Space X: The Sky Network - Is It Unstoppable?

06/16 2026

06/16 2026

561

561

As we discussed in our previous article, 'From Daydreams to Billions: Is SpaceX Really That Sci-Fi?', Starlink has quietly taken the lead, becoming the absolute core driving SpaceX's performance growth and profit generation. It even provides crucial financial 'infusions' for SpaceX's ambitious AI strategy.

Starlink is far more than just a communications segment; it serves as the 'super foundation' supporting SpaceX's long-term ambitions. Imagine if Starlink were stripped away—SpaceX's valuation would revert to its original prototype of a rocket manufacturing and launch provider. Without Starlink's stable cash flow to support it, the enormous costs of Starship development and heavy investment in AI would be untenable.

So, how exactly was this 'super cash cow' created? In this report, we shift our focus to the fundamentals and conduct an in-depth analysis of this 'space network' asset, which has achieved a commercial closed loop and holds an absolute monopoly. Dolphin Research will concentrate on answering four core questions about Starlink's business:

1. Why has Starlink succeeded in establishing a viable business model and become a stable profit-generating 'cash cow'?

2. Mobile Network Satellite Edition: Can it directly compete with mobile operators?

3. As a communications operator, what advantages does Starlink have over its peers?

4. What are the core competitive moats and barriers of Starlink's business?

The following is a detailed analysis:

I. How Starlink Achieved a Viable Space Communications Business Model

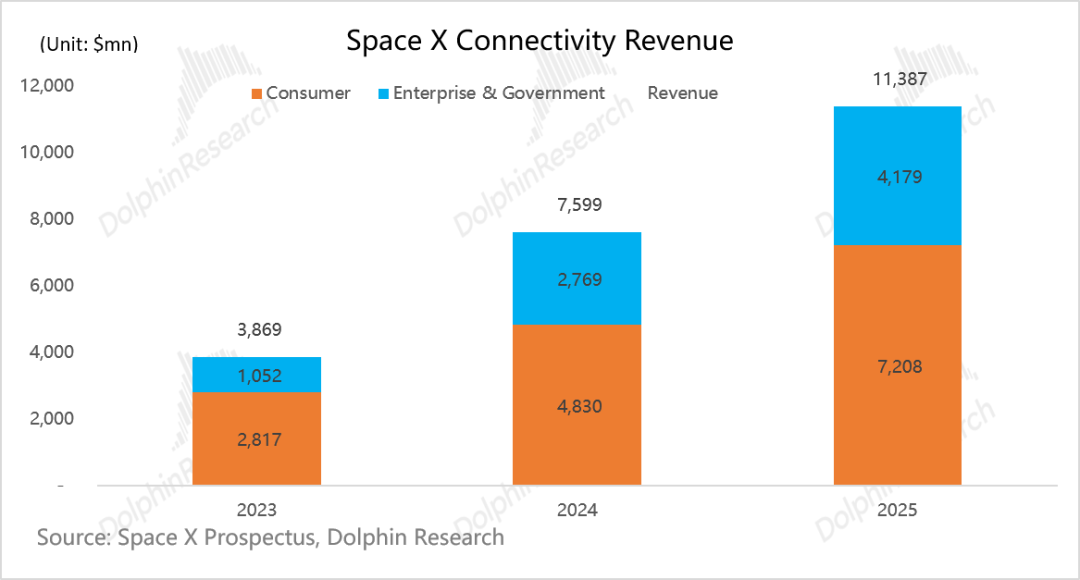

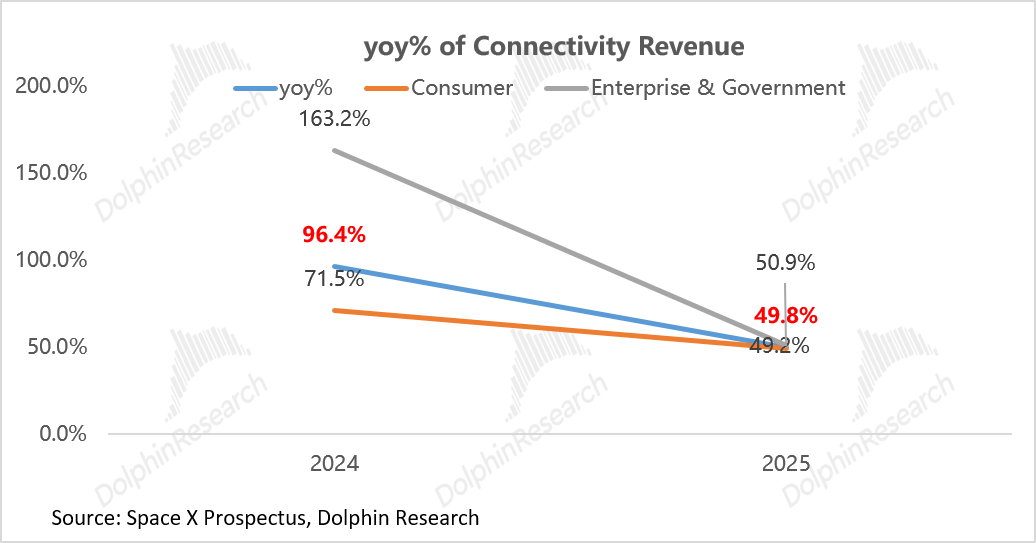

Starlink is the cornerstone of SpaceX's transformation from a 'rocket launcher' to a 'global communications and computing operator.' From 2023 to 2025, Starlink's revenue surged from approximately $3.9 billion to $11.3 billion, with a two-year compound annual growth rate exceeding 70%. Its operating profit soared past the break-even point, jumping from $470 million to around $4.4 billion, with an operating profit margin nearing 40%.

SpaceX's ability to achieve non-linear growth in both revenue and profit is fundamentally rooted in its success in establishing a commercial closed loop by 'using low-Earth orbit (LEO) satellite constellations to outmaneuver traditional geostationary (GEO) satellites and ground-based base stations.' It has also successfully activated a self-driven cycle of 'launch cost reduction → accelerated network deployment → user growth → profit reinvestment → rocket iteration.'

1) Satellite Communications: Dimensional Reduction Strikes from SpaceX's LEO Satellites

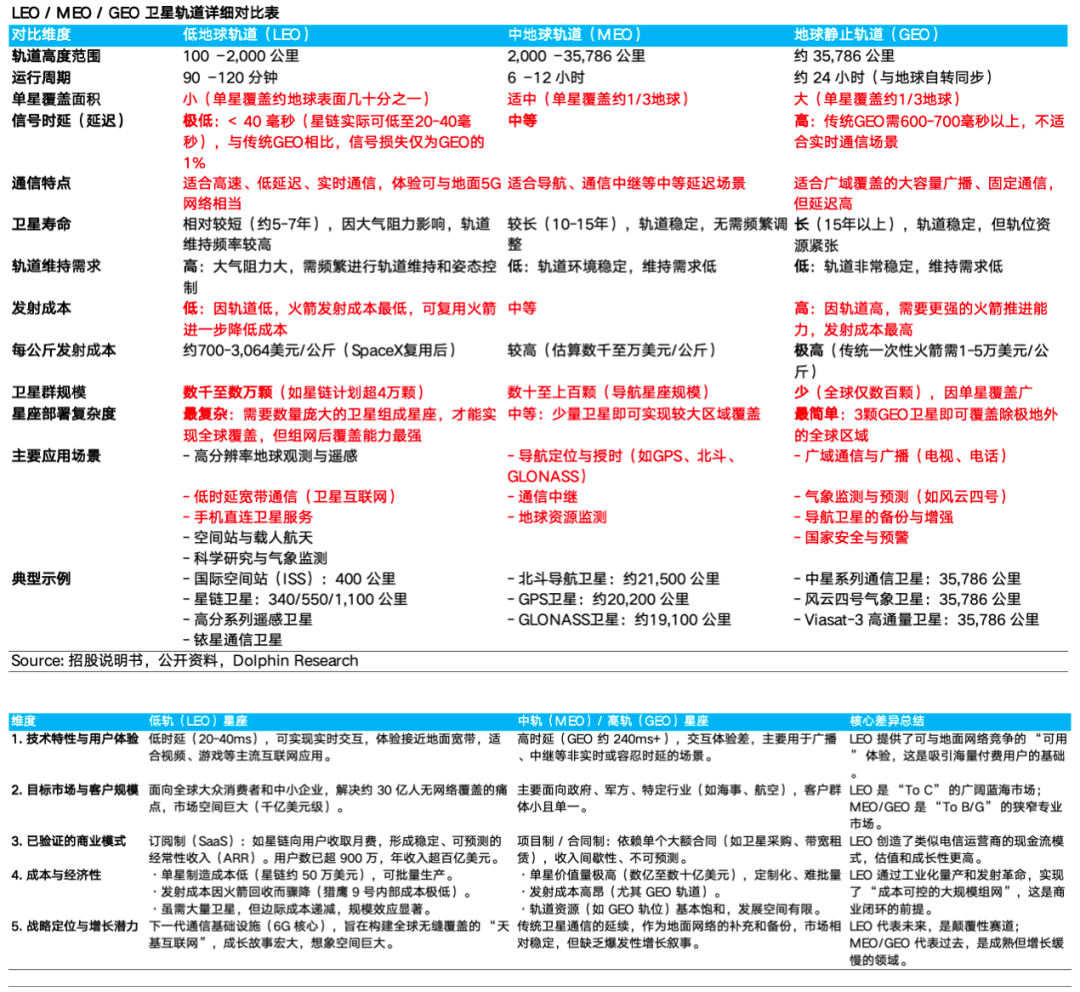

Traditional satellite internet relies heavily on GEO satellites (which appear stationary in the sky due to matching Earth's rotation speed and direction). However, located 36,000 kilometers above Earth, these satellites suffer from significant signal latency (actual interaction delay > 600ms) and poor throughput, making them unsuitable for modern applications like streaming media and cloud collaboration.

How does SpaceX address this?

a. LEO vs. GEO: Tackling Latency

Starlink's satellites are LEO satellites, orbiting at an altitude of just 550 kilometers. Due to their lower position, latency is only a fraction of that of GEO satellites, offering a user experience similar to ground-based fiber optics (low latency).

b. Constellation: Achieving Coverage

However, since these satellites complete an orbit around Earth in just a few dozen minutes, a single satellite's coverage time over a given location is limited. Full coverage requires a large constellation of satellites. This aligns perfectly with SpaceX's cost-effective launch services, enabling the creation of a massive satellite network.

c. Satellite Manufacturing: Assembly Line Cost Reduction

Under traditional artisanal methods, GEO satellites are nearly 'handcrafted,' with individual costs reaching hundreds of millions of dollars. SpaceX has reduced the cost of individual LEO satellites to just $500,000 through automotive-style assembly line production.

2) Customer Scenarios: Niche Market Competition

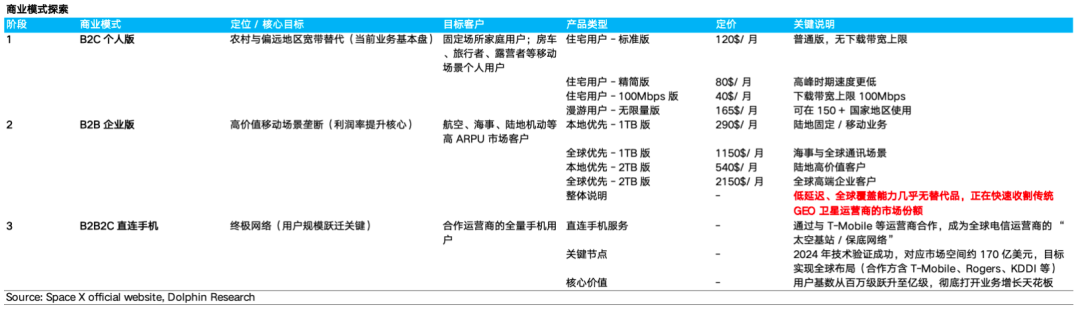

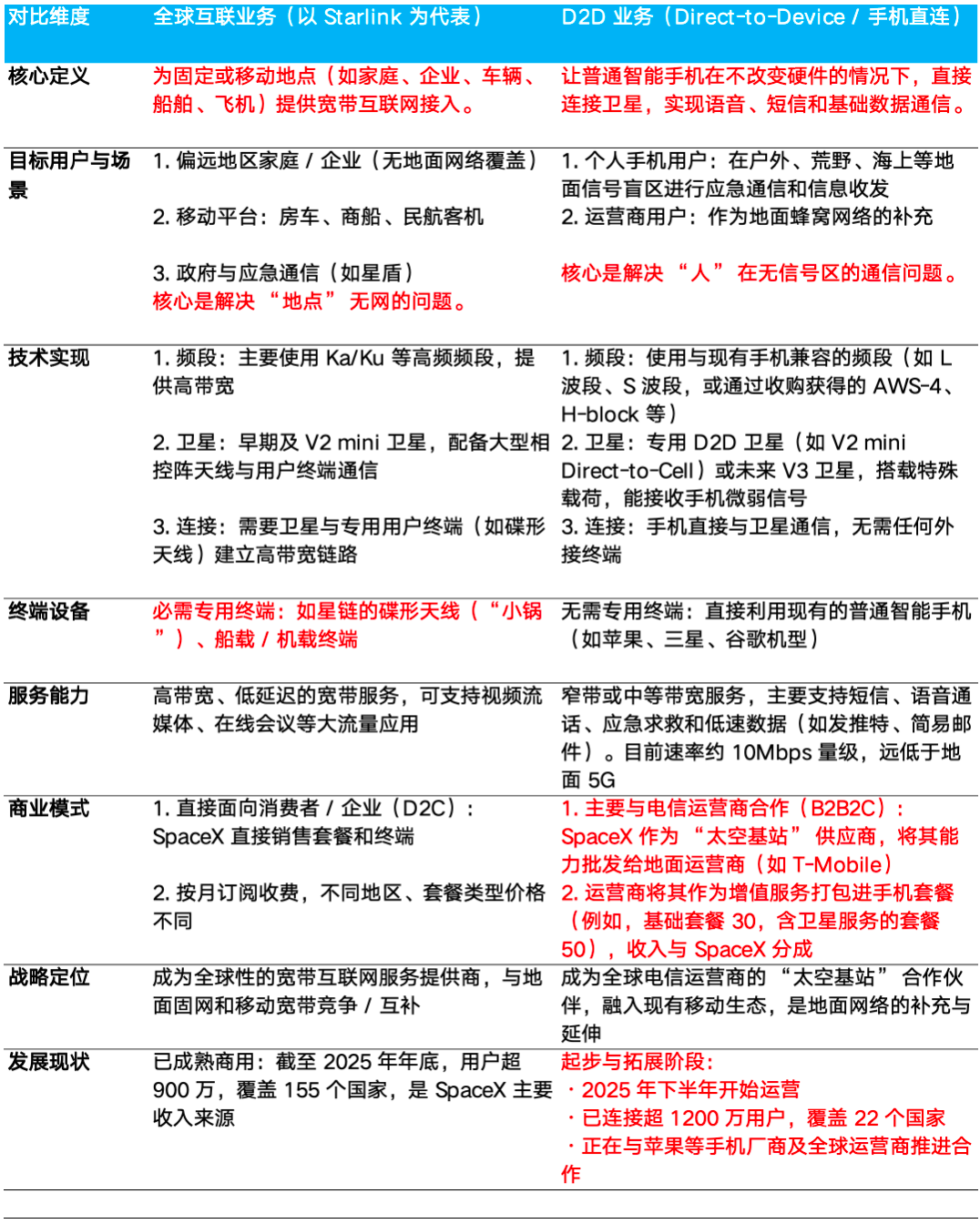

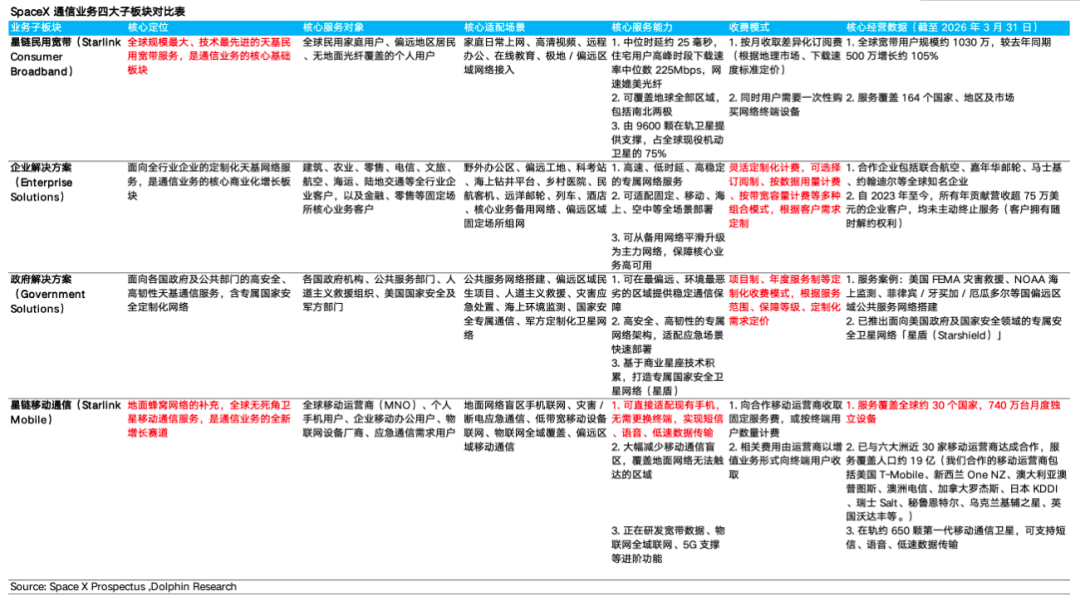

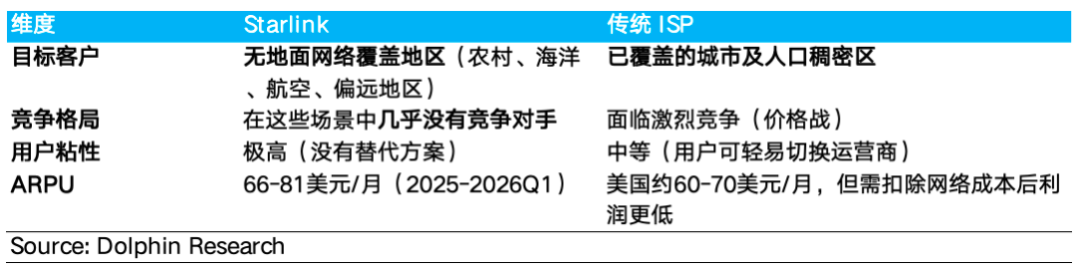

Starlink's strategy is clear: it avoids direct competition with traditional telecom operators in densely populated urban areas (where satellites cannot compete in terms of cost, bandwidth, or indoor coverage). Instead, it focuses on 'economic dead zones'—areas lacking ground-based coverage or where ROI for infrastructure deployment is unattainable (e.g., remote rural regions, oceans, aviation, and developing areas). This strategy has unlocked Starlink's commercial potential across three key segments:

a. To C Broadband: Targeting Ground Operators' 'Dead Zones'

Even in the AI era, approximately 3 billion people worldwide remain offline, with 90% located in rural or geographically complex remote areas. For traditional telecom operators, deploying fiber optics in these vast, sparsely populated regions is prohibitively expensive, making it an economically unviable 'long-term negative ROI' proposition.

Starlink's LEO satellite-based internet, forming a massive constellation network, represents the only technically and economically feasible solution for global, high-throughput coverage, capturing ground operators' 'economic dead zones.'

Technically, satellite broadband typically uses high-frequency bands (e.g., Ku/Ka bands). These signals, like fine sand, can carry vast amounts of data (high speed) but have extremely poor penetration, easily attenuating when encountering obstacles (e.g., tree leaves, walls, rain, or snow).

Therefore, Starlink broadband users must install a signal reception dish (technically known as a phased-array flat antenna, a core component of Starlink's ground terminals. It is a high-gain, electronically scanned smart antenna capable of focusing signals from passing satellites, something a small mobile phone antenna cannot achieve).

While slightly more complex than ground-based internet setups, dish installation is relatively straightforward—unbox, plug in, and connect to the internet without professional installation. Users simply place the dish in an open area with a clear view of the sky (no obstructions), connect it to power and a router, and they're set.

Currently, the dish costs around $500 (with a design lifespan of approximately 10 years). Early manufacturing costs for this device reached $3,000. However, by reshaping the supply chain in collaboration with consumer electronics giants (STMicroelectronics, MediaTek, Micron), SpaceX has reduced terminal costs to the hundreds of dollars, achieving hardware break-even.

In terms of pricing, beyond the cost of the signal reception dish, users pay a monthly network subscription fee. Starlink employs a highly precise price tiering strategy:

It offers premium plans ($120–165/month) for high-value regions and lower-tier entry plans (as low as $40/month in some emerging markets), rapidly expanding its user base with 'high quality at an affordable price.'

b. To B Broadband: Dimensional Reduction Strikes Against Traditional GEO for High-Value Demand

Enterprise Segment: In mobile scenarios such as aviation, maritime, and land-based oil and gas exploration, there is a demand for highly reliable, low-latency networks. This demand was previously met by GEO satellites, but LEO communications now offer a dimensional reduction strike. To B contracts generally feature significantly higher values and profit margins than consumer businesses.

Geopolitical To G: Demand for highly resilient, interference-resistant global connectivity in defense and security continues to rise. SpaceX has launched the dedicated 'Starshield' network, which has become the core infrastructure for critical U.S. military communications, supporting confidential communications, reconnaissance data relay, missile warning systems, and other defense-grade missions.

These contracts typically follow a 'cost-plus-fixed-profit' model with durations of 5–10 years, providing SpaceX with highly predictable revenue streams.

II. Mobile Network Satellite Edition: Direct Competition—Is There Hope?

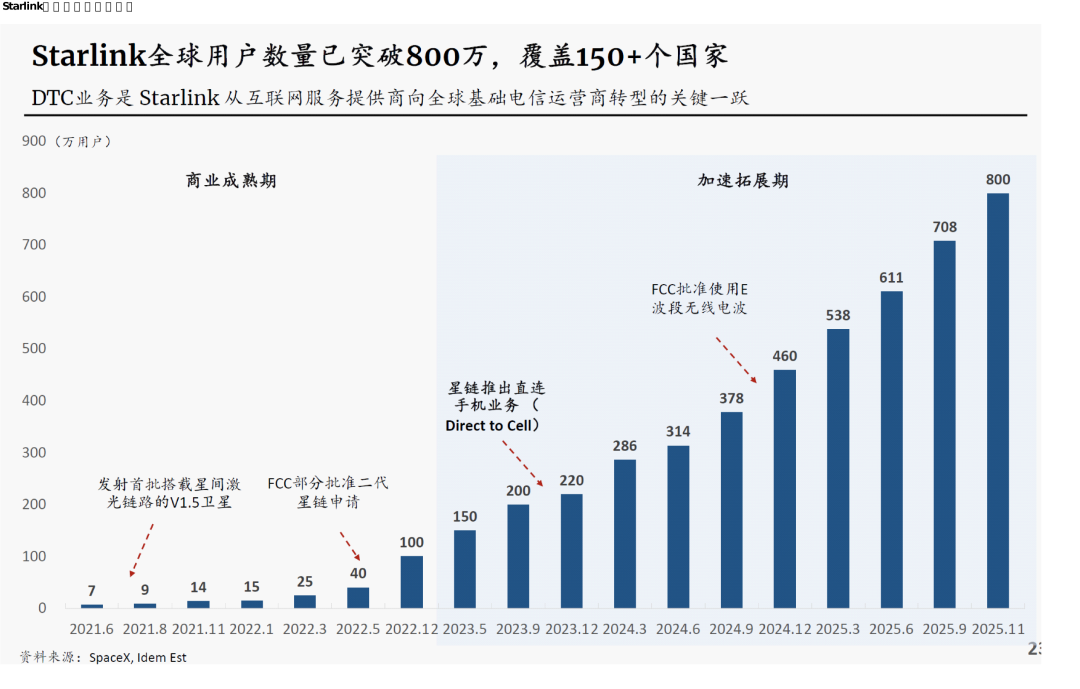

Thus far, Starlink's commercial success has primarily relied on niche market competition. However, Starlink aims to take the next step by pursuing inventory replacement (existing market substitution). Its solution is satellite-based mobile communications (Direct-to-Cell) to challenge traditional ground-based mobile networks.

From a user perspective, the high cost of the 'dish' and its limited usability have prompted the company to pursue satellite mobile communications (Direct-to-Cell) to enter the cellular market. Currently, global ground-based cellular networks cover only about 20% of land area. Solving mobile network issues in uncovered regions through satellite connectivity offers its own form of niche competition.

Of course, the essence of direct-to-cell technology is to eliminate the need for a 'dish' for user convenience, without altering the form factor of mobile phones. This requires:

a. Amplifying Satellite Signals: D2C satellites are typically equipped with massive phased-array antenna arrays spanning dozens or even hundreds of square meters (resembling giant kites in space).

The satellite uses this 'super megaphone' to broadcast loudly, allowing ground-based phones (with weak antennas and low power) to barely hear it. Simultaneously, the satellite possesses extremely strong (extremely strong) reception capabilities to 'hear' faint signals from phones.

Currently, SpaceX has 9,600 satellites in orbit, with only 650 dedicated to DTC mobile communications. However, deployment will accelerate starting in the second half of 2025.

b. Spectrum Switching: D2C typically uses lower authorized frequency bands (e.g., L-band 1.5–1.6 GHz, S-band 2.0–2.5 GHz). These signals, like 'small streams,' have strong penetration, barely passing through tree leaves or thin glass (allowing outdoor phone use). However, they carry limited data and cannot support high-speed internet (only enabling voice, text, and basic data communication).

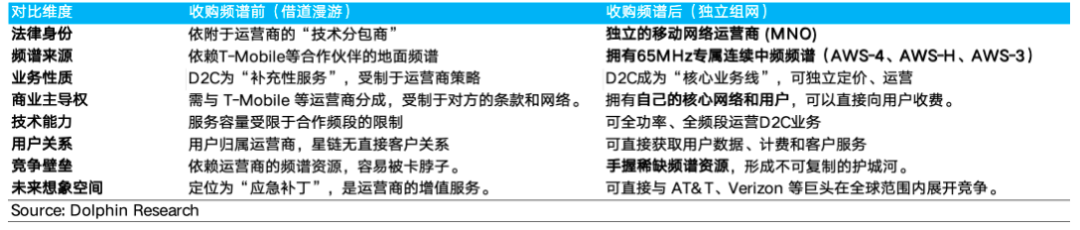

Spectrum is a scarce resource, with low-frequency bands primarily controlled by major operators. Starlink must 'roam' by partnering with operators. In these partnerships, SpaceX acts as a technical subcontractor: operators lease Starlink's satellite resources and sell 'satellite mobile data plans' to users in their stores, with revenue shared between SpaceX and the operator.

However, Dolphin Research notes that this technical compromise results in narrower bandwidth when broadband signals are converted to mobile signals (currently megabit-level shared access rather than hundred-megabit exclusive access). Its core positioning is 'availability of experience' rather than 'quality of experience'—meeting demand for emergency texting, calls, and narrowband data, not ultra-high-definition video or high-speed downloads.

Since video and high-speed downloads are nearly universal internet needs, Starlink's current mobile business model complements rather than competes with existing operator services. This service was only introduced in the second half of last year.

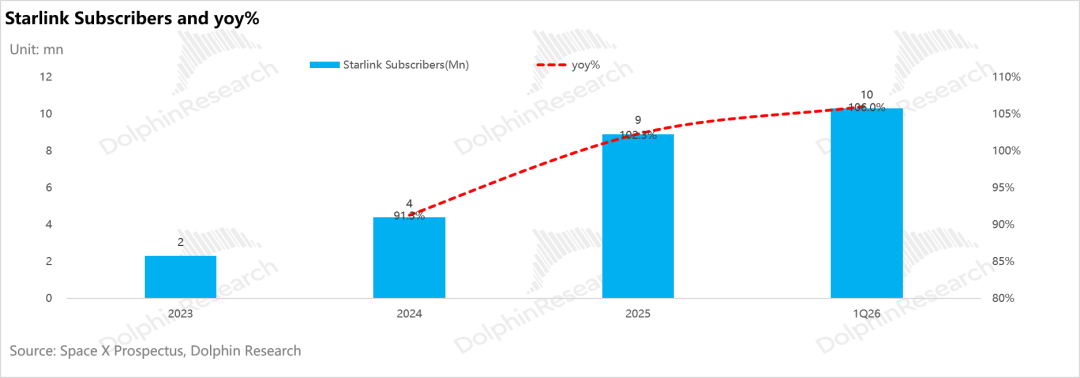

As of Q1 2026, Starlink mobile coverage spans 30 countries, with 7.4 million active devices and revenue-sharing agreements with 30 global mainstream mobile operators.

Based on Dolphin Research's estimates, the D2C business employs a revenue-sharing model with mobile operators. For example, in SpaceX's partnership with T-Mobile, users pay an additional ~$10/month, with SpaceX receiving ~$5.5/month in revenue share (according to public reports).

Assuming ~6 million connected devices by the end of 2025, the D2C business is projected to contribute ~$400 million in revenue in 2025, accounting for just 5.5% of Starlink's total C-end revenue (~$7.2 billion).

The next critical question is: Is it possible to compete directly with mobile operators using direct satellite connectivity? Let's examine how SpaceX is addressing its key vulnerabilities:

1) Spectrum Resources: Buying Spree?

We know that direct mobile-to-satellite connectivity faces a fundamental frequency band conflict—mobile terminals have extremely low transmission power (typically 200-500 milliwatts), requiring signals to penetrate the atmosphere and ionosphere for satellite capture.

High-frequency bands (e.g., Ka/Ku) offer high transmission speeds but have weak penetration and are susceptible to rain fade, making them unsustainable for uplink with mobile device transmission power. Low-frequency bands, with strong penetration and wide coverage, are adequately supported by mobile device transmission power for satellite reception and are already broadly adopted in ecosystems led by Qualcomm, MediaTek, and other mobile chip manufacturers.

Previously, Starlink's DTC service essentially relied on operator-owned frequency bands. However, in 2024, SpaceX acquired 65 MHz of Sub-6 GHz spectrum in the United States (with the acquisition set to complete after 2027), securing mid-to-low-band resources and enabling the possibility of independent network deployment.

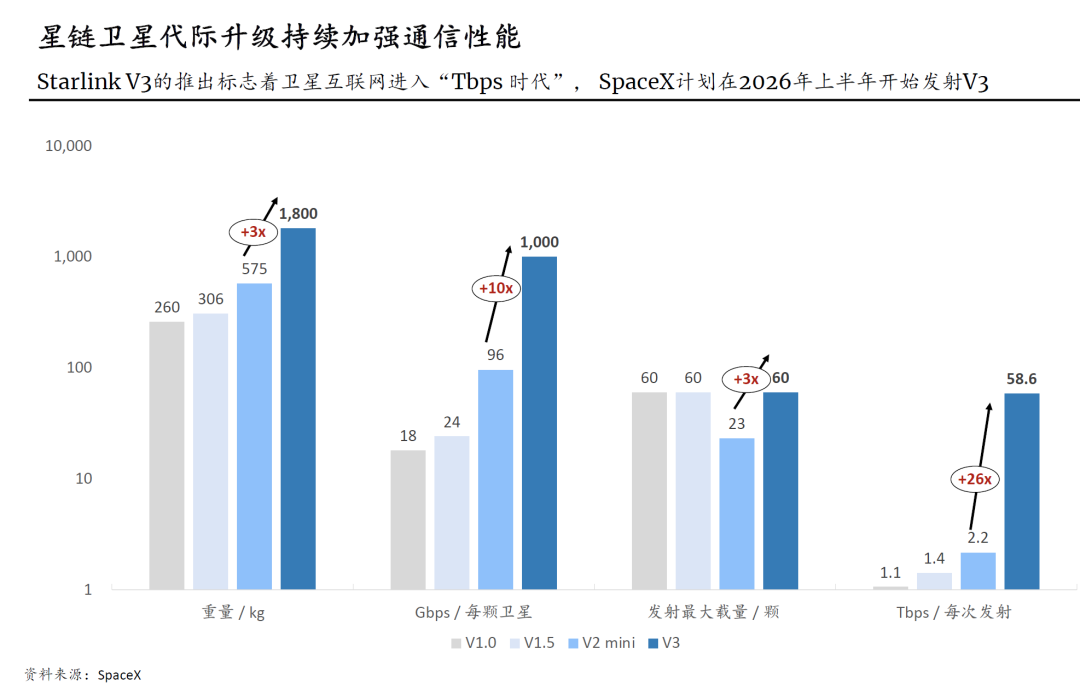

2) V3 Satellites: The Answer to Limited Bandwidth?

Each V3 satellite boasts a capacity of up to 1 Tbps. Deploying thousands of these satellites could result in a total constellation capacity of several thousand Tbps, representing tens of times the capacity of the current V2 Mini constellation.

However, Dolphin Research notes that while these solutions address some challenges of mobile network deployment, achieving full substitution remains difficult:

First, radio spectrum usage rights are strictly governed by national sovereignty principles. Starlink's 65 MHz spectrum was approved by the U.S. Federal Communications Commission (FCC), with legal effect limited to U.S. territory (including airspace and parts of its territorial waters).

SpaceX cannot use its FCC spectrum license to launch the same service in Japan, Germany, or Brazil—each country's spectrum requires independent approval or auction by its regulatory authority (e.g., Japan's MIC or Germany's BNetzA).

Furthermore, even with spectrum resources, terrestrial operators can reuse the same frequency in densely populated areas through dense base station deployment, whereas a single satellite's signal covers tens of thousands of square kilometers. All users in that region must share the same 65 MHz bandwidth, preventing spatial reuse.

This means that in densely populated areas, the 65 MHz bandwidth would be instantly divided among thousands of concurrent users, causing per-user actual speeds to plummet to unusable levels—far inferior to the dedicated 1-2 Gbps speeds offered by terrestrial 5G base stations. User experience would actually be better in remote areas.

This fundamentally complements terrestrial operators' services.

Second, mobile hardware support is an issue: No current mobile devices natively support 5G direct connectivity on the spectrum bands acquired by SpaceX. Hardware manufacturers would only modify devices if SpaceX had a sufficient user base.

Even with V3 satellites increasing bandwidth, speed limitations would shift back to the mobile device side: Regardless of satellite-side upgrades, the physical size and power constraints of mobile devices impose new ceilings, primarily because their weak signals struggle to traverse hundreds of kilometers of space for satellite capture. D2C is destined to offer "fast downloads but slow uploads."

From this analysis, it is clear that while Starlink may pursue a differentiated competition strategy initially, directly competing with mobile operators within three years remains challenging due to spectrum resource constraints.

However, beyond 3-5 years, operators' "spectrum bargaining power" may continue to diminish. Nevertheless, mobile communication services are inherently "data-sensitive," and fundamental technological differences persist. SpaceX still faces significant hurdles in achieving full substitution. After expanding beyond the United States, it will likely need to partner with local operators to mitigate regulatory risks.

III. What Advantages Does Starlink Have Over Other Communication Operators?

In its Starlink business, SpaceX has developed four primary revenue streams based on customer scenarios. Broadband services have become a stable business, while mobile services show promise for further growth.

When aggregated, these revenue streams form an exceptional economies-of-scale curve:

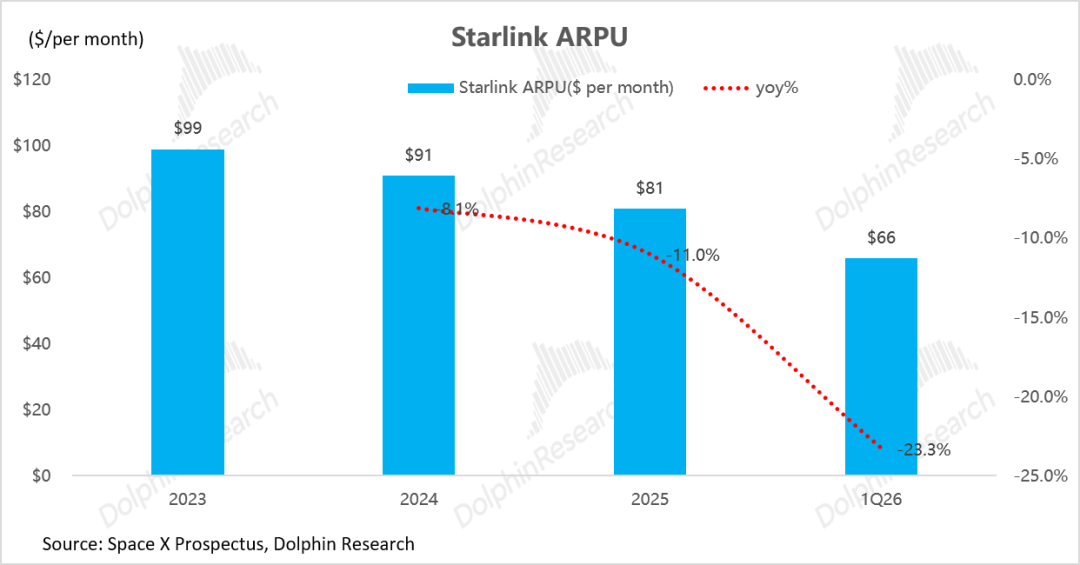

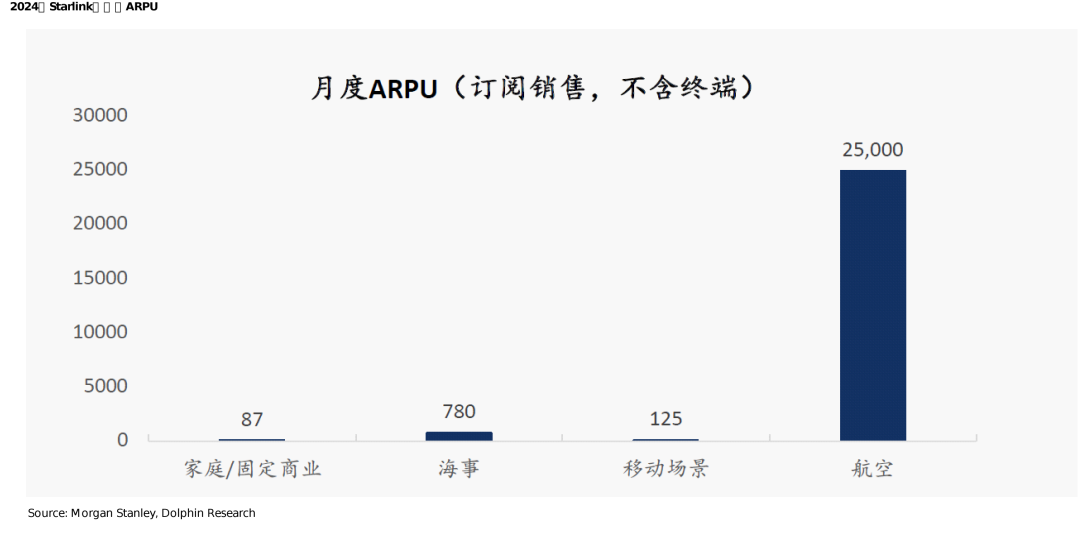

a. Declining Average Revenue Per User (ARPU) with Explosive Revenue Growth: SpaceX's ARPU decreased from $99/month in 2023 to $66/month in Q1 2026 (a 33% reduction), while revenue surged from approximately $3.9 billion in 2023 to $11.4 billion in 2025.

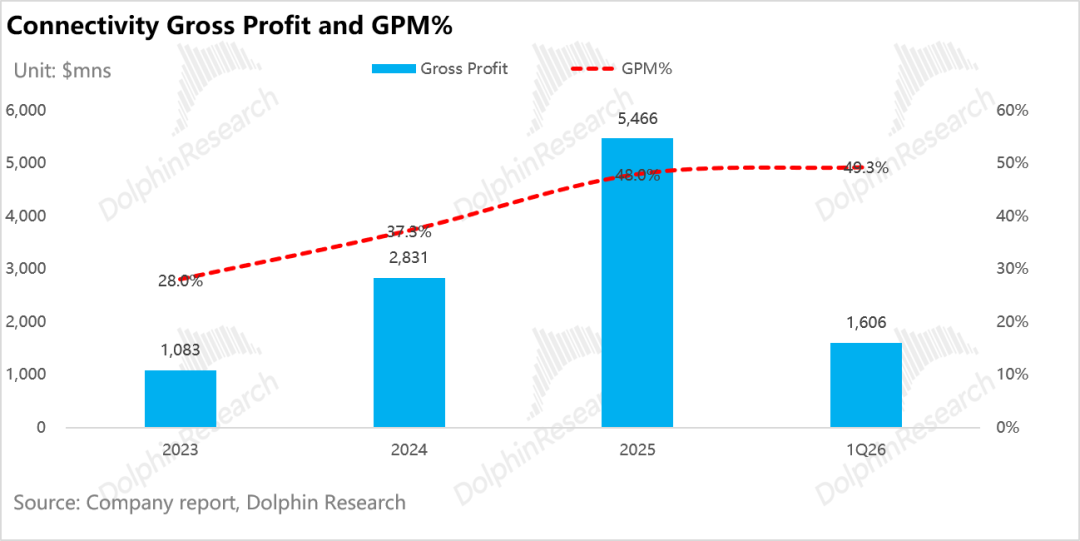

b. Rapid Profit Release: Gross margin improved from just 28% in 2023 to 48% in 2025, with a two-year CAGR exceeding 70%. Operating profit skyrocketed from $469 million to $4.423 billion, achieving nearly 10x growth (operating profit margin jumped from 12% to nearly 40%), while EBITDA margin surged from 41.4% in 2023 to 63% in 2025.

Declining unit prices and rising profits mark Starlink's transition from a "loss-leading network deployment" phase to a "low-cost rental" business model:

a. Extreme Operating Leverage:

Starlink's input structure features high upfront fixed costs and low operational expenses for revenue generation. Before network completion, rocket transportation, satellite manufacturing, and ground equipment production represent upfront costs.

However, once the constellation is deployed and commercialized, the marginal cost of adding a user becomes extremely low—network capacity is fixed, and new users simply allocate existing bandwidth resources with minimal incremental investment.

From 2023 to 2025, Starlink's user base grew from 2.3 million to 8.9 million (nearly 4x), while operating profit increased from $469 million to $4.423 billion (over 9x)—more than double the user growth rate, embodying extreme operating leverage.

b. "Hidden Subsidies" from Launch Cost Reductions: The Falcon 9's single-launch cost has plummeted from $60 million to below $15 million, reducing per-satellite launch costs for Starlink to just 1/4-1/5 of competitors' costs (Falcon 9's internal launch price is $15 million versus $62 million externally, essentially monopolizing capacity for internal use).

Starlink's network deployment launches are capitalized as satellite deployment costs and amortized over five years—meaning the business effectively occupies SpaceX's rocket capacity at low cost. This vertical integration creates internal synergies that competitors cannot replicate.

c. Drastic Reductions in Satellite Manufacturing Costs: Starlink satellites follow three cost-reduction principles, achieving exponential compression: Manufacturing costs per satellite have dropped from over $1-1.5 million early on to $600,000-$800,000 (with V3 expected to fall to $200,000).

Satellite depreciation is one of Starlink's largest cost components. SpaceX achieved rapid cost reductions through:

- Material substitution: Replacing aerospace-grade chips with automotive- or industrial-grade chips from companies like STMicroelectronics and Texas Instruments.

- Assembly-line production: The Redmond factory produces 70 satellites per week through automated processes, contrasting with traditional handcrafted satellite production. This vertical integration in the supply chain enables modular, automobile-chassis-like assembly lines, allowing mass production due to standardized satellite designs.

d. Terminal Hardware Cost Reductions: At $500, the terminal price is not cheap for users but covers costs for the company, no longer dragging down profits.

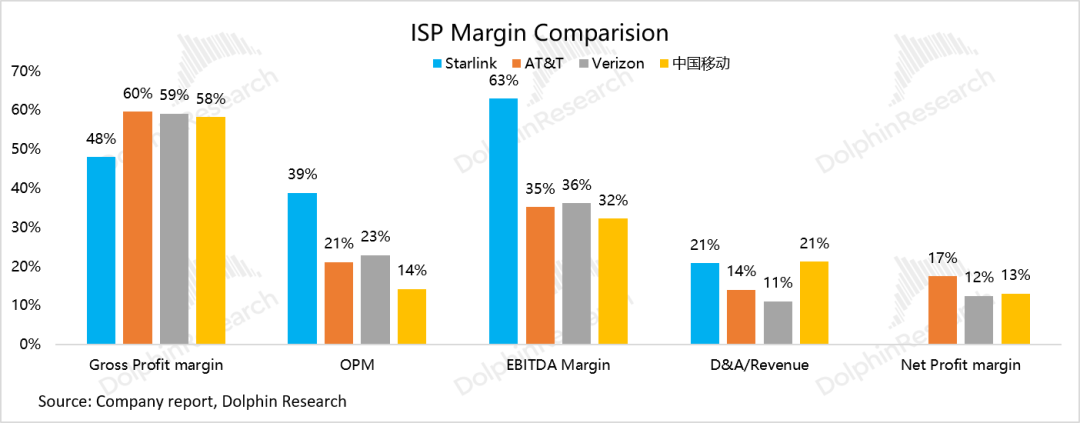

Notably, Starlink's economies of scale during profit release far exceed those of traditional telecom operators. Dolphin Research found that despite having only 1/10 the revenue of peers, Starlink's profitability—whether excluding or including depreciation and amortization—surpasses competitors.

Upon analysis, Dolphin Research identified:

a. Tiered Pricing: A Hard Currency in Low-Frequency Demand

Traditional operators offer flat pricing, with high enterprise dedicated line (dedicated line) prices justified by customized infrastructure costs. Starlink's tiered pricing maintains uniform maintenance costs across customer segments, making higher price tiers equivalent to higher profits.

b. Cost Structure: Zero Marginal Costs and Lower Maintenance

Low marginal costs: Traditional operators face last-mile constraints, with base station costs for remote users. Starlink operates in space with shared networks, so marginal costs remain unchanged whether new users are in deserts or oceans.

Low maintenance costs: Traditional base stations require substantial maintenance CAPEX. Traditional ISPs maintain large customer service centers and thousands of field workers driving engineering vehicles.

Starlink adopts an internet-based asset-light model, with clean satellite environments and minimal ground maintenance, keeping labor costs low.

c. Vertical Integration Advantages in the Supply Chain: This has been discussed repeatedly and will not be elaborated further here.

IV. Looking Ahead: What Are Starlink's Core Moats and Competitive Barriers?

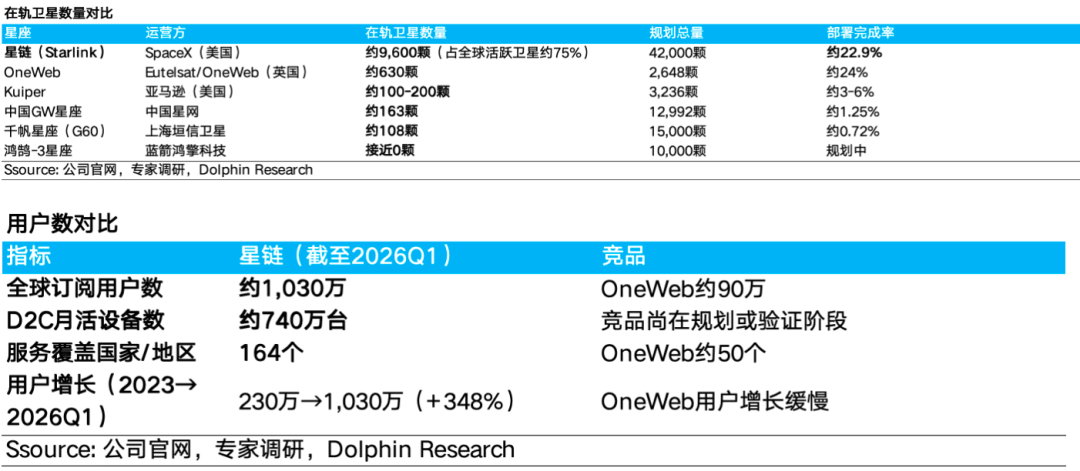

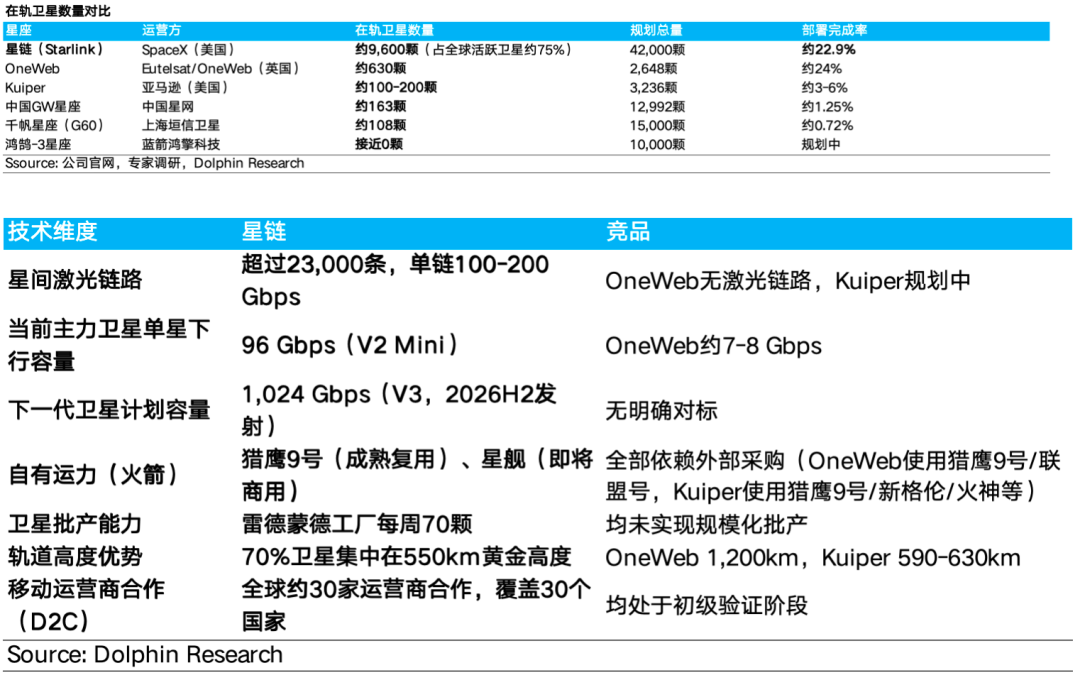

To date, Starlink has achieved a dominant lead in satellite count, subscriber numbers, revenue, and cost efficiency within the LEO sector. It holds over 80% market share, with its in-orbit satellites accounting for more than 70% of global low-Earth-orbit communication satellites.

