Transsion Holdings Pursues A+H Listing, as the 'African Mobile Phone King' Gradually Loses Its Luster

06/24 2026

06/24 2026

521

521

Delving into Business Essence, Straight to the Heart of Enterprises

Author | Yang Cheng

Recently, Shenzhen Transsion Holdings Co., Ltd. (hereinafter referred to as 'Transsion Holdings', 688036.SH) has applied to the Hong Kong Stock Exchange for listing, aiming to establish a presence in both the 'A+H' markets.

Once hailed as the 'African Mobile Phone King', the company carved out its niche in emerging overseas markets. However, with smartphone giants like Xiaomi, Vivo, and OPPO intensifying their overseas expansion, Transsion Holdings can no longer sidestep direct competition.

According to the prospectus, in 2025, Africa remained the sole growth market for Transsion Holdings. That year, the company reported revenue of RMB 65.591 billion, a 4.5% year-on-year decline, with net profit plummeting by 53.5% to RMB 2.605 billion.

Confronted with challenges such as uneven growth across overseas regions, dwindling smartphone sales, and weakening profitability, Transsion Holdings is also entangled in patent disputes overseas, adding further uncertainty to its Hong Kong Stock Exchange listing journey.

01

Africa: The Sole Growth Market

Established in 2013, Transsion Holdings embarked on its African odyssey through 'niche competition'. Founder Zhu Zhaojiang, a former executive at Ningbo Bird, a trailblazer in China's mobile phone industry, witnessed the rise of feature phones in China.

While most mobile phone manufacturers vied for domestic market share, Zhu chose to bet on the then-nascent African market, charting a differentiated course for overseas expansion.

In 2019, Transsion Holdings went public on the Science and Technology Innovation Board of the Shanghai Stock Exchange. Nearly seven years later, on June 18, 2026, the company submitted its application to the Hong Kong Stock Exchange, seeking a dual 'A+H' listing.

However, Transsion Holdings' 'beyond Africa' expansion narrative is now facing fresh hurdles. While the African market, which once fueled the company's meteoric rise, continues to drive growth, expansion in other global regions has stalled.

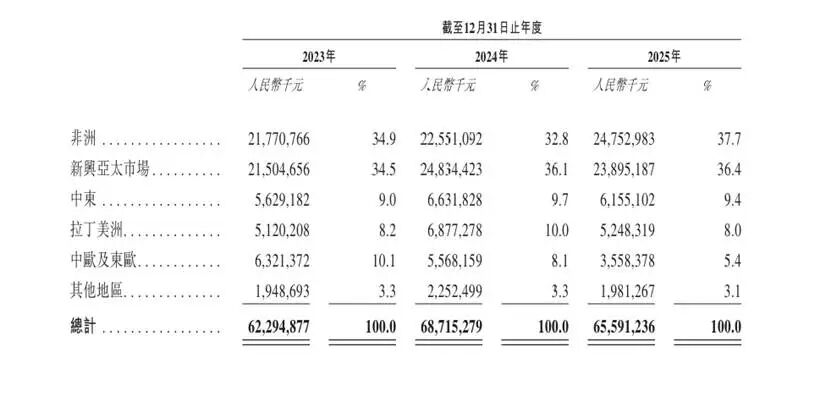

In 2025, Africa emerged as Transsion Holdings' only market to witness revenue growth, reaching RMB 24.753 billion and accounting for 37.7% of total revenue. The second-largest market, emerging Asia-Pacific, contributed 36.4% but saw a 3.6% year-on-year decline. Additionally, revenue in the Middle East, Latin America, and other regions also decreased to varying extents.

In terms of revenue composition, smartphone sales constituted the primary income stream for Transsion Holdings, accounting for 89.1% of revenue in 2025, followed by mobile internet services, IoT products, and other offerings.

Nevertheless, Transsion Holdings' smartphone sales have taken a significant hit. In 2025, the company sold 169 million smartphones, 32.404 million fewer than in 2024, marking a 16.1% year-on-year decline. The pressure on smartphone sales across regional markets ultimately weighed on Transsion Holdings' overall performance. In 2025, the company reported revenue of RMB 65.591 billion, a 4.5% year-on-year decrease, down approximately RMB 3.124 billion from RMB 68.715 billion in 2024.

More strikingly, the decline in net profit far outpaced the drop in revenue. In 2025, net profit tumbled to RMB 2.605 billion from RMB 5.597 billion in 2024, a decrease of RMB 2.992 billion, nearly halving.

Furthermore, given that a substantial portion of Transsion Holdings' revenue is derived from overseas markets, exchange rate fluctuations have emerged as an unavoidable operational risk. The prospectus highlights foreign exchange risk as one of the company's primary market risks.

Currently, the functional currencies of Transsion's numerous overseas subsidiaries encompass the US dollar, Indian rupee, UAE dirham, Ethiopian birr, and Bangladeshi taka. Currency fluctuations in diverse markets directly impact the company's financial results.

The repercussions of exchange rate movements are already evident in cash flow. In 2025, the 'effect of exchange rate changes on cash and cash equivalents' in Transsion Holdings' consolidated cash flow statement was -RMB 239 million, indicating that currency fluctuations in overseas markets have transitioned from mere financial statement risks to tangible cash flow impacts.

02

Escalating Costs and Compounded Risks

The pressure on Transsion Holdings' performance in 2025 may partly stem from intensifying competition in overseas markets. Once able to penetrate markets by 'avoiding giants and focusing on Africa', Transsion Holdings now faces direct competition from an increasing number of Chinese smartphone brands.

In the mid-to-low-end smartphone segment, manufacturers like Xiaomi, OPPO, and Vivo are increasingly targeting emerging markets. Meanwhile, the recent surge in memory prices has directly driven up smartphone manufacturing costs, eroding Transsion Holdings' profit margins.

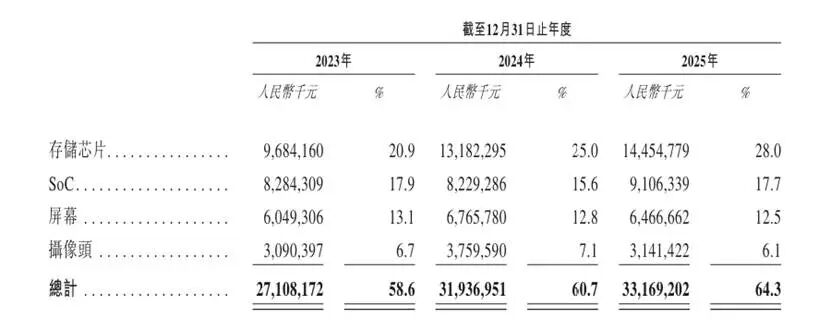

According to the prospectus, from 2023 to 2025, Transsion Holdings' procurement costs for memory chips were RMB 9.684 billion, RMB 13.182 billion, and RMB 14.455 billion, accounting for 20.9%, 25.0%, and 28.0% of raw material costs, respectively. Consequently, the company's gross profit margin declined, reaching 23.2%, 20.9%, and 18.7% over the same periods.

Overseas, Transsion Holdings is under sustained pressure from two patent/standard essential patent (SEP) holders. In November 2025, telecom equipment behemoth Ericsson publicly stated that it had initiated legal proceedings against Transsion in Brazil, India, Nigeria, and the Unified Patent Court (UPC), citing Transsion's prolonged refusal to accept its FRAND licensing terms. Subsequently, Ericsson extended its legal actions to Morocco, Indonesia, Colombia, Thailand, Vietnam, the Philippines, and South Africa.

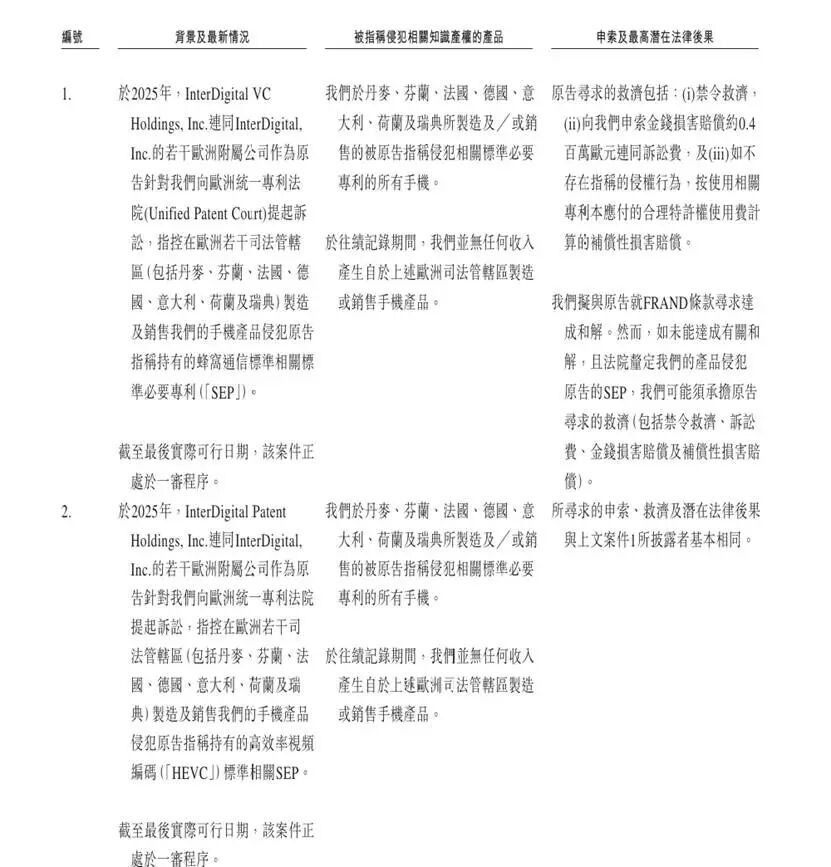

Transsion Holdings' prospectus confirms that Ericsson has filed multiple lawsuits or complaints in Europe, Thailand, and other regions. InterDigital has been even more aggressive.

According to the prospectus, InterDigital and its European subsidiary sued Transsion in the UPC in 2025, alleging infringement of SEPs related to cellular communication standards and HEVC video coding in its smartphone products across European jurisdictions, including Denmark, Finland, France, Germany, Italy, the Netherlands, and Sweden.

On April 1, 2026, InterDigital announced that a court in Rio de Janeiro, Brazil, had issued a preliminary injunction, granting it the right to a temporary injunction and restricting Transsion Holdings from selling 5G-compliant devices in Brazil.

It is noteworthy that patent litigation in the smartphone industry is not merely a typical dispute but a 'hard risk' that can directly impact sales, distribution channels, and profit margins. Transsion Holdings also acknowledged in its prospectus that if a court finds infringement, it may face injunctions, legal fees, monetary damages, and compensatory penalties.

As Transsion Holdings advances toward its Hong Kong Stock Exchange listing, these overseas operational risks will become a focal point for regulators and investors. With intensifying competition, fluctuating supply chain costs, and emerging patent barriers, Transsion must demonstrate to the market not just its past 'African miracle' but its resilience and adaptability amid global challenges.

END

The images in this article are sourced from the internet.

-

![]()

Proposed to Raise 955 Million Yuan through Private Placement! Huicheng Vacuum Boosts Localization of Ultra-Precision Optical Coating Equipment

-

![]()

Cash Flow Soars 13-Fold! What Major Strategic Move is Wuhan Five Square Optoelectronics Planning?

-

![]()

Leaked Design of vivo X500: Reverts to Circular Camera Module in Top-Left Corner, Pays Homage to Classic X90 Aesthetic

-

![]()

DeepSeek Shows Signs of Foraying into Code Agents, Launches WeChat Official Account Focused on Harness

-

![]()

Auto Companies Deny Claims That ‘Cooperation with Huawei Is Non-Essential’, as Huawei Transforms into a ‘Public Platform’

-

![]()

Starship to Independently 'Return to the Launch Tower': SpaceX's Ambitions Extend Beyond Rocket Building to Dominating Space Transportation

-

![]()

Starship Set to Independently 'Return to the Launch Tower': SpaceX is Revolutionizing Space Transportation, Not Just Building Rockets

-

![]()

Anthropic and OpenAI Face Off Against Deepseek