Reversing the Decline: Japanese Automakers Reinforce Their China Presence

08/21 2025

08/21 2025

580

580

From mere slogans to tangible actions, Toyota, Honda, and Nissan have once again widened the gap in their strategies.

In recent years, internal competition in China's automotive market has emerged as a prominent topic. On one hand, independent brands have achieved significant breakthroughs in market share through electrification and intelligent technologies, increasing from 50% to nearly 70%. On the other hand, rapid market changes have posed significant challenges for traditional joint venture automakers. The transition from premium pricing to price cuts to survive underscores the brutal nature of the market, especially for Japanese brands that once dominated but are now gradually losing ground amidst the new energy wave.

At the beginning of 2025, Japanese brands' market share in the domestic market fell to 9.2%, dropping below 10% for the first time. This triggered a strong desire for survival among Japanese joint ventures.

On February 25th, Toyota announced the establishment of Lexus (Shanghai) New Energy Co., Ltd. in Shanghai, becoming the second wholly foreign-owned automotive company after Tesla.

Subsequently, Honda, Nissan, and even Mazda embarked on a new round of launching new energy models, demonstrating their determination to succeed or perish.

Half a year later, an examination of Japanese automakers' performances reveals that the trio, which once advanced and retreated together, have now diverged significantly.

Crossing the Rubicon

July data indicates that only brands that actively face market competition have a chance to survive.

First, Toyota. Amid the overall decline in Japanese sales, Toyota China achieved sales of 126,000 vehicles, a year-on-year increase of 6.8%, making it one of the few joint venture automakers to achieve positive growth.

In the crucial fuel vehicle market, Toyota still firmly holds a dominant position. Especially with the continuation of its "one-price" policy, Toyota remains a significant player in the fuel vehicle market. The RAV4 sold 18,400 units, the Corolla Cross sold 14,900 units, and the Fenglanda sold 13,600 units in a single month.

Moreover, Toyota's efforts in new energy vehicles have showcased the courage of the world's largest automotive group in the domestic market. In addition to the still-under-construction Lexus, both FAW Toyota and GAC Toyota have introduced powerful new energy products to compete in the market.

Among them, the pure electric SUV BZ3 launched by GAC Toyota in the first half of the year achieved a breakthrough for Toyota's new energy vehicles, selling 6,833 units in July. While this is still modest compared to domestic new forces, it is quite competitive among many joint venture brands.

Of course, the success of BZ3 cannot be separated from its pricing strategy. The entry-level version is priced at only 109,800 yuan, making it more affordable than Toyota's fuel vehicles of the same level. The high-end intelligent driving version, equipped with lidar and Orin-X chips, is priced at only 159,800 yuan, giving it a pricing edge over independent brands.

With an absolute price advantage, Toyota has achieved dual success in both fuel vehicles and new energy models in the domestic market, with sales rebounding. This proves that there are no unsellable cars, only uncompetitive prices.

Nissan, following Toyota's footsteps, achieved sales recovery for the first time. In July, Nissan sold a total of 58,200 new vehicles, a year-on-year increase of 21.8%. Dongfeng Nissan contributed the majority of sales, breaking the curse of long-term decline with 53,500 units and a growth rate of 19.4%.

Dongfeng Nissan's sales are primarily driven by fuel vehicles. As expected, Sylphy once again won the sales championship among joint venture sedans, with a monthly sales volume of 26,300 units, still maintaining some of its former glory.

However, such glory is dwindling. When the terminal transaction price of the entry-level model starts with a '6', sales volumes only serve as a reminder of past glories.

Nevertheless, Nissan has demonstrated its determination to stay in the Chinese market with greater courage, especially amidst the parent company's operational difficulties. Dongfeng Nissan launched a counterattack with the N7 priced at 119,900 yuan.

This pricing has shown the market a different Dongfeng Nissan. Even Toyota dares not set such an aggressive price like Nissan.

From its launch before the Shanghai Auto Show to the present, Nissan N7 has sold over 10,000 units. Behind this sales surge is the proof that joint venture new energy vehicles can also succeed in the Chinese market. Electrification and intelligence are not insurmountable technological barriers.

In contrast, Honda seems to have become the most disappointing Japanese brand, with sales of only 40,300 units in July, a year-on-year decline of 14.6%. Among them, GAC Honda experienced a year-on-year decline of over 50%, making it the worst-performing joint venture brand in July.

First, Honda has completely lost ground in the fuel vehicle market. Against the backdrop of declining fuel vehicle prices, Honda has struggled to maintain its basic fuel vehicle market. Both the CR-V and the Accord have seen sales fall below 10,000 units, and with refreshes failing to maintain competitiveness, they have been forced to cede an already tight market.

On the other hand, Honda's electrification strategy has yet to break out of its inherent perceptions compared to Toyota and Nissan. For example, Dongfeng Honda's annual heavyweight new energy model, the S7, sold over 100 units in its first month but hovered in the double digits for the rest of the months. Moreover, after the launch of its sister model by GAC Honda, it had to adjust its pricing a second time.

Of course, GAC Honda's P7, with a lower starting price, also failed to find a new energy remedy. On one hand, the oil-to-electric hybrid model Accord PHEV flopped, with monthly sales of only a few hundred units. On the other hand, the highly anticipated P7 also struggled to open up the new energy market, making Honda the slowest among Japanese brands in this year's transition.

Stuck in Fuel, Breaking Through New Energy

From the results, the Japanese trio's half-year reform has been effective, especially for Toyota and Nissan, which have maintained their sales base through a two-pronged price war.

From a market share of 9.2% at the beginning of the year to 9.8% in July, Japanese brands have become one of the few joint venture brands to maintain growth. In contrast, the entire market is witnessing independent brands maintaining their growth momentum, with a market share nearing 70% that squeezes the survival space of joint ventures. Joint venture brands other than Japanese ones have all declined.

Behind this is the operable space brought about by the long-term scale effect of Japanese brands. Although the prices of Toyota and Nissan's fuel vehicles continue to decline, they can still maintain the most basic gross profit margin and profitability. This is the benefit of sales volumes reaching hundreds of thousands or even millions.

Scale effect has always been the best solution for automakers. As long as sales exceed a certain threshold, profit margins can be maintained, especially for Japanese fuel vehicles. With minimal changes to the basic engine, transmission, and chassis, the scale effect can be maximized, continuously reducing production costs.

Popular models like the Corolla and the Altima can still maintain basic profitability even at current prices.

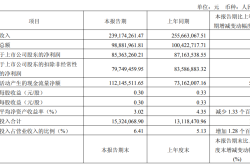

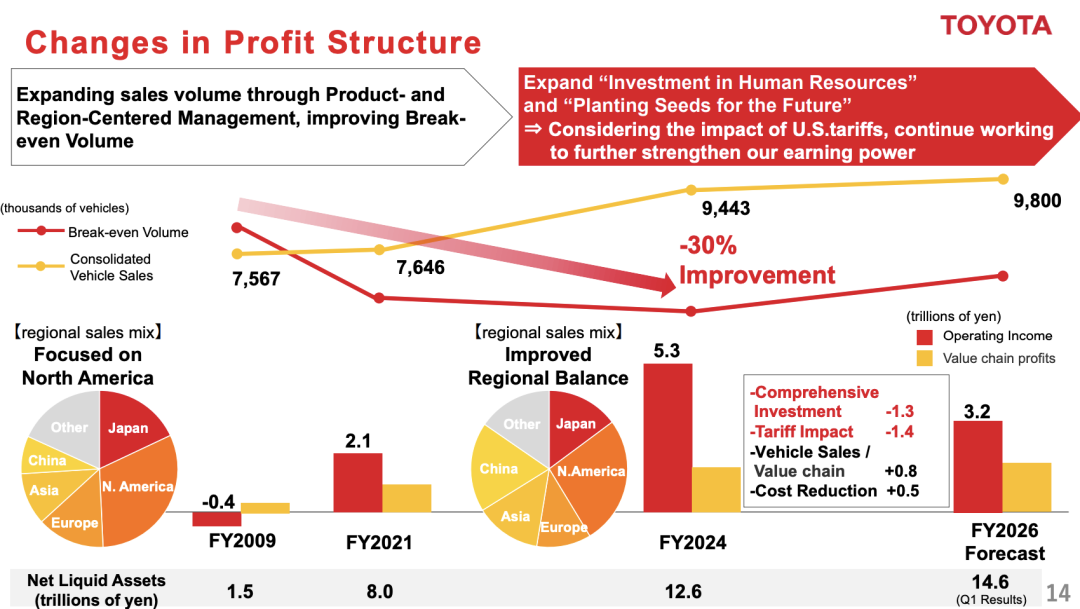

This strategy is not only implemented in China. Toyota is increasing global production capacity to ensure profits. According to the half-year financial report, Toyota achieved global sales of 4.92 million units in the first half of 2025, a year-on-year increase of 6.8%, but profitability declined significantly, with operating profit down 10% and net profit down 36.9%.

Faced with declining profits, the only thing Toyota can do is increase production. After releasing second-quarter sales, Toyota raised its annual sales target to 10 million units, hoping to offset declining profits through sales growth.

All this is to maintain the basic fuel vehicle market. Although Toyota's new energy models have made inroads in the Chinese market, sales of a few thousand units are still insufficient to cover the cost of transformation for Toyota.

After all, the early stages of new energy development involve constant capital expenditure, and there are not many automakers at home and abroad that have achieved profitability in new energy. Toyota cannot escape the realistic dilemma of subsidizing electricity with oil.

However, from Toyota's new energy strategic layout this year, it can be seen that as the world's largest automaker, Toyota still has the ability to adapt to a single market. The pricing of BZ3 shows that Toyota is relying on China's new energy supply chain to achieve self-innovation.

Under the "ONE R&D" research and development system, you can see Momenta's intelligent driving assistance system, Huawei's HarmonyOS cabin, and Hesai's lidar appearing on Toyota models.

At the same time, Toyota's courage also highlights Honda's stubbornness. The day before Dongfeng Honda's S7 was launched, GAC's BZ3 was officially unveiled, demonstrating the determination to reform with a pricing lower than that of independent brands. However, Dongfeng Honda's S7 still chose a starting price of 259,900 yuan without hesitation.

It was not until April, when GAC Honda's P7 was released at a price of 199,900 yuan, that Dongfeng Honda adjusted its pricing. Behind this is Honda's long-standing stubbornness and misjudgment of the new energy market.

Times have changed, and the premium ability of joint venture brands has long been weakened. When the Cadillac CT5 is priced at only 206,900 yuan, what confidence does the Accord have in selling its lowest configuration at 179,800 yuan?

Nissan, which is more aggressive than Toyota, fully understands this principle. The current sales of Nissan's N7 already account for more than 10% of its total sales, proving the success of Nissan's new energy strategy this time. Moreover, Nissan has also started to capitalize on its success, with the extended-range version of the N6 scheduled for release in just half a year, quickly closing the gap.

It can only be said that Japanese reforms are still ongoing. Toyota has successfully "defended" with fuel vehicles, Nissan has "counterattacked" with electrification, and Honda has "fallen behind" due to lagging strategies.

Under the wave of new energy dominated by independent brands, localized research and development and agile pricing have become the core competencies for the survival of joint venture automakers. In the next two years, whether the three Japanese automakers can establish a complete new energy matrix will determine whether they can return to the mainstream track.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for removal.

-END-

-

![]()

Is Tencent AI Heading in the Right Direction?

-

Latest Update! Jinding Optics’ GEM IPO Review Now “Under Inquiry”

-

![]()

VOYAH’s CBO Sets Ambitious Target: Secure Top 3 Spot in Luxury BEV Market Within Two Years, Launch 4 New Models to Cover All BEV Segments

-

![]()

Sehwa Technology Invests 740 Million Yuan, Eyeing the Lucrative Optical Film Market!

-

![]()

150 Million Users, $40 Million ARR: AIShige Technology Enters the Final Round of AI Video Competition

-

![]()

StepOn Star Forays into Smartphone Manufacturing: A Rationally Sound Yet High-Risk Endeavor

-

![]()

TCL Zhonghuan: Embracing a New Story Despite Anticipated Losses

-

![]()

Forty Years On: From Volkswagen’s State-Backed Entry into China to BYD’s Hiring of a Former European Foreign Minister