Leapmotor Recaptures March Sales Throne, Triggering a Reshuffle in New Energy Automaker Rankings

04/03 2026

04/03 2026

458

458

The ultimate victor in this race remains to be seen.

While April 1st marks April Fools' Day in the digital era, none of the new energy automakers dared to indulge in frivolous antics. Their sales posters showcased authentic data, leaving no margin for error.

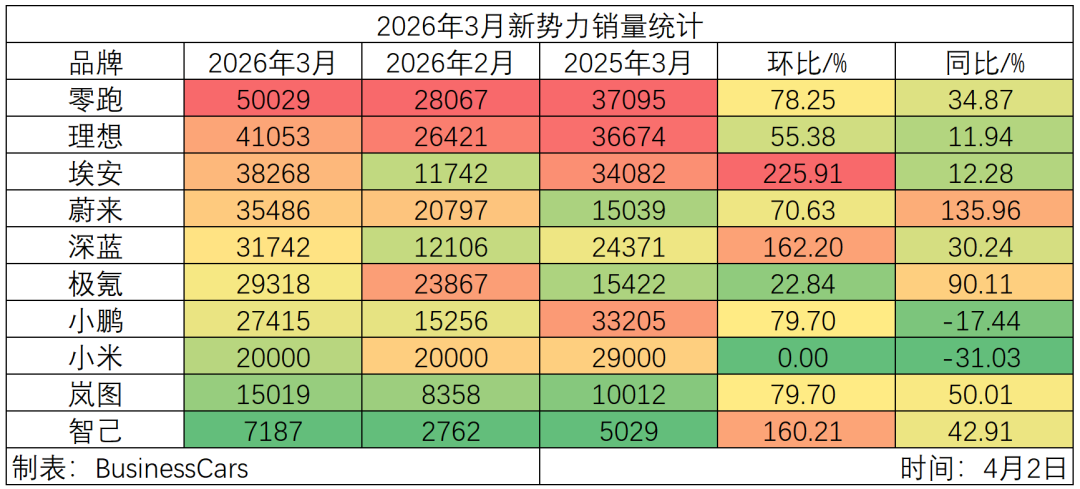

With March sales figures now public, new energy automakers have demonstrated a significant rebound, shaking off the earlier performance slump. The industry is no longer trapped in the lethargy of January and February.

As sales recover, the performance gap among new energy automakers has widened dramatically. After a decade of fierce competition, leading players are now achieving monthly sales of 50,000 units, while those at the bottom struggle to reach 10,000. Inevitably, some are falling behind in the pursuit of shared success.

More notably, certain brands opted not to release sales posters at the start of the month, leaving ambiguity as to whether this was a strategic withdrawal from intense competition or a sign of lacking confidence in facing reality.

Extended-range technology emerges as the frontrunner among new energy automakers

In the published sales rankings, extended-range hybrid technology—once a subject of criticism—has now become the preferred choice for new energy automakers. Unlike traditional automakers, which have invested in engines for decades, new entrants in the new energy era have found extended-range models to be the most reliable path, free from supply chain constraints.

The top three brands in March sales all leveraged extended-range products to capture market share. Leapmotor, projected to lead new energy automakers in sales by 2025, rebounded after a brief February slowdown to surpass 50,000 units in March, cementing its leading position. This achievement aligns with Leapmotor's philosophy of offering "high-quality yet affordable" vehicles.

While luxury new energy vehicles priced at 300,000 yuan may attract envy, the mainstream market—vehicles under 200,000 yuan—remains the primary driver of automotive consumption. Sustaining sales growth requires dominance in this segment.

Leapmotor clearly understands its core market. In March, it unveiled the A10, the first model in its A-series, with a starting price of 65,800 yuan. This launch reaffirmed Leapmotor's commitment to affordable mobility. Even the top-spec variant, equipped with LiDAR and advanced driver-assistance systems, costs just 86,800 yuan, making intelligent driving technology accessible to a broader audience.

While Leapmotor offers four product series (A, B, C, D), its current focus remains on the A, B, and C series, all priced under 200,000 yuan and targeting the mainstream market. Only the upcoming D19 aims to break into the premium segment.

Leapmotor also balances present and future demands by offering both battery electric and extended-range models, empowering consumers with choice. This strategy enabled it to surpass Li Auto, widely regarded as the pioneer of extended-range technology in China.

Leapmotor's cost advantage stems from its highly self-reliant supply chain. By controlling key components in-house, it has effectively managed production costs. As economies of scale take effect, profitability has followed. In 2025, Leapmotor achieved its first annual profit, a milestone for any new energy automaker.

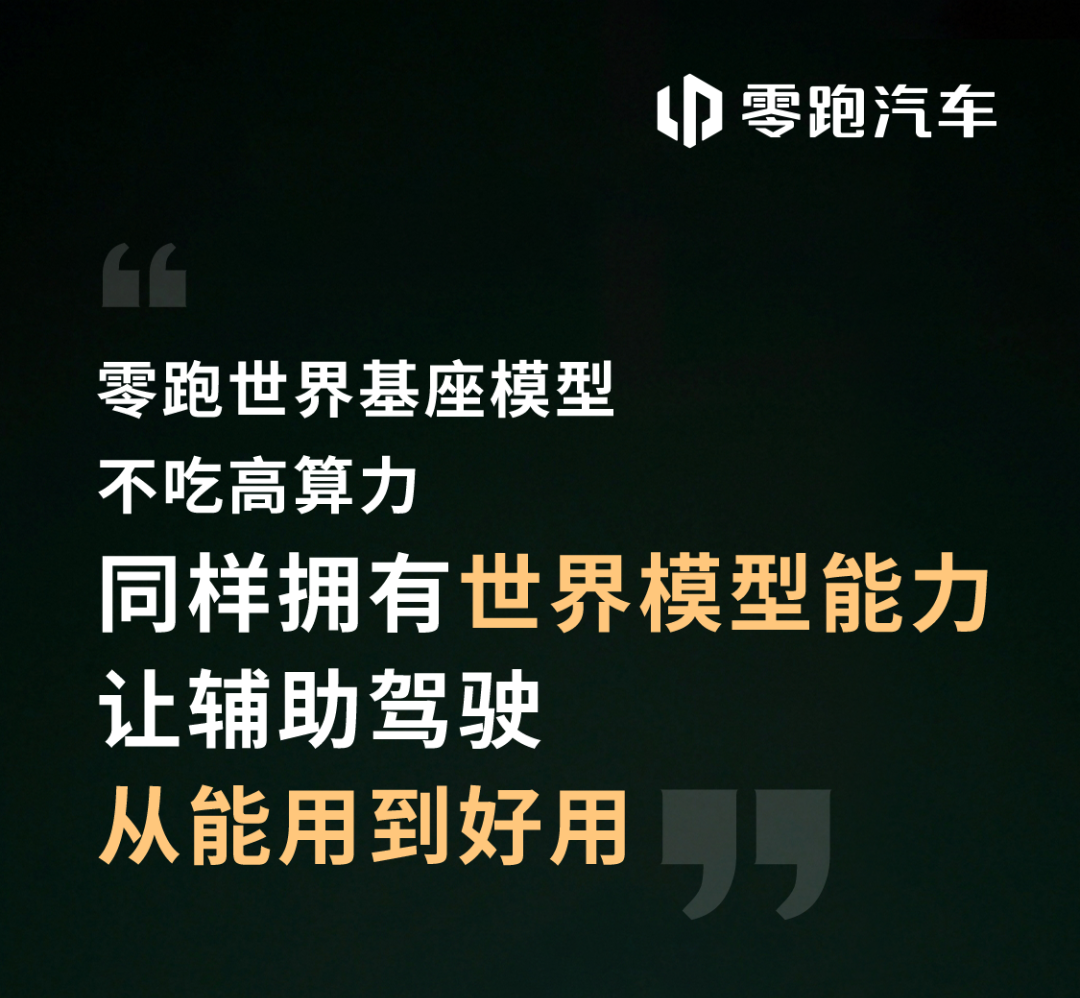

At the A10's launch event, Leapmotor showcased its commitment to self-reliance by unveiling a proprietary world model, elevating its previously criticized intelligent driving capabilities to industry-leading levels. This innovation underpins Leapmotor's ability to offer advanced driver-assistance systems in an 80,000-yuan vehicle—a feat considering that such systems typically cost as much as half an A10 in mainstream models.

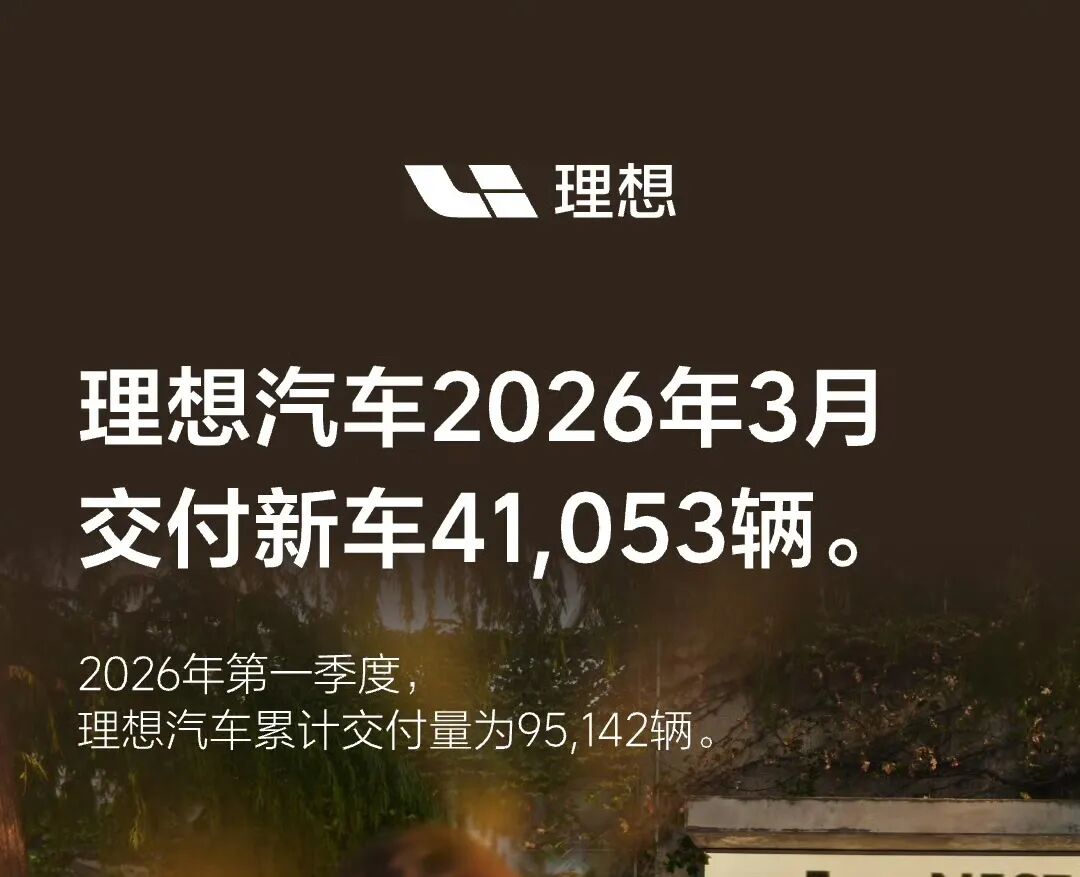

The second-place finisher in March sales was somewhat unexpected yet unsurprising. Li Auto outperformed Nio and XPeng, reclaiming its position among the top new energy automakers with 41,053 units sold.

Li Auto's sales had been lackluster in the fourth quarter of 2025 and early 2026, even affecting the "Nio-XPeng-Li Auto" trio's standing. However, as the first profitable new energy automaker, Li Auto remained confident. After extensive reforms led by founder Li Xiang, its sales rebounded sharply, with significant year-over-year and month-over-month growth. This indicated a solid step forward in transitioning from extended-range to extended-range + battery electric models.

Li Auto's slump had been attributed to slow product refreshes and insufficient battery electric production capacity. Both issues now appear resolved, with i6 production normalized and the L-series remaining competitive.

A refreshed Li Auto L9 is on the horizon, featuring proprietary chips as a key differentiator that will strengthen its competitive edge in the AI era.

Aion, ranking third, finally emerged from its slump. While its sales tally includes those of its premium brand Hyper, Aion's own performance has clearly improved.

The driving force behind this recovery is the reformulated i60 model. According to official data, 11,145 i60 units were delivered in March, accounting for nearly 30% of total sales—equivalent to an entire brand's February sales.

The successful i60 is Aion's first extended-range model. Having transitioned from a battery electric sales leader to embracing extended-range technology, Aion's shift reflects not just a technical change but a market-driven realignment. Technologies validated by the market are truly superior.

Seeking Comfort Zones

Among mid-tier players, only Zeekr fell slightly short of 30,000 monthly sales, while the other two regained momentum, surpassing that threshold.

Nio, for instance, defied the February downturn experienced by other new energy automakers, maintaining upward sales momentum. While its portfolio includes lower-priced brands like Onvo and Firefly, Nio's high-end market positioning remains intact.

Official data reveals that 16,255 ES8 units were delivered in March, accounting for half of Nio's sales and cementing its status as a flagship model. This success indicates that Nio has found its comfort zone in the large battery electric SUV segment. According to online reports, the Nio ES9 is set to launch soon, further expanding its presence in this space.

The ES8's success is no accident. By combining luxury, battery electric technology, and SUV practicality, Nio has translated a decade of market exploration into product success. Its battery-swapping infrastructure, once a liability, now proves advantageous for large SUVs.

The inclusion of "luxury" is warranted due to the underperformance of Onvo. While the Onvo L90 initially generated buzz, its sales have since plateaued. Combined, Onvo's two models barely exceed 6,000 units monthly, underscoring the need for Onvo to carve out its own niche rather than serving as a cheaper Nio alternative.

Shenlan Automotive saw a significant sales rebound in March, not only surpassing 30,000 units but also climbing the rankings.

However, Shenlan's February sales data differed markedly from previously disclosed figures. Its official poster claimed an 87.8% month-over-month global sales increase in March, implying February sales of 16,000 units. Yet domestic production and sales data reported just 12,106 units, suggesting a 4,000-unit discrepancy attributable to overseas sales.

Consistency in sales reporting is crucial to avoid misunderstandings from third-party data analyses.

Shenlan's sales were primarily driven by the S05 compact model, which sold 17,586 units in March (including 3,517 overseas units). This indicates that Shenlan has found its direction amid a diverse model lineup.

The highly anticipated L06 saw a 170% month-over-month sales increase, according to Shenlan, though no specific figures were provided. Equipped with magnetorheological technology, this model needs stronger sales performance to validate its innovation.

More critically, as Huawei's ecosystem expands through partnerships like Harmony Intelligent Mobility and Huawei ADS, Shenlan must define its unique position within this ecosystem. Since adopting the ADS SE system, it has yet to see a substantial sales boost from intelligent driving-equipped models, leaving many challenges unresolved.

In March, Shenlan celebrated the production of its one-millionth electric drivetrain, highlighting its self-reliance in core technologies. However, these innovations must translate into market success through compelling products—a goal Shenlan has yet to fully achieve.

Zeekr, though falling just short of 30,000 monthly sales, appears to be on the right track. The launch of the 9X has bolstered its position, proving that high-end new energy vehicles require complementary mainstream offerings.

Previously, Zeekr's experiments yielded few truly premium products aside from the 400,000-yuan-plus Zeekr 009. The niche MPV market limited Zeekr's ability to compete at the high end, but the 9X fills this gap.

While the 9X dilutes Zeekr's pure battery electric identity, its luxury features distinguish it from sibling brands like Lynk & Co. By embracing extended-range technology, Zeekr has discovered a new path after a prolonged period of stagnation.

Zeekr's pre-sales of the 8X in March signal further ambitions in the large luxury battery electric SUV market. Equipped with multiple technologies, this model promises strong competitiveness, pending a surprisingly attractive launch price.

Meanwhile, Zeekr continues refreshing its product lineup, including the Zeekr 007. Though delayed, this move demonstrates Zeekr's commitment to its other series.

Striving to Stay in the Game

Rear-guard new energy automakers face unique challenges. XPeng and Xiaomi, both starting with "Xiao" (a term often associated with "small" or "young" in Chinese, but here likely coincidental), are the only brands experiencing year-over-year sales declines amid broader market growth—a clear sign of trouble.

XPeng, despite selling 27,000 units, lags significantly behind peers. More critically, its attempts to explore lower-priced segments and extended-range technology have yet to yield a stable advantage.

Now, XPeng is pinning its hopes on second-generation Vision-Language-Action (VLA) technology for a comeback. At the MONA M03 launch on April 2, XPeng rolled out its Turing chip, but only the top-spec Ultra SE variant offers the full-fledged VLA 2.0 system. The MAX version, delayed until the second half of the year, will feature a distilled version.

XPeng aims to establish intelligent driving as its competitive moat while maintaining price differentiation across models. This strategy results in the MONA M03's awkward six-variant lineup, attempting to balance affordability with profitability.

Xiaomi, meanwhile, sold over 20,000 units in March and unusually disclosed sales of its next-generation SU7: over 7,000 units delivered in less than two weeks, surpassing the original SU7's six-month delivery pace in 2024.

Lei Jun's claim that the new SU7 outperforms its predecessor holds merit.

However, Xiaomi's March sales raise questions about its future. Previously, its sales were constrained by production capacity, which lagged far behind orders. Monthly sales figures reflected this slow ramp-up.

The sudden sales dip suggests Xiaomi may have exhausted its order backlog.

Factoring out production constraints, March sales indicate that Xiaomi's initial hype has faded. The availability of "limited" inventory on its app further suggests that production now exceeds demand.

While Xiaomi officially describes its inventory as "limited," only the company knows the true extent of excess capacity.

Online reports claim that two Tesla China executives have joined Xiaomi Automotive: Kong Yan, former Tesla China general manager, will oversee sales, while Song Gang, former vice president of manufacturing at Tesla's Shanghai plant, will lead production. Xiaomi has not confirmed this, leaving the reports unofficial.

After market turbulence in 2026, some new energy automakers have abandoned monthly sales posters. Currently, only Voyah and Zhiji persist in releasing them despite monthly sales below 20,000 units.

VOYAH sold 15,000 vehicles in March, showing strong year-over-year and month-over-month growth. It has steadily kept pace with the advancing wave of new energy vehicles, and its persistent dedication proves that its efforts have not been in vain.

As for IM Motors, facing the reality of 7,187 units sold is commendable, but amid the constant release of new models, IM Motors needs to reflect on why it's struggling to achieve rapid sales breakthroughs. After managing to sustain monthly sales exceeding 10,000 units in 2025, why did this momentum suddenly collapse?

From a product strength perspective, IM Motors lacks nothing. Backed by SAIC, it possesses robust R&D capabilities, complemented by technologies from Alibaba and Momenta, placing it at the forefront of the industry.

If the product is not the issue, then the problem must lie in marketing or other areas. IM Motors needs to conduct an internal review to identify and address these internal challenges promptly.

Only through diligent efforts can new energy vehicle startups maintain their position in the market.

Note: The image is sourced from the internet. In case of any infringement, please contact us for its removal.

-END-

-

![]()

Chip Market Booms as AI Hardware Goes Mainstream

-

![]()

【Jialichuang】Participates in the 'OFweek 2026 China Intelligent Manufacturing Industry Annual Awards'

-

![]()

Car Companies Unite in 'Humanoid Creation': The Embodied AI Revolution Transforming the Automotive Industry

-

![]()

XREAL, a Realist in the Smart Glasses Space

-

![]()

68% Surge in Market Enthusiasm: The Game Behind Cerebras' Rise to Fame and the AI Chip Race

-

![]()

The Boom of Short Drama Going Global: In the 3.6 Billion Market, Only a Few Are Truly Making Money

-

![]()

Alibaba AI: Flourishing Amidst Challenges

-

![]()

Surge of Short Drama Exports: Only a Few Truly Profit in the $3.6 Billion Market