CATL and Automakers: Three Questions on Profit Distribution in the Industrial Chain

04/22 2026

04/22 2026

551

551

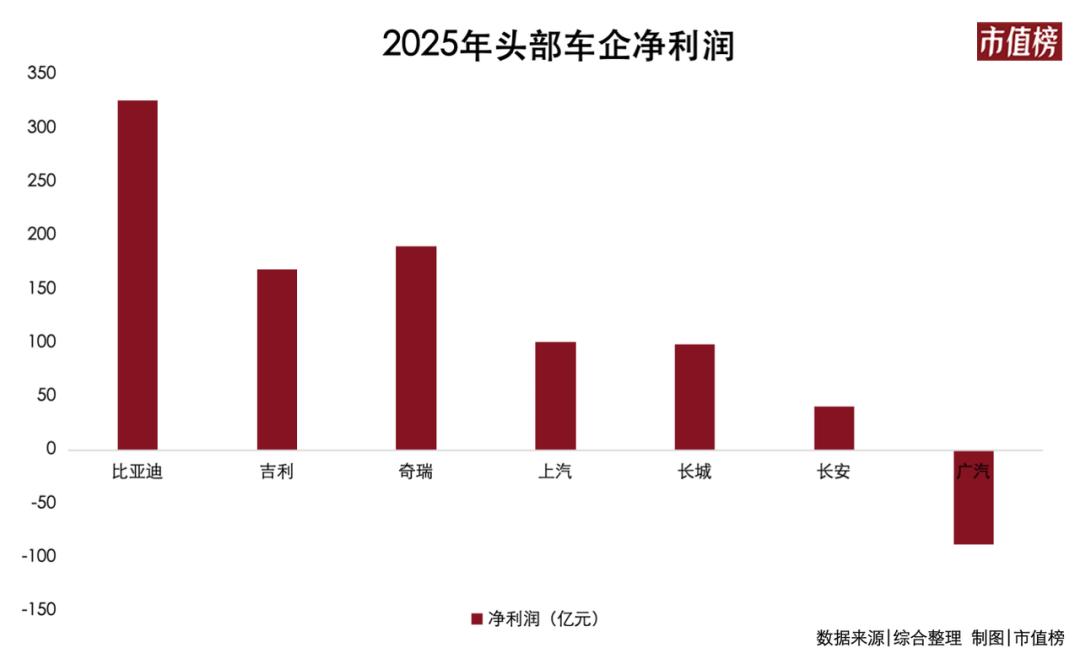

The profits of one battery supplier rival those of four leading automakers.

In 2025, CATL reported a net profit of 72.2 billion yuan, nearly 4 billion yuan more than the combined profits of three leading automakers (BYD, Geely, and Chery) during the same period—almost equivalent to the profit of Changan Automobile. In the first quarter of 2026, CATL's net profit grew by over 48%.

Cui Dongshu, Secretary-General of the China Passenger Car Association, described the situation as 'dismal' at a public event in March this year, stating that 'most remaining automakers are essentially out of money.'

Profits in the industrial chain are increasingly concentrated upstream.

A similar scenario recently unfolded with Ctrip, where the majority of profits in the travel industry were captured by the platform, leaving merchants struggling with meager margins. When one segment captures an excessive share of the entire chain's profits, criticism naturally follows.

Meanwhile, news of 'market capitalization exceeding 2 trillion yuan' and 'surpassing global automotive leader Toyota' continues to emerge, putting CATL in the spotlight.

But how did this profit distribution pattern form? While division of labor should bring mutual benefits, why hasn't the automotive industry's upstream and downstream sectors experienced a 'rise and fall together' dynamic? What does the imbalance in industrial chain profits signify?

I. Automakers' Ledger: Rational Division of Labor, Strategic Misalignment

In 2025, the profit margin on sales for China's automotive industry dropped to 4.1%. In some months, it fell below 2%, with December seeing a mere 1.8%. In contrast, the manufacturing sector's average was 5.9%.

Selling cars at a profit has become the norm across the industry. Meanwhile, power batteries—a core component accounting for 30% to 40% of a vehicle's cost—have emerged as the profit hub of the entire industrial chain.

In 2025, CATL secured a 43.4% share of China's power battery market and 39.2% globally. When a single supplier dominates nearly half the market, pricing power naturally rests with it.

Additionally, since the second half of 2025, the core raw material for batteries, lithium carbonate, has surged from a low of 58,000 yuan per ton to nearly 190,000 yuan per ton.

Upstream, imported inflation persists, while among peers, a prisoner's dilemma unfolds.

Price wars have repeatedly erupted in the new energy vehicle (NEV) industry since 2023. To maintain market share, automakers have had to follow suit, leading to reduced profits and cash flow pressure.

In 2025, NEV prices dropped by approximately 11%. By early 2026, the price-cutting trend continued, with nearly 70 models across the industry reducing prices, averaging 38,000 yuan per NEV.

Downstream consumers now have more choices and are increasingly cautious, comparing specifications, prices, and reputations. The battery brand itself has become a critical decision-making factor. CATL's years of accumulated consumer-end recognition makes automakers hesitant to switch suppliers due to potential consumer backlash.

The result of this triple squeeze is that upstream CATL operates at nearly full capacity, with a 96.9% utilization rate in 2025, reaping substantial profits. Automakers, meanwhile, not only have thin profit margins but also must wait in line to prepay for capacity.

How did this situation arise? As NEVs transitioned from a niche category to the mainstream, Chinese automakers faced a choice: build batteries in-house or purchase them?

Building in-house meant entering an entirely unfamiliar technical field.

On one hand, power batteries are products of electrochemical systems, requiring long-term material accumulation and manufacturing process expertise—areas outside automakers' core competencies in mechanical and electronic integration.

On the other hand, the technological path was uncertain at the time. The power battery industry is also highly volatile, with lithium carbonate prices capable of doubling or halving within a year. Expanding production requires billions in investment, and choosing the wrong technology could result in total loss.

Purchasing batteries, however, meant adopting a light-asset, fast-turnover, and risk-controlled approach. Savings could be reinvested in chassis development, marketing, and intelligence. From a financial perspective, this was a clear-cut decision.

Most automakers chose to purchase. Given the context, this choice was understandable.

From Adam Smith's division of labor theory to David Ricardo's comparative advantage, economics has repeatedly demonstrated over centuries that focusing on what one does best and trading for the rest maximizes efficiency and returns.

This has been the automotive industry's dominant, mature division of labor model for the past 30 years: automakers handle integration, while suppliers provide components.

From 2017 to 2021, the number of power battery companies achieving vehicle integration dropped from 102 to 58, a over 40% decline, validating the rationality (rationality) of automakers' risk-averse decisions at the time.

Over the next decade, Chinese automakers rapidly advanced along this division of labor path, propelling China's NEV production and sales to global leadership.

The problem lies in the object of division.

In the traditional internal combustion engine vehicle era, the engine was the core technology, but its collaborative interface had been highly standardized over years of refinement. Power batteries in the electrification era are entirely different, deeply integrated with a vehicle's BMS, thermal management strategy, and chassis structure.

In this context, switching battery suppliers involves systemic redevelopment across multiple levels, including cells, modules, battery packs, BMS, thermal management, and vehicle control units. Procuring batteries with a 'buy tires' mentality represents a strategic misalignment.

An exception is BYD, which self-develops and self-produces its three electric systems (battery, motor, and electronics). This approach, rooted in BYD's battery origins, comes with heavy asset investment and high risks, reflected in its balance sheet's substantial capital commitments. The payoff is a thicker buffer when the entire industry struggles with battery costs.

In 2025, BYD's automotive business still maintained a gross margin of 20.49%—the lowest in three years but leading among peers. It could withstand price wars and even initiate them.

II. CATL's Ledger: Leverage Gained Through Risk-Taking

CATL's position in the industrial chain is clear from its financial reports.

On its income statement, CATL reported a full-year net profit of 72.2 billion yuan in 2025, with a net profit margin exceeding 18%. In the first quarter of 2026, as lithium carbonate prices approached 180,000 yuan per ton and the industry faced pressure, CATL maintained its gross and net profit margins, with revenue and net profit both growing by around half.

A research report by Capital Securities attributed this to the company's use of long-term agreements to hedge raw material price fluctuations while optimizing its product mix to boost profits. In simpler terms, CATL either absorbed or passed on pricing pressures.

On its balance sheet, CATL held over 40 billion yuan in contract liabilities—prepayments from customers—which grew by over 70% in 2025. Meanwhile, its accounts payable and bills payable to upstream suppliers exceeded 300 billion yuan by the end of March 2026.

CATL collects payments from downstream customers in advance while delaying payments to upstream suppliers, controlling funds from both ends. Few manufacturing firms achieve such bidirectional capital occupation, underscoring CATL's leverage in the industrial chain.

Where does this leverage come from?

First is market share. When planning their supply chains, automakers cannot overlook CATL. Its dominant market position has effectively made its battery dimensions and specifications industry standards.

Second is technological coupling. From CTP to Qilin batteries to Shenxing ultra-fast charging, CATL has continuously upgraded batteries from 'components' to 'technology platforms.' These solutions are deeply integrated with vehicle chassis structures, BMS control strategies, and thermal management systems, raising the cost for automakers to switch suppliers. Thus, even if cheaper alternatives exist, automakers are reluctant to migrate.

Third is joint ventures.

The NEV industry has long moved beyond a simple 'procurement-supply' model, entering a phase of deep integration where 'you are in me, and I am in you.'

Over the past few years, CATL has established multiple joint venture battery factories with automakers such as SAIC, GAC, FAW, Dongfeng, Geely, Changan, and Chery. These automakers have invested heavily in equipment, production lines, and capacity planning for these joint ventures, making it even harder to pivot away.

Building such leverage takes time, and the power battery industry has never been peaceful.

Beyond technological uncertainties, the industry faces repeated questions about 'overcapacity,' especially after subsidy reductions, with fears of widespread failures. In 2017, total capacity exceeded 200 GWh, but utilization rates remained low. Huang Shilin, CATL's vice chairman, publicly predicted then that 'less than one-fifth of capacity might be used by 2019' and that 'overcapacity would persist until 2023.'

CATL itself has not had an easy journey.

Amid declining capacity utilization and the abolition of the 'white list' for power batteries—allowing foreign battery firms to re-enter the Chinese market—any shortfall in industry demand or worsening competitive landscape could turn its massive capital expenditures into sunk costs, repeating the solar industry's post-expansion collapse scenario.

Thus, CATL's counter-cyclical expansion raised questions about 'excessive financing' and whether it would become 'the next Suntech Power.'

CATL won its gamble. Its profits represent not just technological premiums but also compensation for the risks it shouldered over the past decade—anticipating demand, investing in capacity, and managing heavy assets.

III. Rebalancing the Industrial Chain

Over more than a century in the automotive industry, vertical integration and horizontal division of labor have each had their heyday—and their setbacks. Profit distribution across the industrial chain has always been dynamically balanced.

What remains constant is that whoever controls irreplaceable segments captures the largest share. A decade ago, that segment was vehicle brands and distribution channels; a decade later, it is power batteries.

However, excessive profit concentration upstream is unlikely to benefit the industry's long-term health.

With automakers' profit margins on sales dropping to 4.1%, investments in vehicle platforms and intelligent driving will inevitably suffer. Ultimately, consumers do not purchase battery specifications but entire vehicles. If innovation at the vehicle level stalls, battery technological leadership will lack a platform for implementation.

Imbalanced leverage also makes life difficult for smaller firms in the industrial chain.

In 2024, domestic automakers' average payment terms extended to 170–200 days, with suppliers waiting nearly half a year for payment. Some small and medium-sized parts manufacturers faced collection periods exceeding 300 days.

In response, in June 2025, 17 automakers, including FAW, Dongfeng, BYD, and Geely, collectively pledged to reduce supplier payment terms to within 60 days. The China Association of Automobile Manufacturers (CAAM) later issued a similar proposal (initiative). By February 2026, CAAM surveys indicated that most major automakers had shortened payment terms to around 54 days.

Meanwhile, Wind data showed that in 2025, CATL's accounts payable turnover days (excluding bills payable) exceeded 160 days. As the most powerful player in the industrial chain, CATL should also shoulder certain corporate social responsibilities.

Automakers at the end of the chain have long recognized the issue of 'working for CATL' and have attempted to shift the dynamic in recent years by introducing secondary and tertiary suppliers and developing in-house batteries.

Progress has been made in 'de-CATL-ization.'

In 2025, CATL's domestic market share was 43.42%, down 1.67 percentage points year-on-year. Contemporary Amperex Technology Co. Limited (CALB) shipped 53.61 GWh, capturing nearly 7% of the market; Gotion High-Tech shipped 43.44 GWh, accounting for 5.65%; and Sunwoda shipped 24.35 GWh, ranking sixth.

In-house battery development has also begun yielding tangible results. Geely consolidated its battery business into 'Jiyao Tongxing,' which shipped 15.08 GWh in 2025, entering the top 10 for the first time. GAC's Inova Battery, with a planned total capacity exceeding 60 GWh and 18 GWh of mass production line (mass production lines) already built, ranked 12th in shipments. These were the first automaker-affiliated battery brands to make the annual shipment rankings.

Simultaneously, another trend is intensifying.

Since the second half of 2025, CATL has signed 10-year strategic cooperation agreements with Beiqi Foton, Great Wall Motor, JAC Group, GAC Group, and Voyah Automobile, along with a five-year comprehensive deepening memorandum with Changan Automobile.

While automakers are 'de-CATL-izing,' they continue to 'lock in' CATL for high-end and critical projects, reflecting the reality that bypassing CATL is unrealistic in the liquid battery era.

In the first quarter of 2026, CATL's market share rebounded to 50.1%, regaining half the market for the first time in five years—a testament to this point.

The true window for reshaping the supply chain landscape lies in the next technological node: solid-state batteries.

Geely plans to complete self-developed all-solid-state battery pack production and vehicle integration testing by 2026, with small-scale industrialization in 2027. Changan expects to complete 'Golden Bell' solid-state battery integration into robots and vehicles by Q3 2026, with gradual mass production in 2027. GAC has built its first pilot production line for high-capacity all-solid-state batteries, aiming for small-scale vehicle integration testing in 2026.

Industry consensus suggests that vehicle integration testing will occur in 2026, with demonstration mass production starting in 2027 and scalable markets emerging around 2030.

Solid-state batteries require a complete overhaul of electrolyte materials, manufacturing processes, and core equipment. Whether automakers can build autonomous solid-state battery capabilities within this window will determine whether the industrial chain undergoes a 'reshuffle' or if they continue 'working for others.'

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’