Behind SpaceX’s IPO: Musk, With a Trillion-Dollar Net Worth, Still Faces a Cash Crunch

06/23 2026

06/23 2026

495

495

When news surfaced that SpaceX was preparing for a Nasdaq listing, the financial world took notice. Subscriptions soared past $250 billion, with demand exceeding availability by over fourfold. As of press time, SpaceX’s market valuation has surpassed $2.5 trillion.

Yet, beneath the hype lies a striking reality: Musk may not have taken SpaceX public because the company was “ready,” but rather because his sprawling business empire is facing a severe cash shortage.

01. The Cash-Draining Core of Musk’s Empire

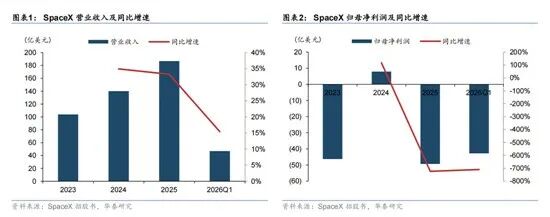

A closer look at SpaceX’s prospectus reveals a staggering truth: This company, valued at over $2 trillion, reported a net loss of nearly $5 billion in 2025.

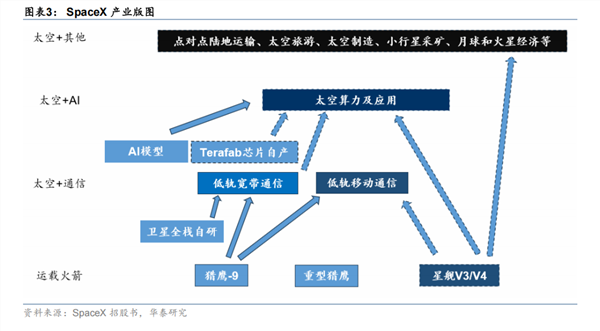

Only Starlink operates in the black—generating $11.4 billion in revenue and $4.4 billion in operating profit, single-handedly sustaining the company’s cash flow. While the rocket launch business, anchored by Falcon, has proven its viability, the massive R&D investment in Starship keeps it in the red. Meanwhile, the AI venture xAI, despite $3.2 billion in revenue, incurred losses of nearly $6.4 billion, nearly erasing Starlink’s entire profit.

Starship’s cash burn rate is particularly alarming. SpaceX has poured over $15 billion into this project, with roughly $3 billion spent in 2025 alone—double the previous year’s expenditure.

Beyond Starship, nearly every business under Musk’s umbrella is a cash drain. For instance, xAI opted for the most capital-intensive path: building its own computing infrastructure. The “Colossus 1” supercomputing cluster utilizes 230,000 GPUs, with hardware costs alone reaching astronomical levels. Neuralink, founded in 2016, has raised over $1.3 billion, achieving a $9 billion valuation after a $650 million Series E funding round in 2025. However, it remains in clinical trials, with each unit costing $40,000 and no clear path to mass adoption.

The situation resembles balancing a canoe on a tightrope: Starlink works frantically to fill the financial voids left by Starship and xAI, while Neuralink stands by, eagerly awaiting further funding.

02. Burning Cash Isn’t Recklessness—It’s the Only Defensible Moat

One might ask: Why not adopt a more cautious approach? Why not expand after achieving profitability? The answer lies at the heart of Musk’s business philosophy.

In every sector he enters, failing to burn cash equates to self-destruction. Rocket launches, low-Earth orbit satellite internet, general-purpose AI, and brain-computer interfaces all share a common trait: extremely high fixed costs, extremely low marginal costs, and a winner-takes-all dynamic. Whoever achieves technological breakthroughs and scales first can permanently shut out latecomers. A single misstep means eternal elimination.

Consider rocket launches first. Traditional giants like ULA charge hundreds of millions per launch. SpaceX’s Falcon 9 slashed prices to around $60 million, and now, reports suggest single-launch costs have dropped to $15 million—a 75% reduction—thanks to reusable technology honed over a decade, hundreds of tests, and countless explosions.

Starship aims to reduce payload costs per kilogram to below $200. Once achieved, all disposable rockets globally will struggle to compete. But before that, SpaceX must shoulder tens of billions in R&D and test flight costs. This is “buying barriers with blood”: If you dare burn through the cash first to perfect the technology, no one can engage in a price war with you later.

Starlink’s business model is even more straightforward. Low-Earth orbit satellite internet is a “constellation density race.” SpaceX has over 10,000 satellites in orbit, while rivals OneWeb and Amazon’s Kuiper lag far behind. Why so many? Because orbital and frequency resources are “first come, first served,” and only with sufficient density can ground terminals become compact and low-cost. Starlink now has over 10 million users, generating positive cash flow. But to maintain its lead, SpaceX must launch over 1,000 new satellites annually. Competitors face a choice: build their own launch capacity (costing tens of billions and a decade) or rely on third-party rockets (at double the cost). Starlink’s moat isn’t patents—it’s “I’ve spent $30 billion, and no rival dares follow.”

xAI’s cash-burning logic is identical. Training large models is an arms race in computing power. xAI’s decision to build its own supercomputing cluster and purchase 230,000 GPUs may seem redundant, but Musk’s calculation is clear: Long-term reliance on cloud computing would lead to runaway rental costs as usage grows. Self-built computing power is a capital expense—once built, marginal costs plummet. It’s like the difference between renting and buying a home: Renting means endless monthly payments, while buying requires a massive upfront cost but becomes cheaper over two decades. xAI bets that AI inference will become a public utility like electricity and water, and only those with self-owned computing power will have pricing power. Until then, whoever scales their model closest to general AI first will capture most of the market. There’s no room for second place.

Neuralink, though smaller, follows the same logic. Brain-computer interfaces require year-over-year, billion-dollar investments to build technical barriers. Once Neuralink achieves FDA long-term approval, latecomers will need 5–10 years to repeat the clinical process. This time gap is an invaluable moat.

Thus, Musk isn’t a reckless spender. He knows full well: Every dollar is soil for his moat. Today’s massive losses are tickets to future monopoly status.

03. SpaceX’s IPO: A Cash Infusion for the Empire, a Liquidity Play for Musk

But this strategy has a fatal flaw: It demands a relentless cash flow. Once funding dries up, not only will moat-building halt, but even existing defenses may crumble due to inadequate maintenance.

A closer look at SpaceX’s IPO details reveals a whiff of “forced listing.” All shares are newly issued, with proceeds flowing directly into company coffers—the most efficient “cash infusion” method SpaceX could find. While Starlink generates revenue, Starship and xAI’s colossal losses have wiped out its profits.

Meanwhile, for Musk personally, shares in a public company offer greater flexibility: He can pledge SpaceX stock for liquidity to support other ventures, avoiding forced Tesla stock sales as in the past.

04. Conclusion: It’s Not About Patience—It’s About Running Out of Time

Some may ask: Why not wait until Starlink is more profitable and xAI turns a profit before going public? The answer is brutal: There’s no time.

SpaceX now teeters on a precarious balance: Starlink works furiously to offset Starship and xAI’s massive losses. Goldman Sachs predicts xAI’s revenue will skyrocket from $3.2 billion in 2025 to $322 billion in 2030—but this hinges on xAI not falling behind OpenAI and Anthropic in the AI race. To stay competitive, xAI must continually buy advanced GPUs, expand computing power, and iterate large models, each step demanding billions in funding.

It’s like riding a unicycle on a tightrope—neither stopping nor speeding too fast. Stop, and rivals overtake you; speed too fast, and the chain might snap.

Investors’ enthusiasm for SpaceX’s IPO is essentially paying for a grand narrative of “space + AI.” But how much of this narrative will materialize depends on whether Musk has enough cash to finish the blueprint. And on this point, he knows his weakness better than anyone—precisely because he’s short on cash, he must go public; precisely because he’s short on cash, he must push SpaceX’s valuation to $1.77 trillion; precisely because he’s short on cash, this unprecedented “Planetary IPO” must proceed. The business model he holds is, in essence, a high-stakes gamble on the future: betting he can trade present cash for time others can’t buy, betting every moat he burns will be deep enough to despair rivals.

- End -

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek