Hesai: Fear a Collapse in Unit Prices? The 'Abandoned by Tesla' Company Fights Back with Volume

03/26 2026

03/26 2026

488

488

Overall, Hesai Group released its Q4 2025 financial results after the market closed in Hong Kong on March 24 (Beijing Time). The results continued to reflect the typical characteristic of high shipment growth driven by 'price declines,' but the company managed to maintain its gross margin through solid cost control and provided optimistic shipment guidance for 2026. Here are the key details:

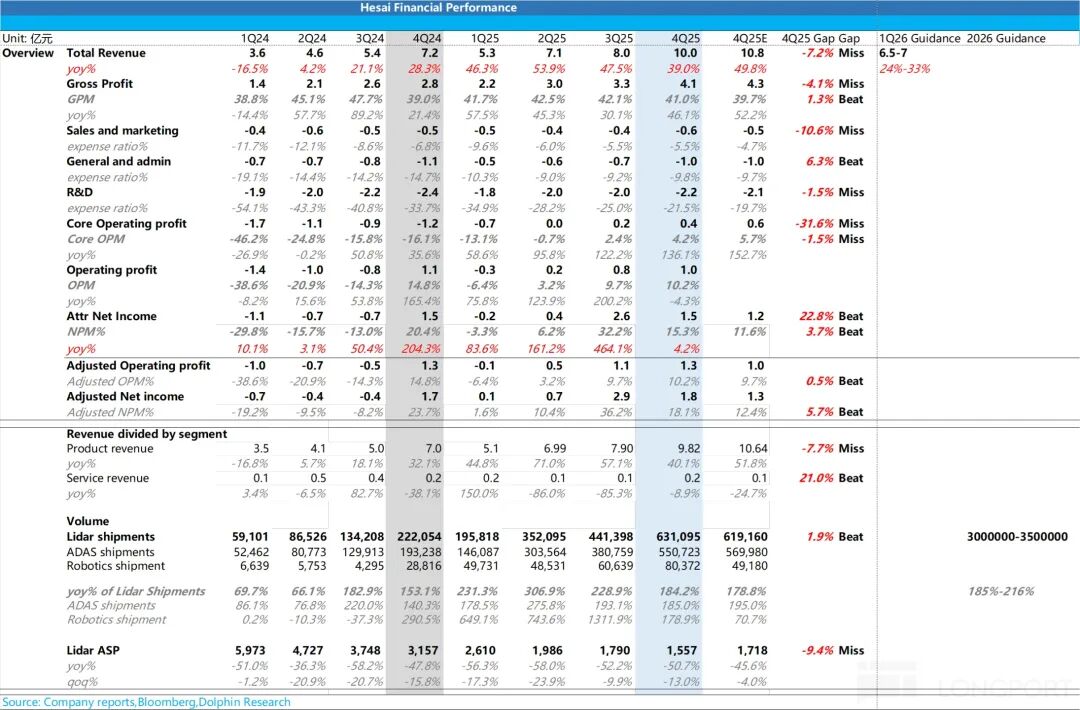

1) Revenue at the lower end of guidance, primarily due to lower-than-expected unit prices: Total revenue in Q4 was approximately RMB 1 billion, up 39% YoY, but below market expectations of RMB 1.08 billion and at the lower end of the previous revenue guidance range of RMB 1.0-1.2 billion. The core reason was the continued decline in LiDAR unit prices.

2) Shipment volume exceeded expectations again: Total LiDAR shipments in Q4 reached 631,000 units, up 184% YoY, surpassing both market expectations of 619,000 units and the company's previous guidance of 600,000 units. Breakdown:

a. Robot LiDAR shipments reached 80,000 units, significantly exceeding market expectations of 50,000 units, likely due to an increased proportion of lower-priced JT series shipments.

b. ADAS LiDAR shipments reached 550,000 units, up 185% YoY, primarily driven by accelerated adoption of the lower-priced 'sub-$1,000' ATX model. Management guided that ATX would account for 80% of total shipments in Q4.

3) But unit prices continued to decline sharply: The average selling price (ASP) of LiDAR in Q4 dropped to approximately RMB 1,557, down 51% YoY and 13% QoQ from RMB 1,790 in Q3, significantly below market expectations of RMB 1,718 (which anticipated a slight QoQ decline). This was the most direct reason for the revenue miss. Dolphin Research believes the continued ASP decline is mainly due to the following three factors:

a. Product mix shift: The proportion of lower-priced ATX models continued to rise (expected to increase from 70% in Q3 to 80% in Q4), with the 'sub-$1,000' ATX accelerating the replacement of the older, much more expensive AT128 model.

b. Pricing strategy: The market price of ATX products is around $200, and the company offered discounts to major customers in Q4, further driving down the average selling price.

c. Robotics business dragging down average prices: LiDAR shipments for robots surged in Q4, with a higher proportion of lower-priced JT series models, structurally lowering the overall average price.

4) Scaling effects and cost reductions from technology kept gross margin robust: Despite the pressure from rapidly declining unit prices, Hesai still achieved a gross margin of approximately 41% in Q4, higher than market expectations of 39.7% and the company's guidance of 40%. This was mainly due to:

a. Dilution of fixed manufacturing costs from surging shipment volumes: LiDAR sales reached 630,000 units in Q4, up 43% QoQ.

b. Effective cost reductions through a platform-based product line, application-specific integrated circuit (ASIC) design, and continuous optimization in the supply chain and manufacturing processes, offsetting the risk of price declines.

c. A rebound in high-margin service revenue.

5) Core profit slightly below expectations, but overall expense control remained solid:

GAAP net profit was RMB 150 million, at the upper end of the guidance range (RMB 70-170 million), mainly due to the recognition of interest income and other gains (totaling approximately RMB 120 million). Hesai received approximately $6.4 million (about RMB 45 million) in intellectual property arbitration compensation from Ouster in Q4.

After excluding these factors, core operating profit was approximately RMB 40 million (gross profit - core three expenses), slightly below expectations of RMB 60 million, mainly due to a QoQ increase in R&D and sales expenses. However, overall, the company's expense control remained robust (solid and reasonable).

Dolphin Research's Core View:

Overall, Hesai continued to demonstrate the logic of 'volume growth with price declines' driven by technology-enabled cost reductions and accelerated penetration this quarter. Although Q4 revenue was somewhat lackluster due to the continued decline in LiDAR ASPs, the company successfully maintained a high gross margin of over 40% through excellent cost control and scaling effects.

Looking ahead to 2026, Hesai significantly raised its shipment guidance, further underscoring the logic of 'technological democratization' and accelerated penetration of LiDAR in the automotive industry:

a. Strong full-year shipment guidance with extremely robust order backlog: The company raised its full-year 2026 shipment guidance to 3.0-3.5 million units (from the original 2.0-3.0 million units), representing continued YoY growth of 85%-116%, far exceeding market expectations of 2.66 million units. To meet surging demand, the company plans to double its annual production capacity from 2.0 million units in 2025 to over 4.0 million units in 2026.

ADAS Business: The company has secured all orders from China's top 10 OEMs, covering over 40 brands and more than 160 models. The order backlog for the revamped ATX model has exceeded 6.0 million units (expected to start SOP in April 2026, equipped with the self-developed FMC500 SOC chip), demonstrating strong scalability. Hesai guided that ADAS business shipments are expected to double (2.77 million units).

Robotics Business: The JT series shipped over 200,000 units in its first year, with intention (tentative) orders from leading brands like Dreame and Mova for lawn mowing robots reaching the ten-million-unit level. Additionally, it achieved nearly full coverage in the Robotaxi/Robovan sector. Robotics LiDAR shipments are also expected to double YoY (480,000 units).

b. Q1 off-season remains strong, with product mix optimization supporting ASP stabilization:

The 2026 Q1 net revenue guidance is set at RMB 650-700 million, up 24%-33% YoY. Considering Q1 is typically a slow season for the automotive industry (historically accounting for about 12% of annual shipments), shipments in Q1 2026 are expected to be around 400,000-450,000 units.

Dolphin Research expects that while the price of the core ATX model will continue to decline from around $200 in 2025 to $150 in 2026 (down about 25% YoY), the comprehensive ASP in Q1 is expected to be RMB 1,548, roughly flat QoQ with RMB 1,557 in Q4.

This is mainly due to an improved shipment mix: ADAS LiDAR shipments will slow down in Q1, while shipments of high-end robotics LiDAR, which has higher prices and gross margins, are expected to reach about 100,000 units, accounting for 22%-25% (a significant QoQ increase of 13 percentage points), providing a good hedge.

Dolphin Research believes Hesai is a high-conviction stock that continues to benefit from 'rising penetration of intelligent driving' and 'expansion into the second-growth curve of robotics' at the fundamental level:

① Solid leadership in the passenger vehicle sector with a clear competitive landscape

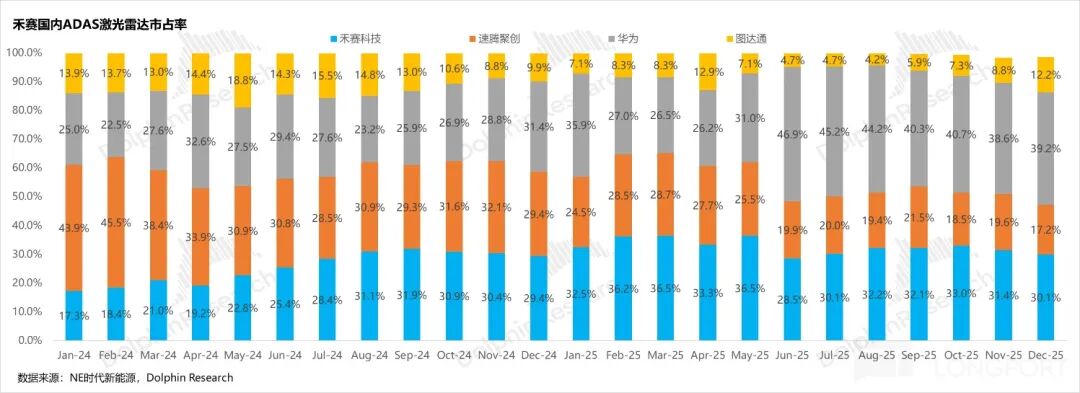

In terms of market share, although Hesai's share has fluctuated since June last year due to Huawei's ramp-up of short-range LiDAR shipments, Huawei's LiDAR is primarily sold as part of a hardware-software integration package at higher prices, serving the Smart Selection and HI mode ecosystems.

Therefore, in the independent third-party Tier 1 market, the actual competition remains focused among Hesai, RoboSense, and Innovusion. Currently, Hesai leads the market with strong shipments of the low-priced ATX model, capturing a 31.3% market share in passenger vehicle LiDAR in Q4, nearly 13 percentage points ahead of second-placed RoboSense, maintaining its industry-leading position.

② 2026 guidance vastly exceeds expectations, dispelling concerns over 'customer loss,' with the 'volume growth with price declines' logic continuing to play out

Previously, the market was concerned about slowing growth in Hesai's ADAS LiDAR business in 2026 (even raising fears of losing major customer orders). The significantly raised guidance to 3.0-3.5 million units has completely dispelled these market doubts. The massive increase primarily comes from four dimensions:

1) ATX enters the 'sub-$1,000' era, continuing to penetrate the lower-end market:

Models like the Changan Qiyuan Q05 and Leapmotor A10 have become the first sub-RMB 100,000 vehicles equipped with LiDAR. Dolphin Research expects LiDAR adoption to accelerate in vehicles priced below RMB 100,000 in H1 2026.

Breaking down by customer, Dolphin Research expects the core growth in 2026 to be driven by large orders from Xiaomi (sole supplier for ~550,000 units), Leapmotor (near-exclusive supplier for ~600,000 units), Li Auto (sole supplier for ~450,000-500,000 units), BYD (~300,000-350,000 units, accounting for half), Geely (~500,000 units), and Great Wall (~200,000 units).

2) L3 advanced intelligent driving drives a multiple increase in per-vehicle LiDAR adoption:

Dolphin Research expects the implementation of L3 autonomous driving regulations in 2026 to be a significant catalyst. L3 perception requirements will double, with per-vehicle solutions upgrading from a single main LiDAR in L2 to '1 main LiDAR (ATX/ETX) + multiple short-range LiDARs (FTX).' This will not only drive per-vehicle value up from about $200 to $500-$1,000 but also increase customer price tolerance for LiDAR due to high L3 usage frequency.

3) Overseas market breakthroughs, empowered by the NVIDIA ecosystem:

Hesai has completed development of long-range LiDAR C-samples for a leading European automaker, with overseas mass production expected to begin by the end of 2026.

Meanwhile, the NVIDIA Drive Hyperion full-stack platform (covering hardware, software, and pre-trained AI models) has significantly improved the integration efficiency of Hesai's products, aiding rapid expansion among overseas OEMs. Given overseas customers' lower price sensitivity and preference for high-end products, overseas expansion will be a key tool to hedge against domestic ASP declines.

4) Robotics sector becomes the second growth curve, with Hesai remaining the Robotaxi leader:

The potential TAM in robotics is twice that of autonomous driving, and robotics LiDAR ASPs and profit margins are generally higher than ADAS products, making it a core factor enabling Hesai to hedge against passenger vehicle LiDAR price pressures and maintain overall high profitability.

Strong orders in consumer/service robots: Leveraging products like the JT series designed for micro and high-performance scenarios, Hesai has signed exclusive supply agreements with Dreame and its subsidiary Mova for lawn mowing robots, with an order backlog exceeding 10 million units, demonstrating strong shipment momentum in this sector.

Robotaxi/Robovan leadership remains unchallenged: In the L4 autonomous driving market, Hesai remains the dominant player.

The company holds a 60%-70% absolute share in the global Robotaxi market, with supply agreements with top autonomous driving companies in North America, Asia, and Europe.

It has also established leadership in the autonomous urban delivery vehicle (Robovan) sector—ranking first in GGII's LiDAR fixed point rankings and being the sole exclusive LiDAR supplier for multiple global leaders like Neolix and DoorDash.

Regarding unit prices, Dolphin Research expects LiDAR ASPs to continue declining by about 21% YoY to RMB 1,460 in 2026:

This is mainly due to the increasing proportion of low-priced ADAS shipments (e.g., ATX declining to about $150, down 25% YoY), volume-based discounts for major customers, and annual price reduction requests from automakers. However, this will be partially offset by the implementation of L3 multi-LiDAR solutions, the ramp-up of high-priced ETX shipments, the onboarding of high-margin overseas orders, and the high-profitability robotics business.

Despite continued ASP declines, Hesai still expects its overall business gross margin to remain resilient in 2026, primarily due to technology-enabled cost reductions + scaling effects:

a. Localization and high integration of main control chips (the self-developed FMC500 SOC chip, based on RISC-V architecture, highly integrates MCU, FPGA, and ADC, significantly reducing core chip costs, which account for 40% of BOM).

b. Self-developed SPAD integration technology (mass production in 2026).

c. Extreme scaling effects (3.0-3.5 million units diluting fixed costs) and highly automated manufacturing.

On the expense side:

The company expects overall operating expenses to grow in the mid-double digits, primarily due to proactive investment of about $200 million in R&D to develop cutting-edge new products for perception ('eyes') and execution ('muscles') endpoints.

Excluding new business expenses, core operating expenses for the main business are expected to remain flat or decline by a low single-digit percentage. This still stems from Hesai's strong cost control capabilities + operating leverage release + deep application of AI in internal operations (already delivering tens of millions of yuan in quantifiable cost savings).

A more detailed value analysis has been published in the same name (same-titled) article in the「Dynamic - In-Depth (Research)」section of the Longbridge App.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated entities. It does not consider the specific investment objectives, product preferences, risk tolerance, financial situation, or unique needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information mentioned or the opinions expressed in this report shall not be considered or deemed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor shall it constitute advice, solicitation, or recommendation regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or for use by, any person or entity in any jurisdiction or country where such distribution, publication, availability, or use would be contrary to applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliates to any registration or licensing requirements in such jurisdiction.

This report solely reflects the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?