the massive computing power of Anthropic's Memphis Colossus1, exceeding 300 megawatts (MW) in total capacity, is equivalent to acquiring nearly the entire dispatched computing power available to OpenAI across its network in one fell swoop. It is no exaggeration to say that this has helped Anthropic achieve a significant leapfrog in computing power, perhaps demonstrating Musk's determination to compete head-on with OpenAI.

However, Musk still holds the most advanced computing power center. SpaceXAI (formerly xAI) has migrated all of its core training tasks for the Grok series to the newer, larger, and fully Blackwell-architected Colossus2 cluster. Colossus2 is hailed as the next-generation supercomputing cluster, with a total power output of 1 gigawatt, more than triple that of Colossus1, and a cost of approximately $17 billion, representing a quantum leap in scale from the first generation.

Some may worry that this computing power lease will help Anthropic widen the gap with Grok, but let's not forget that the ever-shrewd Musk would not engage in a losing proposition. Musk emphasized on the social platform X that SpaceX has not committed to a multi-year lease; in fact, it is a '180-day lease' that either party can cancel with 90 days' notice at any time.

Therefore, it is premature to conclude that Musk has lost his ambition to dominate the AI industry. AI remains one of Musk's core businesses that he cares about most. In the AI computing power war, the fear is not about

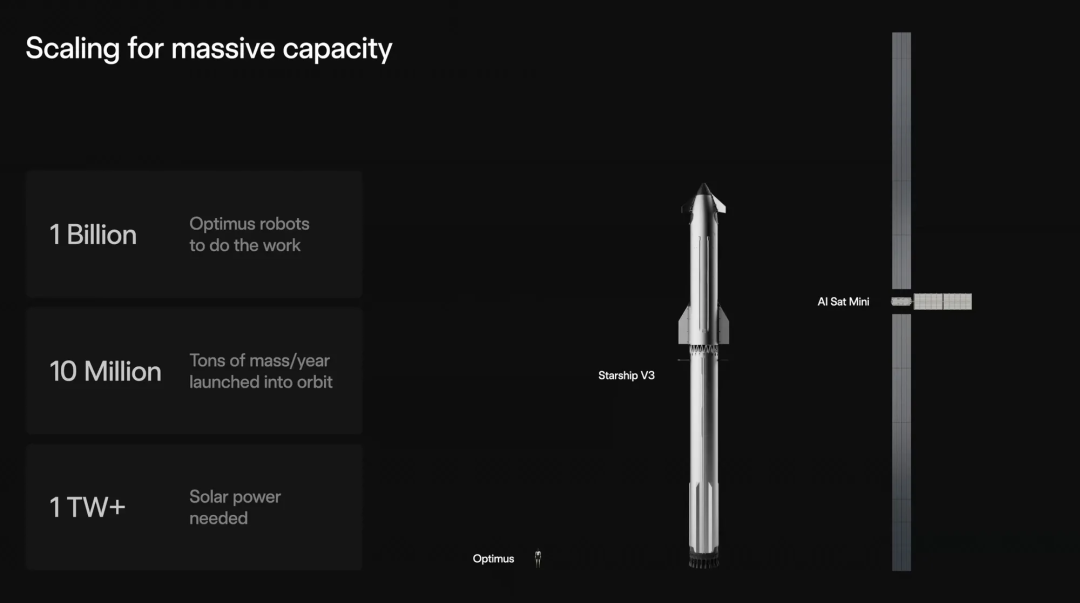

The Starship stands as the pivotal powerhouse for all of SpaceX's forthcoming ventures. The deployment of V3 satellites hinges on the Starship (boasting a single-satellite capacity of 1Tbps, 20 times greater than current offerings), Mars colonization necessitates the Starship for transportation, and the construction of the orbital AI computing power center relies on the Starship as well. The prospectus explicitly outlines that the Starship is set to officially commence commercial operations in the latter half of 2026, and its current grounding could potentially throw the entire timeline into disarray. Some investment banks project that this technical setback might result in a valuation markdown ranging from 5% to 15%. Musk himself weighed in on Blue Origin's explosion incident on X, remarking, "It's truly regrettable. Rockets are just that challenging." He is also cognizant that this sentiment applies to his own endeavors as well.

In Conclusion

SpaceX undoubtedly ranks among the most remarkable startups in human history. It has slashed launch costs by 85%, secured a dominant 80% share of global payload orbit insertion tasks, and transitioned satellite internet from a mere concept to a daily reality for millions of users. These accomplishments are indisputable.

However, a great company does not automatically translate into a great investment opportunity, particularly at a valuation hovering between $1.8 trillion and $2 trillion.

Starlink indeed stands as a cash cow, yet its average revenue per user (ARPU) is on a downward trajectory. Rocket launches do enjoy a global monopoly, but the Starship remains grounded. AI certainly holds promise for the future, but it is burning through $2.5 billion every quarter with an unclear path to profitability. Coupled with a 5% risk-free interest rate, the largest IPO bloodletting effect in history, and 85% super-voting rights, SpaceX's IPO pricing has already factored in all optimistic projections for the next 5-10 years.

The lingering question is, if one of these projections fails to materialize, how much of a safety margin will remain?

References:

'Losses of $4.9 Billion, Musk Controls 85% of Voting Rights' Source: Wall Street See

'SpaceX Launches IPO, Musk Harbors Grand Ambitions' Source: Cyzone

'Can SpaceX Weather the U.S. Debt Storm?' Source: Economic Observer Report

Some information was gathered with the assistance of AI.

Click 'Recommend' and may fortune smile upon you!

- The End -

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek