From 'Daydream' to 'Inestimable Wealth': Is SpaceX Truly So 'Sci-Fi'?

06/15 2026

06/15 2026

660

660

'Iron Man' Musk has once again presented a grand offering to the capital markets with his Martian aspirations—SpaceX, a 'crazy idea' valued at $27 million two decades ago, has metamorphosed into a $2 trillion space commercial behemoth.

Indeed, in the early exploration of space economics earlier this year, Dolphin Research elucidated in "Musk Strikes Again with a Game-Changer: SpaceX Reshapes Space Economics" how SpaceX evolved from a cost-cutting concept into a viable business model.

Now, armed with clearer data from the prospectus, Dolphin Research re-examines SpaceX from valuation and business operations perspectives:

In this report, Dolphin Research delves into the following inquiries:

1) Valuation Transformation: How did SpaceX ascend to prominence? What were the primary drivers behind each 'valuation surge' at the billion-dollar level?

2) Business Matrix: How are the company's current core business landscape and capital flows distributed?

3) Launch Market Foundation: How long can the absolute monopoly barrier of an 80% market share be sustained? Why has revenue growth in the launch business been sluggish despite a surge in capacity? How will the full orbital entry of Starship shatter market ceilings?

Below is a detailed analysis:

I. From 'Disruptor' to 'Trillion-Dollar Infrastructure Builder'

The company's offerings—Starship, Starlink, etc.—seem plucked from 'Star Trek.' Stripped of their sci-fi allure, they essentially involve constructing vessels, venturing out to sea, casting nets, and reaping the bounty.

Of course, the distinction lies in their 'vessels' being launch vehicles, their 'nets' being space communication networks, and their 'bounty' being network communication fees—and potentially future space computing fees.

The cornerstone of this entire space economy is constructing a transport vessel capable of delivering these 'nets' into space. While launching rockets into space is not novel, achieving economies of scale hinges on vessel and transportation costs. This is where SpaceX made its breakthrough:

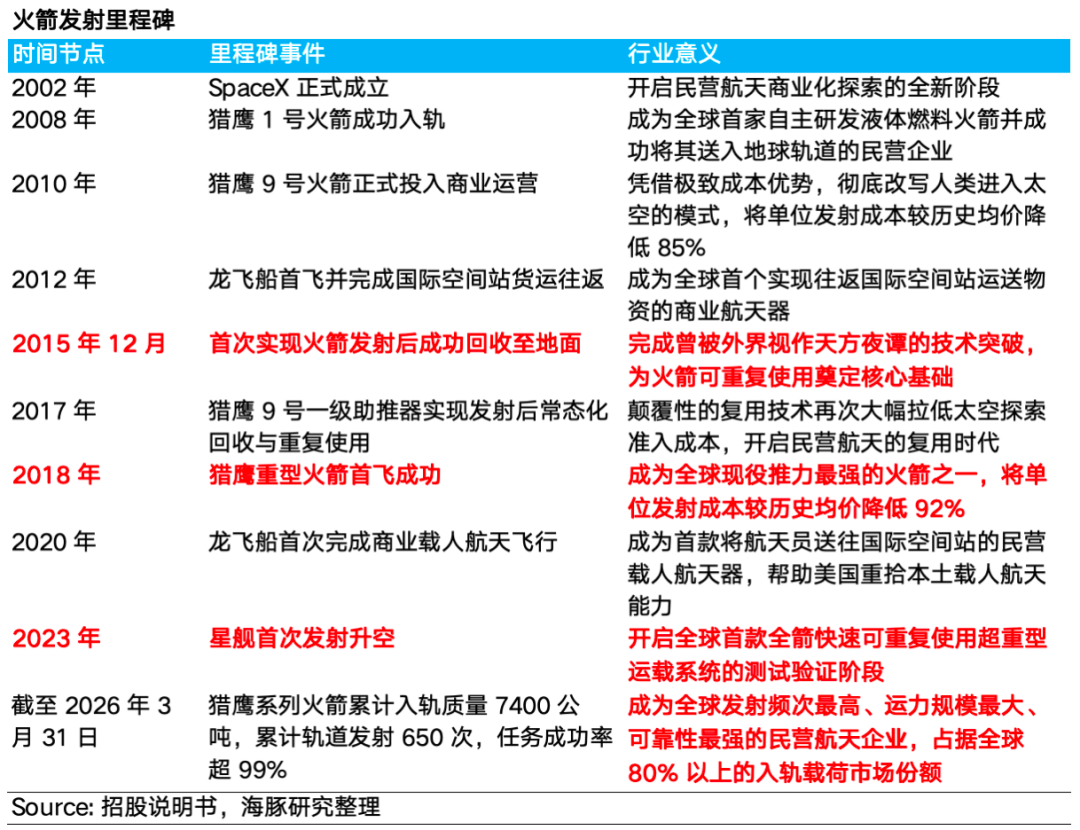

(1) Persevering Through 'Daydreams': Prior to SpaceX, the aerospace launch sector was niche with few players (Boeing and Lockheed Martin), and pricing was based on cost-plus models. Following the 2003 'Columbia' disaster, NASA outsourced low-Earth orbit (LEO) transportation, switching to 'fixed-price' and 'milestone payment' models, creating a survival niche for SpaceX, founded in 2002.

After three consecutive failures, SpaceX's fourth 'Falcon 1' launch succeeded in 2008, securing a $1.6 billion NASA contract and giving the company hope for survival. Its valuation soared from $27 million at inception to $200 million, with pricing shifting from backing a 'madman's dream' to something with 'potential.'

(2) Rocket Recovery: The Hardcore Innovation. The true supply chain core was reducing rocket costs—the cargo transport tool—using methods others couldn't replicate. Musk's solution? Rocket recovery technology.

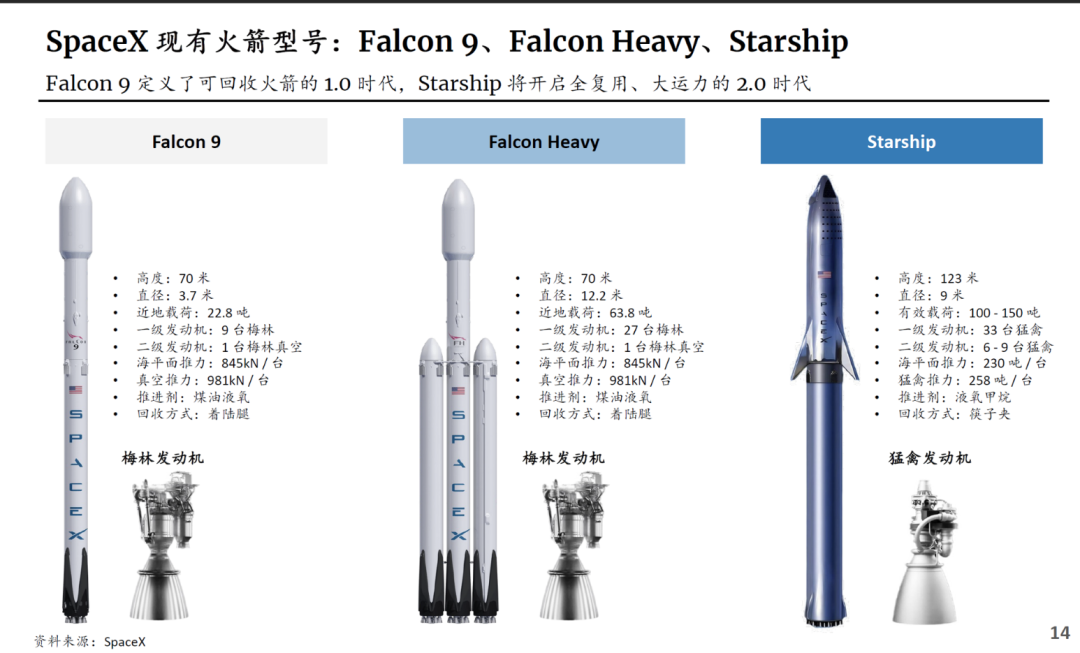

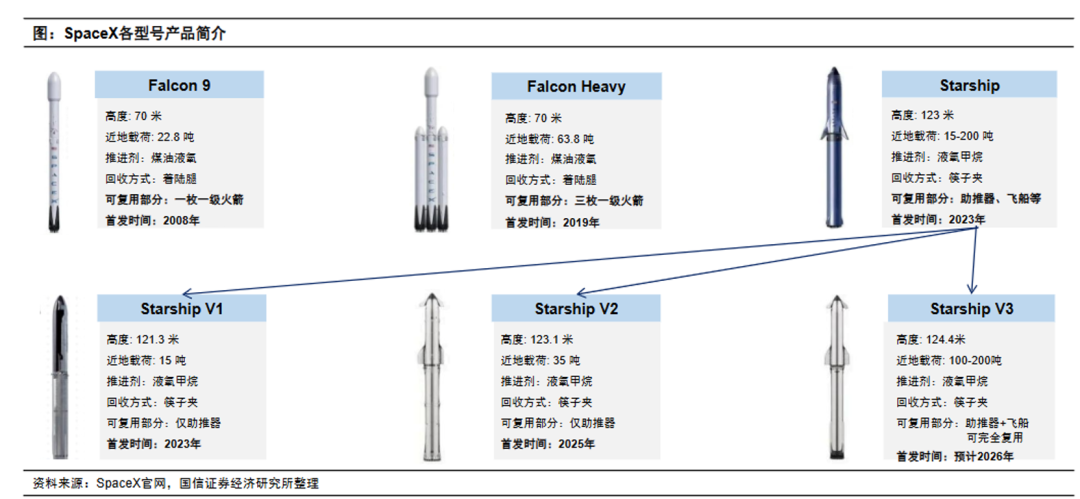

This became a reality in late 2015 with the recovery of the first-stage booster, slashing the Falcon 9's per-launch cost from ~$50 million to ~$15 million (with reuse exceeding 20 times). By March 2017, SpaceX became the first to conduct commercial launches using recovered first-stage boosters.

In 2018, building on the Falcon 9, the 'heavy freighter' Falcon Heavy (with a 63.8-ton payload) debuted, halving transport costs again. By then, legacy players were left far behind.

The company's valuation rose to $12 billion during its technological breakthrough phase (2010–2015) and surged to $30.5 billion after technological maturity and commercialization (2015–2019), with pricing beginning to reflect a premium for technological leadership.

(2) Casting Nets and Reaping Rewards: Communication Satellite Networks and Fees

While space transport cost reductions progressed, external demand remained limited, keeping valuations below $50 billion. The real valuation driver was leveraging this technology to build a downstream commercial empire—the Starlink broadband satellite communication network.

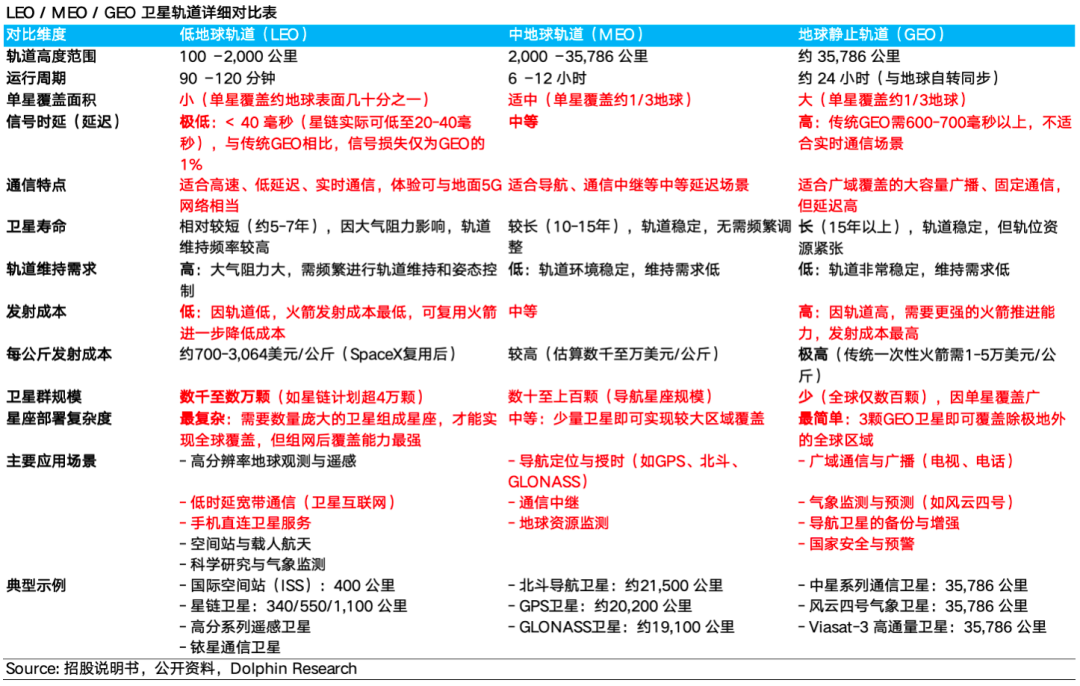

A basic explanation: Low-Earth orbit (LEO) satellites are categorized into different orbits based on their altitude above Earth. Starlink's satellites typically operate below 2,000 kilometers, classifying them as LEO satellites.