Key competitors include:

OneWeb: ~630 in-orbit satellites, ~900,000 users, <10% market share. Relies on SpaceX's Falcon 9 and Soyuz-2 for launches, lacking autonomous capacity. Revenue ($200 million in 2025) is two orders of magnitude smaller than Starlink's ($11.4 billion).

Amazon Kuiper: Began first launches in 2025 with ~100-200 in-orbit satellites. Plans 3,236 satellites but depends on external launch providers and has not entered scaling (large-scale) commercialization.

China Satellite Network (GW Constellation) and Qianfan Constellation: Each has ~100+ in-orbit satellites focused on the Asia-Pacific region. The Honghu-3 constellation is still in early planning stages, lacking global networking capabilities.

In fact, at this point, the barriers to entry for Starlink are already clear:

a. Leveraging the capacity tilt of its monopolistic rocket launch business to achieve large-scale networking.

This is Starlink's most core and difficult-to-replicate competitive advantage. SpaceX possesses the world's only mature reusable rocket system, enabling Starlink to structurally outperform competitors in terms of networking costs.

The stark gap in per-satellite launch costs: The Falcon 9's single-launch cost is $15 million. Assuming approximately 24 V2 Mini satellites are launched each time, the launch cost per Starlink satellite is about $600,000-$700,000.

For competitors relying on externally procured launch services (e.g., OneWeb renting Falcon 9 or Soyuz rockets), the launch cost per satellite soars to $2-3 million or even higher. This means Starlink's launch costs are merely 1/4 to 1/5 of its competitors'.

b. First-mover advantage in orbital slots and spectrum: The 'land grab' for space resources.

Orbital positions and radio spectrum are scarce, non-renewable resources allocated on a 'first-come, first-served' basis by the International Telecommunication Union (ITU). Leveraging its first-mover advantage and strong deployment capabilities, Starlink has effectively claimed its territory in space.

Orbital layer positioning: Theoretically, the LEO orbit (100-2000 km) can safely accommodate a maximum of 60,000-100,000 satellites. Starlink has already secured multiple prime low-Earth orbit layers at 340 km, 550 km, and 1100-1325 km. Around 70% of its active satellites are concentrated at the optimal altitude of 550 km (low network latency, minimal cosmic radiation exposure, enabling the use of low-cost 'automotive-grade/consumer-grade chips').

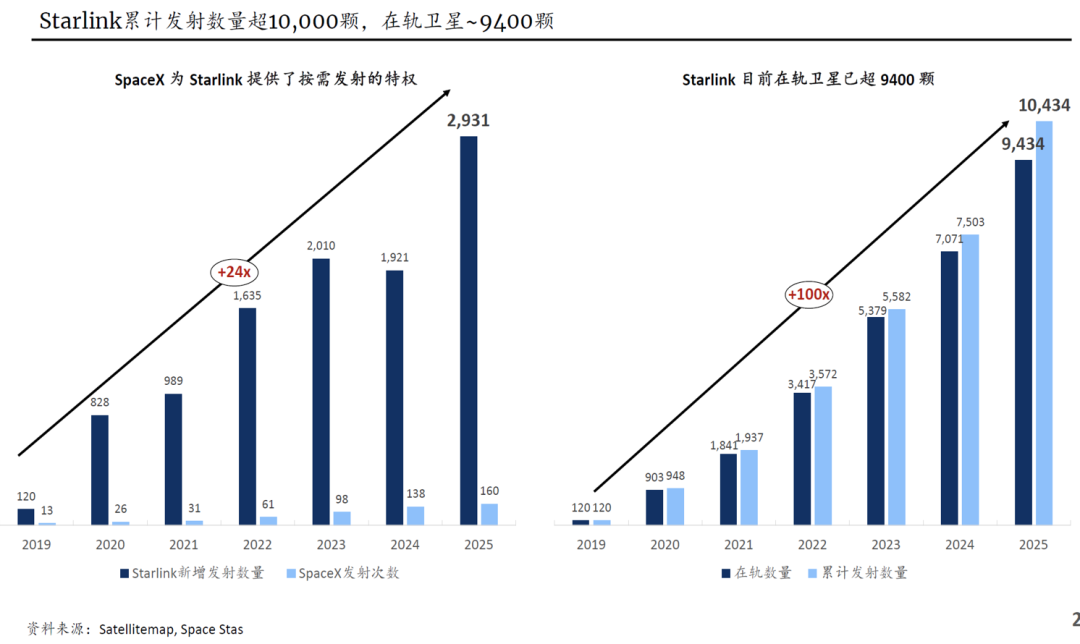

Once these orbital positions are occupied, subsequent satellites attempting to operate at the same altitude will face extremely high collision risks and coordination costs. The FCC has approved Starlink to deploy up to 42,000 satellites, and as of early 2026, Starlink has over 10,000 satellites in orbit, accounting for approximately two-thirds (about 65%-75%) of the world's active satellites.

Locking in core spectrum: Starlink has secured core communication high-frequency bands such as Ku, Ka, V, and E (enabling extremely high internet speeds and small antennas). These spectrum resources also follow the 'first-come, first-served' principle, and the communication frequency bands primarily used by low-Earth orbit satellites are nearing saturation.

Starlink has deployed over 23,000 inter-satellite laser links (with single-link rates reaching 100-200 Gbps), constructing a dynamic space mesh network that further solidifies its exclusive control over spectrum resources.

According to ITU rules, the first satellite must be launched within seven years of filing, with 10%/50%/100% of the declared satellites to be deployed within 2/5/7 years of the first launch. Failure to meet these conditions will result in a reduction of the declared satellite quantity.

Starlink is currently the only operator capable of completing such a large-scale deployment on schedule, creating a de facto permanent barrier in terms of orbital slots and spectrum resources.

c. Manufacturing cost reduction: Material substitution and vertical integration.

Both satellite manufacturing and terminal dish production are seeing cost reductions. The V3 satellites will eventually cost as low as $200,000 each, while terminal dishes have dropped to $500. Yet, product performance is improving: from 20 Gbps downlink per satellite in the V1.0 era to 96 Gbps for V2 Mini, with future V3 satellites reaching 1 Tbps per satellite (approximately a 10-fold increase in capacity compared to V2 Mini).

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibility or loss that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be construed or deemed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or intended to be distributed to citizens or residents of jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials conflicts with applicable laws or regulations or would require Dolphin Research and/or its subsidiaries or affiliated companies to comply with any registration or licensing requirements in such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek