Chinese Cars Enter the 'Era of Price Hikes' Amid 'Sales Slump'

04/24 2026

04/24 2026

515

515

Lead

Introduction

As sales curves decline, the legacy of price wars and the rise of pure electric vehicles (EVs) are jointly propelling domestic car prices upward. After years of languishing in a discount rut, the 'era of price hikes' has quietly arrived.

Sales are declining, yet prices are rising. This is not a paradoxical defiance of conventional wisdom...

'I’ve never been so eager for a Beijing Auto Show.'

An auto brand sales manager paused thoughtfully. This statement carries dual undertones: optimistically, there is anticipation that the world's largest Beijing/Shanghai Auto Show will drive market recovery; pessimistically, there is concern over the continued slump in China's auto sales in March.

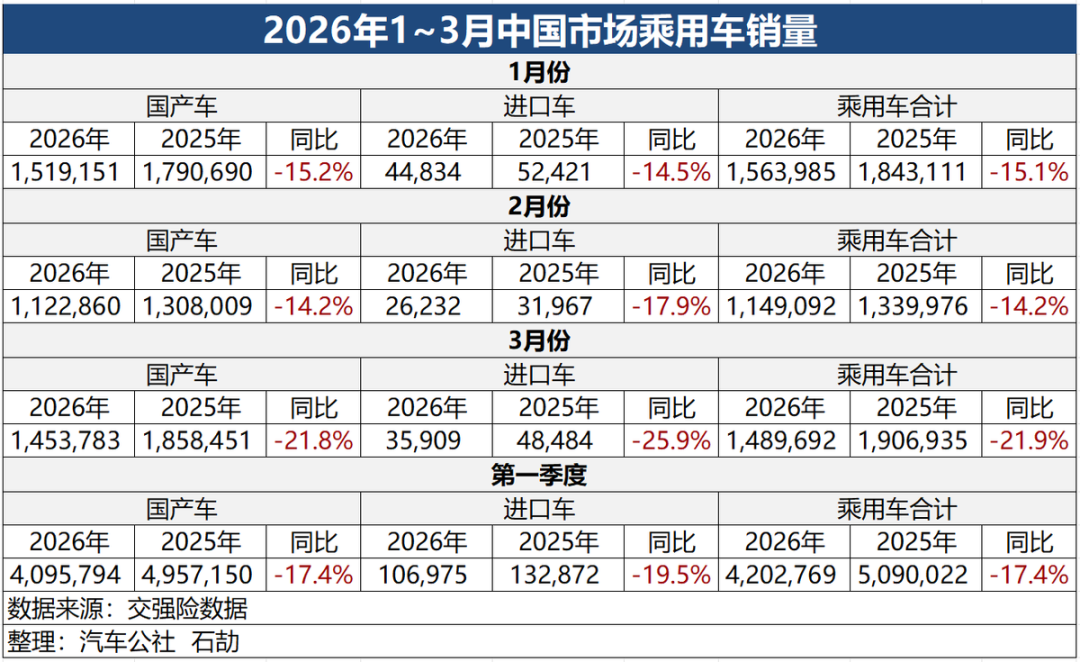

According to data compiled by Automobile Commune on insurance registrations, domestic passenger vehicle sales (both locally produced and imported) fell by over 20% year-on-year last month, with an overall decline of 21.9%. The much-lamented sales drops in January and February were around 14-15%.

In the third week of April, retail sales plummeted by 33% year-on-year.

However, this is not merely a story of automotive decline. If we look beyond monthly sales fluctuations, a deeper contradiction emerges: conventional wisdom dictates 'cut prices when sales lag,' yet new car prices are quietly rising.

'Compact car sales shrink due to policy rollbacks,' but structural market changes are not the sole driver. Terminal data indicates that price discounts have indeed weakened from their 2022 peak. As macroeconomic policy shifts slightly from deflation toward inflation, the auto industry follows suit.

Coexisting gains and losses, fire and ice. This industry landscape defies simple linear logic. Its essence is not sudden price volatility but an inevitable backlash and positive correction at a specific developmental stage.

To decode seemingly anomalous consumer sentiment, we must examine the uppermost cost chains, the deepest technological pathways, and the value logic quietly redefined on auto show stages.

For years, price wars dominated China's auto market—from 'involutionary cuts' by new energy vehicles (NEVs) to 'clearance sales' of traditional fuel vehicles. Each round of price reductions eroded automakers' profits and strained the supply chain.

