Many Newcomers Have Been in the Market for Quite a While, Yet Only a Handful Are Turning a Profit

11/19 2025

11/19 2025

483

483

Text by Wang Xin, Design by Yang Lingxiao, Produced by Electric New Species

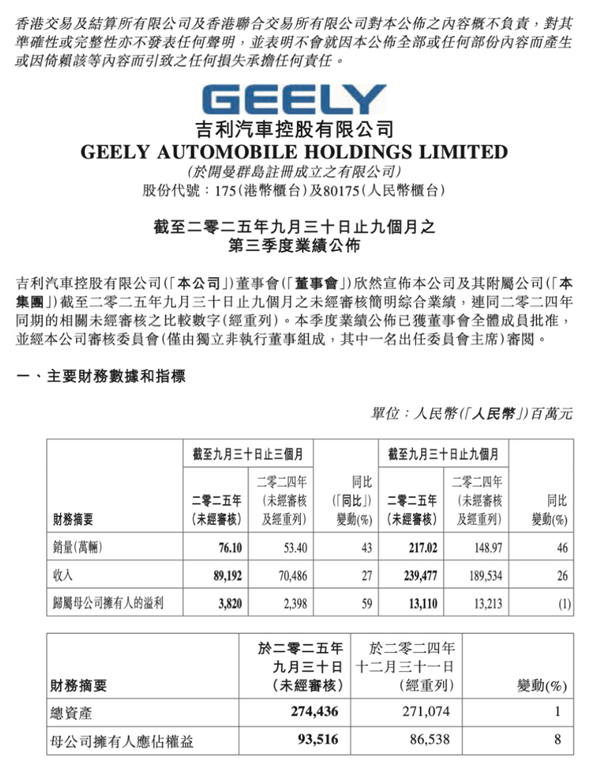

On November 17, during Geely Auto's Q3 2025 earnings conference call, Gui Shengyue, CEO and Executive Director of Geely Auto Holding Co., Ltd., highlighted that numerous newcomers in the automotive sector boast a relatively lengthy development history, with some even having been established for eight to nine years. Despite experiencing notable sales growth this year, merely a small fraction of these newcomers are currently profitable.

Gui Shengyue also stressed, "Next year, the auto market will embark on a stringent selection process. Without robust profitability, I believe it will be exceedingly challenging to survive."

With the penetration rate of the new energy vehicle market surpassing 50%, this debate on "scale versus profitability" marks a pivotal turning point for the industry, transitioning from rapid expansion to high-quality development.

Geely's own performance strongly corroborates these statements. Geely Auto's financial report reveals that revenue in the third quarter soared to a record high of 89.2 billion yuan, with net profit reaching 3.82 billion yuan, marking a 59% increase year-on-year. Total sales in the first three quarters amounted to 2.1702 million units, a 46% rise year-on-year, with the new energy penetration rate hitting 58%.

On one hand, traditional leading automakers are achieving stable profitability post-transformation, while on the other, most newcomers are ensnared in the dilemma of "high volume but low profitability." China's new energy vehicle market is undergoing an unprecedented industry shakeout, with profitability emerging as the core criterion for assessing a company's vitality.

01 The Gap Between Scale and Profitability Among Newcomers Has Become Apparent

The evolution of China's new energy vehicle manufacturers has spanned over a decade. From the early explorations of "NIO, XPeng, and Li Auto" to the emergence of brands like Leapmotor, Xiaomi, and Harmony Intelligent Mobility, the industry landscape has undergone substantial transformations.

However, a stark reality persists: even though some companies have attained monthly sales of 40,000 units, profitability remains an elusive goal for the majority.

Currently, only three domestic new energy vehicle manufacturers have achieved profitability: Li Auto, AITO, and Leapmotor. Xiaomi Auto and NIO, which are on the cusp of entering the profitability ranks, have also undergone a lengthy period of market refinement.

Xiaomi Auto has achieved monthly sales of 40,000 units with just two models, while NIO, leveraging its "NIO, Leapmotor, and Firefly" brand matrix, surpassed 40,000 deliveries in October, charging towards its goal of profitability in the fourth quarter.

The common trait of these companies is that they have all established mature product matrices and stable user bases, gradually reducing costs through economies of scale.

In contrast, numerous once-prominent newcomers are now facing difficulties.

Neta Auto has merely 15 million yuan in cash on hand but is saddled with 5.1 billion yuan in debt. WM Motor, after accumulating over 20 billion yuan in liabilities, only resumed production with government and capital support. HiPhi's plan to introduce overseas capital has hit a snag.

These cases substantiate Gui Shengyue's assessment that companies lacking automotive heritage and profitability will find it increasingly arduous to compete in the industry.

Meanwhile, the profitability practices of leading companies offer valuable benchmarks for the industry.

Leapmotor has led newcomer sales for eight consecutive months, with deliveries surpassing 70,000 units in October, achieving profitability through its "good cars at affordable prices" strategy. AITO, relying on the Harmony Intelligent Mobility ecosystem, not only set a record of reaching one million deliveries in just 43 months but also achieved an average transaction price of 390,000 yuan, attaining a dual breakthrough in scale and profit.

The success of these companies demonstrates that only brands that genuinely cater to consumer needs and build core competitiveness can stand firm in the market.

02 Geely: A Transformation Benchmark Supported by Heritage

While most newcomers grapple with profitability, Geely Auto's consistent performance underscores the unique advantages of traditional automakers in transformation.

The "automotive heritage" emphasized by Gui Shengyue is fully embodied in Geely's development. This heritage is not only evident in mature manufacturing experience but also in precise insights into supply chain control and market demand.

Geely's profitability is no fluke. Third-quarter data indicates that its fuel and new energy vehicles have grown concurrently, driving a 43% increase in total sales year-on-year.

By brand, Geely Galaxy has emerged as the absolute mainstay with 327,000 units sold, while China Star fuel vehicles maintained stable output of 219,000 units. The Zeekr and Lynk & Co brands also contributed significantly to sales. This multi-brand, full-category layout endows Geely with stronger resilience against market fluctuations.

More notably, Geely's integration of Zeekr is a pivotal step in leveraging its supply chain synergy advantages. Gui Shengyue clearly stated at the earnings call that Zeekr's delisting and merger with Geely face no legal impediments, with the transaction expected to be finalized by the end of the year.

This integration initiative is a crucial move for Geely to capitalize on its supply chain synergy advantages. By integrating resources and eliminating redundant investments, overall operational efficiency is enhanced—a mature corporate management logic that many newcomers lack.

Geely's financial reserves lay the foundation for its sustained development. As of the end of September, Geely's net cash level reached 45.2 billion yuan, with ample cash flow enabling continuous investment in R&D and product iteration.

In the fourth quarter, Geely will launch several new models, including the Galaxy Star Glory 6, to sprint towards its annual sales target of 3 million units. This "steady growth + continuous innovation" model not only achieves the company's profitability but also sets a transformation benchmark for the industry.

Compared to the development paths of newcomers, Geely's advantage lies in combining the quality control and supply chain management capabilities amassed in traditional automotive manufacturing with intelligent technologies and user experiences in the new energy era.

This "old foundation + new approach" model circumvents the trial-and-error costs of starting from scratch, enabling it to maintain healthy profitability while expanding its scale.

03 Accelerated Industry Shakeout: China's New Energy Vehicle Market Poised for Qualitative Transformation

Gui Shengyue's prediction that "next year, the auto market will commence a rigorous selection process" is not an exaggeration.

As market competition intensifies, the survival rules in the new energy vehicle market are becoming increasingly clear: in addition to profitability, comprehensive strengths in product competitiveness, brand influence, and ecological layout jointly constitute a company's core competitiveness.

Product competitiveness remains the linchpin of market competition. Leapmotor's success stems from its commitment to product cost-effectiveness, covering multiple market segments from "half-price Li Auto" to "full-spec Leapmotor." The launch of its full-size flagship SUV, the Leapmotor D19, in October further enhanced its product matrix.

The construction of brand ecosystems is reshaping the competitive landscape. Harmony Intelligent Mobility has achieved full coverage of products priced between 150,000 and 1 million yuan through its "five-brand integration" layout, setting a record of reaching one million deliveries in just 43 months and proving the formidable strength of ecological synergy.

NIO's "NIO, Leapmotor, and Firefly" brand matrix caters to different price segments, with the Leapmotor L90 surpassing 33,000 deliveries in just three months after its launch, securing the top spot in pure electric large SUV sales. This multi-brand operation model effectively expands market share.

Channel layout has become a pivotal factor influencing sales. Leapmotor has established 942 stores, while Harmony Intelligent Mobility relies on Huawei's terminal experience stores to achieve channel coverage of over a thousand locations, making it more convenient for consumers to access products.

IM Motors, with core technologies such as the 800V high-voltage platform and city NOA without maps, has made its new-generation LS6 a phenomenal product in the 200,000-yuan-level new energy mid-to-large SUV segment. These cases prove that continuous technological investment is imperative for building formidable competitive barriers.

Meanwhile, healthy competition in the industry is driving overall industrial upgrading. Ford CEO Jim Farley once stated that the leading level of China's new energy vehicle manufacturers is astonishing, and this competitive pressure has prompted Ford to accelerate its reforms.

From the consecutive five-month decline in the proportion of extended-range vehicles to the collective shift of newcomers towards the core pure electric vehicle track, the market is continuously optimizing its product structure and driving technological progress through competition, ultimately benefiting consumers.

Summary: Profitability Emerges as a Stringent Indicator for Newcomer Survival

China's new energy vehicle market is bidding farewell to the era of rampant growth and entering a high-quality development phase centered on profitability.

Gui Shengyue's remarks underscore a key proposition for the industry: automotive manufacturing is not a fleeting trend but a long-term endeavor requiring heritage, technology, and sustained profitability.

From Geely's consistent profitability to the profitability breakthroughs of Leapmotor and AITO, from the ecological rise of Harmony Intelligent Mobility to the technological innovation of IM Motors, the practices of leading companies are defining new development paradigms for the industry.

This industry shakeout is not a zero-sum game but an inevitable process of industrial upgrading. Companies that can strike a balance between scale and profitability and prioritize both technology and user experience will emerge as industry leaders.

With Geely completing its integration of Zeekr and companies like NIO and Leapmotor gradually entering the profitability ranks, China's new energy vehicle market is forging a healthier and more mature competitive landscape.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving