Expected to Rake in a Staggering 24.4 Billion in the First Half of the Year: What Gives Foxconn Industrial Internet the Competitive Edge?

07/16 2026

07/16 2026

367

367

Author|Ren Tianqin

Editor|Chen Xiaoran

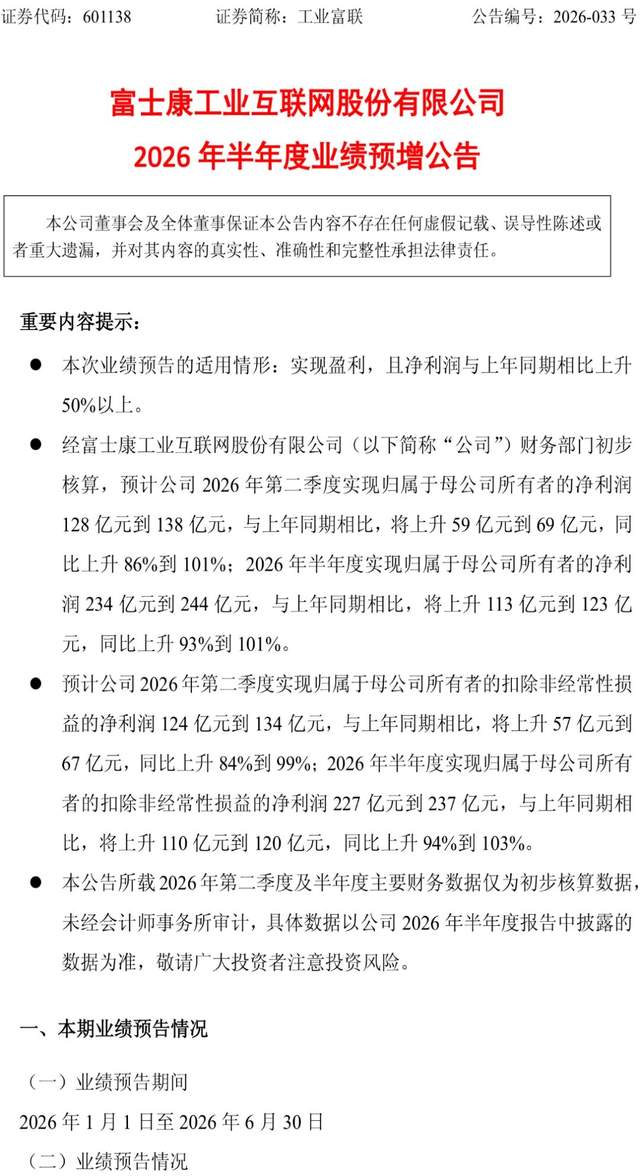

On the evening of July 9, Foxconn Industrial Internet (601138.SH) unveiled its semi-annual performance forecast, indicating another significant surge in net profit, building on an already high base.

Behind these impressive financial figures, the real surge and potential long-term risks within the AI supply chain warrant a closer examination. As the global computing infrastructure wave continues to rise, the success of 'shovel sellers' (those providing essential tools and services) ultimately depends on whether 'gold miners' (end-users investing in AI technology) continue to spend.

Image source: Foxconn Industrial Internet announcement

As of the close on July 9 (Beijing Time), Foxconn Industrial Internet's stock price closed at RMB 69.53, marking a 5.33% increase for the day. Its total market capitalization stood at approximately RMB 1.38 trillion, with a daily trading volume of RMB 11.77 billion.

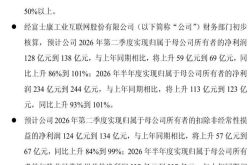

That evening, Foxconn Industrial Internet released its semi-annual performance forecast for 2026, projecting a net profit attributable to shareholders ranging from RMB 23.4 billion to RMB 24.4 billion for the first half of the year. This represents a year-on-year increase of 93% to 101%. Non-recurring net profit also reached RMB 22.7 billion to RMB 23.7 billion, up 94% to 103% year-on-year. This marks the first time that semi-annual net profit has surpassed RMB 20 billion, setting a new historical high.

Breaking down the quarterly performance, the continuity of growth becomes even more evident.

In the second quarter of 2026, Foxconn Industrial Internet's net profit attributable to shareholders for the quarter is expected to reach RMB 12.8 billion to RMB 13.8 billion, showing a year-on-year increase of 86% to 101% and a sequential increase of 20% to 30% from the first quarter.

Combined with the first-quarter report data for 2026, Foxconn Industrial Internet's revenue reached RMB 251.078 billion, up 56.52% year-on-year. Meanwhile, net profit attributable to shareholders surged by 102.55% year-on-year to RMB 10.595 billion.

Net profit growth significantly outpaced revenue growth, primarily driven by an increased revenue share from high-value-added AI products. Foxconn Industrial Internet has achieved quarterly net profit exceeding RMB 10 billion for three consecutive quarters.

The drivers of this performance are clear, with two main lines firmly anchored in the AI infrastructure sector.

In the cloud computing segment, AI server revenue from cloud service providers soared by over 230% year-on-year in the first half, becoming the absolute performance engine. In the telecommunications equipment segment, shipments of 800G and above high-end data center switches grew 1.4 times year-on-year, meeting the high-speed interconnection needs of computing clusters.

Additionally, Foxconn Industrial Internet plans to commence mass production of new-generation AI hardware jointly developed with leading clients in the second half of the year.

The continuous expansion of the high-end product matrix is already reflected in profitability. In the first quarter of 2026, the company's gross margin improved by 0.62 percentage points year-on-year to 7.35%, with the high-end AI server business driving overall profitability upward.

Industry Dividends Continue

Foxconn Industrial Internet's performance surge is not just an individual company's gain but a microcosm of the global AI computing infrastructure arms race.

From a global supply chain perspective, Foxconn Industrial Internet is already the undisputed leader in the global AI server ODM field. Goldman Sachs research defines it as the 'largest ODM supplier in the AI server rack sector,' projecting its global market share to rise from 55% in 2026 to 69% by 2028.

This position is supported by deep coverage of global core clients. Foxconn Industrial Internet is deeply tied to NVIDIA, Microsoft, AWS, Google, Meta, and other global tech giants, with core orders secured through the fourth quarter of 2026.

The stability of client relationships stems from extremely high industry entry barriers. Supplier certification cycles for leading cloud vendors last 18 to 24 months, with designated partnership periods typically spanning 3 to 5 years, creating formidable barriers to entry.

In terms of product matrix layout, Foxconn Industrial Internet has extended its reach across the entire chain, from servers to supporting infrastructure. Beyond its mainstay AI servers, 800G high-speed switches continue to scale up, with CPO all-optical switch prototypes shipped in bulk. Simultaneously, the company is ramping up liquid cooling technology research to meet next-generation high-density computing cabinet cooling demands.

Industry demand-side data further confirms that the boom cycle is far from over.

According to iiMedia Research, global AI server shipments surged from 500,000 units in 2024 to 720,000 units in 2025, with projections exceeding 1 million units in 2026.

Capital expenditures are expanding in tandem. The combined capital expenditure ceiling for Microsoft, Google, Amazon, and Meta in North America reached USD 725 billion in 2026, up 77% from 2025.

Institutional analysts offer optimistic guidance. Wind data shows that 21 brokerages issued research reports in the past six months, forecasting Foxconn Industrial Internet's full-year 2026 net profit to average RMB 61.242 billion, up 73.56% year-on-year.

Growth Has Limits

However, amid the market's collective pursuit of AI computing dividends, four hidden risks cannot be ignored.

Client Concentration Risk: Foxconn Industrial Internet is deeply tied to global tech giants like NVIDIA, Microsoft, and Meta, with over 60% of sales from its top five clients. A capital expenditure cut by any single cloud vendor would directly impact revenue. Northbound capital already reduced its stake by 12.36% in the first quarter, intensifying bull-bear battles.

Profit Ceiling Constraints: In the first quarter, the company's overall gross margin was just 7.35%. With upstream GPU and HBM chips monopolized by NVIDIA and others, and downstream cloud vendors wielding strong bargaining power, the midstream contract manufacturing segment faces persistent profit margin pressures. As more players enter the sector, further gross margin improvements appear limited.

Industry Cycle Downturn Pressure: Mainstream analysts predict that capital expenditure growth among the five global cloud giants will plummet from nearly 100% in 2026 to 22% in 2027. Once computing hardware procurement slows, new order demand will quickly cool.

Inventory pressures also loom. Whether large-scale inventory accumulation reflects normal order fulfillment or signals structural demand shifts remains debated in the market.

Additionally, Taiwanese peers like Quanta and Wistron are gaining momentum, while domestic players like Inspur Information and Super Micro Computer are accelerating their breakthroughs. With over 60% of revenue from overseas, Foxconn Industrial Internet faces ongoing disruptions to supply chain layouts and order fulfillment from global export controls and trade policy shifts.

Overall, Foxconn Industrial Internet's performance forecast fully delivers on the short-term dividends of the AI computing supply chain, with its leading position intact. As of July 9, its static price-to-earnings ratio stands at approximately 33.9 times, with valuation premiums fully pricing in growth expectations.

While the business of 'shovel sellers' in the AI gold rush remains booming, any weakening in 'gold miners'' willingness to invest will inevitably dent shovel sales.

-

![]()

Liu Qiangdong Gains Crucial Foothold as Tencent Forms Alliance to Counter ByteDance's Dominance

-

![]()

Physical AI Infrastructure Race: U.S. Firm General Intuition Trains Robots Using Game Footage, Reaches $2.3 Billion Valuation

-

![]()

DeepSeek May Launch IPO as Early as This Year Amid 'Insatiable Demand for Computing Power'

-

![]()

Huawei and Tesla Pioneer the Path! Modular Design Takes Center Stage, Electric Vehicles Bid Adieu to 'Instant Obsolescence'

-

![]()

Expected to Rake in a Staggering 24.4 Billion in the First Half of the Year: What Gives Foxconn Industrial Internet the Competitive Edge?

-

![]()

Tencent Invests 13.6 Billion to Become a 'Minority Shareholder': What Are Its Ambitions with Manus?

-

![]()

Computing Power Extends to Space: Aerospace AI Sparks a New Industrial Era

-

AI's Richest Person Revealed: A Native of Zhanjiang!