Leapmotor Emerges as a New Profit King: Revenue Triples in H1, Will "Price and Volume Increases" Continue in H2?

08/21 2025

08/21 2025

601

601

The Chinese new energy vehicle market in 2025 is akin to a boiling cauldron. Some players tighten their lids due to cost pressures, while others dilute their soup in price wars. Many struggle to maintain a delicate balance between "scale" and "profit" on a tightrope.

Yet, while most automakers have adjusted their annual sales targets to a "conservative range," Leapmotor has boldly raised its full-year sales target to 580,000-650,000 units, aiming for one million units in 2026. This is a virtually "disruptive" growth expectation in the history of new force automakers.

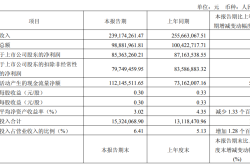

The latest financial report reveals that Leapmotor's revenue in the first half of 2025 amounted to 24.249 billion yuan, a staggering 174% increase from the same period last year, nearly doubling and significantly outpacing the 155.7% growth in sales volume.

With "price and volume increases," Leapmotor achieved its first positive semi-annual net profit during this reporting period, suggesting that the likelihood of its first annual positive profit financial report is becoming increasingly certain.

Transitioning from a "money-burning new force" to a "profitability breakthrough," Leapmotor's financial report shatters the conventional wisdom that "new forces struggle to achieve profitability." Though this performance was anticipated by the market, it doesn't prevent the company from boldly announcing to the industry: When cost-effectiveness and scale effects form a positive cycle, the "flywheel effect" will inevitably take hold.

Revenue surpasses sales volume as Leapmotor realizes "efficiency generates gold."

In the new energy vehicle industry, "profitability" remains the "Damocles' sword" hanging over most new forces. Li Auto pioneered annual profitability in 2023, yet leading companies like NIO and Xpeng continue to grapple with prolonged losses.

Clearly, in the current market where "differentiation intensifies and profits concentrate at the top," Leapmotor's "counterattack" cannot be coincidental.

A detailed breakdown of its financial report data reveals a double leap in revenue and profit. Leapmotor's revenue in the first half of 2025 was 24.249 billion yuan, a year-on-year surge of 174%, far exceeding the industry average and the company's sales growth rate for the same period. During the same period, its total deliveries increased by 155.7% year-on-year to 221,700 units.

On the profitability front, its net profit shifted from a loss of over 2.2 billion yuan in the same period last year to a profit of about 33 million yuan, making it the second new force to achieve semi-annual profitability after Li Auto.

Behind this profit growth, its gross profit margin witnessed a significant "V-shaped reversal," increasing from 1.1% in the same period last year to 14.1%, a new high since the company's inception. Leapmotor Vice President Li Tengfei predicts that this peak will continue to rise, with the gross profit margin expected to increase to approximately 15% in the second half of the year.

This leap is not solely due to the scale effects of sales growth but also benefits from the dual efforts of "cost control + product structure optimization."

The financial report shows that its cost of sales increased by only 137.9%, markedly lower than the revenue growth rate, indicating that scale effects directly reduced unit costs. Simultaneously, the launch and popularity of new models like the lidar-equipped B series increased the proportion of its high-margin intelligent configuration models, further optimizing the revenue structure. Ultimately, Leapmotor achieved high-quality expansion with both volume and price increases in the first half of the year.

Simultaneously, Leapmotor's "operating leverage" began to emerge. In the first half of the year, its revenue increased by 15.37 billion yuan year-on-year, but R&D, marketing, and administrative expenses increased by only 1.53 billion yuan. Revenue growth was 10 times the expense growth, and the overall three-expense ratio also showed a significant decrease from 28.7% in the same period last year.

This means that Leapmotor has shifted from "exchanging money for market growth" to "balancing market expansion with efficiency for profit growth."

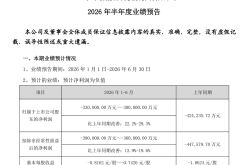

According to the latest sales guidance in the financial report, Leapmotor has raised its 2025 sales guidance to 580,000-650,000 units: Sales in July have already surpassed the monthly high of 50,000 units, and sales in August-September are expected to continue to grow, with the entire third quarter expected to reach 170,000-180,000 units, while overseas sales remain unchanged at 50,000 units.

The profit forecast is also brimming with confidence. During this financial report conference, Leapmotor clearly stated its aspiration to achieve full-year profitability in 2025, aiming for a net profit in the range of 500-1 billion yuan.

Differentiation intensifies; why can Leapmotor "win first"?

Compared to Thalys achieving "high gross profit + high turnover" through Huawei collaboration and high-end positioning, and Li Auto achieving "scale-based cost reduction + technology deferred revenue" through extended-range technology and supply chain vertical integration,

As a "latecomer" among new forces, Leapmotor has achieved semi-annual profitability in less than five years. Its core difference lies in "precise strategic focus" – avoiding the "profit trap" of the high-end market and targeting the mass market of 100,000-200,000 yuan. It uses technology-empowered "extreme cost-effectiveness" to rapidly increase volume and then leverages scale to feed back into costs and R&D.

Specifically, Leapmotor's "platformization" strategy can be regarded as the "cornerstone" of its cost control. Taking the popular B series in the first half of 2025 as an example, models like B01 and B10 are all developed based on the LEAP 3.5 platform, with a parts commonality rate as high as 88%, significantly higher than the industry average.

The high commonality rate directly brings three advantages: First, on the procurement side, the surge in procurement volume of a single part can significantly reduce supplier quotes. Second, on the R&D side, the chassis and electronic architecture of the same platform can be reused, shortening the new vehicle development cycle. Third, on the production side, standardized parts reduce production line adjustment times and improve capacity utilization.

The financial report shows that in the first half of this year, Leapmotor's R&D efficiency for the Qualcomm 8650 domain control combined assisted driving solution based on the EEA 3.5 architecture was significantly improved, with development completed in only six months and first applied to B-platform models.

On the product side, in the highly homogenized 100,000-150,000 yuan market, Leapmotor chooses to establish a differentiated label with "over-level configurations." For example, the 120,000 yuan B10 model is equipped with lidar + Qualcomm 8650 chip (supporting urban NOA), while competitors at the same price point mostly only have millimeter-wave radar + Mobileye solutions, without lidar, such as BYD Yuan PLUS and AION Y. The B01's intelligent cockpit supports "four-voice zone recognition + multi-modal interaction." Although there is still a gap in high-end functions like AR-HUD and vehicle-road coordination compared to models above 200,000 yuan, the interactive experience is already relatively close.

This strategy of "using 200,000-yuan level configurations to compete in the 100,000-yuan level market" seems to "sacrifice gross profit" but actually greatly reduces customer acquisition costs through "user word-of-mouth."

In this regard, Leapmotor's founder and chairman, Zhu Jiangming, has repeatedly emphasized the development positioning of technological equality and scale victory. "Ultimately, cars are just durable consumer goods and transportation tools. Manufacturing cars as transportation tools gives us a greater advantage in industrial development."

Additionally, Leapmotor's "asset-light" strategy permeates production, supply chain, and management links. On the production side, it adopts a "leasing + OEM" model, such as early cooperation with Changjiang Automobile, and now gradually self-builds but primarily leases factories to avoid heavy asset investment. On the supply chain side, it locks in core component prices through "centralized procurement + long-term agreements." On the management side, it establishes a "cost control committee" to conduct "cross-departmental joint audits" for every expenditure exceeding 5 million yuan to eliminate "ineffective investment."

Leapmotor's profitability also benefits from the "right timing" of the external environment. Over the past year, the cost center of power battery raw materials has shifted downwards, and there is a time lag for cost reductions to be passed on to end prices, which also provides a "time window for improving gross profit" for Leapmotor.

It must be acknowledged that in this mass market, Leapmotor will inevitably face many powerful domestic automakers, especially the competitive pressure brought by BYD, which has achieved early profitability through its strong barriers of vertical integration across the entire industry chain and the scale advantage of annual sales of one million units. Leapmotor Vice President Li Tengfei also bluntly stated, "BYD is our main competitor, and we have been observing them."

However, even so, Leapmotor is maintaining its own expansion pace for layout: for example, in terms of business policies, Leapmotor has not seen a significant promotion. Additionally, with excellent cost control through full-stack in-house research and development, Leapmotor has its own pace in setting terminal prices and business policies, including expectations for competitors and its own profitability, all within expectations.

Through these detailed financial indicators, it is evident that Leapmotor's profitability is essentially the result of an "efficiency revolution." From product development to supply chain management, from sales channels to overseas expansion, the entire system it has built around "efficiency" is strengthening Leapmotor's survival strength and internal driving force for rise as a new force.

Sprinting towards the one million target, the road is longer after the semi-annual report victory

Leapmotor's semi-annual report is a "phased victory" and also proves the feasibility of its cost-effectiveness strategy to the mass market, but the future challenges continue. As annual sales approach one million units and profitability begins to emerge, the market begins to wonder how Leapmotor will complete the leap towards "brand upgrading" and further improve its profit structure in the future.

According to plans, the first car of the D series, positioned at 200,000-250,000 yuan, will be unveiled in October this year and released in the first quarter of next year. Whether the logic of cost-effectiveness can be reused in a higher-end market remains to be seen.

It is reported that unlike the B series, the D series will focus on "tech luxury," equipped with more advanced three-electric systems (such as solid-state battery pre-research technology), a more immersive intelligent cockpit (AR-HUD + surround sound), and will attempt a mixed sales model of "direct sales + agency" for the first time to increase the output value per store.

However, the reality that must be faced is that competition in the high-end market is no less intense than in the mass market: the 200,000-250,000 yuan range is crowded with strong competitors such as the AITO series, Xpeng G6, BYD Han, and Zeekr, which not only have higher brand recognition but have also established technical barriers in intelligent driving and chassis tuning.

If Leapmotor wants to replicate the "cost-effectiveness advantage" of the B series on the D series, it needs to resolve two contradictions: first, the conflict between the demand for "brand premium" from high-end users and Leapmotor's "cost-effectiveness label"; second, the contradiction between the cost increase brought by high configurations and the pricing ceiling.

Furthermore, intelligence is the "deciding factor" in the second half of the game for new forces, but Leapmotor has been questioned for its "slow progress in intelligent driving." According to the financial report, it plans to adopt the "end-to-end algorithm + VLA" technology route to achieve urban NOA by the end of 2025 and is expected to enter the "first-tier assisted driving team" at the latest in early 2026, officially competing with Huawei ADS, Xpeng XNGP, and others.

To achieve this goal, Leapmotor is accelerating R&D investment: the scale of its intelligent driving team and the investment in computing power resources nearly doubled in the first half of the year. However, the industry generally believes that the implementation of urban NOA requires a vast amount of real road data for verification. If Leapmotor wants to meet the standard by the end of the year, it needs to rely on the sales volume of B-series models to quickly accumulate data.

As for the profit structure, within the framework of the goal of reaching one million sales next year, Leapmotor is currently more focused on scale, which is the survival line set by Zhu Jiangming. The Leapmotor management team also bluntly stated, "In overseas markets, even if gross profit improves, profits will be prioritized for market expansion."

It is clear that "counterattacking" is not the end but a new starting point. Leapmotor's one million sales target, high-end attempts, and global expansion all need to find a balance between "scale" and "quality," "efficiency" and "innovation."

As Zhu Jiangming said, we are now equivalent to 'just winning the Anti-Japanese War,' lacking everything – but as long as we maintain rapid growth, we have the opportunity to become the ultimate survivor.

In this "marathon with no finish line" of new energy vehicles, Leapmotor has already won half the race. For the remaining half, can it continue to maintain the "Leapmotor speed"? We will wait and see.

-

![]()

Is Tencent AI Heading in the Right Direction?

-

Latest Update! Jinding Optics’ GEM IPO Review Now “Under Inquiry”

-

![]()

VOYAH’s CBO Sets Ambitious Target: Secure Top 3 Spot in Luxury BEV Market Within Two Years, Launch 4 New Models to Cover All BEV Segments

-

![]()

Sehwa Technology Invests 740 Million Yuan, Eyeing the Lucrative Optical Film Market!

-

![]()

150 Million Users, $40 Million ARR: AIShige Technology Enters the Final Round of AI Video Competition

-

![]()

StepOn Star Forays into Smartphone Manufacturing: A Rationally Sound Yet High-Risk Endeavor

-

![]()

TCL Zhonghuan: Embracing a New Story Despite Anticipated Losses

-

![]()

Forty Years On: From Volkswagen’s State-Backed Entry into China to BYD’s Hiring of a Former European Foreign Minister