Charging Pile Fees Surge, with Scarce 0.5 Yuan/kWh ‘Bargain’ Options Left

04/20 2026

04/20 2026

643

643

Lead

Introduction

The tug-of-war between EV owners and charging operators leaves no clear winner.

Following successive fuel price hikes, many new energy vehicle (NEV) owners have noticed a corresponding rise in charging pile fees. A Beijing-based owner reported that previously, a full charge costing around 50 yuan could cover over 400 kilometers. Now, during peak hours, the price per kWh has increased by nearly 0.5 yuan, making a full charge cost over 80 yuan. Some have bluntly stated, “The cost advantage of electric vehicles is barely holding up.”

However, investigations reveal significant regional variations in price increases at charging stations. In Shanghai, most shopping malls and residential charging piles, as well as ride-hailing drivers, report stable prices without noticeable increases. Yet, some Shanghai netizens note a decline in the availability of low-cost charging piles nearby. Other cities also show a divided trend, with some users reporting increased charging costs while many vehicle owners claim stable prices.

Unlike uniformly priced fuel, public charging pile electricity prices vary significantly by time and location, even though the electricity itself has no quality difference. This amplifies user sensitivity to price fluctuations. Lower usage costs have been a core reason for most people choosing NEVs. Especially now, with high fuel costs, the relatively low energy expenses of electric vehicles remain their key competitive advantage.

Therefore, even small electricity price increases of a few cents or mao can directly impact vehicle owners’ cost perceptions and travel choices.

01 Price Fluctuations Vary by Station

“I haven’t noticed any changes; it’s always been this price.” In April, visits to several old residential areas in Shanghai revealed stable charging pile prices with no increases.

Xiao Shen, a part-time ride-hailing driver who owns a BYD Song with a pure electric range of about 100km, is not sensitive to electricity prices when charging in his neighborhood. “The price has always been 1.3 yuan per kWh, with 0.6 yuan for electricity and 0.7 yuan for service fees.” Xiao Shen also mentioned that charging pile spots in his area are limited, and sometimes he cannot charge if he returns late, forcing him to use fuel instead. “I’m more sensitive to fuel prices, but since it’s just a part-time job, I don’t pay much attention to costs.”

Taxi driver Xiao Dang, who lives in the more remote Chuansha area, also charges in his neighborhood. Compared to the city center, their electricity prices are cheaper. “It’s 1.2 yuan during the day and 0.6 yuan at night. My car’s battery can last 300 kilometers, so I usually charge once during the day and once at night.”

Even though daytime charging is more expensive, Xiao Dang must charge at high prices to continue working. Sometimes, to save time, he also visits battery swap stations. “Swapping a 290-kilometer battery costs a bit more than charging but is faster.”

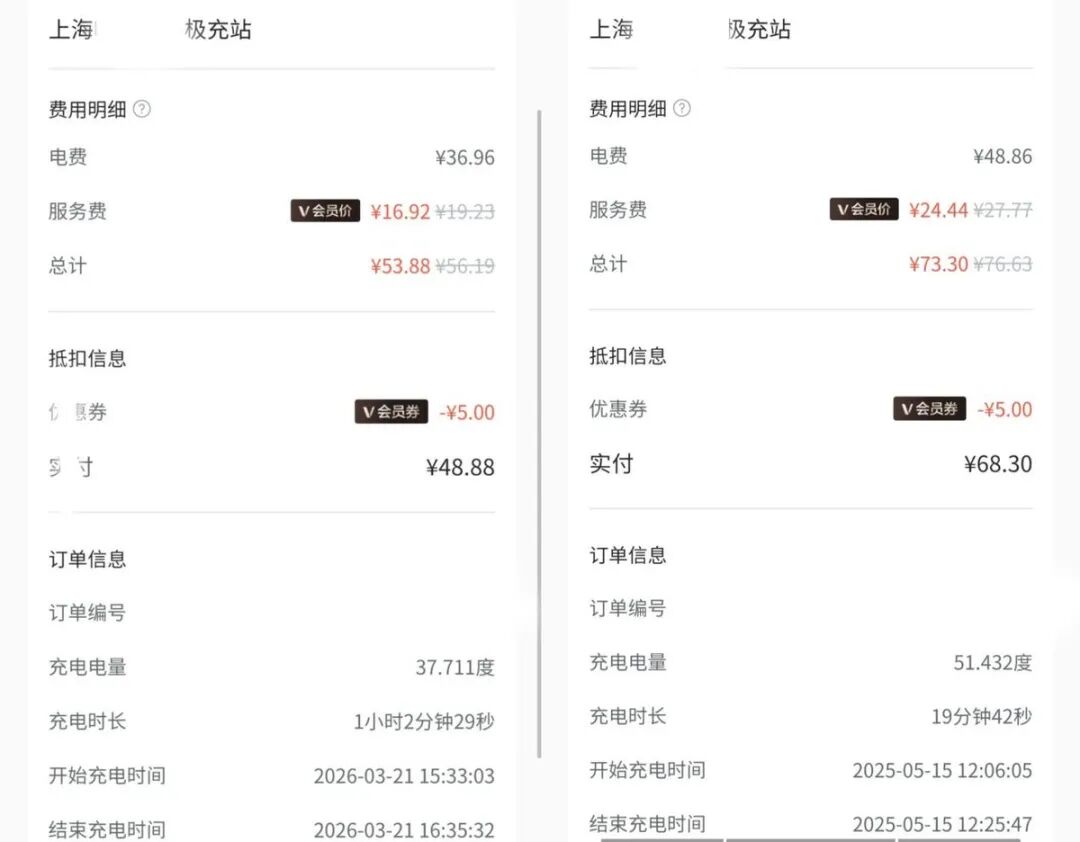

Thus, charging price increases have not significantly impacted ride-hailing drivers, who face the most urgent charging needs. In office areas like office buildings and shopping malls, charging price fluctuations are also insignificant. For example, the author charged 51.43 kWh last year at the same charging pile in the same office building, costing 68.3 yuan (1.32 yuan per kWh). This year, charging 37.71 kWh cost 48.88 yuan (1.29 yuan per kWh). With coupons applied, the unit price actually decreased.

In daily posts by users in other Shanghai areas, some mention nearby charging pile price increases, with few “bargain” options at 0.5 yuan per kWh available at night. This indicates that charging pile price adjustments lack specific targeting, with significant differences between stations.

The situation in lower-tier cities is similarly varied. Some netizens complain about small local price fluctuations, while others in the same region report stable charging prices. Overall, whether charging costs increase largely depends on the region, charging time, and operator pricing strategies.

While consumers worry about charging pile price increases, operators have not achieved revenue growth through price adjustments.

Lao Jiang, the owner of a charging station in a fourth-tier city, stated that he invested 900,000 yuan to build the station in 2020. At the time, with few charging stations, vehicle owners queued to charge, and each gun could charge up to 300 kWh per day. With a 0.3 yuan per kWh service fee, he earned a pure profit of 500,000 yuan that year.

However, after 2023, with more operators entering the market, charging pile service fees gradually declined due to competition, with the original 0.3 yuan per kWh fee dropping to 0.05 yuan. Meanwhile, charging pile idle rates also increased, and profits sharply declined. Lao Jiang said that since 2023, his station’s revenue has plummeted to 80,000 yuan, with daily income now only around 200 yuan and annual profit further dropping to 60,000 yuan.

The stark contrast between users’ perceived “price hikes” and operators’ actual “revenue struggles” is not simply due to market supply and demand fluctuations but results from electricity pricing policies, cost structures, and industry competition.

02 Prices Return to ‘Normal,’ but No One Wins

A closer look reveals clear pricing logic behind public charging pile price fluctuations. Home charging piles follow residential electricity prices set by the government, remaining stable long-term. Public charging pile fees consist of industrial and commercial electricity prices and operator service fees, which are the core sources of price fluctuations.

In December 2025, the National Development and Reform Commission and the National Energy Administration jointly issued the “Basic Rules for the Medium- and Long-Term Electricity Market,” stating that starting March 1, 2026, fixed peak-valley electricity prices for public charging piles will be canceled, and fully market-based dynamic floating pricing will be implemented, with electricity prices adjusting in real-time based on grid load, new energy power generation output, and market supply and demand. “It’s not an increase; lows are just more flexible,” an industry insider said in a previous interview.

Besides flexible industrial and commercial electricity price adjustments, users’ perceived price increases largely relate to service fee adjustments. Service fees are operators’ main revenue sources to cover site rent, equipment depreciation, maintenance labor, and power losses, with operators having significant control over them. The core reason for fluctuations in Lao Jiang’s charging station revenue lies in service fee changes.

Industry data shows that Teld and StarCharge lead the industry with market shares of 18.88% and 15.37%, respectively. However, even these top companies have slowed their expansion amid continuously declining service fees. As of December 2025, StarCharge operates over 38,000 charging stations nationwide. Despite large-scale cost dilution, its full-cycle operating costs remain at 0.4 yuan per kWh, meaning service fees must exceed this level to break even.

A 0.4 yuan per kWh service fee is not low. In Shanghai, where charging prices are higher, most charging pile service fees exceed this range. For vehicle owners in lower-tier cities accustomed to low prices of a few mao, this pricing is likely even less acceptable.

The significant gap between market acceptance and operator costs clearly shows a complete reversal in the industry’s profit logic.

Comparing the 2020 scenario where private charging stations could earn 500,000 yuan annually with a 0.3 yuan per kWh service fee to today’s situation where top companies barely break even at 0.4 yuan per kWh, the service fee benchmark in the charging pile industry has undergone dramatic changes over six years.

However, following normal market logic, with more entrants, marginal costs should gradually decrease—just like in car manufacturing, where producing more vehicles lowers the cost per unit and increases profits. Why has the charging pile market not followed this trend?

On one hand, significant capital and new entrants have improved user charging convenience but also severely dispersed customer traffic. Many charging piles remain idle on weekdays, causing resource waste. Coupled with rising site rent and maintenance labor costs year by year, operators’ profit pressures continue to intensify.

On the other hand, a noticeable charging gap exists among users, with “a shortage of piles during peak hours.” Charging queues at highway service areas during holidays have become common, highlighting the severe charging shortage. Currently, charging pile entrants include professional operators like Teld, car brands, and individual investors.

From operators’ perspectives, deploying charging stations is necessary to dilute costs and capture market share. For car companies, accelerating the deployment of supercharging stations and battery swap stations is crucial for improving user services, bundling car purchase benefits, and enhancing brand competitiveness. For example, BYD plans to build 20,000 flash-charging stations this year, NIO is accelerating supercharging station deployment, and NIO’s battery swap stations now connect the Sichuan-Tibet section of National Highway 318. Private charging station operators, driven by profit considerations, also fill the gap in charging piles in lower-tier cities and are indispensable.

However, amid malicious competition to capture customers and increased user choices, operators find it difficult to cover costs through reasonable pricing, leaving them torn between “lowering prices to grab orders” and “raising prices and losing customers.” A top operator executive previously stated that after leading nearly ten initiatives opposing internal competition and advocating for prices to return to normal ranges, progress remains difficult.

For operators and car companies, the dilemma at highway charging stations is particularly typical. Limited by geographical location, highway station maintenance costs are higher, and electricity prices are more expensive. Vehicle owners usually charge before going on the highway and only recharge during long-distance travel, resulting in low station usage rates on weekdays and further pushing up service fee costs. During holidays, traffic surges, and pile shortages occur, necessitating continuous new construction and forming a vicious cycle of “idleness—price hikes—queues—new station construction.”

From individual operators’ perspectives, lacking the membership fees, government subsidies, and additional revenue from battery sales that come with scale advantages, they can only compete by offering even lower service fees.

Thus, while service fees are somewhat regulated and expected to rise back to so-called “normal” price levels, the current situation represents a lose-lose scenario for consumers and charging piles: consumers face higher charging service fees and worse experiences, while charging piles see increased costs that cannot cover operating expenses.

For new energy vehicle owners, fluctuations in charging costs are gradually eroding the core competitiveness of electric vehicles. Although this price increase is not yet widespread, with market-based pricing fully implemented, charging prices will more closely reflect supply and demand and true costs. This means bidding farewell to past “one-size-fits-all” low-price benefits and entering an era where charging requires price comparisons, timing choices, and careful budgeting.

For the entire industry, ensuring reasonable service fees and operator survival while preventing excessive cost pass-through to consumers, improving charging pile usage efficiency, alleviating the structural contradiction of “idleness during off-peak hours and shortages during peak hours,” and maintaining healthy profitability will be core challenges in the coming years.

Editor-in-Chief: Du Yuxin Editor: He Zengrong

THE END

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’