These satellites offer low communication latency due to their proximity to Earth. However, they orbit rapidly (~90–120 minutes per revolution), covering any single Earth location for only ~10 minutes. To achieve continuous coverage, a large constellation of satellites (Musk's Starlink) is needed, with seamless handoffs between satellites.

Thus, Musk expanded from building 'vessels' to casting his own 'nets,' dramatically increasing transport demand. The 'net-casting' phase spanned 2020–2023, with 'reaping rewards' becoming evident thereafter.

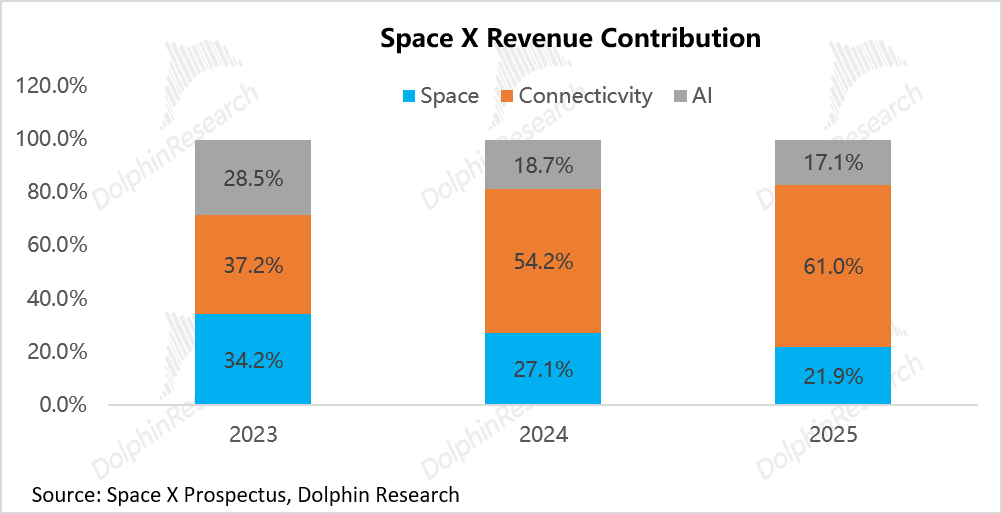

By 2023, Starlink's revenue surpassed that of the launch business, becoming SpaceX's primary revenue source. By 2025, Starlink accounted for 61% of revenue, with nearly 9 million subscribers.

A perfect commercial 'flywheel' had formed: High-frequency launches reduce satellite costs → satellite constellations enhance network value → C-end subscriptions/B-end commercial use generate stable cash flow → cash funds next-gen rocket (Starship) R&D.

With technological leadership and a closed commercial loop, capital valuations began repricing SpaceX based on 'high-barrier communication infrastructure' and 'SaaS-like subscription model' logics, catapulting its valuation from below $100 billion to $800 billion.

(4) The Next Big Play: Space Computing Hegemony?

With the satellite communication network thriving, the next planned 'big net' is the 'space computing network.' This network will be far costlier than the communication satellite network and require in-house AI model development. This new venture is a capital sinkhole, making an IPO seem essential.

To assemble this vision, Musk orchestrated a key move: Full acquisition of xAI (February 2026): Completed at a $1 trillion SpaceX valuation and $250 billion xAI valuation. xAI includes the 'Grok large model,' 'Colossus computing cluster,' and 'X platform.'

The core narrative is deploying hundred-gigawatt-scale orbital AI data centers via Starship V3's ultra-low launch costs (target: <$200/kg to orbit), leveraging space's boundless solar energy to slash computing costs (theoretically ~1/10 of terrestrial costs). Clearly, Musk believes the future AI battle hinges on energy control.

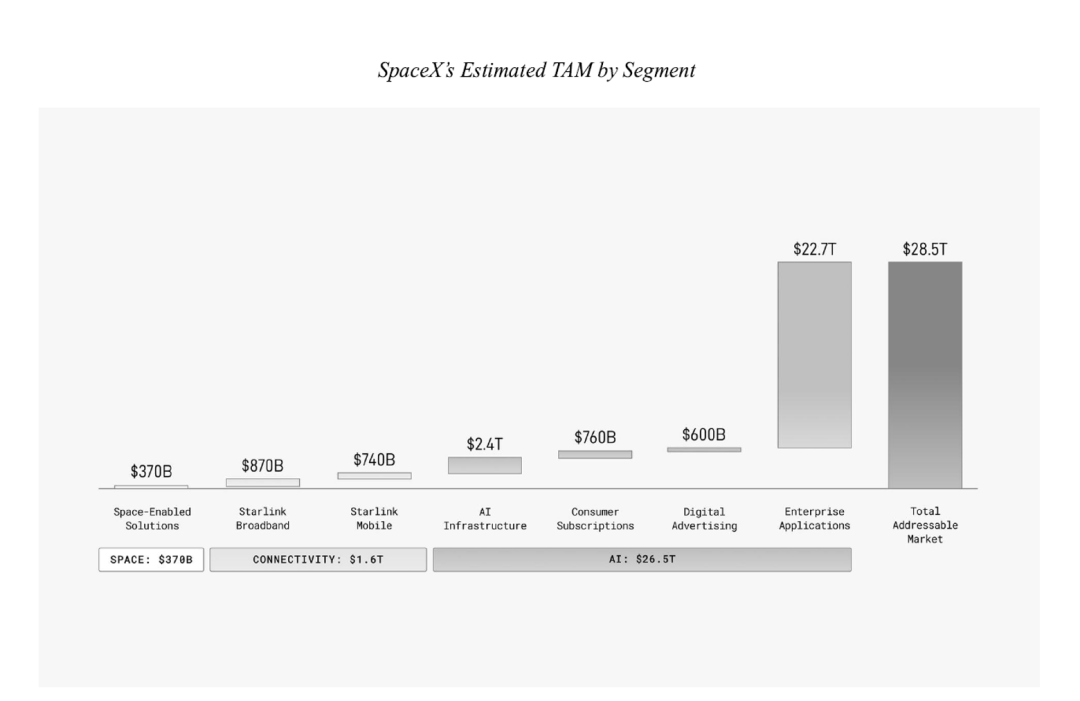

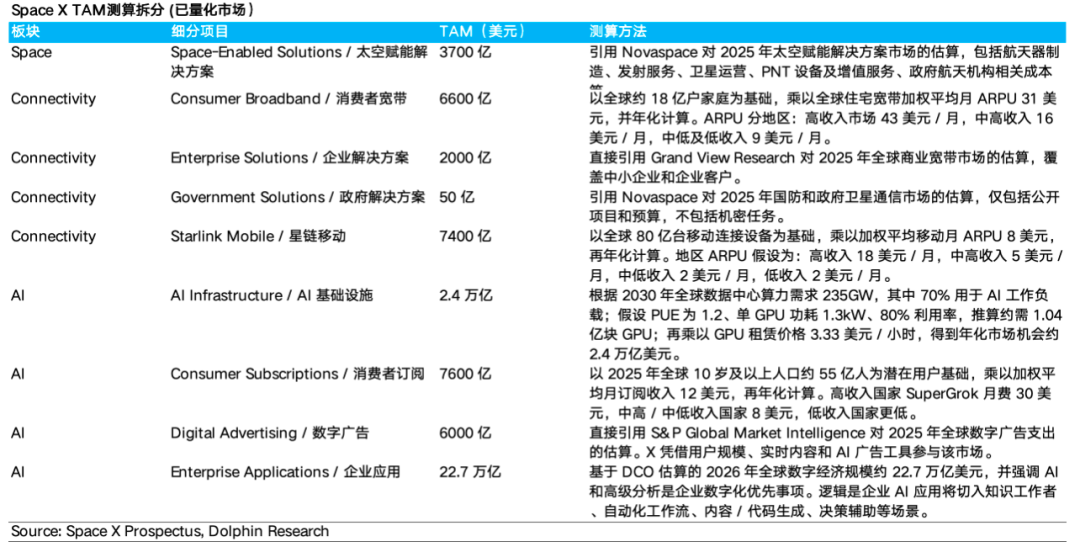

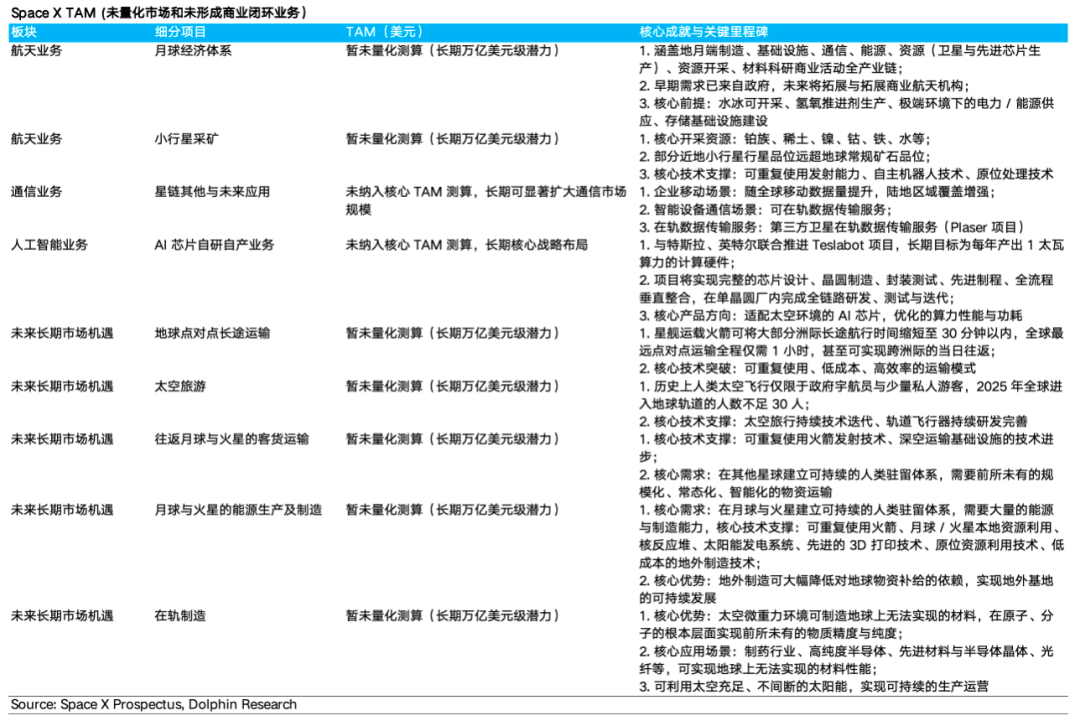

This move abruptly expands SpaceX's addressable market from '$0.37 trillion space solutions + $1.6 trillion global connectivity' to a '$26.5 trillion AI market,' totaling $28.5 trillion (excluding China and Russia). Enterprise applications will dominate ~80% of the future TAM.

While space-based AI data centers remain conceptual—facing major engineering challenges like heat dissipation, hardware iteration, power transmission, and space radiation—they provide SpaceX with a multi-trillion-dollar 'long-term growth option.'

II. Where Does the 'Inestimable Wealth' Originate?

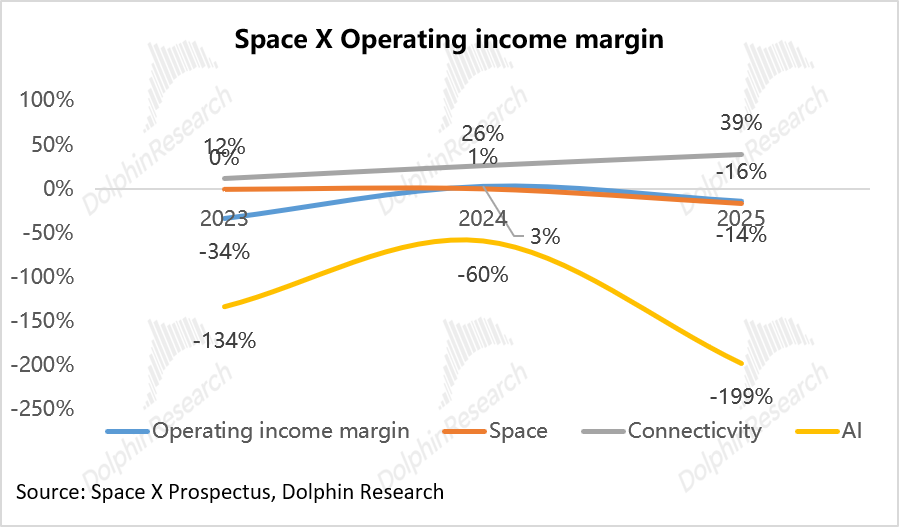

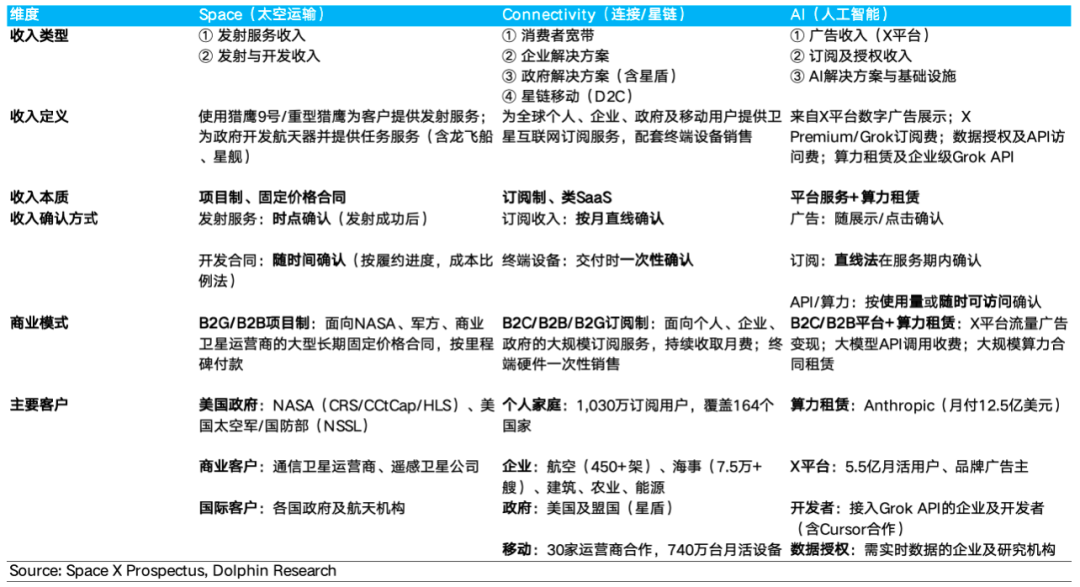

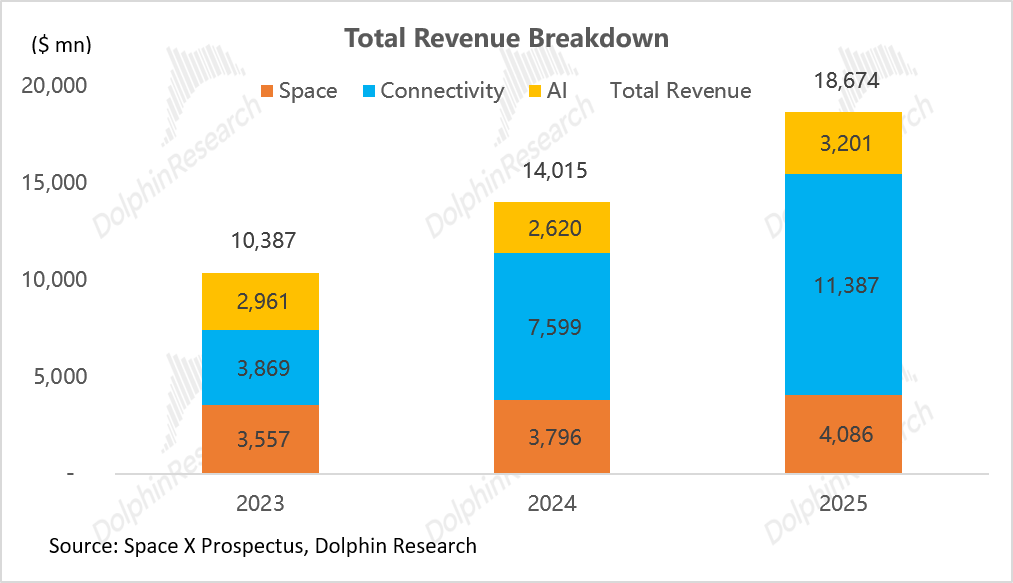

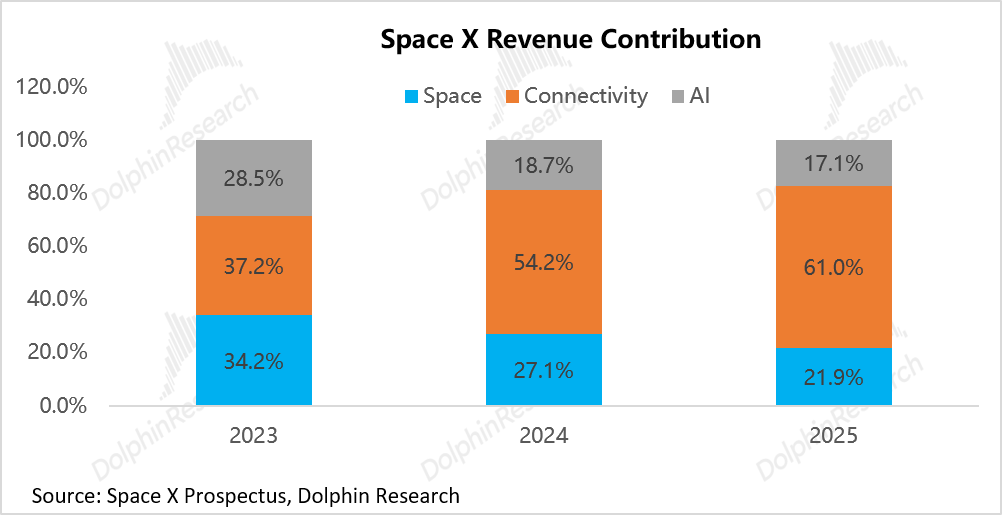

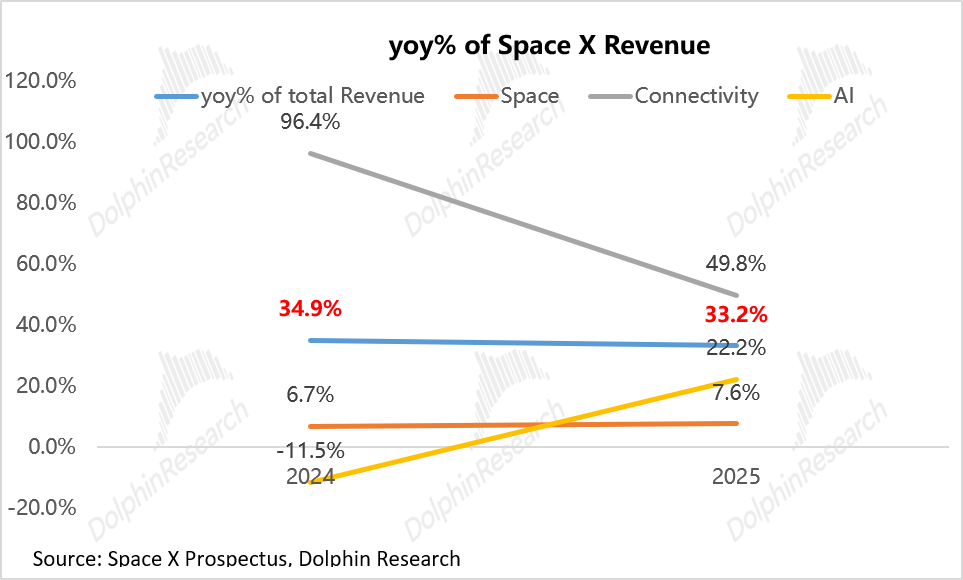

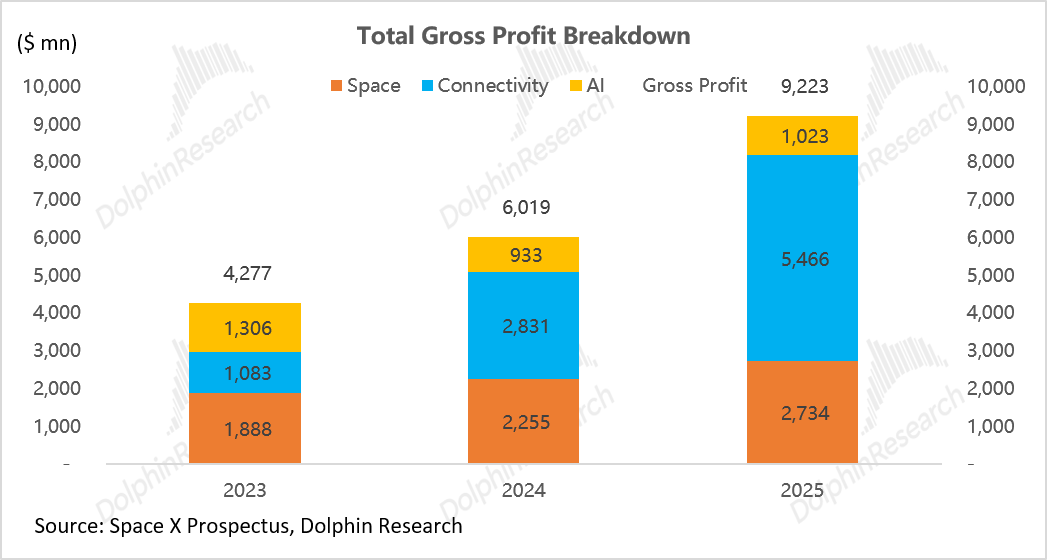

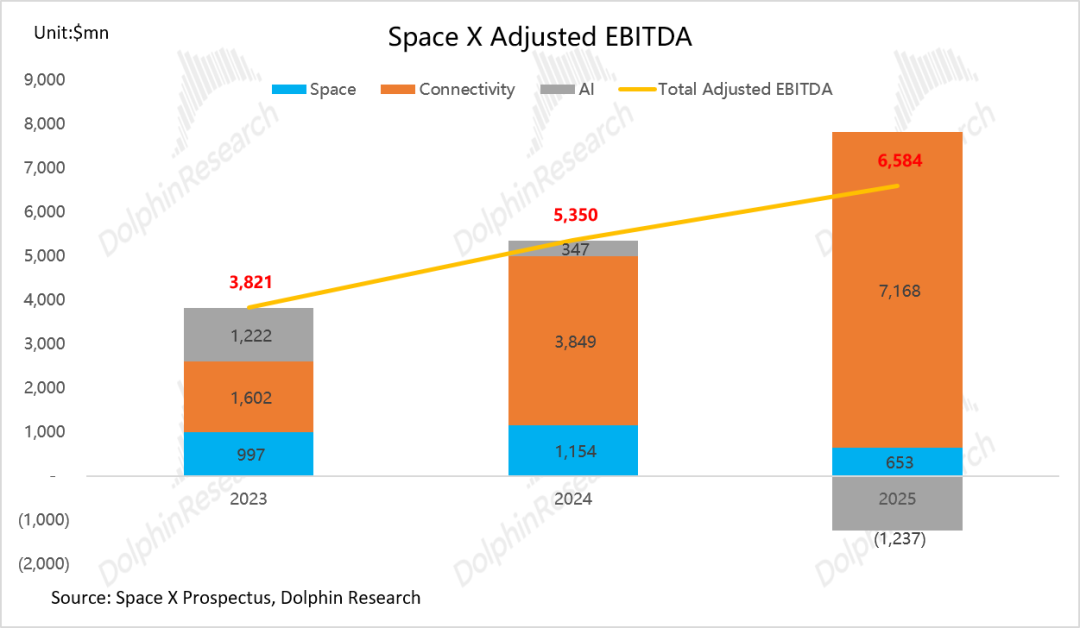

From 2023 to 2025, SpaceX formed a 'Space (transport/launch), Broadband Connectivity (Starlink), AI (Artificial Intelligence)' trifecta; total revenue soared from $10.4 billion to $18.7 billion, a 34% increase.

Revenue Breakdown: Transport Understates, Network Monetizes, AI 'Burns Cash'

In SpaceX's financials, rocket transport is the 'hidden monk'—the core barrier—but generates little revenue, mainly because it primarily transports in-house cargo, not reflected as income: Space launch revenue grew at a mere 7.2% CAGR over two years; slow growth stems purely from SpaceX’s strategic priority of internal guarantee (self-sufficiency).

The revenue pillar is the Starlink network, built using transport capacity: Its revenue contribution surged from 37% in 2023 to 61% in 2025, with a staggering 72% CAGR over two years. The AI segment, still in its infancy, generated a mere ~4% CAGR over two years.

② Profitability: Starlink as the Cash Cow

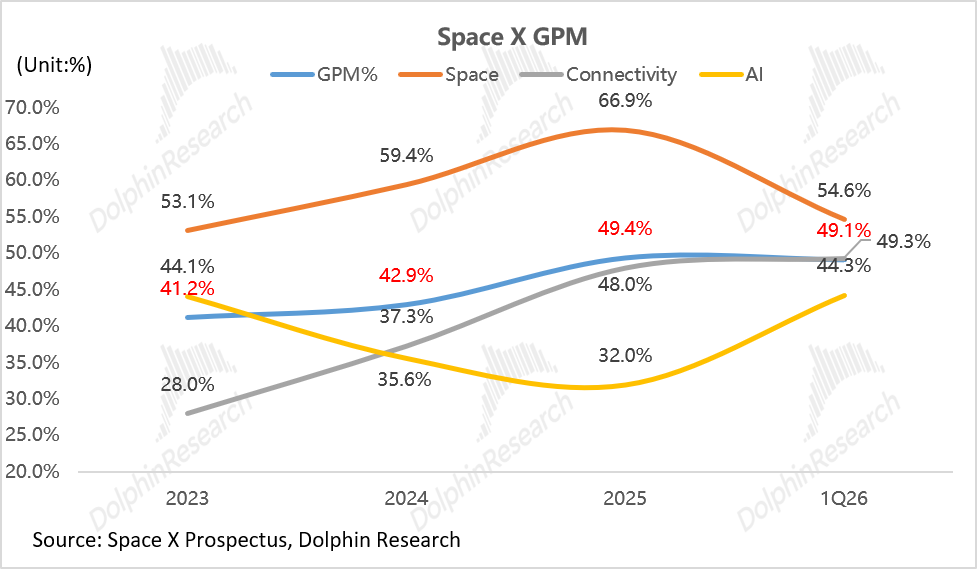

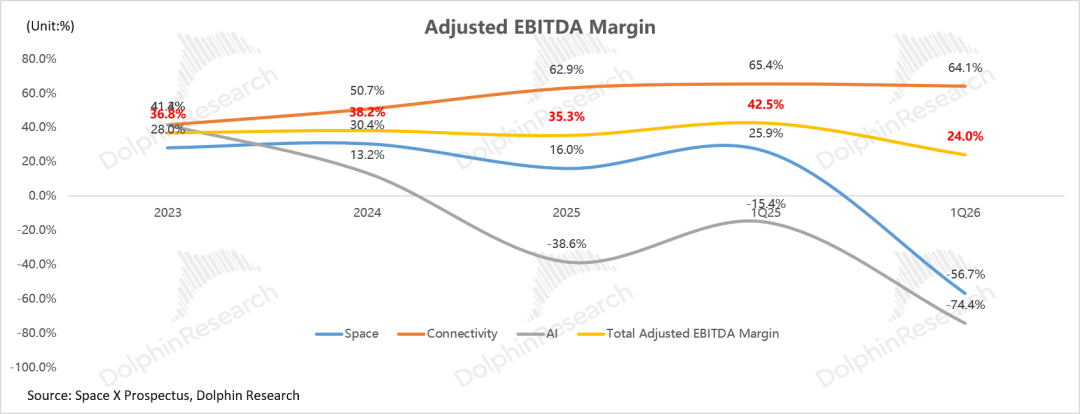

With economies of scale, SpaceX's overall gross margin steadily climbed from ~41% in 2023 to 49% in 2025, with gross profit doubling ($4.28 billion to $9.22 billion).

Once the network was established, Starlink's profits shone: Its gross margin leaped from 28% in 2023 to 48% in 2025, with a 125% CAGR in gross profit over two years.

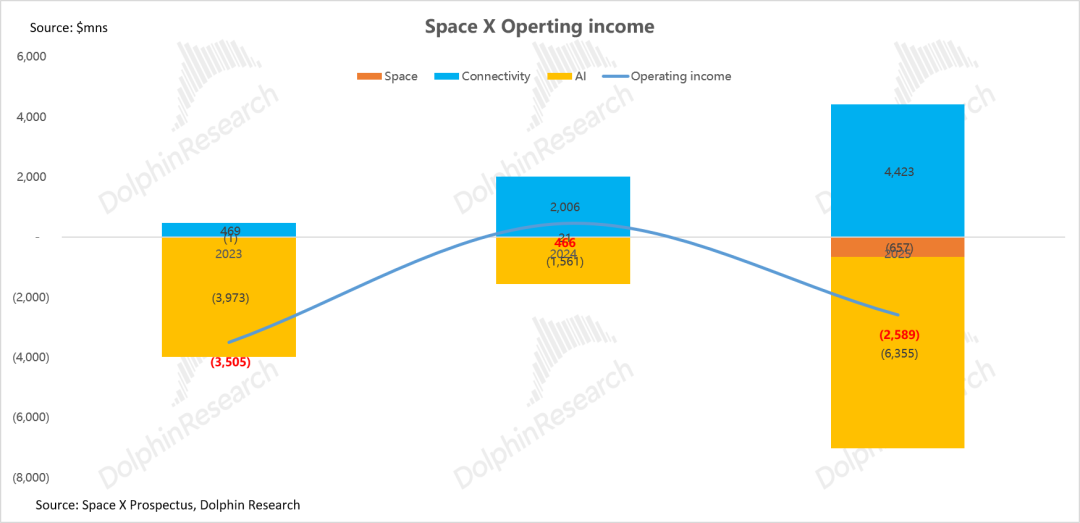

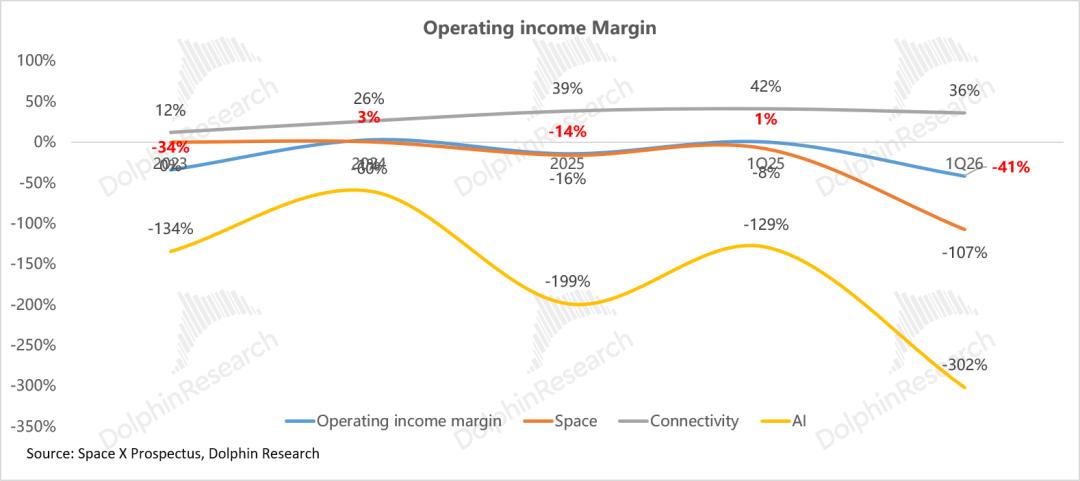

Operating profit skyrocketed nearly 10x from $470 million to $4.4 billion, with a segment EBITDA margin of 63%—a true cash cow.

③ Feeding Two 'Cash Incinerators' with Starlink Profits

With grand space conquest dreams, Starlink's profits won't be used for dividends. The two major 'cash incinerators' are Starship and space AI.

AI: Operating losses of $6.4 billion, devouring all Starlink profits and more. Investments focus on two areas: AI R&D—$5+ billion in 2025 (59% of total R&D spending)—and $12.7 billion in capex, accounting for >60% of capital outflows.

Space Segment Accounting Losses: While Falcon 9 is a cash generator, Starship's R&D entered a critical phase, with $3 billion in iterations causing the space transport business to post a $660 million operating loss in 2025 instead of profits.

III. The Soul of Space Hegemony: Where Lies the Confidence in Space Transportation?

The foundation of space infrastructure is space transportation. The key question here is: does space transportation have real business barriers? Let us explore this core business.

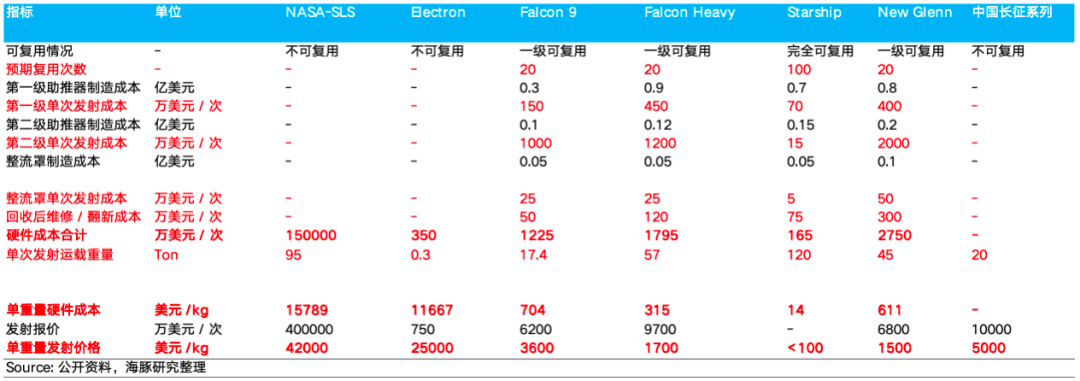

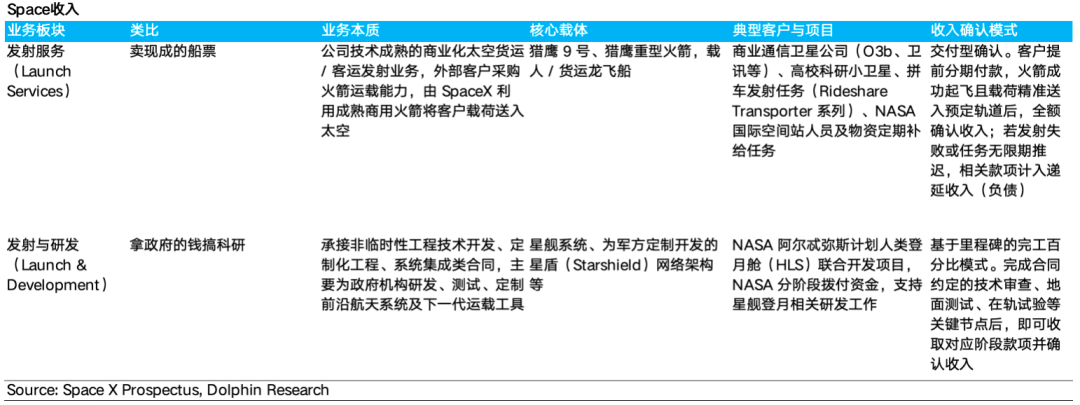

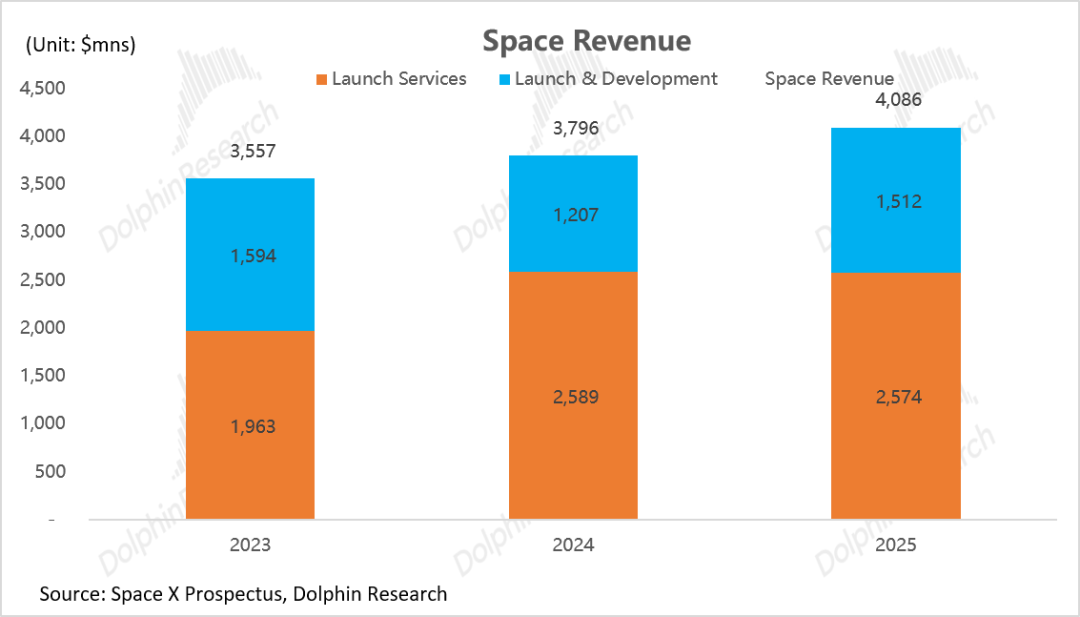

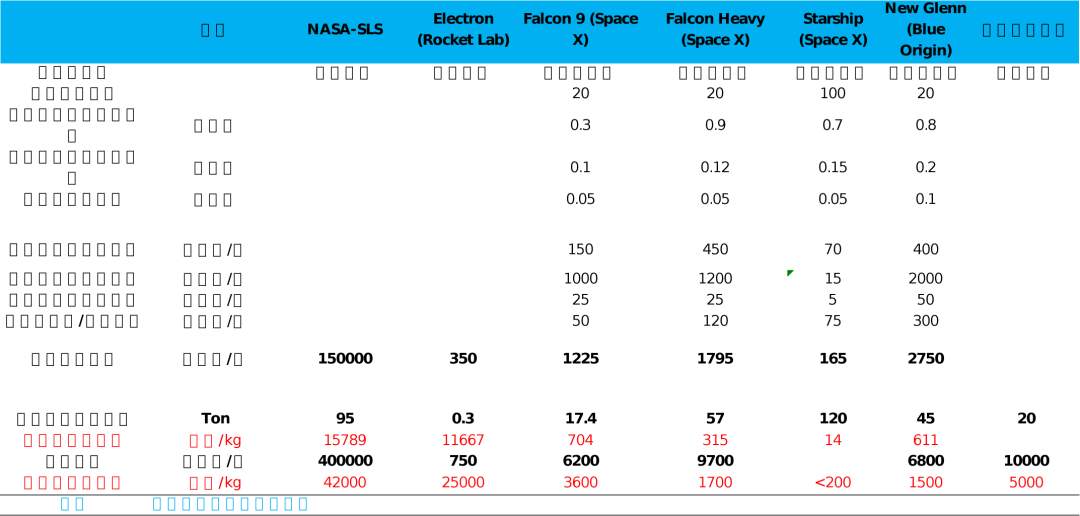

This sector is primarily composed of two core businesses: launch services, and launch and R&D operations. Together, they amounted to only USD 4.1 billion over 25 years, which is not a large sum.

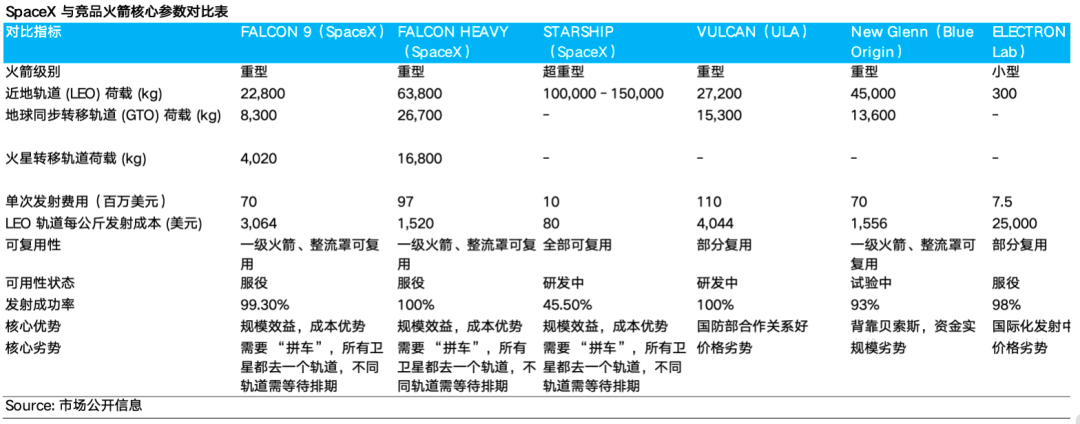

Currently, the primary investment focus lies in the development of the Starship rocket, which aims to achieve the world's first "fully and rapidly reusable" launch architecture (with both stages recoverable and striving for extremely short turnaround times and rapid relaunch capabilities). This innovation is expected to slash transportation costs to USD 200/kg, a significant reduction compared to Falcon 9's orbit insertion price of approximately USD 3,000/kg and traditional non-reusable rockets, which cost around USD 18,500/kg.

If this cost target is met, within the space economy ecosystem, objectives such as the deployment of the Starlink V3 satellite constellation and space-based computing, which require payload transportation, will naturally fall into place. The success or failure of Starship will directly determine whether SpaceX can unlock the next USD 10 trillion-scale market. This is not only a strategic gamble for the space sector but also crucial for the future valuation ceiling of the entire company.

For the space business, three critical questions arise:

① How significant are the barriers to achieving first-stage rocket reusability?

From Dolphin's perspective, these barriers primarily stem from engineering complexity, vertical integration, and hard-won experience. Competitors will take a considerable amount of time to catch up.

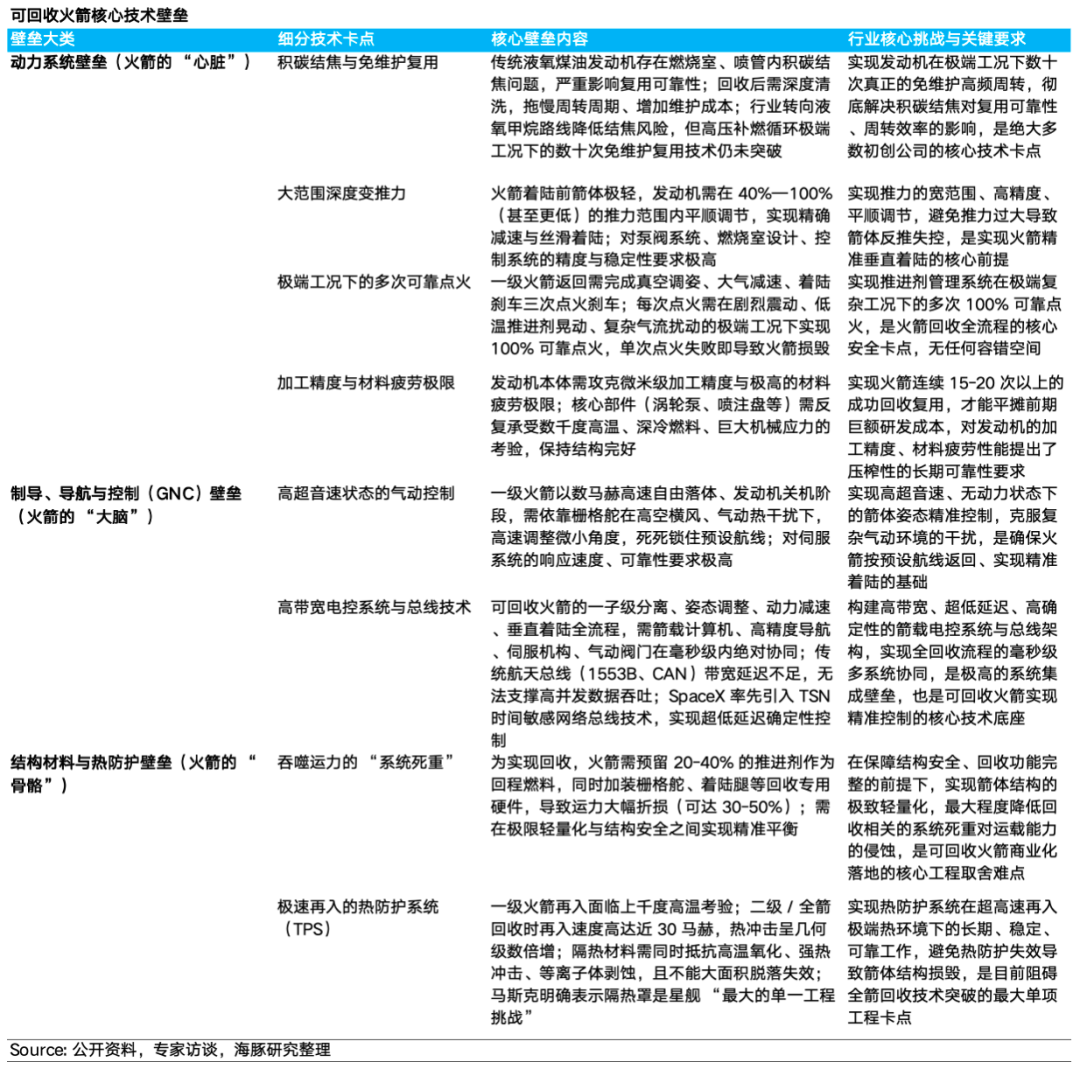

a. Technical Barriers: Engineering Challenges of the Highest Order

Vertical recovery is a feat of systems engineering that defies conventional physical limits. To land a rocket weighing dozens of tons and traveling at multiple times the speed of sound, fundamental engineering limits must be overcome across three dimensions: propulsion, control, and materials.

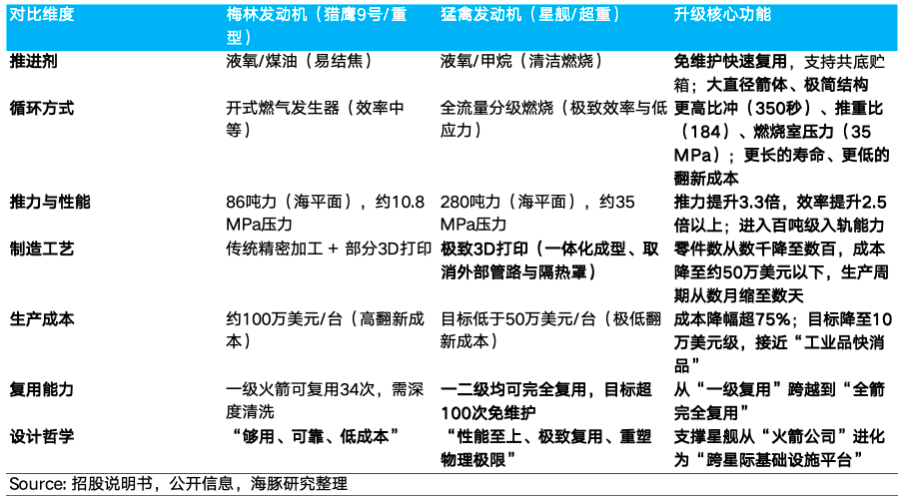

Propulsion (engines): Traditional fuels are prone to carbon deposition, which affects reusability. Therefore, liquid oxygen-methane engines are necessary for longevity and reliability. Engines must also possess "deep throttle capability" (the ability to precisely reduce thrust to below 40% to prevent backflight) and execute three high-altitude ignition decelerations flawlessly under extreme conditions of high-speed descent and severe turbulence.

Control (the brain): The difficulty is akin to "throwing chopsticks from dozens of kilometers high and landing them upright." As the rocket hurtles supersonically toward Earth, it must rely on titanium alloy grid fins at the top to efficiently counteract strong winds, correcting its attitude with millisecond-level precision to lock onto the recovery vessel at sea.

Materials (the skeleton): The exterior must withstand friction temperatures exceeding a thousand degrees Celsius during atmospheric reentry, while the interior must accommodate cryogenic propellants at -200°C. Simultaneously, the rocket body must be ultra-lightweight to offset the payload penalty caused by retaining recovery fuel.

For details, see the figure below:

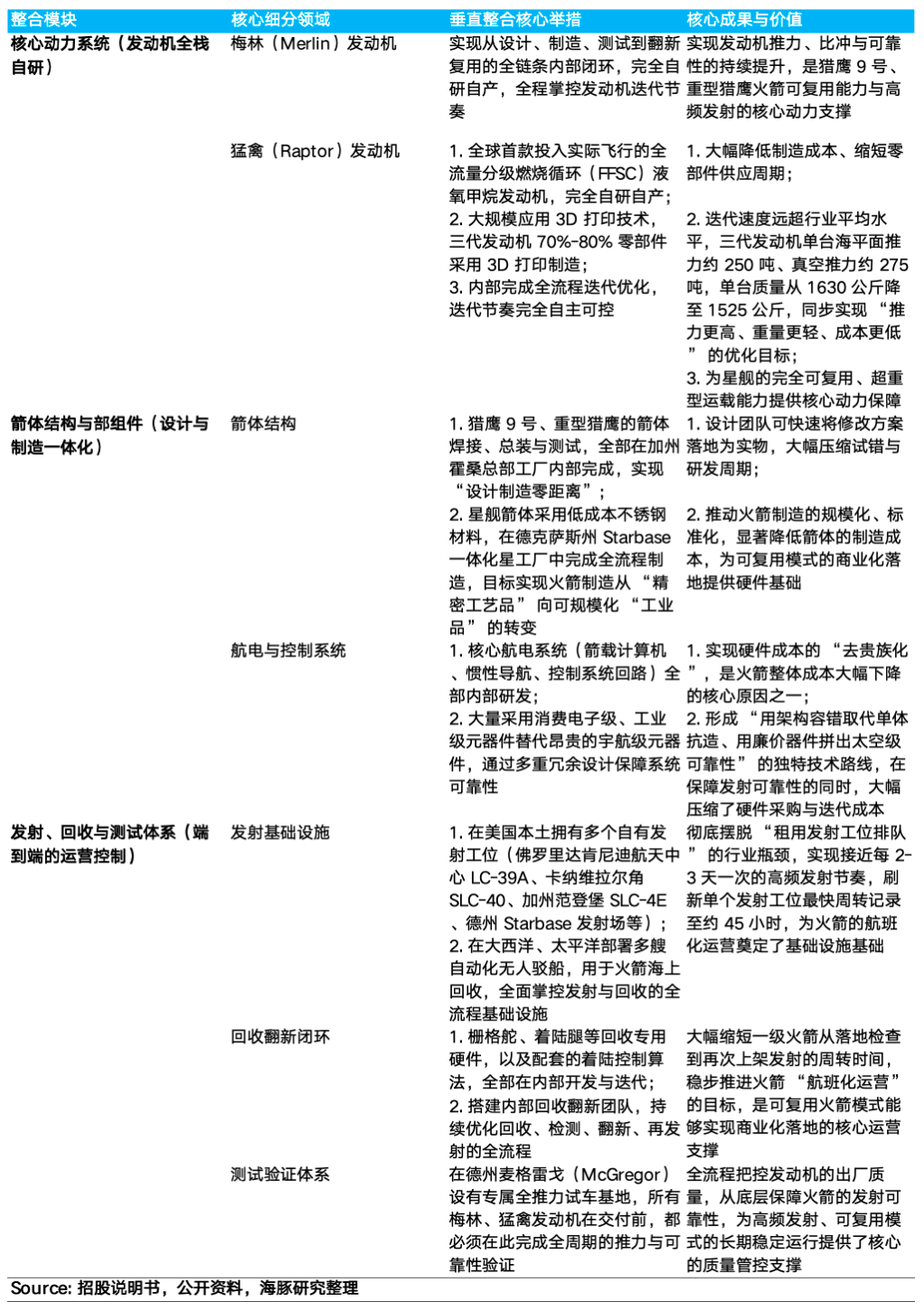

c. Vertical Integration: Core Competencies Kept In-House

Unlike traditional aerospace enterprises, which heavily rely on tiered supplier systems, SpaceX's strategy is to internalize as much as possible, pursuing extreme vertical integration. Currently, SpaceX has achieved approximately 80% self-research and self-production of core hardware, with only about 20% of standardized or specially customized components dependent on external procurement (e.g., specific high-precision sensors, specialized composite materials, and some general electronic components).

Vertical integration covers the highest-cost and most technologically critical areas: rocket engines, airframe structures, and launch, recovery, and testing systems. Competitors will face significant time costs to catch up.

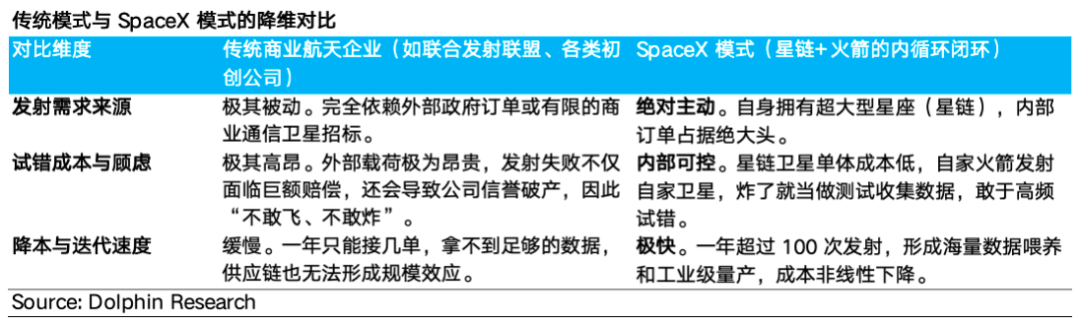

c. Barriers of Launch Density and Flight Experience (Self-Sufficient Starlink Internal Circulation and Data Feeding):

In the commercial space market, "reliability" is the paramount metric. A high-orbit commercial communications satellite can cost hundreds of millions of dollars, and a launch failure means years of investment evaporate. Thus, government and commercial clients always prioritize flight experience as a hard indicator.

SpaceX has its own transportation business, providing high-frequency real-world trial-and-error opportunities. Each rocket launch returns vast amounts of extreme-condition data (temperature distribution, vibration frequency, aerodynamic disturbances, etc.), which are used to refine flight control code and structural models.

This "data flywheel" and engineering know-how, nurtured by hundreds of real flights, constitute an absolute "time barrier" that cannot be quickly overcome by simply throwing money at talent poaching.

d. Barriers of Cost and Pricing Power (Economic Dominance)

The reusability of first-stage rockets, achieved through extreme engineering control, vertical integration, and accumulated launch experience, yields significant economic benefits:

