From a Profit of 2.3 Billion to an Investment of 10.4 Billion: Is Horizon Robotics Squandering Funds or Fortifying Its Position in 2025?

03/20 2026

03/20 2026

501

501

Author | Zhang Lianyi

Horizon Robotics is clearly making a high-stakes bet on the future, as evidenced by its financial records.

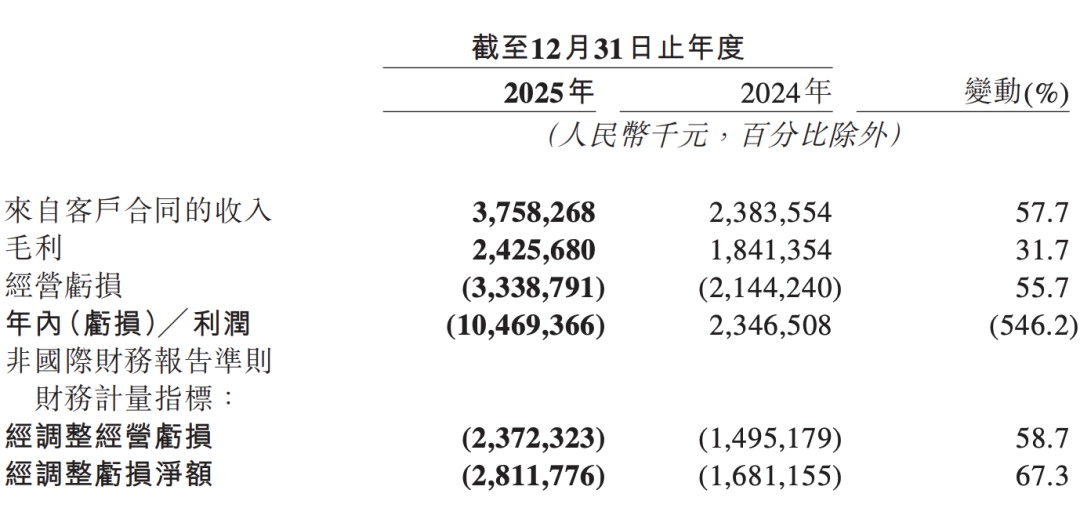

On March 19, Horizon Robotics unveiled its 2025 financial results, showcasing a stark dichotomy: On one hand, the company achieved a full-year revenue of 3.76 billion yuan, marking a 57.7% year-on-year increase. On the other hand, it reported a loss for the year, despite having recorded a profit of 2.347 billion yuan in 2024.

Horizon Robotics 2025 Financial Highlights

Horizon Robotics 2025 Financial Highlights

At first glance, this financial report does not fit the traditional mold of a "beautiful" report. However, behind the revenue growth without a corresponding increase in profit lies the true strategic landscape of this intelligent driving chip company: high growth, high investment, robust delivery, and securing technological and market positions through significant spending during the critical phase of mass production and popularization of high-level intelligent driving.

01

Financial Records: The "Contradiction" of High Growth and High Investment

Let's first delve into the core revenue data.

In 2025, Horizon Robotics achieved revenue of 3.758 billion yuan, a 57.7% increase from the previous year. Amidst intensifying price wars among automakers and widespread supply chain pressures, this growth rate is commendable.

More noteworthy is the "quality" of this revenue.

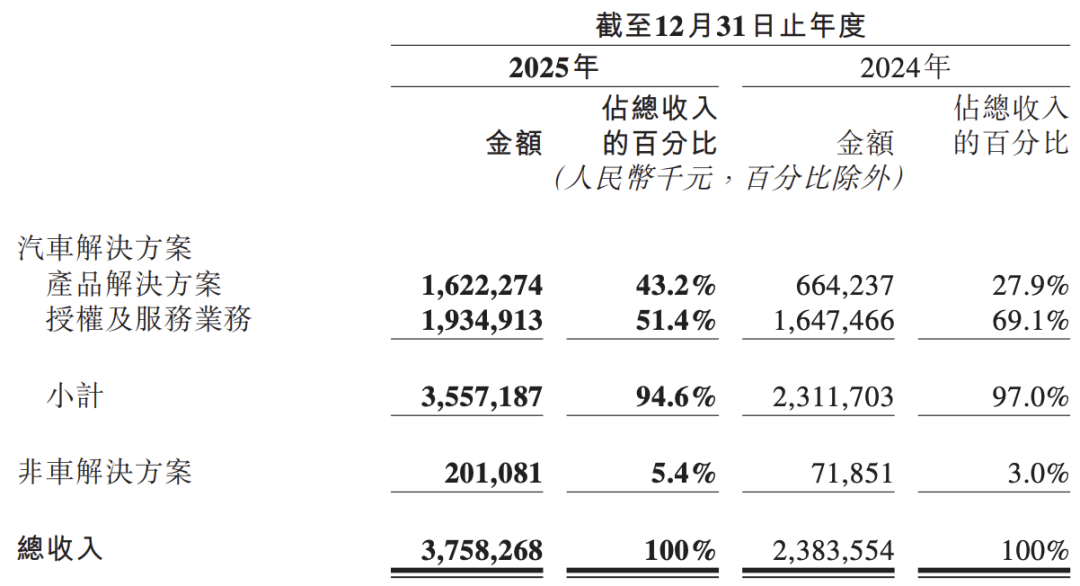

Horizon's revenue primarily stems from two segments: product solutions and licensing and services.

Horizon's Revenue by Business Segment

Horizon's Revenue by Business Segment

In 2025, Horizon's product and solution revenue soared to 1.622 billion yuan, a 144.2% year-on-year increase. This indicates that Horizon is no longer solely reliant on licensing fees ("ticket money") but is genuinely selling substantial volumes of hardware and integrated hardware-software solutions. This segment's share of total revenue surged from 28% last year to 43%.

Licensing and service revenue reached 1.935 billion yuan, a 17.4% increase from the previous year. While growth has slowed, it still provides a stable cash flow foundation. Horizon CEO Yu Kai revealed during the earnings call that, in addition to collaboration with Volkswagen's joint venture, Horizon has also initiated algorithm and software licensing partnerships with Japan's largest automotive parts group, which became one of Horizon's top five customers in 2025.

"This reflects a structural optimization of revenue sources following the mass production cycle of mid-to-high-level intelligent driving assistance solutions," Yu Kai stated.

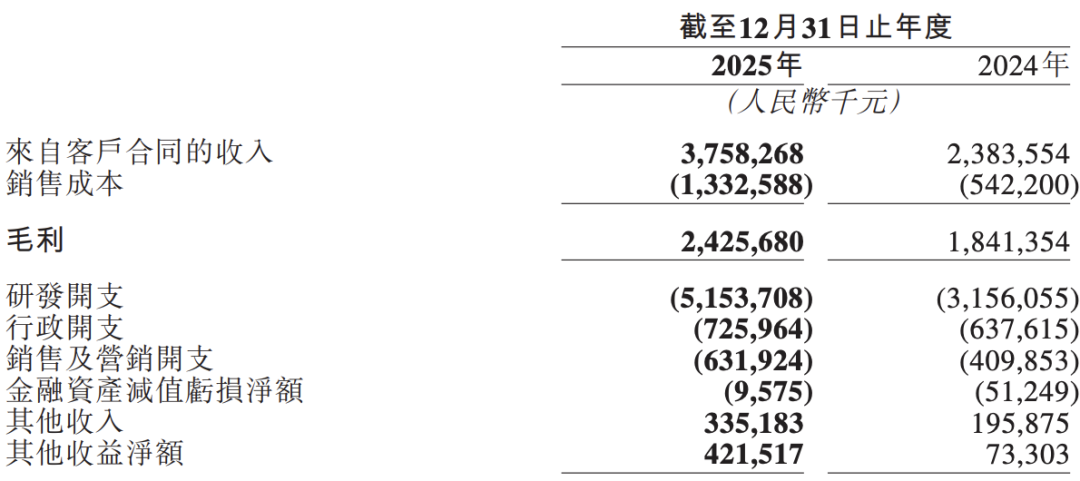

In terms of gross profit, Horizon achieved 2.43 billion yuan in gross profit in 2025, maintaining a high overall gross margin of 64.5%. The core automotive business gross margin reached 67.2%. Although slightly down from the previous year, it demonstrates that Horizon's products still command some pricing power and technological premium amidst fierce market competition.

However, the flip side of the coin is substantial losses.

In 2025, Horizon's annual loss ballooned to 10.469 billion yuan. In contrast, the company recorded a profit of 2.347 billion yuan in 2024.

Why did profits transform into even larger losses?

The financial report indicates that the primary reasons for the expanded loss are high-intensity R&D investment, market expansion costs, and non-cash factors such as changes in the fair value of preferred shares. In simpler terms, Horizon is reinvesting all its earnings into the future.

Horizon Increases R&D Investment

Horizon Increases R&D Investment

The financial report reveals that Horizon's R&D expenditure reached 5.154 billion yuan in 2025, a 63.3% year-on-year increase. These investments were primarily allocated to cloud service fees and procurement of other technical services, with a focus on supporting the development of the all-scenario urban navigation-assisted driving solution HSD and advanced driver-assistance systems based on the Journey 6 platform.

In terms of cash flow, as of the end of 2025, cash and cash equivalents stood at approximately 20.2 billion yuan, a 31.3% increase from 15.371 billion yuan at the end of 2024. This may be the confidence behind Horizon's willingness to "burn money" for the future.

02

Business Breakthroughs: Not Just "Volume" but Also "Upgrading"

Compared to the fluctuations in financial data, business breakthroughs are even more remarkable.

In 2025, the penetration rate of mid-to-high-level intelligent driving in China's passenger vehicle market doubled, and Horizon precisely capitalized on this wave of dividends.

According to industry data, the penetration rate of intelligent driving assistance in China's passenger vehicle market reached 67.6% in 2025, with the proportion of vehicles equipped with NOA (Navigate on Autopilot) surging from 21.6% in 2024 to 42.6%. In the mainstream market below 200,000 yuan, the penetration rate of mid-to-high-level intelligent driving rose from 5% at the beginning of the year to over 50% by the end of the year. Horizon captured a 44% market share in this price segment, ranking first.

The financial report shows that total shipments of Horizon's Journey series chips reached 4.01 million units in 2025, a 38.8% year-on-year increase. Among them, shipments of mid-to-high-end chips supporting functions such as highway NOA and urban NOA reached 1.8 million units, nearly quintupling year-on-year.

This means that for every 10 chips sold, 4.5 are used for high-level intelligent driving. Mid-to-high-end chips contributed over 80% to overall product and solution revenue.

The successful mass production of the Journey 6 series is a key weapon for Horizon to capture market share. The application of the single Journey 6M solution has brought urban NOA to the 100,000-yuan mass-market vehicle segment, achieving full-range coverage from affordable to premium models.

In the basic ADAS market, Horizon also retained its championship with a 47.7% share. Over 95% of chip shipments supporting NOA functions were delivered through ecosystem partners.

Horizon is clearly not content with this; it aims to continue "moving upward."

In November 2025, Horizon's HSD achieved mass production, becoming China's first mass-produced intelligent driving model based on end-to-end technology. It was first deployed in mainstream models priced around 150,000 yuan, with over 22,000 units delivered within a month.

Horizon HSD Mass Production in November 2025

Horizon HSD Mass Production in November 2025

Yu Kai stated during the earnings call that the successful mass production of HSD and its enthusiastic market reception have validated the effectiveness of the company's R&D investments. He firmly believes that HSD is not only Horizon's core strategic product for winning in urban intelligent driving but also the technological foundation for future L4 and L5 autonomous driving. "Its underlying AI foundation model will further become an enabling technological foundation for industries such as robotics."

As of the end of the reporting period, Horizon had secured design wins for over 110 new models, covering mainstream domestic brands and joint-venture automakers. Among them, the HSD solution had secured design wins for over 20 models. Yu Kai added, "This is just a snapshot as of the end of last year. This year, Horizon will see an explosion in design wins for the HSD solution."

Additionally, Horizon's globalization pace is accelerating. As of 2025, Horizon has assisted 11 automakers and over 40 models in going overseas, covering five major regions including Asia, Europe, and South America. Based on the Journey 6 series, Horizon has secured overseas design wins from several Japanese automakers, with expected full-lifecycle shipments being substantial.

03

New Year Plans: Unit Price Increases and New Market Layouts

Regarding the 2026 outlook, Yu Kai expressed full confidence: "In 2025, the automotive segment's revenue growth was 54%. We are confident it will further accelerate to around 60% in 2026."

This confidence is bolstered by two factors. In terms of shipments, Horizon secured design wins for over a hundred new models in 2025, most of which are mid-to-high-end models set to begin mass production in 2026. Yu Kai expects shipments to grow by around 35% in 2026 from the 2025 base of 4 million units.

More importantly, there will be an increase in product unit prices. Shipments of AD chips will rise from 45% to over 55%. The unit price of AD products is significantly higher than that of ADAS products, and the high growth rate of AD chips will also have a positive impact on pricing.

Horizon CEO Yu Kai

Horizon CEO Yu Kai

Yu Kai further revealed that although chip-related business grew by over 75% in 2025, the average selling price was less than $60, leaving 50% room for increase compared to the average selling price of highway NOA products and tenfold room compared to urban NOA products. "The increase in product unit prices will contribute even more to our revenue growth in the coming years than shipment volumes."

In the L4 autonomous driving field, Horizon has also made preparations. The company plans to launch pilot Robotaxi operations in specific Chinese cities in the second half of 2026, in collaboration with ecosystem partners, relying on the foundation model behind the HSD solution.

In terms of new product deployments, Horizon will launch China's first cockpit-driving fusion full-vehicle intelligent agent chip (AgenticCAR SoC) and intelligent agent operating system (AgenticCAR OS) this year. Yu Kai believes, "Cockpit-driving fusion is an inevitable result of technological and product evolution," and Horizon hopes to transform automobiles into AI assistants that surpass smartphones.

Balancing technological investment and commercial returns has always been a core challenge for technology innovation companies. Horizon's financial report, showing 57.7% revenue growth and 63.3% R&D investment growth, demonstrates its tilt toward the latter.

As urban NOA becomes the core competitiveness of next-generation vehicle models, Horizon's choice to heavily invest in technological R&D will ultimately be tested by the market—whether it becomes a moat or a burden.

-END-

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?