History’s Largest IPO Is Set to Debut—But Chinese Investors Are Shut Out

06/12 2026

06/12 2026

486

486

$75 Billion! An IPO That Redefines the Record Books.

On June 12 (local time), Elon Musk’s space exploration behemoth, SpaceX, will officially list on Nasdaq under the ticker ‘SPCX’.

According to its prospectus filed with the U.S. Securities and Exchange Commission, SpaceX plans to issue approximately 555.6 million shares at $135 each, aiming to raise $75 billion in base proceeds. Underwriters also hold an over-allotment option for an additional 83.33 million shares, potentially adding another $11.2 billion in funding.

What does this number signify? It shatters the previous global financing record of $29.4 billion set by Saudi Aramco’s IPO in 2019. Even Alibaba’s $25 billion U.S. IPO in 2014 pales in comparison.

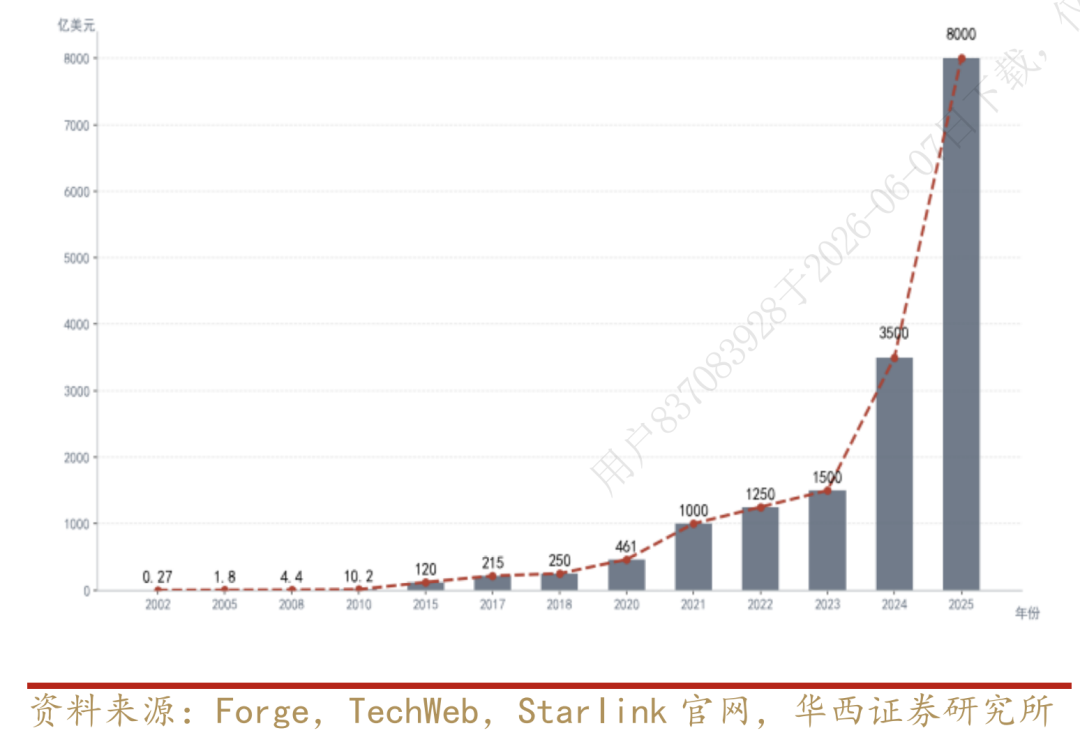

At an issue price of $135 per share, SpaceX’s valuation will soar to roughly $1.77 trillion, surpassing Tesla’s current market cap of about $1.6 trillion. Its valuation has doubled in under a year.

Figure: SpaceX’s Valuation Growth Trajectory.

Image Source: Huaxi Securities Research Institute

Just before listing, SpaceX secured two major deals: a computing power leasing agreement with Anthropic, involving monthly payments of $1.25 billion, and a $30 billion cloud services pact with Google, with monthly payments of $920 million from October 2026 to June 2029. This includes at least 110,000 NVIDIA GPUs, CPUs, and memory resources. Combined, these contracts lock in recurring monthly revenues exceeding $2.1 billion.

The Enigmatic ‘ITAR’

However, this financial spectacle isn’t open to all investors.

Shortly after SpaceX launched its IPO roadshow, Bloomberg reported that underwriters had been instructed to reject subscription orders from investors in mainland China and Hong Kong. The announcement sparked intense debate.

The ban is sweeping, even excluding private banking clients.

SpaceX cited relevant provisions of the U.S. *International Traffic in Arms Regulations* (ITAR). ITAR is a U.S. law governing the export of defense-related technologies, and SpaceX used it to label mainland China and Hong Kong as so-called ‘restricted jurisdictions.’

An internal memo from Citigroup revealed that SpaceX also required underwriting banks not to market this offering to citizens in ITAR-restricted regions through wealth management or private banking channels.

This isn’t an isolated incident. In recent years, U.S. firms seeking government contracts or operating in sensitive sectors typically avoid shareholders that might trigger regulatory scrutiny.

From the perspective of Chinese investors, being excluded from this IPO is undoubtedly disappointing.

Yet, a $1.77 trillion behemoth relies heavily on institutional investor participation, with retail investors receiving only a limited allocation.

Up to 30% of the offering is expected to go to retail investors, though whether this target will be fully met remains uncertain.

Rather than dwell on exclusion, attention should shift to China’s rapidly emerging commercial space sector.

Why Is This the ‘Largest IPO in History’?

The $75 billion fundraising and $1.77 trillion valuation aren’t built on mere hype. Market willingness to assign such aggressive pricing reflects underlying business logic.

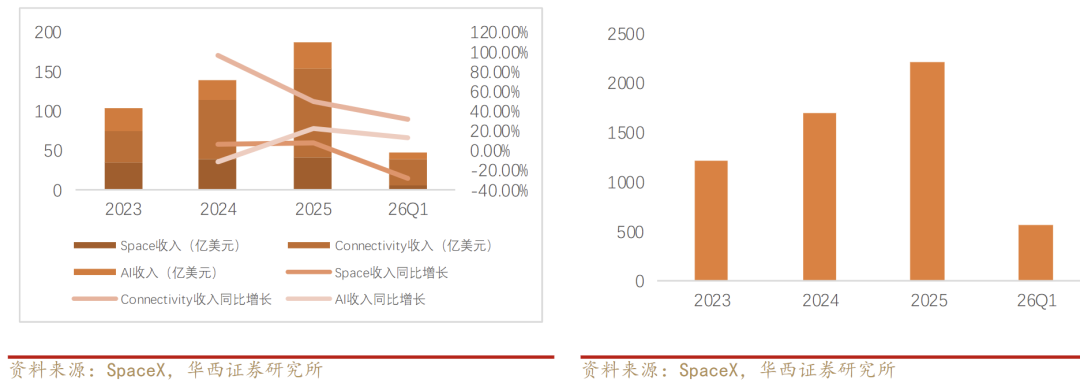

Below are financial highlights for SpaceX’s business segments, as disclosed in its prospectus:

Data Sources: SpaceX Prospectus, Sina Finance, Huaxi Securities Research Institute, etc.

Image Source: Huaxi Securities Research Institute

Starlink is SpaceX’s cash cow. In 2025, its connectivity segment, centered on Starlink, generated $11.387 billion in revenue, $4.423 billion in operating profit, and an operating profit margin of 38.8%.

As of Q1 2026, Starlink had amassed over 10.3 million subscribers across 164 countries and regions.

Why does Starlink turn a profit? It addresses gaps where terrestrial networks fall short: maritime workers, remote mountainous areas, airline passengers, and emergency responders. Essentially, it functions as a ‘space-based telecommunications operator,’ charging monthly subscription fees with high retention and sustainability.

The rocket business, however, remains in the red. The space segment generated $4.086 billion in revenue but suffered a $657 million operating loss in 2025. SpaceX has invested over $15 billion in its Starship heavy-lift rocket. Although the 12th test in 2024 achieved partial success, the super-heavy booster failed to return, underscoring the lengthy road ahead for technical validation.

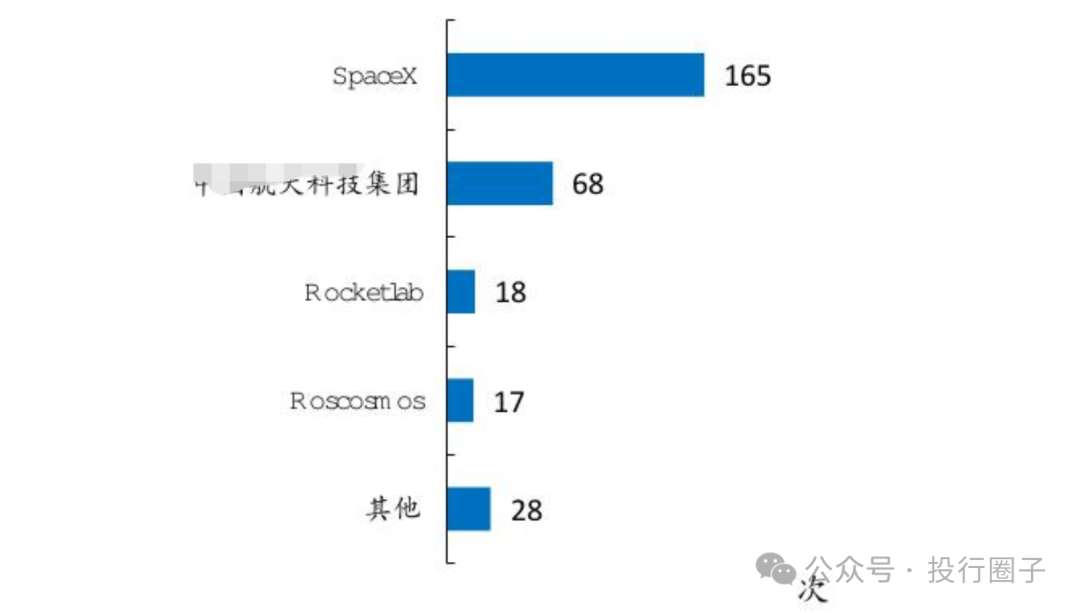

Yet, the launch business boasts formidable barriers to entry. In 2025, SpaceX completed over 160 orbital launches. By April 2026, it had conducted roughly 52 Falcon 9 launches. As of May 3, 2026, SpaceX had completed about 54 launches annually, surpassing the combined total of all other global space enterprises and national launch activities.

Image Source: Kaiyuan Securities Research Institute.

Falcon 9’s reusability slashes launch costs well below competitors. NASA, the U.S. military, and numerous commercial satellite clients rely heavily on this launch corridor, making it nearly irreplaceable in the short term.

Image Source: Huafu Securities Research Institute

The AI segment is the biggest financial drain. In 2025, it generated $3.2 billion in revenue but incurred a $6.355 billion operating loss. In Q1 2026, revenue reached about $800 million, with a $2.469 billion operating loss—more than double Starlink’s profits.

Why does its valuation reach $1.77 trillion despite losses?

The answer lies in ‘computing power leasing.’ The prospectus revealed that Anthropic has contracted xAI’s computing resources, paying $1.25 billion monthly in leasing fees starting June 2026, equating to roughly $15 billion in annual revenue.

Additionally, SpaceX outlined a grander vision in its prospectus: deploying a space-based AI computing network with millions of satellites, relocating data centers to space, and leveraging solar energy and space’s low temperatures to overcome terrestrial computing’s power bottlenecks and cooling challenges.

If realized, SpaceX will evolve from a ‘rocket company’ or ‘satellite company’ into a composite infrastructure platform spanning aerospace, communications, defense, and AI computing.

This is why capital markets are willing to pay a premium: they’re betting on SpaceX’s role in the global space economy over the next decade, not its current earnings.

To grasp the scale of SpaceX’s IPO, let’s revisit previous record-holders.

Data Sources: Public searches, compiled by ‘Investment Bank Little Sister’

These five giants raised nearly $123.1 billion combined. SpaceX alone seeks $75 billion—exceeding the total of Alibaba, SoftBank, and General Motors.

This isn’t just about numbers; it signals unprecedented global capital allocation toward a new frontier: space computing.

Behind the Capital Frenzy

In my view, SpaceX’s IPO transcends mere financial excitement.

The core of global tech competition is shifting from ‘ground’ to ‘space’ and ‘computing power.’ SpaceX’s valuation logic essentially prices in a monopoly on space infrastructure.

It dominates the global commercial rocket launch market, completing about 165 orbital launches in 2025. Falcon 9’s single-launch cost dropped to $27 million, roughly 70% lower than traditional rockets. Starlink has deployed over 9,600 satellites, far outpacing competitors in orbital presence.

Against the backdrop of intensifying Sino-U.S. space competition, this ‘first-come, first-served’ approach to orbital and spectral resources commands a high strategic premium from capital markets.

Space-based frequency and orbital resources are finite. Whoever deploys them at scale first controls the gateway to next-generation global communications and computing infrastructure. This explains why a company with a $4.9 billion net loss in 2025 dares to demand a $1.77 trillion valuation.

For Chinese investors, exclusion is regrettable but no cause for undue alarm. At most, 30% of SpaceX’s IPO will go to retail investors, but for a $1.77 trillion giant, individual allocations will be minuscule.

Moreover, Chinese investors can already participate in domestic ‘hard tech’ capital markets via channels like the Stock Connect, Beijing Stock Exchange, and STAR Market.

China’s commercial space sector is accelerating. On June 1, the Long March 12B Yao-1 achieved a successful maiden flight, deploying the Qianfan Polar-Orbiting 08 satellite group. On June 4 and 5, the Long March 6A and Long March 8 launched the Qianfan Polar-Orbiting 11 and 12 groups, respectively. These consecutive network deployments indicate accelerating satellite mass production and launch demands.

At the policy level, the 2026 *Government Work Report* explicitly calls for ‘accelerating satellite internet development,’ elevating commercial space from a ‘supplementary force’ to an ‘integral part’ of the national space system.

The essence of tech competition is a contest of ‘imagination.’ Michael Burry, the famed investor and inspiration for *The Big Short*, publicly stated that after scrutinizing SpaceX’s S-1 prospectus, he believes ‘nothing in the document justifies a $1 trillion or even $2 trillion valuation.’

The CEO of investment research firm Newconstructs went further, labeling this IPO wave as ‘one of history’s greatest potential scams.’ These criticisms aren’t entirely unfounded.

From a purely financial perspective, SpaceX reported a $4.9 billion net loss in 2025. Its $1.77 trillion valuation implies a price-to-sales ratio exceeding 90x, far higher than most mature tech firms.

But capital markets rarely focus solely on financial statements—they bet on trends.

Just as Amazon endured years of losses before becoming a darling of capital markets, SpaceX’s narrative hinges on whether Starlink can scale its user base, Starship can achieve true reusability, and space-based AI computing can transition from blueprint to reality.

This time, Musk may become the first individual in history with a net worth exceeding $1 trillion.

For us, rather than dwelling on exclusion, we should channel this regret into motivation.

After all, the true ‘final frontier’ belongs to no single nation or company.

When SpaceX rings the Nasdaq bell on June 12, Chinese investors may lack an invitation, but our own ‘space economy’ story is just beginning.

Statement: This article is solely for financial hotspot analysis. The data and information are sourced from publicly available queries, company announcements, and Tonghuashun IFinD. The viewpoints are for reference only and do not constitute any investment or consumption advice.

#FinancialHotspots #DeepThinking #BusinessFinance #InvestmentBankingCommunity #ListedCompanies #AI #FinancialTrending #PrimaryMarket #GoingPublic #SpaceX

What are your thoughts on this topic?

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek