Joint Venture and Local Brands: A Shift in Dynamics

03/20 2026

03/20 2026

448

448

Systemic Shift in the RMB 200,000 Price Range

From premium pricing to discount sales, the competitive advantage of joint venture brands has rapidly eroded over the past five years.

In 2025, domestic sales of passenger vehicles from China's local brands are expected to reach approximately 15.53 million units, capturing a 64.6% market share, while the once-dominant joint venture brands are projected to fall to 35.4%.

Looking back to 2020, the market landscape was vastly different. Joint venture brands held a firm grip with a 64.3% share, while local brands, at 35.7%, were mostly confined to the below RMB 150,000 segment.

In just five years, the offensive and defensive positions have completely reversed. More notably, the 64.6% market share of local brands in 2025 is no longer solely supported by the low-end market. In the mid-to-high-end segments priced at RMB 200,000, RMB 300,000, and even higher, local brands have achieved tangible sales breakthroughs, forming a competitive edge across all price ranges.

Local brands have upgraded from low-price volume sales to mid-to-high-end breakthroughs, gradually breaking through the brand premium and technological barriers that joint venture brands have long relied on. This has reshaped the industry landscape of China's passenger vehicle market.

Joint Venture Brands Cede the RMB 200,000 Price Range

The RMB 200,000 price range was once considered the “comfort zone” and “moat” for joint venture brands. Leveraging their long-accumulated technological advantages and brand premiums, classic B-segment sedans like Volkswagen's Magotan and Passat, Toyota's Camry, and Honda's Accord dominated this segment, becoming the “safe choice” for middle-class families.

However, models that once commanded premium prices of RMB 20,000–50,000 in the internal combustion engine era are now frequently offering substantial discounts. For instance, the plug-in hybrid version of the Accord recently celebrated the brand's 50th anniversary with a promotional price of RMB 138,800. Although limited to 1,000 units and exclusive to repeat customers, this represents a RMB 100,000 discount from its previous official guide price of RMB 238,800—a striking contrast.

The Accord's promotion is not an isolated case. To compete for market share, mid-to-large-sized models from joint venture automakers are lowering their profiles. According to market conditions, the Ford Edge L, with an official guide price ranging from RMB 229,800 to RMB 309,800, is now available at a terminal discounted price as low as RMB 198,800 for the entry-level model. The situation is similar for the Highlander, priced between RMB 249,800 and RMB 325,800, with discounted prices in some regions starting as low as RMB 179,800. The Volkswagen Teramont, with a higher guide price range of RMB 289,000 to RMB 359,900, offers discounts of up to RMB 76,000 in some markets, bringing the starting price down to RMB 213,000.

For new models, the pre-sale of GAC Toyota's new flagship all-electric sedan, bZ4X, starts at just under RMB 200,000, yet includes three core configurations: HarmonyOS cockpit, LiDAR-based intelligent driving, and dual-chamber air suspension. Similarly, Buick's premium new energy sub-brand, “ELECTRA,” has priced its first model, the ELECTRA L7, at just RMB 170,000.

The price reductions from luxury brands are equally astonishing. On March 10, the all-new Audi A6L announced its pre-sale price range of just RMB 323,000 to RMB 436,000, compared to the previous guide price of RMB 427,900 to RMB 558,900. The starting threshold has been slashed by over RMB 100,000, effectively incorporating past dealership discounts into the official pricing. At the beginning of 2026, BMW reduced prices for 31 of its models, with reductions generally ranging from 10% to 20%, bringing models like the M235L below the RMB 300,000 mark.

According to data from the China Passenger Car Association (CPCA), the average market price of passenger vehicles from joint venture brands fell to RMB 173,000 in 2025, down RMB 7,000 from 2024, marking a second consecutive year of decline. Meanwhile, although new energy brands also saw a significant drop in average market prices during the same period, their average transaction price remained at RMB 241,000, far exceeding that of joint venture brands.

Whether through proactive adjustments or passive responses, joint venture brands have effectively used their decades-accumulated brand equity, pricing power, and global reputation as bargaining chips to secure their foothold in the Chinese market. Meanwhile, Chinese consumers have shifted from “brand-centric” evaluations to comprehensive assessments of product strength, intelligence, and cost-effectiveness, enabling local brands to make significant breakthroughs in the high-end market.

According to data from the third-party research firm JL Research in its “2025 China Passenger Vehicle Market Brand Price Annual Review,” brands like WEY, ZEEKR, Xiaomi, and others have solidified their positions in the mid-to-high-end market above RMB 200,000. Brands such as AITO, Li Auto, and NIO have entered the luxury segment above RMB 300,000, breaking the long-term monopoly of joint venture and luxury brands in high-value markets.

Several key figures are particularly noteworthy: Li Auto's average vehicle price reached RMB 300,000, surpassing Audi's RMB 287,000; AITO led with an average vehicle price of RMB 386,000, well ahead of BMW's RMB 341,000; and Xiaomi, as a new industry player, achieved an average vehicle price of RMB 269,000, slightly exceeding Tesla's RMB 266,000.

A Seismic Shift in China's Auto Market

Why have the advantages built by joint venture brands during the internal combustion engine era dissipated so rapidly in just a few years? The core reason lies in China's automotive industry achieving systemic superiority in electrification and intelligence, fundamentally rewriting the underlying logic of the market.

The comprehensive upgrade in product strength is the cornerstone of China's brand resurgence. Today's domestically produced new energy vehicles not only feature more luxurious interiors and stronger performance but also come standard with refrigerators, TVs, and seat massage functions. Intelligent cockpits and advanced driver-assistance systems tailored to local needs have become core advantages over joint venture brands.

Source: JL Research

Source: JL Research

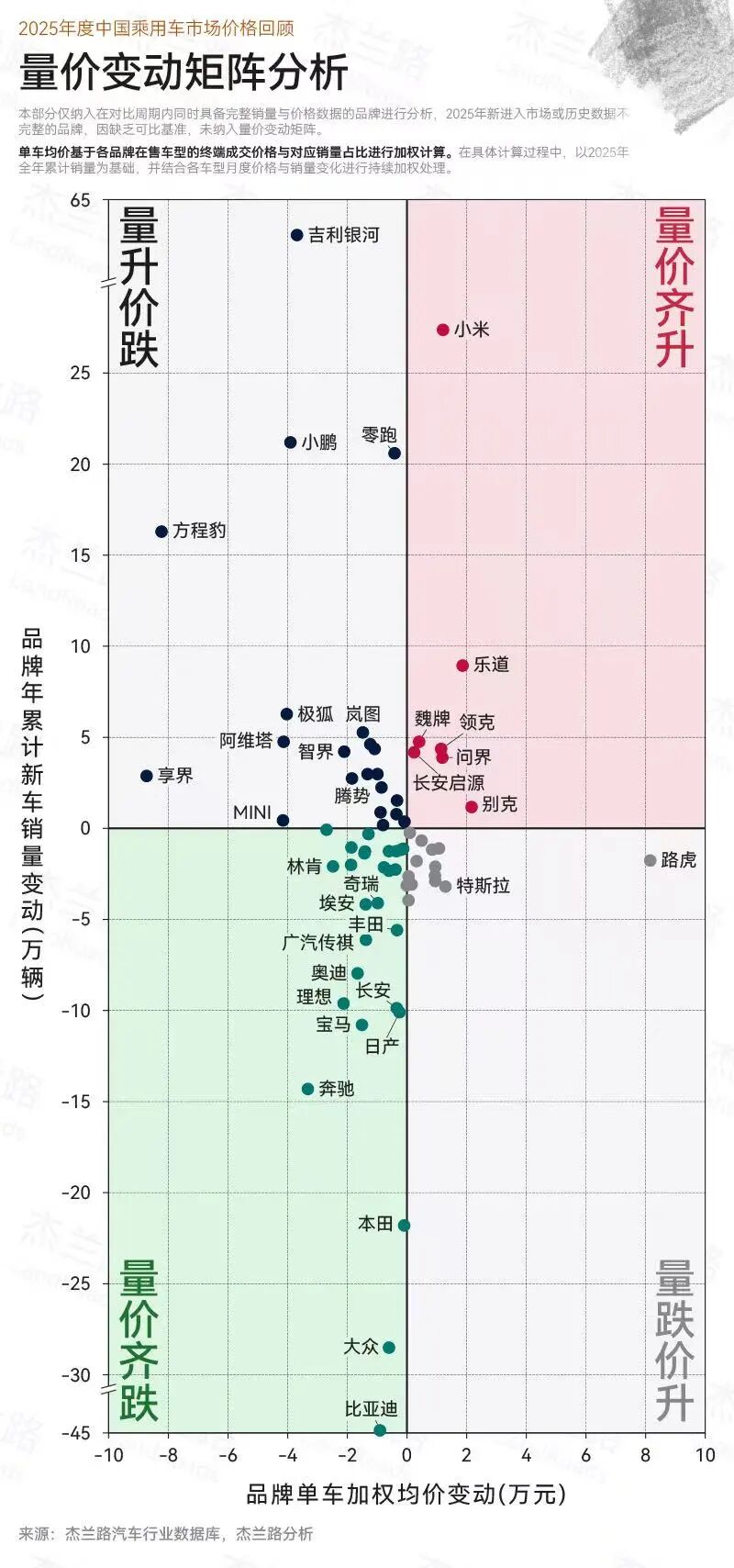

JL Research data shows that in 2025, passenger vehicle brands like Toyota, Honda, Volkswagen, and Nissan experienced declines in both sales volume and average prices, while brands such as Xiaomi, Lectra, AITO, Lynk & Co, and WEY saw simultaneous increases in both metrics.

From an overall market perspective, traditional strong brands like BYD, Volkswagen, Toyota, Mercedes-Benz, and BMW all experienced notable declines in new vehicle sales revenue in 2025. Mercedes-Benz saw a drop of over RMB 80 billion, Volkswagen over RMB 50 billion, and BMW nearly RMB 50 billion. Brands like Honda and Audi also generally declined by over RMB 30 billion, with leading players facing significant adjustment pressures due to price pressures and fluctuating sales volumes.

At the same time, some new energy and transitioning brands achieved significant scale expansion. Xiaomi's new vehicle sales revenue increased by over RMB 75 billion year-on-year, Geely Galaxy by over RMB 45 billion, and Fangcheng Bao by over RMB 30 billion. Brands like XPENG, Leapmotor, and Lectra also saw growth in the RMB 20–30 billion range. AITO, VOYAH, NIO, Buick, Lynk & Co, and ZEEKR generally experienced increases in new vehicle sales revenue exceeding RMB 10 billion, forming the most dynamic growth tier in the current market.

Over the past year, Xiaomi's vehicle sales reached 414,000 units, a year-on-year increase of 387.9%. In the fourth quarter of 2025, NIO achieved quarterly profitability for the first time. In the first two months of 2026, NIO continued its strong growth, delivering 47,979 units from January to February, a year-on-year increase of over 70%.

From 2020 to 2025, China's passenger vehicle market underwent a silent yet profound revolution over five years. The defining event of this revolution was not a single breakthrough by a particular brand but the systemic shift in ownership of the entire RMB 200,000 price range. The technological advantages and brand premiums that joint venture brands relied on in the internal combustion engine era have rapidly eroded in the new energy era. Chinese brands, with more agile product strategies, intelligent experiences tailored to local needs, and competitive pricing systems, have achieved a comprehensive comeback, from market share to pricing power.

However, it is also evident that joint venture and luxury brands are now systematically abandoning their insistence on “technological independence,” embarking on a comprehensive “localization” transformation across R&D, products, and supply chains. For instance, GAC Toyota's bZ4X utilizes Huawei's full suite of intelligent solutions; FAW-Audi has fully equipped new models like the A5L and Q6L e-tron with Huawei's advanced intelligent driving system; while Mercedes-Benz and BMW have chosen to partner with Momenta to develop intelligent driving and interaction systems tailored to Chinese road conditions and user habits.

The window of opportunity gained at the expense of profits and brand stature is narrowing. The competition in the new era of intelligent electric vehicles has only just begun.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?