Now, with lithium carbonate prices rebounding strongly, automotive-grade chip shortages, policy-driven market order regulations, and breakthroughs in pure electric technology, this long-brewing wave of price hikes finally breaks the price war deadlock. It signals China's auto industry officially bidding farewell to 'low-price-only' strategies and entering a new value-centric development cycle.

Thus, the 2026 Beijing Auto Show becomes not just a 'lifeline' to boost market demand but also a pivotal moment for restructuring China's automotive industry logic.

01

Rising Amid Decline – Price Wars Cannot Continue Indefinitely

Market sales fall, yet car prices rise.

'The Performance version does exceed 400,000 (yuan). As a company-owned store, the price is set directly by headquarters,' said sales staff at several Tesla stores visited recently, from the North Fourth Ring Road branch to the Laiguangying Tesla Center. The core message: 'The Model Y Performance version has increased in price.'

A companion accompanying the store visits smugly remarked, 'Looks like my purchase last year was quite prescient.'

Analyzing 'Chinese cars entering the era of price hikes' reveals three dimensions.

First is the intuitive 'structural increase in per-vehicle prices.'

According to CPCA statistics, the average retail price of passenger vehicles rose from 165,000 yuan in 2021 to a peak of 184,000 yuan in 2024. It dipped to 170,000 yuan in 2025 but rebounded to 175,000 yuan in March 2026.

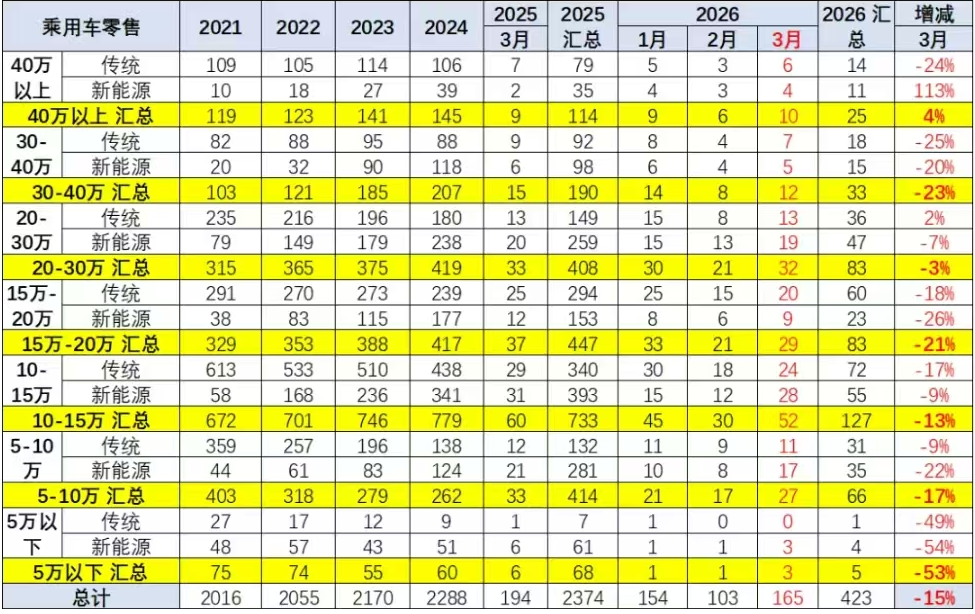

Many observers casually attribute this to 'the collapse of the compact car market due to policy rollbacks,' which is partially true—sales of vehicles under 50,000 yuan plummeted 53% year-on-year in Q1 2026.

Large vehicles still dominate new models at the Beijing Auto Show.

The AITO M9 Ultimate is equipped with six LiDAR sensors, Huawei's latest intelligent driving system, and HarmonyOS cockpit; NIO ES9 aims to replicate the success of the third-gen ES8, while Leapmotor L90 inherits downgraded Neptune 9031 chips and LiDAR; Li Auto's next-gen L9 features an 800V 'magic carpet' suspension, claiming handling comparable to Ferrari sports cars; Mercedes-Benz debuts the new GLC and, more notably, the new S-Class with mid-cycle updates akin to a full model change.

Some brands even launch dual flagships: BYD's Sealion 08 emphasizes extreme charging capabilities alongside AI multi-modal cockpit interactions, while the Tang model prioritizes business appeal and stability; Geely pairs the Zeekr 8X (sport flagship) and 9X (luxury flagship); GWM's WEY brand follows the V9X with the V8X; Leapmotor positions the D19 alongside the D99.

