In-depth Observation of China's Auto Market in Q1 2026: Domestic Sales Decline, Exports Surge, and New Energy Vehicle Prices Rise

04/14 2026

04/14 2026

565

565

The spring of 2026 marked an extremely complex and Tearing sensation (conflicting) quarter for China's automotive industry. Looking at the production and sales data for the first quarter, beneath the seemingly moderate macro-level decline lay intense structural differentiation between the domestic and overseas markets, traditional fuel and new energy vehicles, and low-end commuter and mid-to-high-end improvement-driven demand.

In summary, China's auto market in the first quarter of 2026 exhibited three core characteristics: the 'two extremes' of a domestic market slowdown and an overseas market boom, and the comprehensive dominance of new energy vehicles in the B-segment and high-end markets priced above 250,000 yuan.

These characteristics may very well define China's auto market throughout 2026.

I. Overall Performance of China's Auto Industry in Q1 2026: Significant Month-on-Month Recovery, Year-on-Year Decline

From a macro perspective, the conclusions predicted in the previous article 'Morgan Stanley's 2026 China Auto Market Forecast: When 'Growth Inertia' Fails, How Can We Navigate the Cycle?' were confirmed. In the first quarter, China's automotive industry faced certain pressures on overall volume.

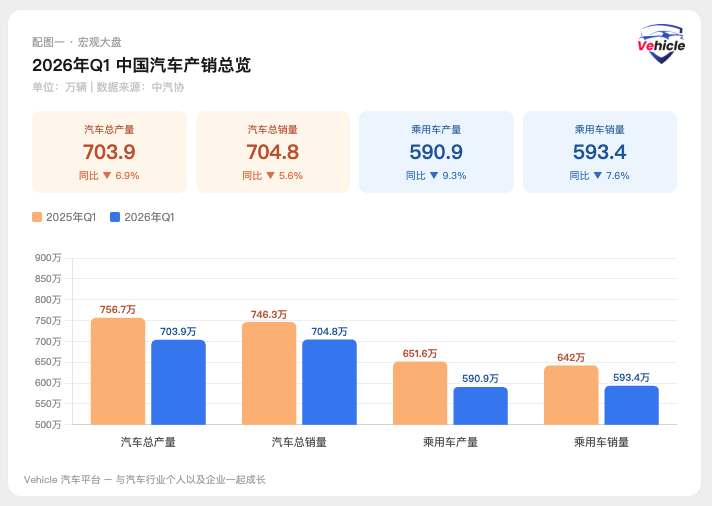

Total Auto Market (including domestic passenger vehicles, exports, and commercial vehicles mentioned below): In the first quarter, auto production and sales reached 7.039 million and 7.048 million units, respectively, down 6.9% and 5.6% year-on-year. The overall market showed a year-on-year decline.

Passenger Vehicle Market: Production and sales of passenger vehicles in the first quarter were 5.909 million and 5.934 million units, respectively, down 9.3% and 7.6% year-on-year.

Interpretation: Both total production and sales declined year-on-year compared to the same period last year, with passenger vehicles experiencing a greater decline.

Although the first quarter saw an overall year-on-year decline, after the sluggishness at the beginning of the year, production and sales data for March alone showed a significant month-on-month recovery. These fluctuations in macro data indicate that the domestic and overseas markets are heading toward two distinct growth trajectories.

II. Domestic Passenger Vehicle Market: Significant Decline in Domestic Sales, but Structural Upgrade Toward New Energy and High-End Markets Continues

Combining data released by the China Association of Automobile Manufacturers (CAAM) for the first quarter of 2026, the conclusion that 'domestic sales have significantly declined, but the structure continues to upgrade toward new energy and high-end markets' has been precisely and profoundly validated. This reflects that the domestic automotive consumption landscape is undergoing a fierce 'breakthrough and reshaping.'

1. Overall Domestic Sales Under Pressure, Traditional Fuel Vehicles Hit Hard

The domestic auto market is facing severe Stock game (market competition for existing shares), with the overall decline primarily driven by the sharp contraction of traditional fuel vehicles.

Significant Shrinkage of the Domestic Base: From January to March, domestic sales of passenger vehicles were only 4.013 million units, a year-on-year drop of 23.4%. Under the dual pressures of price wars and consumer hesitancy, the incremental space for domestic automotive consumption has been severely squeezed.

Fuel Vehicles Lose Momentum: Domestic sales of traditional fuel passenger vehicles reached 2.192 million units, a sharp decrease of 565,000 units year-on-year, down 20.5%.

2. Structural Upgrade: Farewell to 'Low-End Commuting,' New Energy Vehicles Leap into Mainstream and High-End Markets

Against the backdrop of an overall market decline, the market structure has not collapsed across the board but has instead shown a clear shift toward 'higher value.' In the past, new energy vehicles were often labeled as 'ride-hailing vehicles' or 'cheap commuting options,' but the first-quarter data has completely reversed this perception:

Model Segment Upgrade: B-Segment Vehicles Become the New Engine: Affected by policy adjustments and upgrading consumer demand, the once-dominant A00-segment (microcars) has receded. The main sales force for new energy passenger vehicles has firmly shifted to the B-segment market (cumulative sales of 849,000 units in the first quarter, up 8.1% year-on-year despite the overall downturn). In contrast, traditional fuel vehicles remain stuck in the A-segment market (down 6% year-on-year). This indicates that new energy vehicles have successfully broken through into the mainstream family upgrade and business travel markets, achieving a structural leap in product segments.

Price Segment Upgrade: Seizing 'High-End Pricing Power': In the largest base segment of 100,000-150,000 yuan, traditional fuel vehicle sales reached 1.014 million units, down 6.1% year-on-year; while new energy vehicles in this segment reached 617,000 units, up 6.8% year-on-year, accelerating the encroachment on the fuel vehicle base. More disruptively, in the high-end segment above 250,000 yuan, traditional fuel vehicles (especially luxury joint-venture brands) have suffered widespread defeats, with significant declines of 35.5% and 41.8% in the 300,000-350,000 yuan and 350,000-400,000 yuan segments, respectively. In contrast, new energy passenger vehicles have shown double-digit or even nearly doubled explosive growth in the ultra-high-end segments of 350,000-400,000 yuan (+19.9%), 400,000-500,000 yuan (+32.0%), and even above 500,000 yuan (+80.6%).

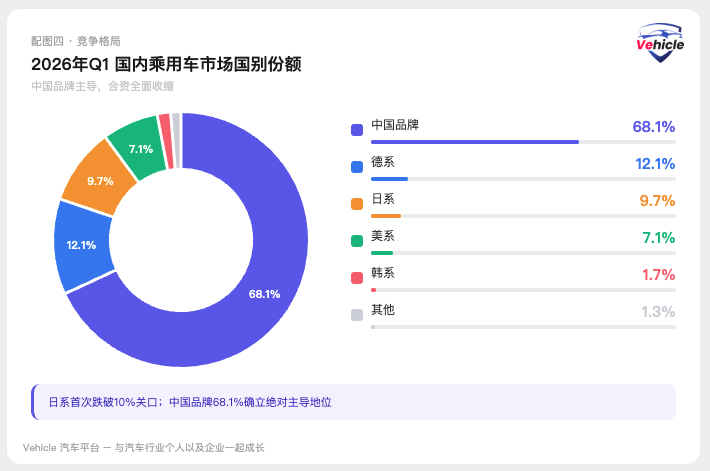

3. Competitive Landscape: Chinese Brands Establish Absolute Dominance, Joint Venture Defenses Fully Contract

Amid intense market competition, Chinese brands have fully established their risk resistance capabilities. The latest market share positions of vehicle nationalities are clearly visible from the long-term trend chart for the first quarter:

Chinese Brands Dominate Absolutely, Accounting for 68.1%.

German Brands Account for 12.1% (Ranking First Among Joint Ventures but Showing a Long-Term Gradual Decline).

Japanese Brands Account for 9.7% (Officially Falling Below the 10% Threshold, with a Clear Declining Trend).

American Brands Account for 7.1%.

Korean and Other Brands Are Further Marginalized, Accounting for Only 1.7% and 1.3%, Respectively.

III. China's Auto Export Situation: Maintaining Rapid Growth, Breaking Through from 'Cost-Effectiveness' to 'Technological Premium'

In contrast to the intense competition and double-digit decline in the domestic market, overseas markets have become the core engine driving growth in China's automotive industry, with new energy vehicles (especially models with intelligent advantages) experiencing explosive growth overseas.

1. Export Volume and Power Structure Soar Together

Maintaining Rapid Growth: In the first quarter, cumulative auto exports reached 2.226 million units, up 56.7% year-on-year. March alone saw extremely strong performance, with exports reaching 875,000 units, achieving significant year-on-year and month-on-month growth (+72.7% year-on-year, +30.2% month-on-month), setting a recent single-month high.

New Energy Exports Double: In the first quarter, cumulative exports of new energy vehicles reached 954,000 units, up 1.2 times (over 100%) year-on-year; March alone saw exports of 371,000 units, up 1.3 times year-on-year. Meanwhile, traditional fuel vehicles remain the absolute mainstay of exports (1.271 million units in the first quarter) but also maintained robust positive growth of 29.9%.

2. Intelligence Spillover Reshapes Overseas Competitiveness

'Go Global or Go Out of Business' has become an industry axiom. Accelerating overseas channel expansion and localized production capacity building is not only about seeking incremental growth but also a critical lifeline for digesting domestic excess capacity and balancing financial profits. The over 1.2 times surge in new energy exports indicates a fundamental shift in the logic of China's auto exports: In the past, reliance on 'low prices and cost-effectiveness' to sell fuel vehicles; now, reliance on 'three-electric systems, intelligent cockpits, and advanced autonomous driving' to sell new energy vehicles. The rapid iteration of Chinese automakers in end-to-end (E2E) algorithms, perception large models, and other intelligent driving technologies is gradually becoming a core selling point in overseas markets, especially high-potential markets (such as Europe and the Middle East).

3. Differentiated Strategies Among Automakers in Overseas Expansion

The leading export echelon (echelon) achieved overall positive growth in the first quarter, but strategies varied among companies:

Chery Remains the 'Top Player,' with cumulative exports of 391,000 units in the first quarter (accounting for 17.6%, up 54.4% year-on-year). Having deep cultivation (cultivated) overseas markets for years, Chery has established deep channel moats by balancing fuel and new energy vehicles in emerging markets.

BYD Follows Closely (321,000 units), leveraging its strong vertical integration capabilities across the entire supply chain and rapidly replicating its global footprint with a fleet of ro-ro ships.

SAIC (299,000 units), Geely (255,000 units), and Changan (213,000 units) rank third to fifth.

Great Wall Motor Performs Steadily, ranking sixth with 130,000 units. Relying on its long-standing overseas reputation, it accelerates the rollout of hybrid/electric product lines in core strategic markets, transitioning from 'product exports' to 'ecosystem exports.'

Tesla's export growth is the most eye-catching (101,000 units, up 1.6 times year-on-year), indirectly reflecting the irreplaceability of China's supply chain manufacturing efficiency in the global system.

Conclusion

The first-quarter data for 2026 serves as a mirror, reflecting the pain and hope of China's automotive industry as it navigates through cycles. Comprehensive data shows that the domestic auto market is undergoing a 'painful transformation.' The cliff-like decline in sales eliminates outdated production capacity and uncompetitive traditional fuel products; while the growth against the trend is seen in intelligent, B-segment and above, and mid-to-high-end new energy models priced above 250,000 yuan.

The competitive logic of China's auto market has officially transitioned from 'competing on scale and price' to 'competing on value and technology.' The red ocean of intense competition in the domestic market will not end in the short term, and the shift from 'price wars' to 'value wars' will become even more brutal.

'Go Global or Go Out of Business' is no longer just a slogan but a survival axiom; while 'no intelligence, no high-end positioning, no profitability' is the lifeline for the second half of the new energy era. In this round of reshuffling, only automakers that produce intelligent products and possess a global strategic mindset can navigate through cycles and win the overall game in the coming quarters.

References and Images

Industry Operations | Auto Industry Production and Sales in March 2026 - China Association of Automobile Manufacturers

*Unauthorized reproduction or excerpting is strictly prohibited-

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’