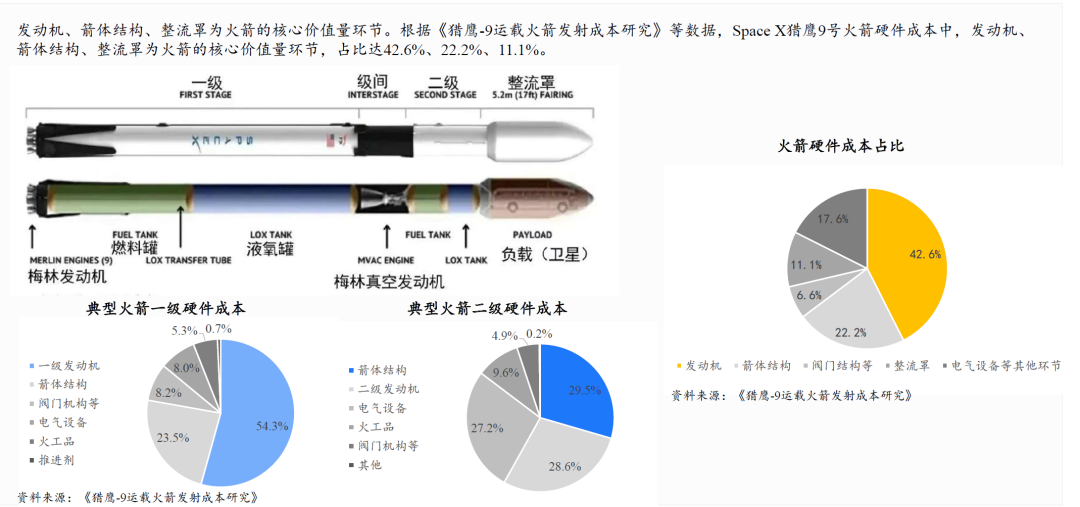

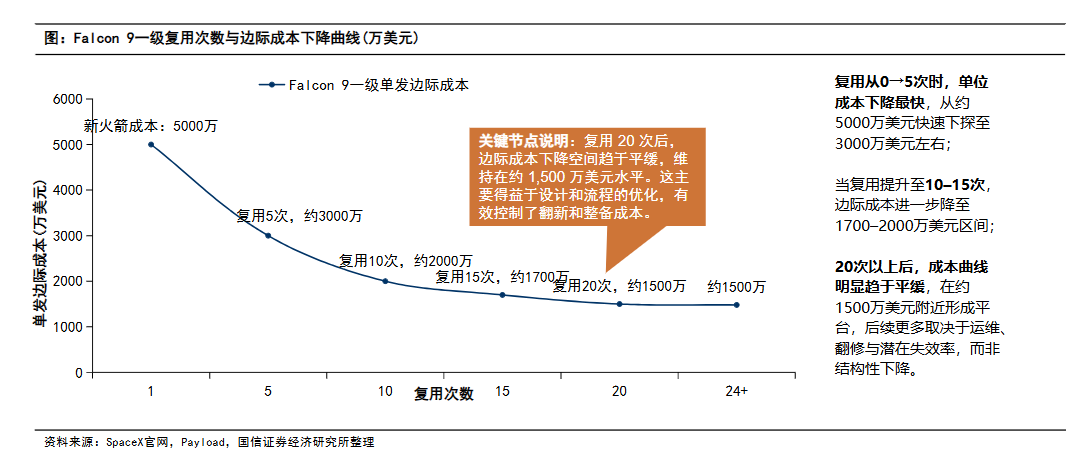

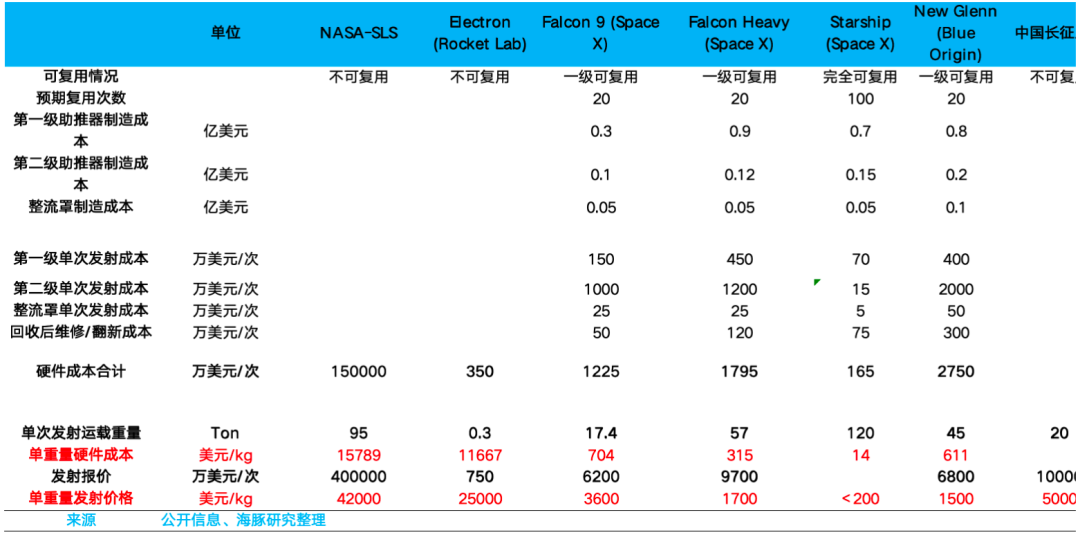

In Falcon 9's hardware costs, the first-stage booster and fairing together account for up to 70%. Under the traditional "expendable" model, each launch required fully bearing approximately USD 50 million in manufacturing costs. Falcon 9's first-stage booster has now achieved up to 34 reuses (as of late 2025), slashing the internal marginal cost per launch (including refurbishment, fuel, and measurement and control) to below approximately USD 15 million, a 70% reduction.

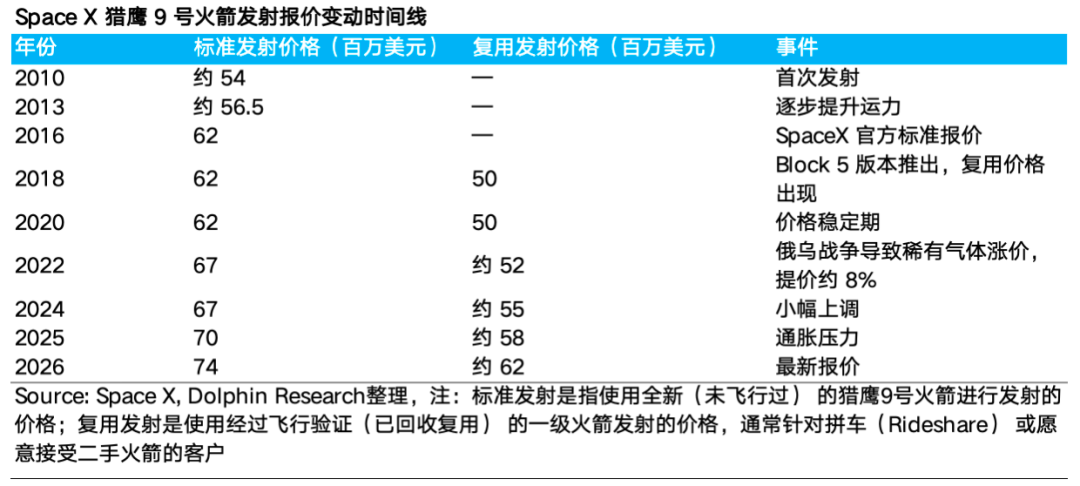

This extreme cost advantage grants SpaceX absolute market pricing power: even maintaining external quotes of approximately USD 74 million/62 million (standard launch/reusable launch), it still enjoys extremely generous gross margins.

If faced with potential competition, SpaceX has ample "price-cutting ammunition" to reduce quotes below USD 30 million, enough to trap any competitor using expendable rockets in a "launch-one, lose-one" death spiral from the starting line.

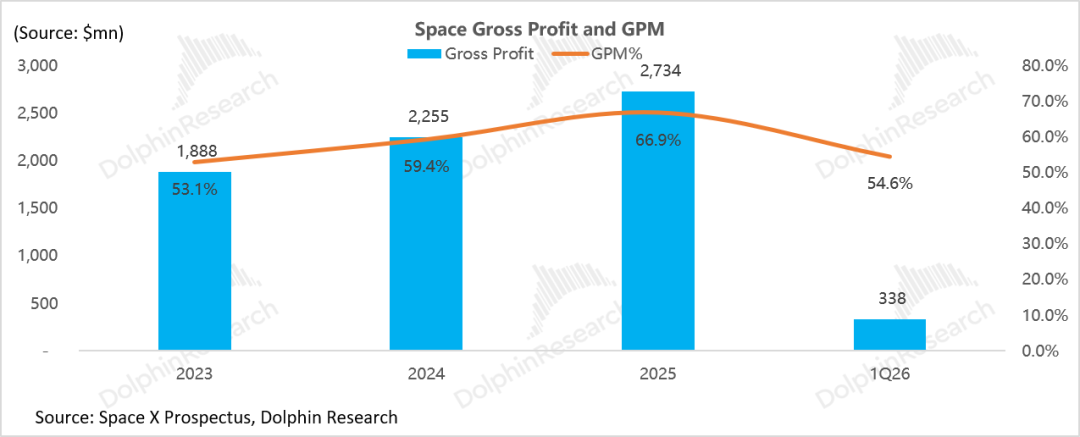

From the gross margin perspective of the launch business, it gradually increased from approximately 53% in 2023 to about 67% in 2025. The core driver is similarly the systemic cost reduction from rocket reuse (as reuse counts increase, marginal costs decrease), while launch pricing has not declined synchronously and has even steadily risen, creating an increasingly large "gross margin scissor gap." In fact, SpaceX has continuously raised prices.

This reflects true supply-demand dynamics: SpaceX is using its monopoly position to reap high profits, while the market lacks low-cost and mature alternative supply. This strategy ensures that nearly all cost-reduction dividends are converted into company profits rather than passed on to clients, thereby funding the next generation of rocket R&D (Starship).

However, in Q1 2026, SpaceX's launch business gross margin declined from approximately 66% year-on-year to about 55%, primarily due to:

a. Changes in launch service revenue mix: With the full implementation of the U.S. Department of Defense's "National Security Space Launch" (NSSL) Phase II contracts and increased tasks under NASA's Artemis program, the proportion of relatively low-margin government and defense task revenue rose from approximately 35% year-on-year to about 47% in the same period of 2026, directly dragging down the overall gross margin.

b. Drag from new product Starship V3's R&D: As a brand-new rocket, Starship V3's manufacturing costs are far higher than those of the mature, mass-produced Falcon 9, which has undergone over 300 recovery validations. The new rocket's low yield rates and high supply chain integration costs have increased fixed costs per launch (e.g., airframe manufacturing, engine test firings).

Although Starship V3's 12th test flight (May 2026) successfully completed most objectives, the first-stage booster fell into the sea due to multiple engine restart failures, with test flight costs (including rocket hardware losses) directly charged to the current launch business costs, dragging down the gross margin.

Meanwhile, the depreciation and amortization costs from Starship's massive capital expenditures are also partially charged to the cost side, further diluting profit levels.

②. How much longer will the leaders in reusable technology stay ahead of their competitors?

Judging from the current progress of competitors in reusable technology, SpaceX still holds an overwhelming lead. However, different competitors are at varying stages of catching up:

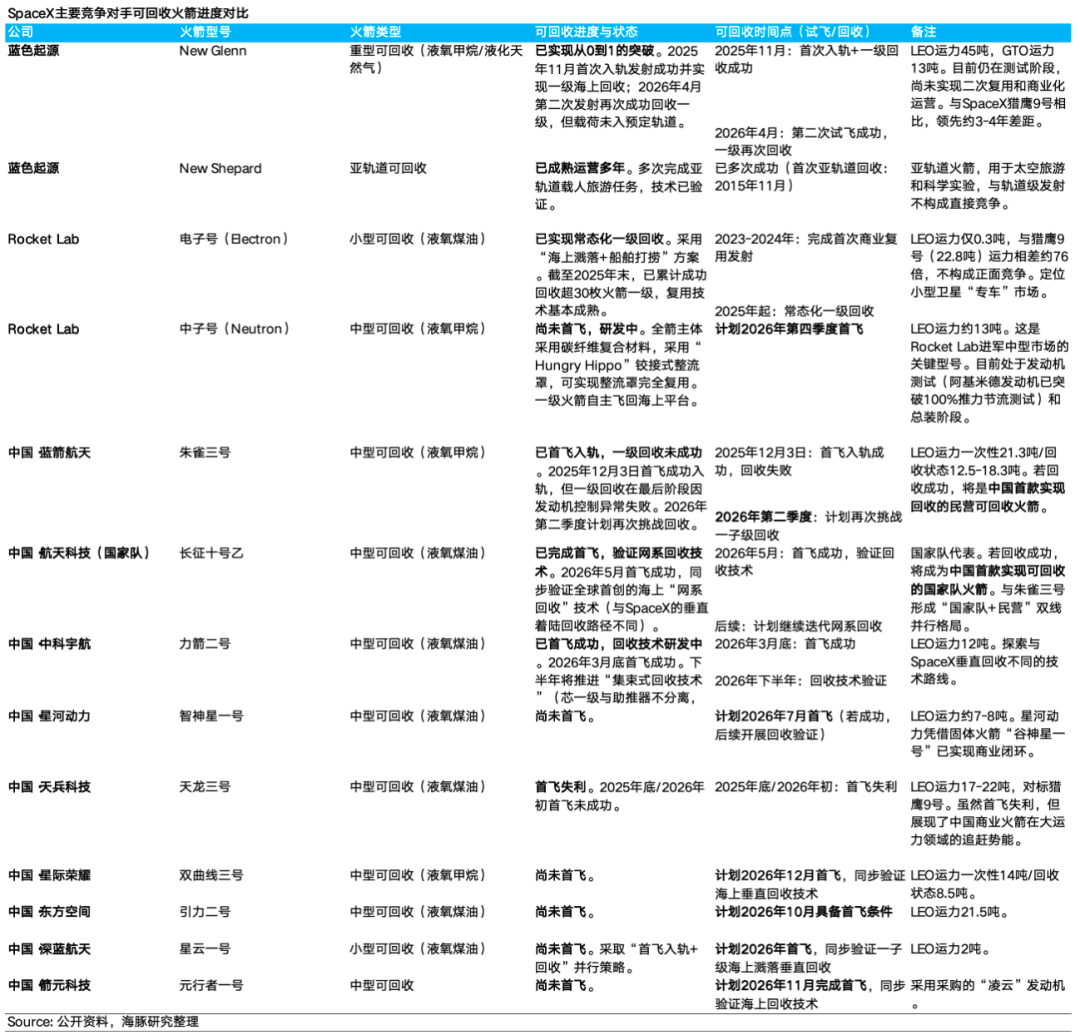

First Tier: Bezos' Blue Origin. The New Glenn rocket successfully achieved first-stage rocket sea recovery in November 2025, becoming the second company globally to achieve orbital-class rocket recovery. In April 2026, it accomplished its first reuse and recovery, marking a breakthrough from 0 to 1.

However, due to insufficient experience in reuse, New Glenn has not yet entered the stage of stable reuse and commercial operation. In contrast, Falcon 9 has accumulated over 10 years of engineering experience and more than 300 recovery data since its first successful recovery in 2015. It is expected to take several more years for New Glenn to reach the current level of stable operation achieved by Falcon 9.

Second Tier: Rocket Lab. The Electron small rocket has partially validated its first-stage recovery and engine reuse capabilities through a parachute descent approach (having successfully reused an engine once). However, full rocket reuse has not yet been achieved.

The highly anticipated Neutron rocket, Rocket Lab's counterpart to Falcon 9, is expected to conduct its maiden flight in the second half of 2026, without attempting vertical recovery on its first flight. Therefore, substantive competition with SpaceX's Falcon 9 is at least 2-3 years away. The true test will be whether Neutron can successfully achieve recovery at that time.

Third Tier: China's commercial space sector. As of June 2026, China has not yet achieved successful recovery of an orbital-class rocket, placing it in the 'pre-reusable era.' However, China is at a critical stage of localized breakthroughs and intensive sprints: The Long March 10B is set for its maiden flight and will validate the world's first sea-based net recovery system. Additionally, models like the Zhuque-3 and Lijian-2 are undergoing intensive launch validations.

The industry widely expects that from the second half of 2026 to the first half of 2027, China is poised to achieve the 'zero breakthrough' in reusable rockets, officially becoming the second country globally with this capability after the United States.

Overall, global competitors are still striving to overcome the '0 to 1' technological threshold, while SpaceX has already entered the '1 to 100' phase of data-driven scaling and exponential growth. This rigid time gap of 10-12 years cannot be bridged by capital alone in the short term.

③. Why is the launch market still 'niche' despite lower prices?

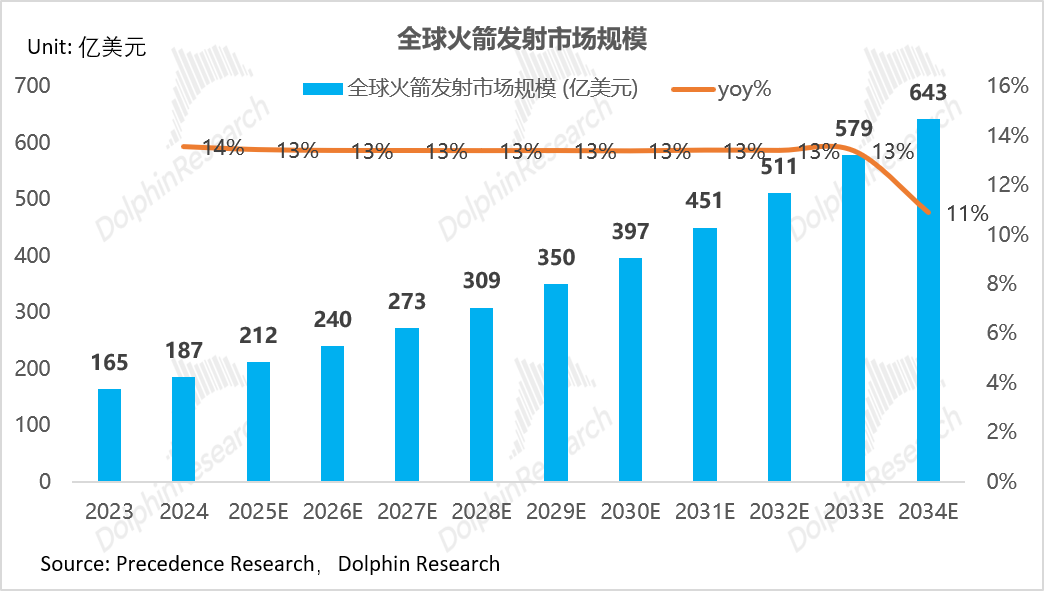

In 2024, the global rocket launch market was valued at approximately $18.7 billion. According to Precedence Research, it is projected to reach only $64.3 billion by 2034, with a compound annual growth rate (CAGR) of around 13%. Compared to other explosive tech sectors (e.g., satellite internet, AI computing power), this growth rate appears relatively modest.

From Dolphin Research's perspective, two key 'locks' are at play:

1. Demand-side structure: Dominated by stock-based competition

a. Traditional communications satellites (GEO) market is saturated or even shrinking: Core clients (e.g., international satellite communications organizations) procure large geostationary orbit (GEO) communications satellites characterized by high unit prices and long lifespans (15+ years). This is essentially a stock replacement market. Coupled with the depletion of GEO orbital slots, the global annual launch volume remains at just a dozen to twenty satellites, making the market extremely stable but lacking growth elasticity.

b. Government and defense missions are high-value but low-frequency: Core clients (e.g., NASA, U.S. Space Force, and national space agencies) undertake missions (e.g., deep space exploration, high-value reconnaissance satellites) with single contract values reaching hundreds of millions of dollars. However, these missions involve extremely long development cycles and infrequent launches, preventing the formation of normalized, high-frequency launch patterns.

c. Non-Starlink low Earth orbit (LEO) constellations are lagging and lack economies of scale: Other players face high transportation costs, failing to establish viable commercial cycles. Only 'Starlink' has successfully implemented a broadband subscription model in the consumer (C-end) market, creating a virtuous cycle of 'launch → network formation → operation → profitability → re-launch.' To some extent, SpaceX selectively prioritizes self-supply of capacity for low-cost transportation, forming a downstream commercial monopoly in scale.

d. The markets for remote sensing and micro/small satellites are characterized as 'long-tail' with notably low average contract values: These markets are primarily driven by long-tail clients, including universities and startups. Micro/small satellites are designed to be lightweight, resulting in extremely low contract values per unit (in the range of millions of dollars), and heavily rely on 'rideshare/secondary launch' models. Although the volume of launches is on the rise, their share of the total addressable market remains negligible, posing challenges for sustaining high growth independently.

2. Supply-side dynamics and industrial synergy: Cost barriers persist, with a mismatch between upstream/downstream capacities and commercial closures.

a. Launch costs remain a significant barrier to unlocking emerging demand: Despite Falcon 9's reusable technology reducing commercial launch prices from $10,000-20,000/kg to approximately $3,000/kg, these costs are still prohibitive for the majority of scientific and commercial missions.

Until launch costs experience a dramatic reduction (e.g., below $100/kg), economic models for emerging sectors such as space tourism, space-based pharmaceuticals, and in-orbit manufacturing will remain unfeasible. Furthermore, high satellite insurance premiums continue to inflate the overall usage costs for clients.

Thus, only when next-generation fully reusable launch vehicles (e.g., Starship) drive launch costs down to the $100s or even $10s/kg range and achieve 'airliner-like' operational turnaround rates—effectively transforming rockets into low-cost 'space trucks'—can downstream new applications truly flourish. Only at that point will the rocket launch market witness genuine exponential growth.

b. 'Rockets await satellites': Persistent issues include lengthy satellite manufacturing cycles and payload capacity bottlenecks. Even with sufficient rocket capacity, traditional satellite manufacturing remains mired in 'artisanal' or small-batch customization phases, with high-value satellites often requiring 2-3 years to construct. To a certain extent, SpaceX has established a near-monopoly on satellite manufacturing capacity.

④. What progress has been made on the next-gen game-changer, Starship? When can it achieve mature reuse of both its first and second stages?

While Falcon 9's reuse technology has reached its limits, with single-launch marginal costs reduced to around $15 million, this figure is constrained by irreducible costs (e.g., non-recoverable upper stages, propellant, and refurbishment), approaching physical lower bounds.

To achieve a significant reduction in orbital launch costs (from approximately $700–1,000/kg to below $200/kg) and unlock higher-value downstream sectors (e.g., large-scale Starlink V3 constellation deployment, space-based AI data centers), full reusability of Starship—enabling recovery of both the first-stage booster and second-stage spacecraft—is essential.

Judging from the current progress, the iteration of Starship is accelerating. On May 23, 2026, Starship successfully completed its 12th test flight, marking the debut of the V3 version.

This test flight validated several key upgrades: a new Raptor 3 engine, improved thermal protection (achieved by removing some heat shield tiles to test extreme heat flux data), and the spacecraft's ability to deploy 20 simulated Starlink V3 satellites and 2 modified satellites in orbit. The spacecraft executed a controlled splashdown in the Indian Ocean.

Although the first-stage booster disintegrated and crashed into the sea prematurely due to multiple engine restart failures during its return, the spacecraft successfully accomplished over 95% of its primary mission objectives. This flight signified Starship's transition from 'technical validation' to 'capability validation'.

The specific timelines for achieving mature reuse of both stages necessitate separate assessments:

First-stage recovery: Starship has already validated the launch, recovery, and reflight capabilities of its super-heavy booster across multiple test flights, with the technical path largely proven. The first stage is anticipated to reattempt and likely succeed in recovery during the 13th or 14th test flight.

Second-stage recovery: This represents the final hurdle for Starship to achieve 'full reusability.' Currently, the spacecraft has only accomplished soft ocean landings, without yet demonstrating tower capture and refurbishment reuse. The spacecraft's thermal protection system, re-entry control, and landing precision still require further refinement through multiple iterations.

Musk previously stated that Starship could achieve full rocket reusability in 2026, with orbital payload delivery missions expected to commence in the second half of 2026.

Following full validation, Starship will initially deploy SpaceX's own Starlink V3 satellites (capable of launching up to 60 satellites per mission, adding over 60 Tbps of network capacity per 2-3 monthly flight validations). Subsequently, it will enter a mature phase of commercial launch services for external clients around mid-2027 (after 5-6 flight validations).

This timeline aligns with market expectations for Starship to commence deploying orbital AI computing satellites in 2028—a necessary precursor for establishing space-based computing infrastructure.

Regarding cost targets, Starship aims to reduce unit launch costs to $200/kg under full reusability, facilitating large-scale Starlink V3 constellation deployment (with per-satellite capacity 20 times higher than Gen 2, launching approximately 60 satellites per Starship mission), space-based AI data centers (planned from 2028), and long-term Mars exploration—unlocking new markets on a $10 trillion scale.

Starship's progress toward full reusability will directly determine whether SpaceX can evolve from a 'capacity hegemon' to a 'cross-interplanetary infrastructure platform.' It serves as the sole bridge connecting SpaceX's current cash cow to future trillion-dollar opportunities and is the core driver for scaling the rocket launch market from its current $10 billion level to higher orders of magnitude.

Overall, in the space transportation sector, Musk seems to have delivered another asset that stands unparalleled, even when viewed through a telescope. We will subsequently shift our focus to satellite manufacturing and communications network businesses—stay tuned.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprints require explicit authorization.

// Disclaimer and General Disclosure

This report is intended solely for general synthetic data purposes, catering to users of Dolphin Research and its affiliated institutions for general reading and data reference. It does not take into account the specific investment objectives, product preferences, risk tolerance, financial status, or unique needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person using or referencing the content or information in this report for investment decisions assumes all associated risks. Dolphin Research shall not be held liable for any direct or indirect damages or losses arising from the use of data contained herein. The information and data in this report are based on publicly available sources and are provided for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, or completeness of such information and data.

The views, opinions, and analytical methods expressed in this report are those of the individual contributors and do not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright exclusively owned by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to any unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek