Geely: Net Profit Per Vehicle Catches Up with BYD, Is Geely Mounting a Major Comeback?

04/30 2026

04/30 2026

575

575

Geely Auto released its Q1 2026 report during the Hong Kong Stock Exchange lunch break on April 29, 2026 (Beijing Time). Overall, while reported revenue and net profit attributable to the parent company fell short of expectations, core metrics such as gross margin and operating profit per vehicle rose against the trend, demonstrating strong operational resilience:

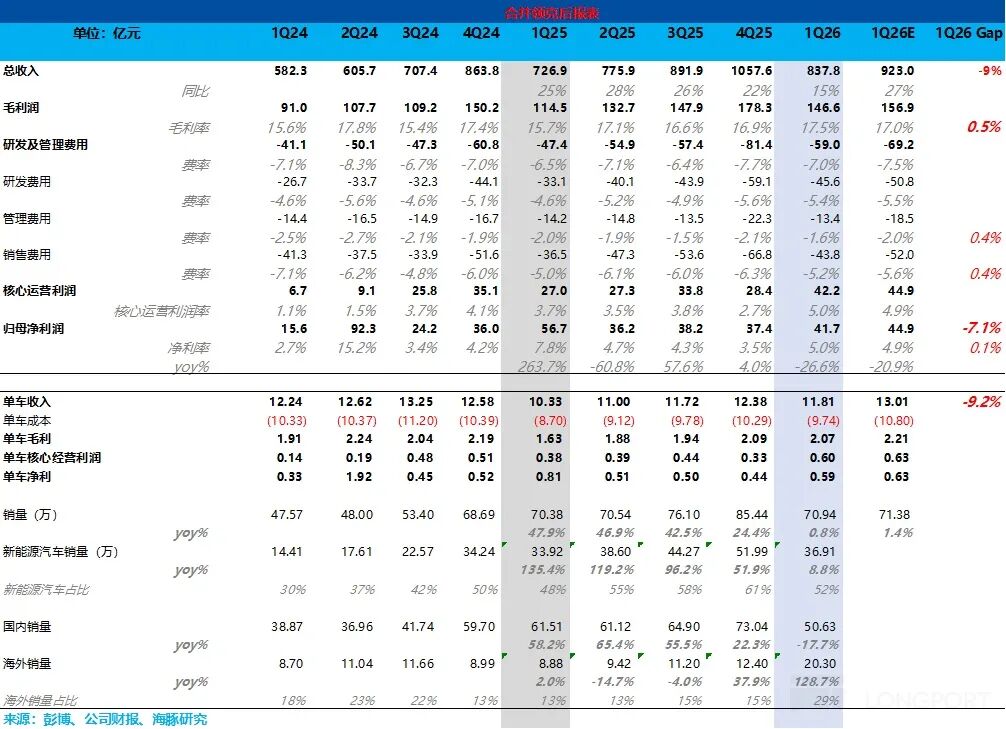

1. Total revenue slightly below expectations, but ASP per vehicle remains stable: Geely Auto's total revenue for the quarter was RMB 83.8 billion, up 15% YoY but below market expectations of RMB 92.3 billion.

The market's primary concern was a potential sequential decline in ASP per vehicle, especially given increased contributions from premium brands (Zeekr) and overseas sales this quarter.

However, the revenue shortfall was not due to weak core automotive operations but rather a decline in component sales and external technology licensing revenue (e.g., battery sales to Volvo). Actual vehicle ASP remained flat QoQ compared to Q4 2025.

2. Vehicle revenue flat QoQ but up sharply YoY: The actual vehicle ASP in Q1 2026 was RMB 112,000, up 18.3% from RMB 94,000 YoY. The increase was driven by higher contributions from premium brands and overseas sales, which lifted average selling prices.

The flat QoQ trend was mainly due to temporary promotions by the Lynk & Co brand offsetting positive impacts from structural optimization (higher premium + overseas sales mix).

Breakdown by brand:

a. Zeekr ASP (upward): Rose from RMB 281,000 YoY to RMB 295,000-300,000 in Q1 2026, driven by strong sales of the premium Zeekr 9X model (priced at RMB 400,000-500,000, with over 10,000 units sold in March alone).

b. Geely brand ASP (upward): Increased from RMB 85,000 YoY to RMB 91,000, driven by accelerated new energy transition and the premium breakthrough led by the Galaxy M9 model.

c. Lynk & Co ASP (slight YoY decline): Partly due to a sequential drop in sales of the high-priced Lynk & Co 900 model and promotional discounts of up to RMB 46,000 on models like the 01, 06, 07, and 08 EM-P.

3. Gross margin improved sequentially against the trend: In Q1, Geely's overall gross margin was 17.5%, up 0.6 percentage points QoQ and exceeding market expectations of 17%. Dolphin Research attributes this to:

a. Surge in overseas sales: Q1 overseas sales reached 203,000 units, up 130% YoY, with their share of total sales jumping from 13% to 29%. The high-margin nature of overseas models was the primary driver of overall gross margin recovery.

b. Strong sales of premium brands: Zeekr sold 77,000 units in Q1 (+34% YoY), with its sales share rising 4 percentage points to 11%. The high-margin Zeekr 9X model provided significant support.

c. Withstanding “negative scale effects” and cost pressures: Domestic NEV purchase tax incentives phased out, leading to a 17.7% YoY decline in domestic sales (to 506,000 units) and a 17% QoQ drop in total sales (709,000 units), creating negative scale effects.

Coupled with rising commodity prices (lithium carbonate, copper, aluminum, etc., adding ~RMB 2,000 to per-unit costs), gross margins faced pressure. However, aggressive cost-cutting measures (nearly 80% of Q1 cost-reduction targets achieved, with full compliance expected in Q2) successfully offset these headwinds.

Looking ahead to Q2, with deliveries of the Zeekr 8X driving further premiumization, Geely expects gross margin to remain stable or increase slightly QoQ.

4. Early success of “One Geely” integration: Significant optimization of operating expenses: Despite incomplete leverage from sales growth, total operating expenses (R&D, selling, and administrative) in Q1 were just RMB 10.3 billion, down 31% QoQ (from RMB 14.8 billion last quarter), with the expense ratio declining 1.7 percentage points to 12.3%.

R&D expenses: Down RMB 1.35 billion QoQ to RMB 4.56 billion, well below market expectations of RMB 5.08 billion. Notably, this was achieved despite a further increase in the R&D expense ratio to 44% (Q1 2025: 28.5%; full-year 2025: 36%), indicating a contraction in actual total R&D investment. This suggests completion of core new product development and cost-saving synergies from the integrated R&D system.

Selling expenses: Nearly RMB 4.4 billion this quarter, down sharply QoQ (from RMB 6.7 billion last quarter) and below expectations of RMB 5.2 billion. This was likely due to reduced marketing spending in the low season and synergies from internal organizational integration.

5. Core operating profit per vehicle doubled, on par with BYD: Benefiting from margin expansion driven by “overseas expansion + premiumization” and sharp expense reductions from “One Geely” integration, core operating profit per vehicle surged from RMB 3,300 last quarter to nearly RMB 6,000, matching BYD's level (which had a higher overseas sales mix of 46% in Q1 2026).

Total core operating profit reached RMB 4.22 billion, up 49% QoQ (56% YoY), with the operating profit margin rising 2.3 percentage points to 5%.

6. Net profit attributable to the parent company declined sharply YoY, mainly due to exchange rate impacts: Q1 net profit was RMB 4.17 billion, down 26.6% YoY. This was primarily driven by non-core business disturbances: (1) A high base effect from significant foreign exchange gains in the prior year (financial expenses rose ~RMB 3.1 billion YoY); (2) Proactive increases in the R&D expense ratio suppressed apparent current-period profits (if the Q1 2025 expense ratio had been maintained, net profit would have exceeded RMB 5 billion). Overall, financial reporting became more prudent, and core financial health remained strong.

Dolphin Research's View:

On the surface, Geely's Q1 results appeared below expectations, with revenue and profit under pressure. However, this was primarily due to non-core revenue declines, a high base from prior-year foreign exchange gains, and proactive increases in the R&D expense ratio—all non-operational factors.

Beneath the surface, Geely's core automotive business continued to improve. Driven by “premiumization and overseas expansion,” the company not only stabilized ASP per vehicle in a challenging market but also significantly improved gross margins. Meanwhile, the “One Geely” strategy began delivering substantial cost synergies and efficiency gains.

In terms of profit release, Geely's core operating profit per vehicle surged from RMB 3,300 last quarter to nearly RMB 6,000 this quarter. Notably, with an overseas sales mix of 29% in Q1 (still lower than BYD's 46%), Geely's per-vehicle profit matched BYD's level.

Additionally, core operating profit rose 49% QoQ, with the operating profit margin increasing 2.3 percentage points to 5%. Geely's profit structure has substantially optimized, entering a high-quality, organic growth phase.

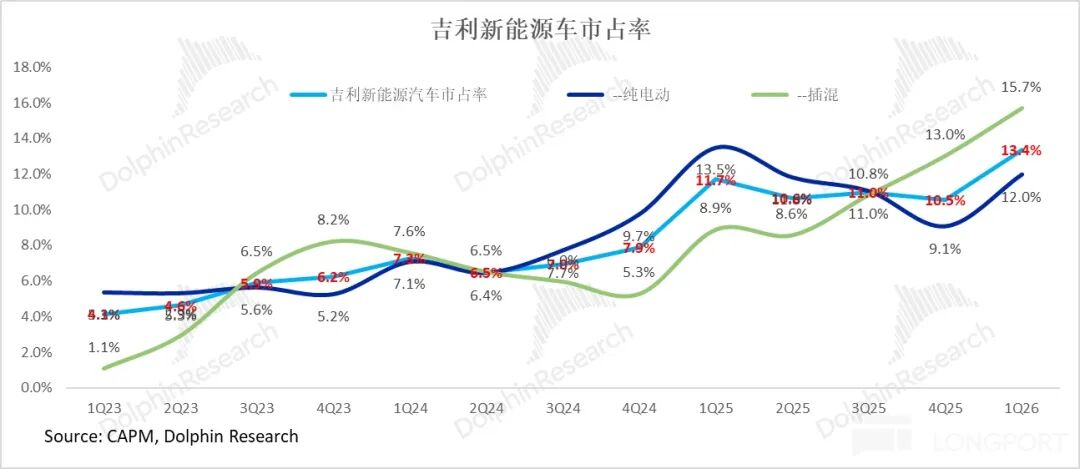

Critically, in new energy transition acceleration, Geely's NEV sales grew 9% YoY to 369,000 units in Q1, despite phased-out purchase tax incentives and a 5% YoY decline in industry-wide NEV sales.

Its NEV penetration rate rose to 52%, up 4 percentage points YoY, while domestic NEV market share jumped from 10.5% in Q4 2025 to 13.4%. The accelerated transition signals that 2026 marks Geely's official entry into a “new energy-driven” development phase.

Breakdown by brand:

a. Galaxy series: Q1 NEV sales were 114,000 units, down 9.5% YoY, mainly due to the impact of phased-out purchase tax incentives, with weaker performance in mid-to-low-end models. However, product mix adjustments are underway, with the Galaxy Starship 7, Galaxy E5, and Galaxy A7 becoming sales mainstays, and the launch of the Galaxy M9 effectively driving premiumization.

b. Lynk & Co brand: NEV sales grew 33.8% YoY to 51,000 units, with NEV models accounting for 62% of total brand sales (up 10 percentage points YoY). The rapid transition was driven by strong sales of the Lynk & Co 900 and 08 models.

c. Zeekr brand: NEV sales surged 85.8% YoY to 77,000 units, led by the Zeekr 7X and 9X. Zeekr's premiumization (especially the blockbuster success of the 9X) further lifted ASP and gross margins.

Overall, Geely's Q1 NEV sales reached 369,000 units, up 9% YoY. Due to the traditional low season in Q1, this represents 16.6% of the 2026 full-year sales target of 2.22 million units.

Looking ahead to Q2, despite pressure from rising commodity prices (lithium, copper, aluminum, etc., adding ~RMB 2,000 to per-unit costs), the launch of the Zeekr 8X will further unleash premiumization momentum, effectively offsetting cost pressures. The company expects gross margin to remain stable QoQ or even increase slightly in Q2.

For 2026 as a whole:

Geely is entering a phase of strong “Davis Double Play,” poised to deliver alpha performance: High-margin businesses (premiumization and overseas expansion) will continue to boost profits (lifting EPS), while accelerated new energy transition will raise valuation ceilings (elevating PE).

① Profit Driver 1: Sustained strong product cycle, premiumization drives ASP upward

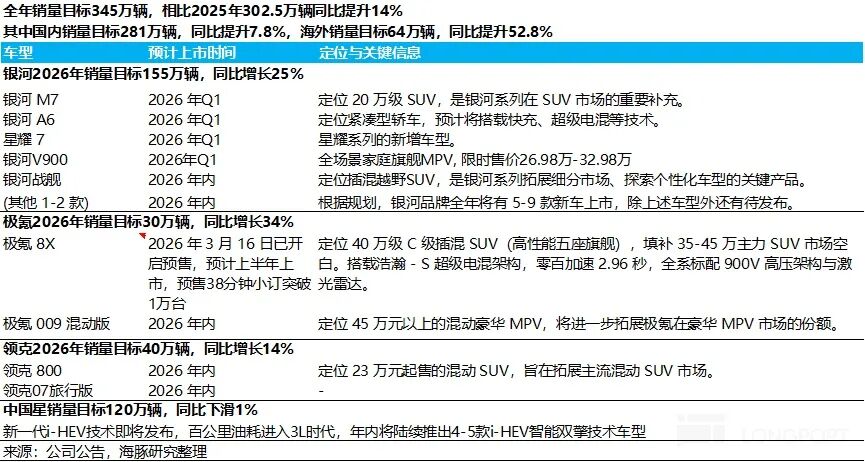

The company has set a 2026 total sales target of 3.45 million units, up 14% YoY, with growth driven by “NEV-led and overseas expansion” characteristics.

NEV sales target: 2.22 million units (+32% YoY), with NEV penetration rising 8.5 percentage points YoY to 64%. Fuel vehicle sales target: 1.23 million units (-8% YoY).

Brand-specific plans: Geely will launch nearly 10 new models in 2026 to achieve these targets:

Geely Galaxy (volume foundation): NEV sales target of 1.52 million units (+23% YoY), relying on models like the M7 and Xingyao 7 to consolidate mainstream market position.

Zeekr (premium profit driver): Sales target of 300,000 units (+34% YoY), with growth driven by the Zeekr 8X (launched in April) ramp-up and sustained strong sales of the 9X. The 8X received over 10,000 pre-orders in 38 minutes, and its leading architecture (shared with the 9X) positions it to become a blockbuster in the luxury full-size SUV segment, forming a high-end portfolio with the 9X to boost brand ASP and margins significantly.

Lynk & Co: Sales target of 400,000 units (+14% YoY), driven by NEV transition (penetration now exceeds 60%) and new models like the Lynk & Co 800.

② Profit Driver 2: Overseas market explosion delivers highest profit elasticity

Overseas markets have become Geely's highest-certainty and most profit-elastic growth area in 2026. The company raised its 2026 overseas sales target to 750,000 units (+79% YoY). Given Q1 2026 exports already reached 203,000 units (+129% YoY), annualized exports exceed 800,000 units, suggesting the target will likely be exceeded.

The high-profit nature of overseas sales is key to boosting group profits: Compared to 2025 data, overseas ASP (RMB 176,500) was 1.7x domestic ASP, with gross margins ~10 percentage points higher and per-unit net profit nearing RMB 10,000. With accelerated overseas channel expansion (planned to exceed 2,200 outlets) and rising NEV export share (expected to reach 45-50%), overseas operations will be the primary profit driver.

③ Cost-efficiency foundation: “One Geely” unleashes systemic synergies

With Zeekr's privatization completed by late 2025, the “One Geely” strategy entered full implementation. Deep integration of R&D, procurement, manufacturing, and management platforms will significantly reduce overall operating costs. Q1 results already showed early benefits, and 2026 full-year selling, administrative, and R&D expense ratios are expected to continue declining, safeguarding profit release.

New energy transition accelerates PE expansion:

Based on Geely's strong fundamentals in “overseas expansion + premiumization,” Dolphin Research expects total 2026 sales to reach 3.5 million units (750,000 overseas, +79% YoY; 2.75 million domestic, +5% YoY). Driven by product mix upgrades (higher premium + overseas sales mix) and cost efficiencies, core net profit per vehicle is expected to rise 13% YoY to RMB 6,300-6,600.

A more detailed valuation analysis is available in the same name article under the「Dynamic-Deep Dive」section of the Longbridge App.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general reference only, intended for users of Dolphin Research and its affiliates for informational purposes. It does not consider the specific investment objectives, product preferences, risk tolerance, financial condition, or unique needs of any individual recipient. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referring to the content herein are at the investor's own risk. Dolphin Research assumes no liability for any direct or indirect losses arising from the use of this report. The information and data herein are based on publicly available sources and are provided for reference only. Dolphin Research strives but does not guarantee the reliability, accuracy, or completeness of such information and data.

The information mentioned or the opinions expressed in this report shall not be considered or deemed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor shall they constitute advice, solicitation, recommendation, etc. regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution, publication, provision, or use would be contrary to applicable laws or regulations or would result in Dolphin Research and/or its subsidiaries or affiliates being subject to any registration or licensing requirements in such jurisdiction.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Is Zhipu's Trillion-Yuan Market Cap, Despite No Profit, Truly 'Outrageous'?

-

![]()

XiaoPai Unveils Home AI Brain, Paving the Way for Smart Homes to First Grasp 'Home Understanding'

-

![]()

Is the Future of Extended-Range EVs Pure Electric or Li Auto’s 5C Extended-Range? A Li Auto Executive Shares Insights

-

Ant Group’s New Board of Directors: Signaling a New Era?

-

![]()

Google Initiates TPU Sales, as Industry Leaders Eye AI Chips for 'Cost-Effective Tokens'

-

![]()

Input Methods: The Rising Star in AI! WeChat, Doubao, and Qianwen Lead the Charge into the Voice Input Era

-

![]()

Struggling to Sell? Cut It Out! Toyota, Volkswagen, and Changan Lead the Charge in Streamlining, Eliminating Non-Core Products in the Blockbuster Model Era

-

![]()

Arm China and Volcano Engine Join Forces to Expedite Cloud Computing and AI Infrastructure Rollout