The second dimension involves expanding into higher-end product categories.

As Huawei's Seres AITO's sales leader, the M9 Ultimate finally breaks the 600,000-yuan price ceiling with a pre-sale price starting at 669,800 yuan.

According to Wilson Analytics, among the 215 models exhibited at this auto show, 29 are C-segment mid-to-large sedans, 34 are C-segment mid-to-large SUVs, and an astonishing 29 are D-segment full-size SUVs.

But the third dimension represents genuine price hikes.

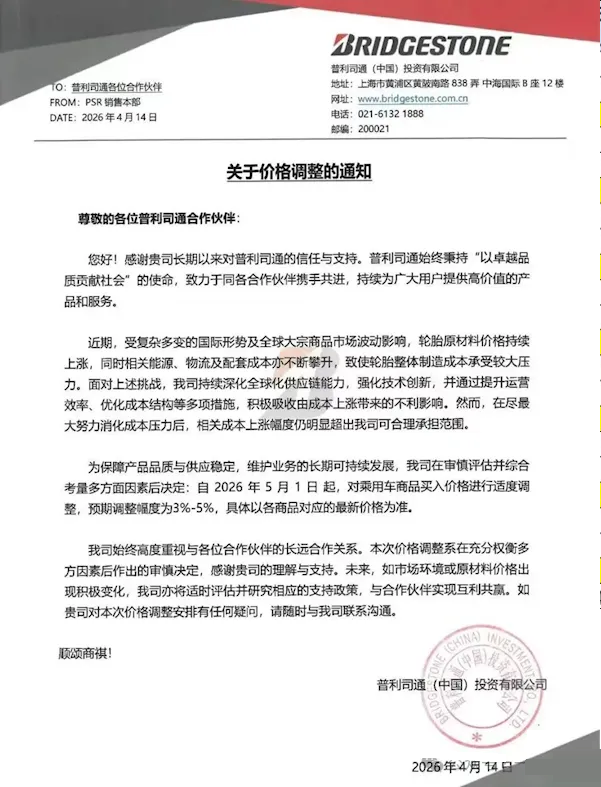

After the Spring Festival, 15 models announced price increases, starting with the Exeed ET5 and Bestune Xiaoma Yueyi.

Unlike past 'temporary promotional recoveries,' this round involves 'actual official price hikes.' The Exeed ET5's high-end variant increased by 5,000 yuan, with its previously free intelligent driving package now priced separately; the Bestune Yueyi 03 raised mid-to-high-end trims by 2,000-5,000 yuan under the guise of added features.

This is no isolated incident. Tesla led the charge, raising the Model Y Long Range from 357,900 yuan to 375,900 yuan and the Performance version from 397,900 yuan to 417,900 yuan with two price adjustments in one week.

Xiaomi followed, increasing the new SU7's price by 4,000 yuan across all trims compared to the previous generation. Lei Jun admitted that material costs alone rose nearly 20,000 yuan, making this a compressed increase.

BYD implemented hikes on March 16, raising prices by 3,000-6,000 yuan for multiple best-selling models in its Dynasty and Ocean series, including the Song PLUS, Han, and Seal. The Avatr 12 saw the largest adjustment, with its pre-sale price jumping from 269,900 yuan to 299,900 yuan—a 30,000-yuan threshold increase.

While the first two dimensions stem from structural adjustments and localized consumption upgrades, the third reflects a blend of 'correction' and 'necessity.' Correction addresses past price wars, while necessity ties to soaring upstream raw material costs.

Battery-grade lithium carbonate prices surged from 75,000 yuan/ton in July 2025 to about 170,000 yuan/ton in March 2026—a 130% increase—adding 3,000-5,000 yuan to per-vehicle battery costs.

Since mid-April 2026, China's tire industry has faced its second annual price hike wave, with over 70 tire companies issuing 'price increase notices.' Passenger car tire prices generally rose 2-5%. Droughts in natural rubber regions, synthetic rubber prices doubling due to crude oil spikes, and carbon black prices jumping 13% monthly due to environmental production curbs collectively raised all-steel tire production costs by nearly 7% from January to March.

Meanwhile, the AI boom rapidly squeezed automotive-grade chip capacity, with memory chip prices soaring nearly 300%, increasing per-vehicle chip costs from 700 yuan to 2,000 yuan.

Additional pressure comes from policies. Starting in 2026, NEV purchase tax exemptions shifted from full exemption to 50% reduction, with a maximum deduction capped at 15,000 yuan. A 200,000-yuan vehicle now costs approximately 9,000 yuan more upfront.

UBS estimates paint a starker picture—the cumulative impact of these factors will raise costs for a typical mid-sized intelligent electric vehicle by 4,000-7,000 yuan.

Thus, 'price hikes' and 'value escalation' became evident around the Beijing Auto Show, driven by both corrective measures and inevitable cost pressures.

02

The Electric Era Is Also an Era of Price Hikes

While geopolitical conflicts drive up oil prices, China's auto market feels the ripple effects thousands of miles away.

'Concerned about affording gasoline, I chose pure electric,' said multiple friends when purchasing vehicles after March 2026.

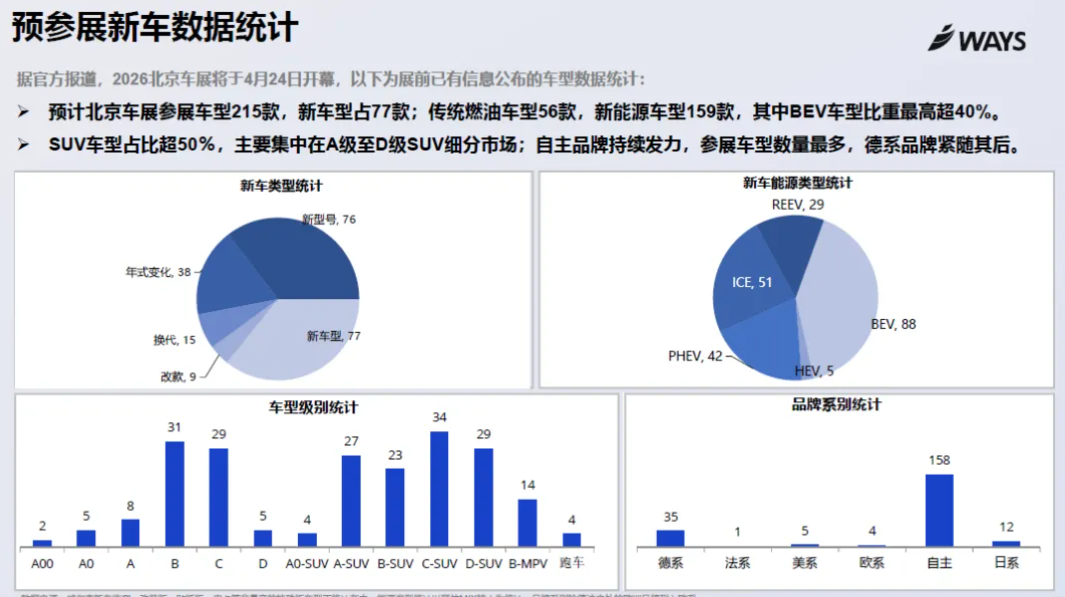

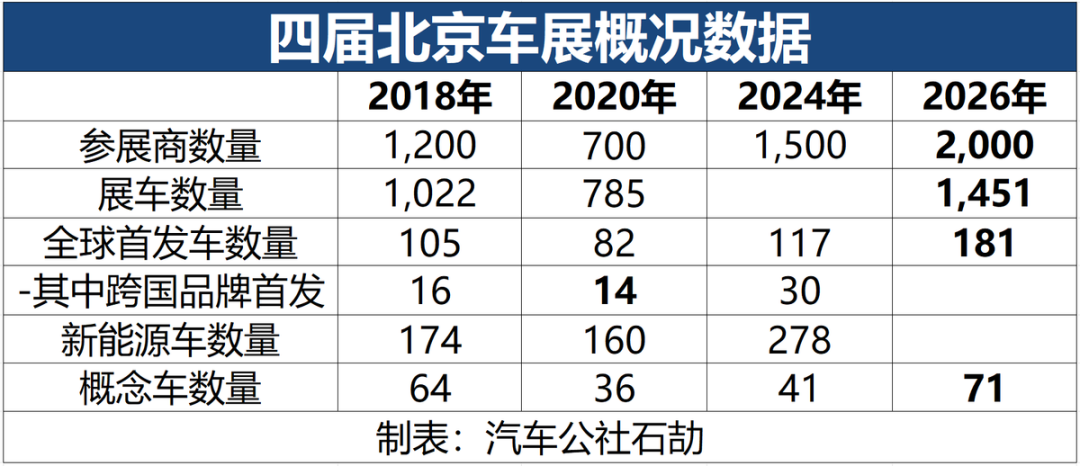

The 2026 Beijing Auto Show will be remembered for two figures: 1,451 total exhibit vehicles and 181 global premieres.

But the truly groundbreaking signal lies deeper in Wilson Analytics' refined statistics: among the 215 exhibited models, 159 are NEVs (70%+ share), with 88 pure electric models—surpassing the 56 fuel vehicles and even exceeding the combined total of plug-in hybrids and extended-range EVs.

This contrasts sharply with the 'PHEV boom' trend of 2024-2025, when 'dual power' (gasoline-electric) models dominated, with extended-range versions becoming a 'must-have' for hitting 10,000 monthly sales. The 2026 Beijing Auto Show marks a complete reversal, with pure electric models asserting overwhelming dominance.

According to CPCA's March 2026 domestic passenger vehicle retail sales data, pure electric vehicle sales fell 11.7% year-on-year to 644,000 units, PHEVs dropped 23.5% to 204,000 units, and extended-range EVs declined 6.0% to 76,000 units. Q1 2026 sales for these three powertrains fell 19.9%, 28.3%, and 6.4% year-on-year, respectively.

Three signals from Automobile Commune indicate pure electric models are cannibalizing hybrid market share:

Signal 1: BYD's Ocean Network leaked data showing 80% of new orders are for pure electric models. This suggests that brands like the Song Pro DM-i and Seal DM-i, which once dominated the PHEV market, are now steering consumers toward pure electric options.

Signal 2: The Tengshi D9—a phenomenal model that propelled the entire PHEV MPV segment—currently sees only 10% of orders for its pure electric version. However, insiders predict this ratio will exceed 40% as the new-gen D9 pure electric's range and charging efficiency improvements far exceed expectations.

Signal 3: Nissan's NX8 pure electric variant accounts for 80% of its orders. Consumers prefer going all-in on pure electric rather than settling for a 'compromise solution.'

Li Auto's transition provides the strongest evidence. Once defined by its 'extended-range strategy,' the company's pure electric i6 model delivered over 24,000 units in March 2026, propelling Li Auto's monthly deliveries back above 40,000 units. The debate between extended-range and pure electric routes has been settled by market data.

Advancements in battery energy density and ultra-fast charging infrastructure have reached a tipping point that erodes the extended-range advantage.

What defines extended-range technology? It uses a small internal combustion engine as a 'fuse' against range anxiety, serving as both psychological reassurance and physical backup until battery energy density can support 1,000+ kilometers of actual range.

SUVs in the RMB 200,000–300,000 price bracket, and NIO's ES8 consistently maintaining monthly deliveries at the 10,000-unit level all provide compelling evidence of this trend.</p>

<p>In contrast, while plug-in hybrid models still offer plenty to see at the Beijing Auto Show, they have become supplementary solutions tailored for specific markets. Range-extended models now primarily serve to defend existing product lines rather than expand them.</p>

<p>For instance, the SAIC Volkswagen ID.ERA 9X showcased at Volkswagen Night was conceived over two years ago, resembling a 'forced march' for a transitional era.</p>

<p>03</p>

<p>The Decline of Large Six-Seaters and the Rise of Large Five-Seaters</p>

<p>If BEVs justify price increases through new powertrain technologies, then changes in body style and size form another pillar supporting the 'era of price hikes.'</p>

<p>Viewed through this lens, the recent popularity of large six-seaters and the resurgence of large five-seaters this year represent a 'baton pass' for high-priced models, continuing to drive up the average transaction price across the auto market.</p>

<p><img src=)

'Bigger body, more seats, fuller configurations'—this is how large six-seater SUVs position themselves as 'typical products of the era of price hikes.'

During the policy-driven sales boom of 2025, this logic seemed unassailable. A combination of trade-in incentives and purchase tax exemptions acted as catalysts, propelling a wave of family buyers into the high-priced six-seater SUV segment.

However, the March 2026 sales rankings for large six-seater SUVs paint a grim picture. The Geely Galaxy M9 sold just 3,773 units that month, while the Lynk & Co 900 plummeted to 1,191 units. After the policy-driven wave, which saw large six-seater SUVs routinely sell over 10,000 units per month last year, receded, it left behind a stranded fleet of 'over-equipped models.'

Behind this lies the reality of declining birth rates—family structures have evolved.

Data reveals a sharp decline in China's birth rate. By 2025, the total fertility rate had dropped to around 1.09, nearly halving from the replacement level of 2.1. Households with three or four members have become the mainstream choice.

