Electric Vehicle Insurance Premiums Skyrocket Again, Unannounced

08/14 2025

08/14 2025

576

576

Amidst losses on multiple fronts, new energy vehicles (NEVs) are facing a protracted growth crisis.

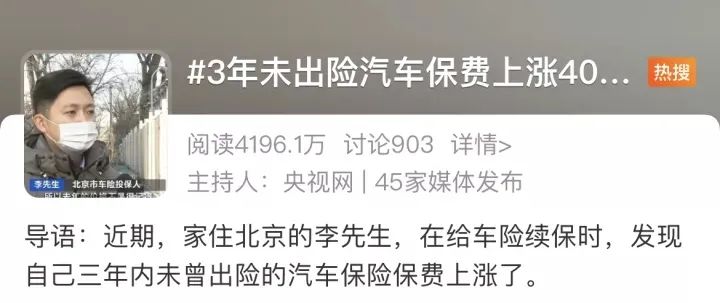

"The savings don't offset the surge in insurance premiums."

A NEV owner lamented in a group chat, sparking a wave of discussions among group members. During this session, everyone realized that NEVs are encountering "insurance assassins".

According to statistical data, the average insurance premium for NEVs in 2024 was 21% higher than that for fuel vehicles. Many vehicle owners have found that their premiums inexplicably increased upon renewal, with hikes exceeding 20%, and some even reaching 40%.

This is just a general trend. Group member Xiao Wang shared that he is in an even more dire situation, currently unable to purchase insurance. Xiao Wang bought an NEV last year due to his long commute, thinking he could save substantially over the year. However, this year he received a notification from the insurance company denying his renewal due to high mileage and suspected ride-hailing use.

Xiao Wang admitted that he only bought the car because it was a popular model from a reputable brand, not considering other factors. Consequently, he was adversely affected because the same model is also widely used for ride-hailing services in the city.

Insurance companies are also complaining. According to Shenwan Hongyuan statistics, from 2023 to 2024, the NEV insurance industry accumulated losses exceeding 12.4 billion yuan, with the comprehensive cost ratio for small and medium-sized enterprises surpassing 110%.

Especially as the number of NEVs increases, the compensation amount also keeps rising. In the first half of this year, the settled compensation for NEV commercial vehicle insurance surged by 33.32% year-on-year, outpacing the entire vehicle insurance industry.

Ultimately, the crux of the problem lies in NEV maintenance.

High Maintenance Costs

Behind the insurance premium hike is the claims management model established by insurance companies during the fuel vehicle era, with a comprehensive actuarial basis for the claims ratio centered on the vehicle model.

However, the rapid proliferation of NEVs has significantly skewed the traditional vehicle insurance model. On one hand, the claims ratio is continuously escalating. According to statistics, among the 2,795 vehicle series underwritten in 2024, 137 had a loss ratio exceeding 100%, with most being NEV series.

Because NEVs typically outperform fuel vehicles within the same price range in terms of performance, the enhanced power results in a higher overall accident rate compared to fuel vehicles.

And unlike fuel vehicles, NEVs involve battery packs, the entire vehicle's electronic architecture, sensors, and hardware and software related to autonomous driving, making repairs through third-party service providers challenging. Repairs can only be carried out at the brand's designated maintenance outlets.

This leads to overall high maintenance costs, with power battery repairs being a significant pain point for NEV maintenance. Due to their high integration and professional requirements, once the battery pack malfunctions, 4S stores often recommend replacing the entire battery pack, which can cost tens of thousands or even hundreds of thousands of yuan.

For users, whether it's insurance compensation or self-funded repairs, they need to bear significant economic losses and sometimes face the dilemma of repair costs exceeding the vehicle's residual value.

Although the repair cost of battery packs is high, it is not the direct factor causing the surge in maintenance costs. According to statistics, battery pack repairs account for only 1% of the total maintenance ratio.

Due to the much higher frequency of model updates for NEVs compared to fuel vehicles, it is difficult to procure parts from third parties, limiting options to original equipment manufacturer (OEM) repairs. Moreover, due to the low production volume, the price of parts is much higher than the vehicle purchase cost.

In the fuel vehicle era, the ratio of parts to the whole vehicle was controlled at 200% for most models, with some luxury models at 300%. However, for many NEV models, this ratio exceeds 300% and even reaches 400%.

In particular, due to the increased weight brought by battery packs, automakers can only control the vehicle weight by using aluminum and lightweight composite materials, but this also causes maintenance difficulties. Most parts can only be replaced instead of repaired, increasing maintenance costs.

For example, when replacing the front bumper, NEVs need to replace the entire bumper because it integrates multiple radars and sensing components, increasing the cost from a few hundred yuan for fuel vehicles to several thousand yuan. If other functions such as light-emitting screens are also integrated, the repair cost can even reach tens of thousands of yuan.

Without the drive of economies of scale, NEVs need to face the dual challenges of a high accident rate and high maintenance costs in the short term, especially with the increasing integration of NEVs and the increase in maintenance costs brought by new technologies. At this stage, vehicle owners can only make cautious choices.

Jointly Building an Ecosystem

It seems that the surge in NEV insurance premiums has become an intractable issue in the short term.

However, the industry has been exploring new models to address the continuous rise in NEV insurance premiums.

For example, Tesla has launched an FSD-based insurance business overseas, collecting real-time driving behavior data (such as hard braking, sharp turns, following distance, etc.) from in-vehicle sensors to generate a safety score ranging from 0 to 100. The higher the score, the lower the insurance premium.

It also shifts from the traditional model of measuring insurance costs based on the user's age, gender, and credit score, instead dynamically adjusting them based on actual vehicle usage (such as mileage and driving time).

This has yielded positive results. For example, Tesla's insurance business loss ratio dropped from 116.6% in 2022 to 103.3% in 2024, marking an exploratory reform for NEV insurance.

In China, BYD also began piloting vehicle insurance business in 2024, allowing online insurance applications for non-commercial private cars with 9 seats or less of its brand in 7 provinces.

Insurance company staff noted that this is a good starting point because automakers have a clearer understanding of NEV owners' daily usage compared to insurance companies. Whether it's driving habits or statistics on vulnerable parts, data acquisition is easier, which is more conducive to forming a reliable premium calculation model.

However, with only BYD, it is still challenging to improve the current situation of rising NEV insurance premiums. On one hand, even with data support, the high maintenance costs still make it difficult to address the loss ratio issue. For example, it took Tesla three years, but its loss ratio is still over 100%, far exceeding the industry average of 66.1%. Including BYD Property Insurance, it was still in a loss state in 2024.

On the other hand, in the domestic market, long-term losses have concentrated vehicle insurance in leading enterprises. According to statistics, in 2024, PICC, Ping An, and China Pacific Insurance underwrote a total of 24.2 million NEVs, accounting for 77% of the NEV parc, 8 percentage points higher than that of fuel vehicles, forming a monopoly.

It is difficult for just one or two automakers to significantly impact the existing insurance pricing system. More collaboration is needed between insurance companies and automakers to optimize insurance models, form premium calculations tailored to each vehicle owner, and prevent the insurance premiums for an entire vehicle model from rising due to the behavior of individual vehicle owners.

Of course, the core of the premium increase is still maintenance costs. In response to NEVs' unique characteristics, parts suppliers have also begun to participate in the automotive aftermarket services.

For example, as the world's largest supplier of power batteries, CATL has been offering after-sales services for battery packs since 2024, with the core goal of addressing the market pain point of only replacing rather than repairing power batteries. Relying on its technical accumulation in power batteries, Ningjia Service can perform low-cost repairs of CTB battery packs, reducing battery maintenance costs.

In addition, CATL has developed non-destructive testing technology for power batteries, which can complete fault detection in just 15 minutes, achieving efficient battery pack diagnosis and avoiding over-maintenance.

Most importantly, Ningjia Service is also open to NEV owners whose insurance has expired. As long as the NEV model uses a CATL battery, battery inspection and maintenance can be performed, solving the pain points of expensive OEM repairs and unprofessional third-party repairs.

Currently, CATL has established over 800 service stations nationwide. On August 10th of this year, it opened a Shanghai direct experience center and the first overseas direct experience center and will continue to expand and standardize the aftermarket service system for NEVs.

With the participation of automakers and parts suppliers, the long-standing issue of expensive NEV maintenance can be somewhat contained. In the long run, it is still necessary to reduce the loss ratio to achieve the healthy development of the insurance industry.

Currently, while insurance companies' method of increasing premiums is direct, it overly pursues short-term interests, which is not conducive to the healthy development of the NEV industry and may dampen potential users' desire to purchase vehicles.

The black box pricing model cannot dominate the market in the long term. It is necessary to strengthen cooperation with automakers to form a transparent pricing system rather than inexplicable price hikes.

At the same time, the rise in insurance premiums also forces automakers to shift from "competition based solely on parameters" to "competition based on the full life cycle experience", ensuring long-term user experience rather than pursuing short-term scale and profitability.

Only when insurance companies, automakers, and parts manufacturers jointly promote repairability, standardization, and data transparency of maintenance can the price of automobile insurance return to a reasonable range.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for removal.

-END-

-

![]()

Weighing the Pros and Cons of In-House Chip Development: Most Automakers Shouldn't Feel Compelled to Pursue It

-

![]()

Can the Leapmotor D99 Gracefully Ascend into the Premium MPV Market as the Brand Climbs Higher?

-

Midea Bets 1 Billion Yuan on Liquid Cooling, Targeting AI Computing Power Market with 2027 Production Launch

-

Amidst Declining Profit Margins, Can Anwen Technology Sustain Its Edge in Automotive Cockpits?

-

![]()

5,000 Companion Robots Sold: Can UBTECH Breathe a Sigh of Relief?

-

![]()

NIO Maintains Brand Premium: Onvo Sets Minimum Price at 150,000 Yuan, Avoids Direct Competition with Leapmotor and BYD | MJ Pro

-

![]()

“From a 5-minute escape window to a zero-fire baseline, I finally feel confident driving an electric vehicle”

-

![]()

Profits Skyrocket! From Leasing to Construction: A Storage Enterprise with Hundred-Billion-Yuan Revenue Plans 1.175 Billion Yuan Investment in New Headquarters