Horizon Robotics' "Triple Challenge": Soaring Revenue, Widening Losses, and Executive Shake-Up

03/20 2026

03/20 2026

771

771

Horizon Robotics Enters the "Deep Waters"

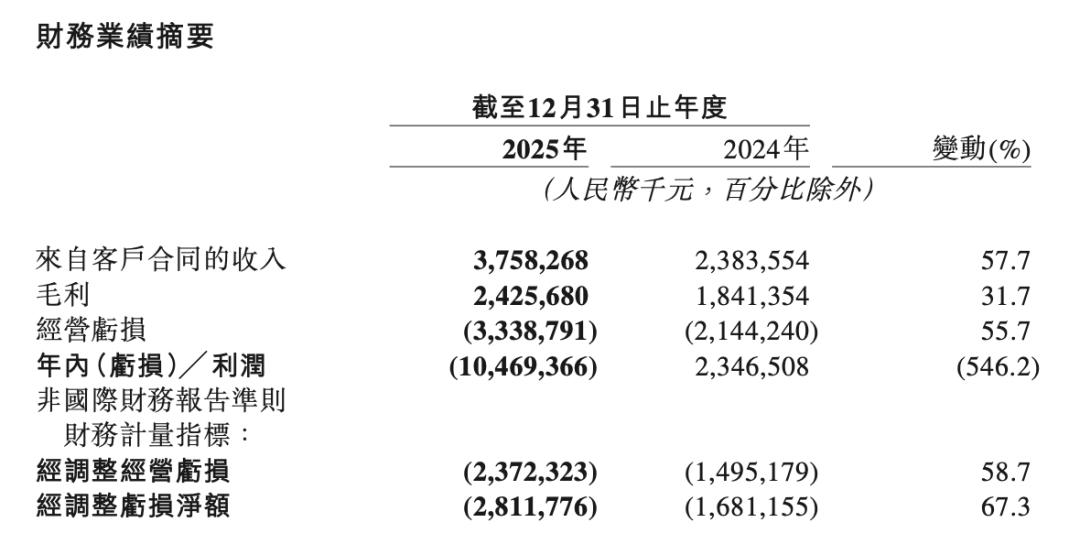

On March 19, Horizon Robotics (9660.HK) released its 2025 financial report, delivering a mixed performance: full-year revenue reached RMB 3.758 billion, up 57.7% year-on-year, but net losses widened to RMB 10.47 billion, compared to a profit of RMB 2.347 billion in 2024, marking a shift from profit to loss. Additionally, adjusted net losses stood at RMB 2.812 billion, up 67.3% year-on-year.

Notably, just before the financial report's release, media reports indicated that Chen Peng, the head of chip R&D at Horizon, was set to depart, with Su Qing, Horizon's Vice President and Chief Architect, potentially taking over his role.

As a seasoned technologist with nearly two decades of experience in the ICT chip industry, Chen Peng played a pivotal role in the architectural design and mass production of Horizon's Journey 6 series chips. His departure is far from an ordinary personnel change.

Image Source: Baidu Screenshot

Timing-wise, this change coincides with a critical phase in the development of the "Journey 7" chip, prompting the outside world to re-examine Horizon's current internal state. In fact, over the past year, Horizon has undergone multiple rounds of internal adjustments, including algorithm team restructuring, executive turnover, and shifts in ecological collaboration models.

Meanwhile, the external competitive landscape is rapidly evolving. "NIO, XPeng, and Li Auto" are accelerating their in-house chip development, while Momenta is expanding into the chip sector, redefining the boundaries of the entire intelligent driving chip industry chain.

In this new round of market competition, can this leading domestic intelligent driving chip company maintain its position and find new growth drivers?

01. Key Figure Departs: The Story Behind Horizon's Executive Turmoil

As a long-time technical leader in the ICT chip industry, Chen Peng joined Horizon during the development phase of the "Journey 6" series and was deeply involved in the entire process, from architectural design and engineering realization to mass production and shipment of the "Journey 6P."

In the highly complex and long-cycle field of chip R&D, a core figure capable of overseeing the entire process from design to mass production wields significant control over product roadmaps, team collaboration, and even supply chain rhythms. Thus, when such a key player chooses to leave during a critical phase of the "Journey 7" rollout, the signal behind it extends far beyond a single personnel change.

Zooming out, Chen Peng's departure appears to be part of a broader organizational restructuring at Horizon. Over the past two years, the company has repeatedly overhauled its internal systems.

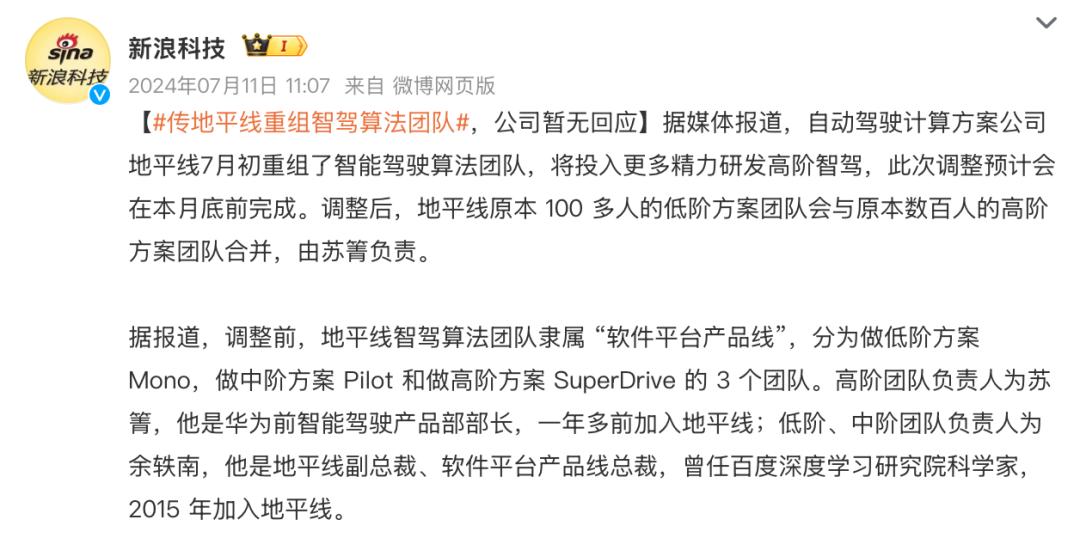

In mid-2024, Horizon integrated its algorithm teams: previously dispersed low-, mid-, and high-tier teams were reorganized, with the low-tier team merged into the high-tier system and the mid-tier team split among joint ventures like Continental Intelligent Driving and CorePower to strengthen global expansion and scaling (mass-market) deployment capabilities. This adjustment essentially concentrated resources on high-tier assisted driving and core products while offloading some commercialization pressure to joint ventures.

Image Source: Weibo Screenshot

Entering 2026, changes accelerated further. Chen Liming, Horizon's Vice Chairman, gradually stepped back from management, while Zhu Wei from the CATL ecosystem joined Horizon as President and President of the Intelligent Vehicle Business Unit. Coupled with news of Chen Peng's impending departure, Horizon is undergoing a denser reshuffling of its technical and management structures.

This round of organizational restructuring comes amid sustained high R&D investment by the company.

Financial reports show that Horizon's R&D expenditure reached RMB 5.154 billion in 2025, up 63.3% year-on-year, accounting for 137.1% of revenue. This investment primarily supported the development of the full-scenario urban assisted driving system HSD and the construction of cloud computing resources.

Image Source: Financial Report Screenshot

Multiple investment banks previously estimated that with intensifying competition in high-tier autonomous driving algorithms, Horizon's R&D spending would remain high in 2026-2027, potentially exceeding RMB 5 billion. This means any turbulence in Horizon's R&D system could impact its substantial R&D investments.

More importantly, amid accelerating competition in intelligent driving chips, external expectations for Horizon are rising. Consequently, any changes in its R&D system or organizational structure are magnified as judgments about the company's pace and capabilities.

02. Chip Competition Intensifies: Journey 7 as the Critical Variable

If organizational adjustments represent "internal variables," at the product level, Horizon faces more direct and tangible pressures.

The "Journey 6" series chips were seen as a crucial step toward high-tier assisted driving, aiming not only to build on past successes in the L2 and highway NOA markets but also to break into urban NOA—a more complex and valuable segment.

However, market feedback indicates that the first products to achieve significant scale were primarily low-cost offerings like the J6B, which leveraged cost advantages to penetrate models priced at RMB 100,000 or below, playing a role in "popularizing intelligent driving."

Financial data corroborates this trend: in 2025, total shipments of Horizon's in-vehicle Journey series chips exceeded 4 million units, up 38.8% year-on-year. Chips supporting mid- to high-tier intelligent assisted driving functions accounted for 45% of total shipments, nearly five times the share in 2024.

In contrast, the rollout of mid- to high-tier product lines, which determine technological ceilings and brand premiums, has proceeded more cautiously and has yet to establish a clear market advantage.

Image Source: Horizon Robotics Official Website Screenshot

More notably, performance in the second half of the year raised concerns. According to financial data analysis, revenue from product solutions—representing core chip hardware business—reached only RMB 840 million in H2, significantly below market expectations of RMB 1.05 billion. Shipments of mid- to high-tier intelligent driving chips (>80 TOPS) declined quarter-on-quarter from 990,000 units to 830,000 units, with their share dropping from 50% to 40%. Consequently, the average chip price stagnated at around RMB 390, well below the expected RMB 510.

Against this backdrop, the importance of Journey 7 has been further amplified. According to Horizon, this generation will adopt the fourth-generation BPU architecture "Riemann" and benchmark against Tesla's next-gen AI5 platform.

As reported by "Late Auto," the highest-performance version, J7P, aims to deliver computational power significantly surpassing NVIDIA's Thor-X, with mass production planned for 2027. From an industry perspective, this is not merely an iterative product but a critical node for Horizon to catch up or even partially benchmark against competitors in computational power generations.

However, competitors are moving swiftly: among automakers, NIO, XPeng, and Li Auto are accelerating their in-house chip rollouts, with NIO's self-developed Shenji NX9031 already exceeding 150,000 units in mass production. In the chip sector, NVIDIA followed Orin with Thor, further raising the computational power ceiling.

Meanwhile, Momenta, a leader in assisted driving, is expanding into chips through a partnership with Xinxin Hangtu, with mass production expected this year and design wins from SAIC Volkswagen and Beijing Hyundai already secured. Under this multi-layered pressure, the time window for Journey 7 is clearly narrow.

This means Horizon is not merely facing a simple product generation shift but a complex systemic challenge. On one hand, Journey 6 is still in the phase of sustained shipment growth and market validation, requiring stable supply and continuous optimization. On the other hand, Journey 7 must accelerate to meet the upcoming new round of computational power competition.

03. "Software-Hardware Integration": Blurring Role Boundaries

From a longer-term perspective, Horizon's transformation extends beyond products and organization; its role in the industry chain is also subtly shifting.

During the Journey 2 to Journey 5 era, Horizon functioned more like a typical intelligent driving chip vendor, entering automaker supply chains indirectly by providing computational power bases to Tier 1 suppliers and algorithm companies. At this stage, its core logic was to "build a platform," attracting partners to construct an ecosystem around it and thereby expanding shipment volumes and industry influence.

However, with the launch of Journey 6, this relatively restrained role began to be actively disrupted. Horizon not only introduced its self-developed intelligent driving solution HSD but also expanded outward through the HSD Together model, opening some algorithm capabilities and development frameworks to ecosystem partners.

Image Source: Horizon Robotics

Results-wise, this strategy significantly enhanced Horizon's influence over entire solutions, transitioning it from merely providing underlying computational power to participating in earlier stages like product definition, functional experience, and even vehicle integration. In other words, Horizon's role has clearly shifted toward becoming a provider of "software-hardware integrated" solutions.

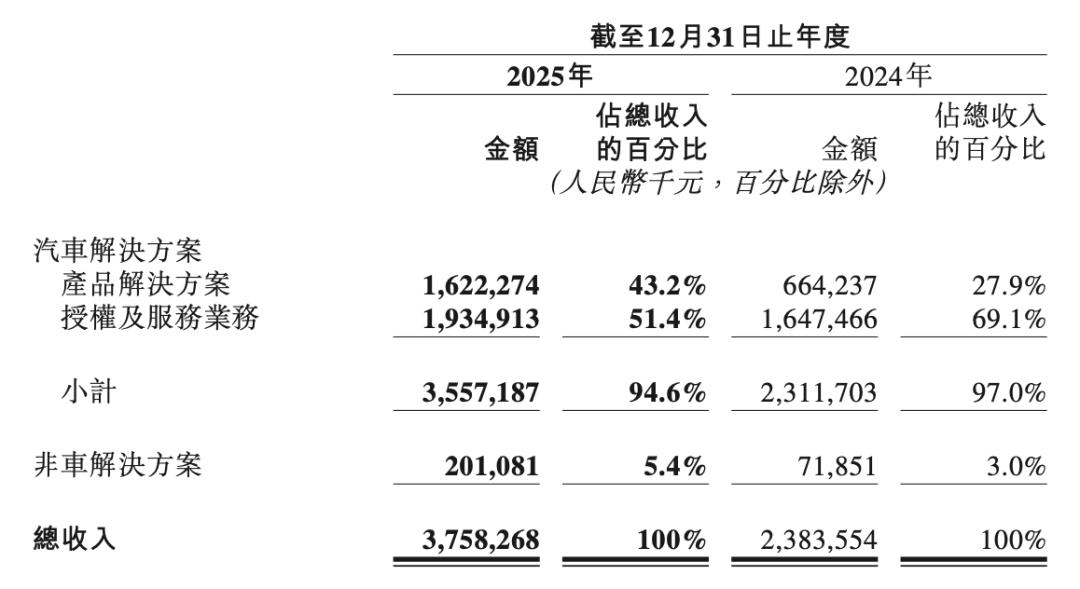

Changes in revenue structure within financial reports also corroborate this shift. In 2025, Horizon's product and solution revenue reached RMB 1.622 billion, up 144.2% year-on-year, with its share of total revenue rising from 27.9% in 2024 to 43.2%. Licensing and service revenue reached RMB 1.935 billion, up 17.4% year-on-year, accounting for 51.4%. These two business segments formed a relatively balanced revenue structure, enhancing risk resistance.

Image Source: Financial Report Screenshot

Behind this shift lies clear practical drivers. First, Huawei has established a strong presence in the high-end market with its full-stack capabilities, while Momenta continues to expand its design wins through algorithmic strengths and is extending into chips to further compress costs and enhance control. Second, urban assisted driving is accelerating its penetration into lower-priced models, with the sub-RMB 100,000 market becoming a new competitive focal point. Financial reports show that in 2025, vehicles priced below RMB 200,000 accounted for 65% of total passenger vehicle sales in China, with Horizon capturing a 44% share in this segment—ranking first in market share.

However, as the company simultaneously plays multiple roles—chip supplier, algorithm provider, and full-solution vendor—new challenges emerge.

For ecosystem partners, Horizon is both a platform and a potential competitor: on one hand, partners can leverage its chips and ecological resources to enter the market quickly; on the other hand, when Horizon itself develops solutions, overlaps with partners in clients and projects become inevitable. As the ecosystem grows, this "coopetition" relationship will become increasingly complex.

Going forward, Horizon's ability to balance strengthening its own solution capabilities with maintaining ecosystem partner trust will not merely be a strategic choice but will directly impact the stability of its ecosystem and whether this business model can truly succeed in the long term.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?