For a family of three or four, transforming the third row into a 'storage expansion zone' filled with strollers and camping gear is the norm, not the exception. Many six-seater SUV owners have come to realize, in hindsight, that when traveling with five people, the third row is cluttered and cramped; with all seats occupied, trunk space shrinks to barely fitting two carry-on suitcases.

Rather than pursuing 'the false prestige of six seats,' it's wiser to embrace 'the practicality of five.'

More ironically, large six-seater SUVs find themselves 'sandwiched' between more rational product forms. For daily commuting, their bulk and difficulty parking make them less nimble than large five-seater SUVs; for true family trips, MPVs outclass them in both space and seat comfort. Large six-seater SUVs have ended up in a 'no-man's-land,' pleasing no one.

Size alone does not equate to genuine demand—'big but appropriate' is the key.

Of course, concluding that 'big cars are over' would also be misguided. The signal from the Beijing Auto Show is that the large SUV segment remains highly competitive, but the approach has shifted.

At least 10 large SUVs have entered the MIIT announcement list, with models like the Ideal L9, NIO ES8, and Seres M9 firmly established in the market. The crucial point is that 'big cars' are now defined not by 'how many seats' but by 'space utilization efficiency.'

When Mercedes-Benz unveiled its largest-ever GLC L at the Beijing Auto Show, we witnessed a landmark restructuring of industry logic: luxury brands derive pricing confidence from making cars large yet agile, with full configurations but no redundancy.

Large five-seater SUVs have truly come into their own.

On March's new energy vehicle (NEV) SUV sales charts, the Ideal i6 firmly held the top spot with 24,198 units sold, while the Titan 7 PHEV and Xiaomi YU7 both surpassed 10,000 units. The combined sales of the top four large five-seater SUV models even exceeded the total sales of the top 15 large six-seater models.

The密集 (concentrated) launches of large five-seater SUVs like the Zeekr 8X, Voyah Taishan X8, IM LS8, and Nissan NX8 mark a shift in the auto market's competitive focus from large six-seaters to large five-seaters. This shift represents more than just a model replacement—it signals automakers' awakening to genuine consumer needs.

As one large five-seater SUV owner wrote on Zhihu: 'Most of my driving involves short, frequent trips. A large five-seater is easy to park, handles well, and has a spacious trunk. Why should I sacrifice 365 days of convenience for 'one day of prestige' each year?'

However, we must caution businesses against short-sightedness: don't let large five-seaters become a repeat of large six-seaters.

This concern is not unfounded: automakers tend to chase visible market trends and quickly create product redundancies. If the prosperity of large five-seater SUVs merely marks the beginning of another round of internal competition, they will surely repeat the collapse of large six-seater SUVs.

The downfall of large six-seaters serves as a warning: over 80% of products feature shockingly similar configurations—axle lengths exceeding 3 meters, range-extended/BEV powertrains, aircraft-style seats, 15-inch screens, L2+ intelligent driving... What differentiates them? Price wars?

Within a narrative framework that truly returns to user scenarios and improves spatial utility, the logic of excessive premiums based solely on seat count can no longer hold.

04

Intelligence—A Justifiable Reason for Price Hikes

At this year's Beijing Auto Show, a clear trend emerged: leading suppliers' events far overshadowed those of most automakers. Huawei Harmony Intelligent Mobility, CATL, Huawei Qiankun, and Horizon Robotics all held high-profile launch events on the eve of the show.

Suppliers related to intelligence, such as Momenta and OmniVision, prepared to launch their media offensives on the second day, April 25th.

This would have been unimaginable at the Beijing Auto Show five years ago, when luxury brands' flagship fuel-powered vehicles and concept supercars dominated the spotlight.

'Whoever masters core technologies holds the center stage.' As several automotive media outlets observed, the unspoken corollary is: 'whoever holds the center stage controls pricing power and the possibility of elevating price tiers.'

How does intelligence drive up car prices? The core lies in value enhancement, as seen in Huawei's automotive story.

On the evening of the 23rd, Jin Yuzhi, CEO of Huawei's Intelligent Automotive Solution BU, revealed several figures that focused the entire Beijing Auto Show spotlight: Huawei will invest RMB 18 billion in intelligent driving R&D in 2026, surpassing the combined total of other domestic intelligent driving suppliers. Its cumulative future investment in autonomous driving will reach RMB 70–80 billion.

Currently, Huawei Qiankun's intelligent driving training computing power has reached 60 EFLOPS, dominating the domestic market. With its ADS system updating annually, it is redefining 'intelligent driving' from a novelty feature to a 'value-preserving asset.'

When Huawei Qiankun announced that ADS 5 would prepare for mass production of L3 conditional autonomous driving, it completely reshaped the competitive landscape for intelligent driving across the auto industry.

Huawei, which 'does not build cars,' pursues a dual strategy through Harmony Intelligent Mobility and its 'Jing' series, with most affiliated brands positioned in the premium segment.

The Zeekr brand under Harmony Intelligent Mobility already leads the ultra-luxury segment above RMB 700,000; Seres has broken through the RMB 600,000 ceiling with its M9 Ultimate, stepping into ultra-luxury territory; at the pre-show Qiankun tech launch, Dongfeng Motor and Huawei Qiankun unveiled the Yijing X9, expected to be priced above RMB 250,000.

Huawei Harmony Intelligent Mobility's Q1 delivery data confirms this trend: 112,700 units delivered across all models, up 41.9% year-over-year (YoY), with cumulative deliveries surpassing 1.35 million units. Qiankun ADS has accumulated over 10.2 billion kilometers of assisted driving miles, providing unparalleled data fuel for algorithm iteration.

Beyond Huawei, Momenta supports intelligent driving functions for high-end models like the Volkswagen ID.ERA 9X and Denza U8 with its 5.0/R6/R7 systems; DeepRoute IO from Yuanrong Qixing enhances intelligence for costly models like the Wey Blue Mountain, Gaoshan, V9X, Geely Galaxy M9, and Leapmotor D19; Horizon HSD equips tech-focused models like the iCar; while Bosch XC and WeRide's end-to-end intelligent driving solutions have earned awards for models like the Exeed Star Era.

'Does your car have LiDAR?'

'What model is the intelligent driving chip? How many TOPS of computing power?'

More and more customers, regardless of their technical understanding, ask these questions when visiting dealerships, much like they ask, 'Is the battery from CATL?' Undoubtedly, intelligence is transforming from a cost burden into pricing confidence.

The industry consensus grows clearer. Initially, intelligence was seen as a massive burden for cost amortization as a 'standard feature' of BEVs; today, it has become the core foundation for vehicle pricing.

Consumers vote with their orders, showing willingness to pay thousands more for 'genuine autonomous driving potential.' This explains why the BEV SUV segment priced between RMB 250,000 and RMB 450,000—which converges the highest levels of intelligent configurations—can achieve the steepest sales growth against the trend in 2026.

The magic of intelligence lies here: as chip computing power rises and LiDAR configurations upgrade, automotive products can still find new battlefields for performance upgrades and user experience iteration despite extremely limited mechanical improvement potential—a classic logic for 'value-added' pricing.

05

Farewell to Price Wars: The Coming-of-Age Ritual for Price Hikes

'The industry has suffered from price wars for too long.'

This is no exaggerated rhetoric but a silent resonance among China's automotive professionals. CPCA Secretary-General Cui Dongshu calculated that the auto industry's profit margin stood at just 2.9% in January–February 2026. Six years prior, that figure was 8%.

What does this mean? An 'early warning line' that investors believe should not dip below 5% has been breached. The polarization of profits across the manufacturing supply chain stands revealed—non-ferrous metals still enjoy nearly 40% margins, petrochemicals approach 30%, but the midstream vehicle manufacturing industry teeters on the brink of unprofitability.

Even for consumers, price wars bring no pure good news. Hidden 'black boxes' always lurk behind them.

When too many brands struggle along the loss line, some inevitably choose 'covert cost-cutting'—eroding galvanized steel plates, scaling back welding processes, substituting safety-critical materials... These occur unnoticed in corners invisible to consumers until a crash test or safety incident exposes the hazards.

Economists often say: 'When all players in an industry operate at a loss, they are not competing—they are self-destructing.' A continuously unprofitable auto industry cannot sustain high-level R&D investment, maintain quality chains for Tier 1/2 suppliers, or provide safe and reliable products to consumers.

This zero-sum game cannot last.

Why has the window for price hikes arrived as scheduled?

The necessary condition for price hikes is not that automakers 'want to raise prices,' but that the entire cost-policy equation has been rebalanced.

On the cost side—lithium carbonate prices have doubled, memory chip prices have surged over 180%, and tires and other components continue to rise. On the policy side—the SAMR's 'Compliance Guidelines' define boundaries for pricing behavior, preventing below-cost dumping.

On the profit side—past price wars have drained the industry's lifeblood, making them strategically 'unaffordable' going forward.

This represents an unplanned yet logically inevitable 'price inflation.' Macroeconomics stands at a delicate moment: after a period of deflationary shadows, the state seeks to moderate inflation through gentle means. The auto industry serves as both the most sensitive conductor and the most proactive driver of this inflationary round.

Prices must ultimately return to value—this marks the spiritual coming-of-age for industrial upgrading.

China's auto industry gradually enters the era of price hikes in 2026, representing an 'overcorrection' toward pricing that reflects value. More bluntly, when countless models collapse under a 2.9% industry average profit margin, the industry must 'treat the root causes of cutthroat competition.'

The result of this round of price hikes may not necessarily lead to consumers bearing higher costs in the long term. This is because, at a sustainable profit level, automakers can maintain their R&D intensity, fulfill quality commitments, and create space to refine differentiated product value.

In a virtuous cycle of pricing ecology, consumers obtain reasonable value at appropriate prices, rather than indulging in the illusion that 'discounts will never end.'

However, the opportunity for price increases also brings with it a heightened sense of responsibility: automakers are now compelled to substantiate, through technological advancements and configuration enhancements, that as prices ascend, so does the value offered. From the integration of intelligence and pure electrification to the 'spatial efficiency' of spacious five-seaters, the automotive industry already boasts compelling selling points that justify premium pricing. Yet, the question remains: do consumers truly believe in this new value proposition? Their purchasing decisions, made with their hard-earned money, will ultimately determine whether the 'era of price hikes' is merely a passing fad or the new norm of the future.

06

Epilogue: What Rises Is Not Price, But Value

From the press conferences held on the eve of the Beijing Auto Show to the subtle shifts in car market prices in March and April, a distinct 'Spring Story' is unfolding.

When pure electrification dismantles the barrier of 'range anxiety,' when intelligence redefines the sense of safety and driving experience, when large vehicles cease to be mere pseudo-needs or 'vanity projects,' and when regulations institutionally shut down the path for 'suicidal low-price dumping'—a more rational value coordinate system is taking shape.

The proposition of the 'era of price hikes' is, at its core, not a penalty for Chinese car consumers but a challenging rite of passage for the industry. It marks the industry's transition from its adolescent phase, characterized by reliance on scale, price wars, and predatory expansion, to a mature stage that hinges on technology, quality, and brand trust.

We must contextualize the significance of this moment within a broader historical perspective. Chinese automobiles began their journey with the launch of the Santana in 1978, evolving from a phase of learning and imitation to a new era of independent R&D; from mass production dominated by joint ventures to an ecological reshaping led by Chinese autonomous brands in the market.

In this lengthy narrative, the 'price hikes' surrounding the 2026 Beijing Auto Show emerge as a symbolic turning point: they signify that Chinese automobiles can triumph in a dimension beyond mere cost-effectiveness—the pricing power at the mid-to-high end of the value chain.

The awakening of consumers is equally remarkable. They are no longer content to be passive recipients of price wars but instead make informed judgments based on three key dimensions: product strength, technological sophistication, and scenario suitability.

They would rather pay a premium for Huawei ADS 5, Horizon HSD, Momenta R7, DeepRoute IO from Rongxing Qihang, or the 900-kilometer range of CATL/BYD batteries than squander their hard-earned money on a product that is 'cheap and nothing else.'

The cyclical fluctuations in oil prices, the new high in new energy penetration rates, the breakthrough of Chinese autonomous brands' market share beyond 55%, and the 1,451 vehicles on display at the Beijing Auto Show... All these variables collectively narrate the same tale:

Chinese automobiles are undergoing a profound conceptual metamorphosis. Prices are no longer dictated by the depths of involution but are calibrated by the true value unlocked through technology, quality, and scenarios.

The era of price hikes has dawned. If one inquires whether this trend is sustainable, the answer may lie in the long and arduous journey of the Chinese automotive industry towards the global pinnacle.

Perhaps, when we look back years from now, the starting line for the true ascent of Chinese automobiles will be, in terms of technology, the 'lane change and overtaking' achieved through electrification and intelligence, while in terms of business, it will be in the spring of 2026 when 'everyone feels that cars have become more expensive.'

After all, it is when an industry finally possesses the capability and confidence to proclaim to itself and the world—'I no longer sell cheap; I only sell what is worth it.'

Editor in Charge: Yang Jing Editor: He Zengrong

THE END

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’