Trancom Credit Technology’s 886 Million Yuan Acquisition of Weiyu Tiandao: Five Key Concerns in a ‘Self-Rescue’ Related M&A Deal | A Lightning Rod for Scrutiny

06/22 2026

06/22 2026

603

603

When a listed company, reporting a non-GAAP net profit loss of nearly 30 million yuan and suffering double-digit revenue declines for two consecutive years, abruptly announces a related M&A deal valued at nearly 900 million yuan—with the target’s intangible asset valuation appreciation rate exceeding 11,000%—the market is justified in asking: Is this a case of genuine strategic synergy or merely a facade for capital maneuvers?

01

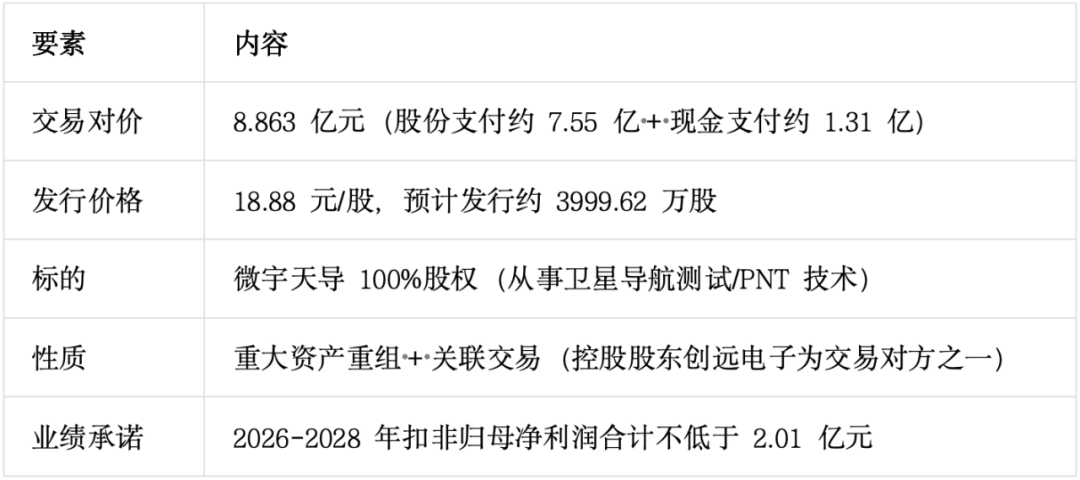

Acquisition Overview: 886 Million Yuan for Weiyu Tiandao

Trancom Credit Technology (920961.BJ) is embarking on its largest-ever capital operation, proposing to acquire 100% of Shanghai Weiyu Tiandao Technology Co., Ltd. for 886 million yuan through a combination of share issuance and cash payment, while raising up to 140 million yuan in matching funds.

The transaction structure is straightforward:

On the surface, this appears to be a strategic expansion by a wireless communication test instrument company into the ‘satellite internet + satellite navigation’ sector—a narrative that aligns with trending topics like 6G, low-orbit satellites, and the low-altitude economy. However, once the veneer of this story is removed and the financial data and transaction details are examined, questions begin to emerge layer by layer.

02

Doubt #1: Parent Company’s Core Business Struggling, Profitability Propped Up by Government Subsidies

To grasp the true nature of this acquisition, one must first understand the operational challenges faced by Trancom Credit Technology itself.

According to the company’s 2025 annual report:

Revenue stood at 204 million yuan, down 12.13% year-on-year—continuing the 13.93% decline seen in 2024, marking two consecutive years of double-digit shrinkage. Net profit attributable to shareholders was just 3.4816 million yuan, down 72.05% year-on-year. Non-GAAP net profit attributable to shareholders was -28.896 million yuan, indicating that the core business actually incurred a loss of nearly 30 million yuan.

How did the company report a ‘book profit’ of 3.48 million yuan? Government subsidies included in current profits amounted to 30.2301 million yuan, with an additional 5.93 million yuan in gains from the disposal of non-current assets.

In other words, Trancom Credit Technology’s 2025 net profit came not from product sales but from subsidies. After excluding subsidies and asset disposal gains, the core business was firmly in the red.

Even more concerning are the operational quality indicators:

Accounts receivable grew 24.6% from the start of the period, while revenue declined 12.13%—indicating that while income is shrinking, collections are slowing, downstream customer payment terms are lengthening, and bad debt provisions are increasing. Selling expenses rose 22.19% despite the revenue decline of 12.13%—a stark contradiction showing that spending is failing to drive sales, with sharply deteriorating marginal returns. Operating profit was negative for three consecutive quarters (-1.88 million, -7.25 million, -4.50 million). The asset-liability ratio climbed to 43.46%, with interest expenses accounting for 137.59% of net profit.

The company’s own annual report highlights risks related to reliance on imported key components while acknowledging that new strategic directions like connected vehicles and satellite internet ‘are still in the market development stage and have not yet contributed significant revenue.’

A listed company with non-GAAP losses, two consecutive years of revenue declines, and a core business nearly drained of cash flow is attempting to finance a nearly 900 million yuan acquisition—where will the funds come from? The answer: issuing new shares. Issuing nearly 40 million new shares equates to a dilution of approximately 21.88% for existing shareholders. Using dilution of original shareholders’ equity to acquire an asset from a related party—this fundamental setup warrants caution.

03

Doubt #2: Related-Party Transactions + ‘Insider’ Pricing: How Independent Is This Process?

While the acquisition follows a market-oriented process in form, its substantive related-party transaction nature cannot be ignored:

There are 14 transaction counterparties, including Shanghai Trancom Electronic Equipment Co., Ltd. (‘Trancom Electronic’), the controlling shareholder of Trancom Credit Technology. Founders Feng Yuejun and Ji Hongxia, a married couple, indirectly control 27.14% of the listed company through Trancom Electronic while also exercising control through the executive partner of another counterparty, ‘Shanghai Youqiduo.’

In other words, the listed company is using shares and cash diluted from minority shareholders to acquire assets within the controlling shareholder’s ecosystem—a setup inherently susceptible to institutionalized self-dealing.

Related-party transactions are not necessarily non-compliant, but when the target’s valuation appreciation is extreme and the listed company’s own performance is collapsing, the ‘related’ label becomes a magnifying glass. When the buyer is weak and the seller is family, the pricing negotiation balance naturally tilts.

The company followed regulations by having related directors and shareholders abstain from voting during deliberations, but abstention mechanisms only ensure procedural compliance—they cannot automatically dispel substantive concerns about pricing fairness, especially given the prevalence of cases where similar related M&A deals later exploded with goodwill impairment landmines.

04

Doubt #3: Weiyu Tiandao’s Valuation Enigma—11,256% Intangible Asset Appreciation: Why?

This is the most jarring alarm bell in the entire transaction.

On January 15, 2026, the Beijing Stock Exchange issued an audit inquiry letter to Trancom Credit Technology, directly targeting one of the core issues: Weiyu Tiandao’s intangible asset valuation appreciation rate reached 11,256.29%.

What does an 11,000-fold appreciation rate mean? It means the target’s book value of intangible assets is nearly negligible, yet assessors have assigned it an astronomical price—likely based on income approach valuations of customer relationships, technical know-how, and self-developed software/patents, which essentially represent discounted expectations of future cash flows and are highly assumption-dependent.

The Beijing Stock Exchange asked pointedly, requiring the company to explain the specific composition and reasonableness of the intangible assets.

Now, examine Weiyu Tiandao’s performance trajectory:

Net profit surged from 14.42 million yuan to 63.57 million yuan in three years—an impressive growth rate. But precisely this stark contrast—‘parent company’s core business collapsing vs. target’s rocket-like growth’—forms the basis of the Beijing Stock Exchange’s explicit doubts: Is this growth sustainable? Does it rely on a few major clients or short-term projects? Once growth slows, the PE multiple corresponding to the 886 million yuan valuation will rapidly shift from ‘reasonable’ to ‘expensive.’

The performance commitment guarantees a floor: non-GAAP net profit of no less than 60.27 million, 65.43 million, and 75.53 million yuan for 2026–2028, totaling 201 million yuan over three years. But note—the upper limit of the compensation mechanism is ‘the total share consideration received,’ meaning even if performance falls sharply, the seller’s maximum loss is merely returning a portion of the shares received, while the listed company’s goodwill impairment risk is borne by all existing shareholders.

05

Doubt #4: ‘Patched’ Performance Commitments and the Beijing Stock Exchange’s Deep Scrutiny

It is worth noting that this transaction did not sail through unchallenged. The Beijing Stock Exchange’s inquiry was no formality—the transaction plan underwent adjustments, including ‘patching’ performance commitments and requiring related-party transaction profits to be excluded from the commitment calculation scope.

This indicates regulatory vigilance toward the authenticity and sustainability of the target’s profits, as well as concerns about potential ‘inflation’ through internal transactions. Investors in the A-share market are no strangers to cases where targets’ revenues and profits are highly concentrated among a few related parties or specific projects, only to ‘revert to form’ once commitment periods end.

Furthermore, the transaction’s review was suspended by the Beijing Stock Exchange on April 30, 2026, due to expired financial documents before resuming after updates. The fact that two revised drafts (second revision, final draft) were required demonstrates that the plan was not finalized in one attempt but continuously patched under regulatory pressure.

06

Final Thoughts: M&A Is Not a Band-Aid for Core Business Wounds

Objectively, the satellite navigation testing/satellite internet sector where Weiyu Tiandao operates has industrial logic, and the two companies do have complementary technical directions. But good strategic logic ≠ good transaction terms ≠ good shareholder returns.

The fundamental issue facing Trancom Credit Technology is not a lack of an M&A target to ‘bulk up’ financial statements but the decline in its core business competitiveness, erosion of market share, and failure to convert high R&D investment into scalable commercial output. Against this backdrop, using a high-premium related M&A to merge the target’s profits may make simulated financial statements instantly ‘attractive’—net profit of 3.48 million yuan in 2025 before restructuring → surging to 66.76 million yuan after simulated merger, a ‘17-fold increase.’

But this ‘surge’ is essentially an accounting consolidation trick, not a genuine restoration of operational capability. If the target’s growth falls short of expectations, the massive 886 million yuan goodwill will become a Damocles’ sword hanging over existing shareholders.

From a regulatory perspective, investors should at least demand clear answers to three questions:

1. A detailed breakdown of Weiyu Tiandao’s 11,256% intangible asset appreciation rate and sensitivity analysis of its cash flow projections;

2. The parent company’s plan to stabilize its core business—M&A cannot become a smokescreen for core business weaknesses;

3. Whether the performance commitment compensation mechanism truly covers the maximum exposure to goodwill impairment risk, rather than merely ‘meeting formal standards.’

After all, capital market history repeatedly proves: Using share issuance to solve profitability problems may provide short-term cosmetic fixes but will only dilute value in the long run. True value creation lies not in consolidation accounting gymnastics but in selling products and collecting payments every day.

- END -

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek