Samsung Withdraws, Joint Venture Automakers Brace for Battle

05/12 2026

05/12 2026

566

566

Will the narrative of Samsung’s departure from the home appliance sector repeat itself in the realm of joint venture automotive manufacturing? On May 6, 2026, Samsung Electronics announced on its official website the cessation of sales for all home appliance products in mainland China, encompassing TVs, refrigerators, washing machines, and air conditioners. A brand that once reigned supreme in China’s TV sales for over a decade witnessed its market share plummet from nearly 20% at its zenith to a mere 3.54% in offline TV sales, 0.41% for refrigerators, and 0.37% for washing machines. Unable to withstand the competition, Samsung opted to withdraw.

Reflecting on the past few years, joint venture automakers have followed a strikingly similar trajectory to Samsung. Once dominant in the Chinese market through technological superiority and brand prestige, they have been progressively eclipsed by local brands capitalizing on cost-effectiveness and rapid technological innovation, leading their market shares to new nadirs. The key distinction is that while Samsung chose to bid adieu, joint venture automakers are mounting a counteroffensive.

A Familiar Tale: From Dominance to Decline

Samsung Home Appliances’ downfall in China can be succinctly summarized: products failed to keep pace, prices remained stubbornly elevated, and understanding of Chinese consumers was perpetually misaligned.

Industry insiders highlight that Samsung’s home appliance pricing has long been inflated, with similarly configured models costing 30–50% more than local brands. Concurrently, its localization efforts lagged behind the evolving needs of Chinese households. Technologies introduced by local brands in 2021 were only broadly implemented by Samsung in 2022. Product designs adhered to European and American large-household templates, appearing out of sync in China’s compact kitchens and small balconies. Furthermore, Samsung’s smart systems failed to integrate with China’s dominant smart ecosystems—for instance, households utilizing Xiaomi smart home devices found Samsung TVs felt like outsiders, unable to join the conversation. Data from CINNO Research reveals that Samsung’s TV market share in China remained below 2% from 2020 to 2025, while local brands collectively surpassed 90%.

This narrative mirrors that of joint venture passenger vehicles almost perfectly. In 2020, joint venture brands held 64.3% of China’s passenger vehicle market share; five years later, this figure dwindled to 35.4%, overtaken by domestic brands. By the first quarter of 2026, their share further plummeted to 24.9%—a halving from majority dominance to less than a quarter in five years.

Joint venture vehicles and Samsung Home Appliances share a common flaw: Chinese consumers now anticipate new energy vehicles (NEVs) with ranges exceeding 800–900 kilometers, high-level autonomous driving under RMB 200,000, and smart cockpits seamlessly connected to mobile ecosystems. Many joint venture NEVs still rely on platforms adapted from internal combustion engine vehicles, offering uncompetitive ranges and outdated infotainment systems compared to domestic rivals’ offerings, which feel like products from a bygone era. The mid-size sedan market, once a profit cornerstone for joint ventures at the RMB 200,000 price point, now sees mainstream models transact below RMB 150,000.

Like Samsung Home Appliances, joint venture automakers’ sluggish adaptation stems from excessively long decision chains and sluggish responses. Samsung’s product definition and decision-making authority for home appliances were highly centralized at its South Korean headquarters, often lagging behind market changes in China. Similarly, joint venture automakers adhered to decades-old practices of “overseas finalization, domestic modification.” New vehicle development projects originated in Wolfsburg, Germany, or Aichi, Japan, and by the time they reached China, domestic brands had already iterated multiple generations.

No More Illusions: Adapt or Exit

Faced with sustained losses, the choices are stark: either cut losses and exit gracefully like Samsung, or fully adapt and restart.

Samsung opted for the former. In 2025, its Imaging Display and Consumer Electronics divisions collectively incurred losses of approximately KRW 200 billion, while its semiconductor business soared, delivering KRW 57.2 trillion in operating profit in Q1 2026 alone. The stark contrast prompted Samsung to ax its consumer appliance retail operations and double down on semiconductors and AI computing. Samsung also clarified that its Chinese factories would remain operational, with Suzhou’s production lines repurposed as export hubs for North America and Southeast Asia.

The automotive sector followed a similar path. In 2025, mainstream joint venture brands sold 5.77 million units, with market share collapsing from 51% in 2020 to 24%. Their NEV segment fared even worse: combined sales of all joint venture NEVs reached just 553,000 units, accounting for a mere 4.43% share in a market where NEV penetration exceeded 50%.

Leading players like Volkswagen Group and Toyota (FAW-Volkswagen and GAC Toyota) clung to baselines of 1 million units. In 2025, FAW-Volkswagen sold 1.5871 million units to retain the top joint venture spot, while the Volkswagen duopoly accounted for nearly one-third of joint venture sales. However, French brands saw their market share plummet to 0.2%, and Korean brands barely held 1%. Hyundai and Kia’s combined domestic terminal sales reached just ~207,000 units, with NEV monthly sales lingering in the hundreds. Skoda even announced it would halt new vehicle sales in China by mid-2026.

Even Volkswagen, with relatively stable shares, paid a visible price. In Q1 2026, Volkswagen delivered 548,700 units in China, down 14.8% YoY, with pure EV deliveries crashing 63.8% to just 9,400 units. Annual profit contributions from its Chinese JVs plummeted from €5.2 billion in 2014 to €958 million in 2025, with China’s profit share shrinking from nearly 30% to just over 10% in 11 years. In essence, Volkswagen sacrificed global profit growth to sustain its Chinese market presence.

However, a critical distinction remains between joint venture automakers and Samsung: decades of joint venture factories, hundreds of thousands of employees, nationwide dealer networks, and massive capacity investments cannot be severed overnight. Moreover, China is the world’s largest auto market—exiting means surrendering the future.

Beijing Auto Show Counteroffensive: Can Joint Venture 2.0 Succeed?

The 2026 Beijing Auto Show’s theme, “Lead the Era, Smart Future,” belies a reality: for multinational automakers, this era grows increasingly ambiguous.

At the show, joint venture brands signaled a unified shift: no more illusions, but no more half-measures either. Unlike previous editions, they abandoned internal combustion engine vehicle displays and showcased truly locally developed NEVs, challenging domestic brands on both price and specifications.

Volkswagen adopted the show’s most aggressive stance, hosting a brand night at Shougang Park half a month before opening, unveiling four global premieres and ten flagship models. The star was the ID.ERA 9X, a range-extended SUV developed exclusively for China, boasting over 1,651 km of combined range on full tanks and batteries. Its autonomous driving solution came from Momenta, and batteries from CATL. Volkswagen revealed the model secured over 10,000 pre-orders within an hour of launch—a figure previously exclusive to NEV startups. It also announced its Hefei VCTC R&D center gained full autonomous project approval, empowering 3,000+ local engineers to develop models without headquarters’ approval, with the CEA electronic architecture enabling an 18-month development cycle.

Nissan displayed two all-new PHEV concept cars, complementing its launched N-series SUV NX8, forming a China-focused SUV offensive. Nissan CEO Ivan Espinosa admitted that adapting global products for China no longer suffices. Nissan plans to launch five NEV models within a year and position China as a global innovation hub.

At the show, nearly all joint venture brands embraced local tech suppliers. Toyota’s bZ7 featured turnkey local supply chain collaborations: cockpit systems by Huawei, autonomous driving by Momenta, and electric drives by Huawei. GM integrated Momenta’s AV large model into core products; BMW’s Neue Klasse OS had 70% of its codebase developed and optimized by Chinese teams. The old joint venture logic—“technology from foreign partners, China as a production base”—is being rewritten.

The market has yet to deliver a verdict on these efforts’ efficacy. One thing is clear: joint venture brands aim to carve a path divergent from Samsung’s—not retreating, but adapting to stay.

Thus, the joint ventures’ collective counteroffensive at the auto show feels less like an offensive than a desperate self-preservation effort. The question remains: Can their self-rescue outpace market elimination? Three factors will decide this.

First, must price structures truly rationalize—Chinese consumers have voted with their wallets, proving that “brand premium” holds little sway in the NEV era.

Second, can localization R&D accelerate sustainably? True localization means Chinese teams dictate product definition and architecture, not just adopting local suppliers’ solutions.

Third, can intelligence gaps be closed? When RMB 100,000-class domestic NEVs offer high-level autonomous driving and seamless smart cockpits, joint venture products can no longer settle for “adequate.”

Epilogue

When news broke of Samsung’s Chinese exit, a retailer remarked, “Samsung never truly understood China.” The same held true for joint ventures five years ago. Fortunately, the Beijing Auto Show reveals that some have awakened to market realities—albeit late. The coming year’s localized NEV deliveries and market performance will likely determine who survives and who exits this cutthroat sector.

-

Kunlunxin, Backed by Baidu, Aims for Dual A+H Share Listing Amid RMB21 Billion Valuation Challenges

-

![]()

Apple’s Performance and Market Value Soar to New Heights: How Did It Get There?

-

![]()

Exploring the Distinctions Between Alibaba and ByteDance in AI-Driven E-commerce: The Comprehensive Integration of Qianwen with Taobao

-

![]()

Qianwen Revolutionizes Taobao: Alibaba's Bold Self-Transformation

-

![]()

What’s the Real Story? China Leads in 5G Patents but Pays More in Royalties!

-

![]()

8 Auto Companies Unanimously Deny 'Summons for Talks' Rumors, but OTA Battery Locking is Real

-

![]()

China’s Premier AI Infrastructure Provider Launches IPO, with Zhipu AI and SenseTime as Key Backers

-

![]()

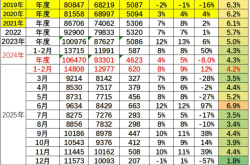

Have car prices gone up?