BYD’s Profits Take a Hit

04/30 2026

04/30 2026

441

441

On the day the 250,000-yuan BYD Datang made its debut, the auto discussion group hosted by Xingkongjun was abuzz with excitement.

Messages poured in—some sharing technical specifications, others crunching numbers on cost-effectiveness, and a few even placing orders. What began as a simple product launch soon transformed into a carnival-like event, drawing in the public.

The main topic of conversation was unmistakable: this car’s cost-effectiveness had left its competitors in the same category “utterly humbled.”

Orders skyrocketed, surpassing 30,000 within just 24 hours.

Xingkongjun recalled his often-repeated joke: “Don’t mess with BYD.”

Whether facing rival auto brands or the industry’s pricing norms, no one could remain unfazed by its “arsenal of price cuts.”

But just as everyone was celebrating the Datang’s explosive popularity, BYD’s Q1 2026 financial report poured cold water on the enthusiasm: revenue was down, and net profit had been “cut in half.”

What exactly was happening to BYD, the shining star among Chinese new energy vehicle brands?

1

From High-Speed Growth to a Controlled Slowdown

Let’s first take a look at BYD’s 2025 performance.

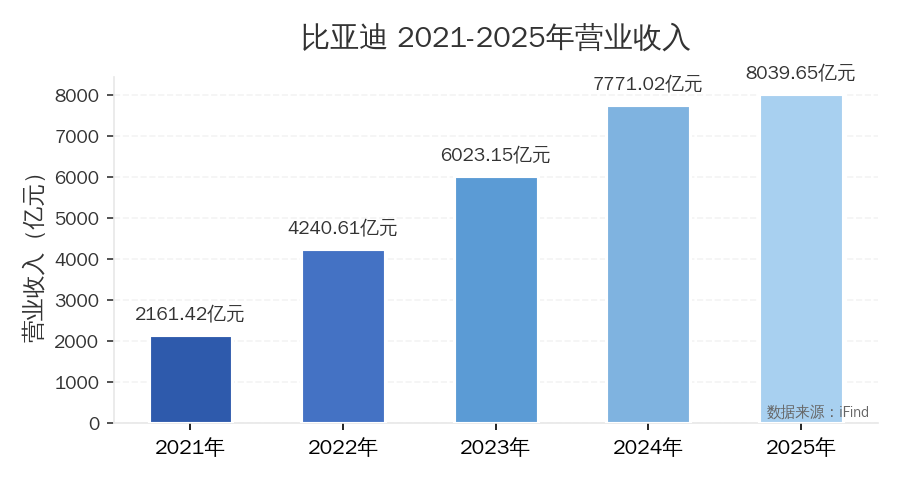

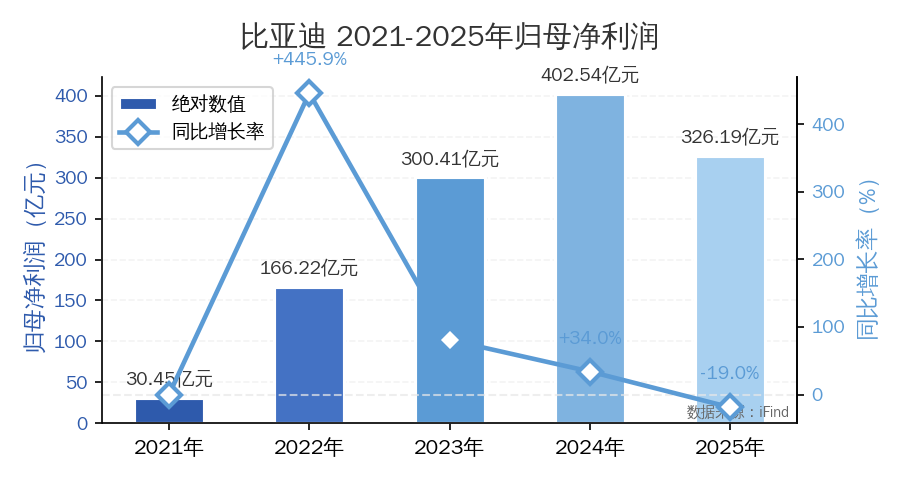

Annual revenue reached 803.965 billion yuan, up just 3.46% year-on-year. This growth rate, which was 29% two years ago and 38% three years ago, marked a significant slowdown. Net profit attributable to shareholders fell 18.97% to 32.619 billion yuan—the first negative growth since 2021. Net profit after non-recurring items dropped even more sharply, by 34.12%, signaling a clear slowdown in profit quality.

Of course, judging solely by growth rates is somewhat unfair. At the 800-billion-yuan revenue scale, every 1% increase represents tens of billions in additional income.

But capital markets are focused on growth momentum. When this momentum shifts from high to low, the valuation logic undergoes fundamental changes.

Why this “convergence”? The answer lies in three key factors.

First, the base has grown to an enormous size.

Jumping from 400 billion to 60 billion, 70 billion, and now 80 billion yuan in revenue while maintaining high growth is an “extreme challenge.”

Even global auto giant Toyota saw its growth naturally slow after hitting 10 million annual sales. This isn’t a BYD-specific issue but the inevitable fate of all industry giants.

Second, the price war rages on.

From 2024 to 2025, China’s new energy vehicle market engaged in a fierce price war. Tesla slashed prices multiple times, and domestic brands followed suit to gain market share. BYD couldn’t remain untouched.

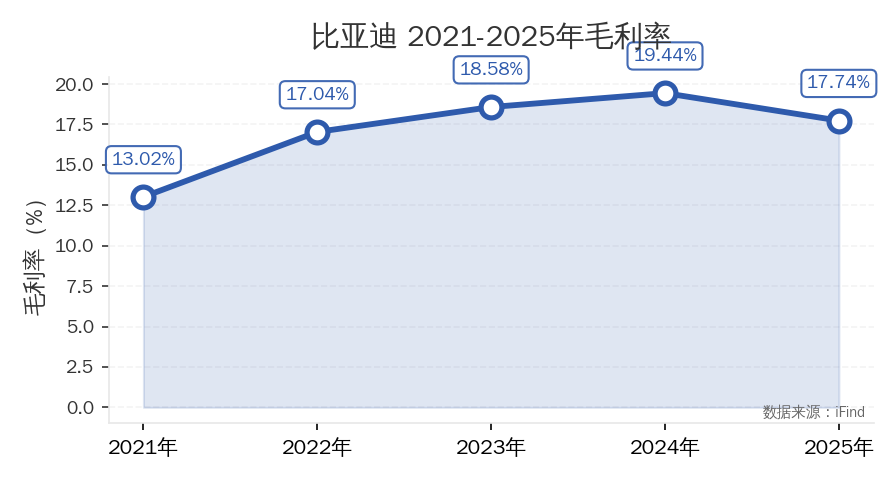

The cost of this chaos directly impacted gross margins. In 2025, the annual gross margin was 17.74%, down 1.7 percentage points from 19.44% in 2024. While seemingly small, this translated to billions in lost profit at the 800-billion-yuan revenue scale.

Third, the mobile components business has hit a “ceiling.”

Little-known outside the industry: BYD is also one of the world’s largest consumer electronics assemblers, manufacturing phones for Huawei and Xiaomi and iPads for Apple.

In 2025, this segment generated about 155.237 billion yuan in revenue, slightly down from 159.6 billion yuan in 2024. With the global smartphone market nearing saturation, significant growth is unlikely. Worse, price fluctuations in core components like chips squeezed margins further.

2

Q1 Report: Gross Margin Rebounds, But Profits Are Cut in Half

If the 2025 annual report showed “deceleration,” the Q1 2026 report marked a “sharp downturn.”

Quarterly revenue declined year-on-year, and net profit plummeted 55.38%.

Yet, the gross margin rose 1.4 percentage points sequentially to 18.81%—the highest in nearly a year. This critical signal suggests BYD’s core business remains healthy, with no deterioration in its ability to generate profits from main operations. In industry terms, “profit efficiency” is recovering, even if “profit scale” has shrunk.

Why did profits halve despite margin gains?

Two primary reasons:

1. Foreign exchange losses from overseas operations. BYD’s global investment in production bases—in Europe, Southeast Asia, and South America—created significant currency fluctuation losses. With overseas revenue exceeding 38% of total revenue, exchange rate impacts were amplified.

2. Revenue contraction. When revenue falls, fixed costs cannot be cut proportionally. Rigid expenses like sales, R&D, and administrative costs further compressed profit margins.

This indicates BYD’s core competitiveness remains intact. The Q1 profit decline stems more from “external shocks” than “internal decay.”

3

Cash Flow: A Key Metric to Watch

Generally, quarterly cash flow statements offer limited insight due to settlement cycles. Most companies collect payments at year-end, causing volatile quarterly data. However, BYD’s Q1 cash flow statement demands extra attention.

The trend is too striking.

In Q1 2026, net cash from operating activities was just 2.79 billion yuan. For context: the same period in 2024 saw hundreds of billions in cash flow. Now, it’s below 3 billion yuan.

Two factors explain this:

1. Global production base investments. BYD is building complete vehicle or assembly plants in Europe, Southeast Asia, and South America. These projects require heavy upfront investment, with returns materializing later. While classified as investing cash flows, they also generate significant operating cash outflows—like a homeowner facing massive renovation costs before enjoying the new space.

2. Rapid capacity expansion. With 4.6024 million vehicles sold in 2025, BYD’s breakneck expansion demanded massive capital expenditures, driving operating cash outflows. Each new energy vehicle production base across China acts as a “cash drain,” requiring sustained funding before capacity is fully utilized.

4

Business Scope

The automotive business is BYD’s undisputed core. In 2025, it generated 648.646 billion yuan in revenue, accounting for 80.68% of total revenue, with a gross margin of 20.49%.

However, automotive growth is slowing. Annual sales reached 4.6024 million units, up just 7.8% from ~4.27 million in 2024—a marked slowdown from previous “explosive” growth.

The mobile components and assembly business is gradually declining, a natural outcome as the global smartphone market saturates.

5

Overseas Success

BYD’s overseas revenue is soaring: 160.2 billion yuan (26.60% of total) in 2023, 221.9 billion yuan (28.55%) in 2024, and 310.741 billion yuan (over 38%) in 2025.

In 2025, complete vehicle exports surpassed 1 million units, up 140% year-on-year, topping China’s new energy vehicle export list—a milestone.

In Q1 2026, overseas sales hit ~320,000 units, up 55% year-on-year, with a presence in 120 countries and regions and cumulative exports exceeding 2.08 million units.

These figures mark BYD’s firm stride from a “Chinese brand” to a “global brand.”

BYD’s overseas strategy has evolved into product exports + localized production. Beyond selling cars, it builds factories, R&D centers, and charging networks locally. This “deep localization” model, though costly and time-consuming, minimizes policy risks and transportation costs.

BYD’s overseas triumph offers a replicable path for Chinese auto brands. Historically, Chinese cars relied on “low-price gimmicks” abroad. BYD proves that Chinese automakers can gain a foothold overseas through a “technology + brand + service” trifecta.

-END-

Disclaimer: This article is based on the public company attributes of listed companies and relies primarily on information disclosed by them in accordance with legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms). Shiyu Xingkong strives for fairness in content and viewpoints but does not guarantee accuracy, completeness, or timeliness. The information or opinions expressed herein do not constitute investment advice, and Shiyu Xingkong assumes no responsibility for actions taken based on this article. Copyright Notice: This article is original content by Shiyu Xingkong and may not be reproduced without authorization.

-

![]()

Is Zhipu's Trillion-Yuan Market Cap, Despite No Profit, Truly 'Outrageous'?

-

![]()

XiaoPai Unveils Home AI Brain, Paving the Way for Smart Homes to First Grasp 'Home Understanding'

-

![]()

Is the Future of Extended-Range EVs Pure Electric or Li Auto’s 5C Extended-Range? A Li Auto Executive Shares Insights

-

Ant Group’s New Board of Directors: Signaling a New Era?

-

![]()

Google Initiates TPU Sales, as Industry Leaders Eye AI Chips for 'Cost-Effective Tokens'

-

![]()

Input Methods: The Rising Star in AI! WeChat, Doubao, and Qianwen Lead the Charge into the Voice Input Era

-

![]()

Struggling to Sell? Cut It Out! Toyota, Volkswagen, and Changan Lead the Charge in Streamlining, Eliminating Non-Core Products in the Blockbuster Model Era

-

![]()

Arm China and Volcano Engine Join Forces to Expedite Cloud Computing and AI Infrastructure Rollout