Have car prices gone up?

05/12 2026

05/12 2026

390

390

The 'Price War' Fizzles Out

The notion that 'car prices will only get cheaper' may need to be reconsidered.

Recently, several domestic new energy vehicle companies have raised the prices of their new cars. On April 28, BYD officially announced that the price of the 'Celestial Eye B' auxiliary driving laser version, an optional feature for certain models in its Dynasty, Ocean, and Fangchengbao series, would increase from 9,900 yuan to 12,000 yuan, a rise of 2,100 yuan. The new pricing will take effect on May 1. Just two days later, on April 30, Changan Qiyuan followed suit with a price adjustment announcement. Due to a significant increase in the global cost of automotive-grade chips, the official suggested price (recommended retail price) of the Qiyuan Q07 Shenshu Intelligent Laser Version produced after May 7 will increase by 3,000 yuan.

According to incomplete statistics, more than ten new energy vehicle companies have officially announced price hikes or reduced terminal discounts since the beginning of the year. Tesla's Model Y Long Range and Performance versions have increased by 18,000 yuan and 20,000 yuan, respectively. The new Xiaomi SU7 is 4,000 yuan more expensive than its predecessor. NIO, Zeekr, and XPeng have explicitly stated that new models in the second quarter will see price increases ranging from 5,000 yuan to 10,000 yuan.

The shift from a 'price war' to some automakers reducing market terminal discounts and officially announcing 'price increases for new cars' marks a reversal in the trend of the automotive market. Behind this reversal lies the industry's sustained pressure from profits nearing the break-even point and soaring costs of upstream raw materials and chips.

The pricing logic in the automotive market is undergoing a refactor (restructuring).

Industry Profits Near the Break-Even Point

Previously, the automotive industry's profit margin hovered around 8%, making it a 'high-quality track ( track , shàidào, refers to a competitive field or industry)' within the manufacturing sector. In recent years, while the scale of China's automotive market has continued to expand, industry profits have been on a downward trajectory.

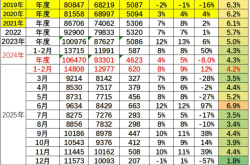

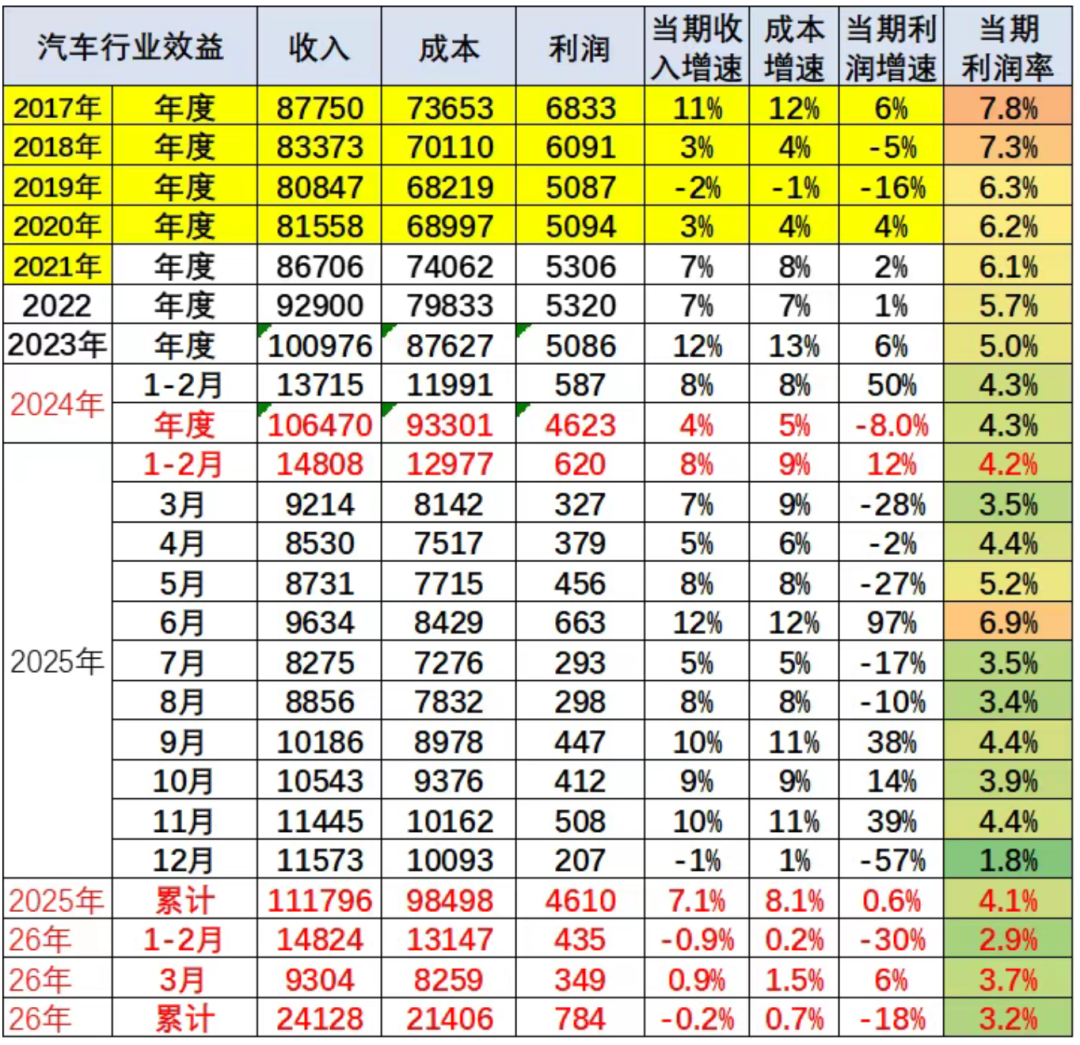

Chart source: Cui Dongshu, Secretary-General of the China Passenger Car Association

According to data disclosed by Cui Dongshu, Secretary-General of the China Passenger Car Association, from January to March 2026, the total profit of the domestic automotive industry was 78.4 billion yuan, a year-on-year decline of 18%, with the sales profit margin dropping to 3.2%, a low level for the same period in recent years. The automotive industry's profit margin is not only significantly lower than the average profit margin of industrial enterprises above a designated size nationwide but is also nearing the operating break-even point for the vast majority of vehicle manufacturers. The industry as a whole has entered a state of meager profits.

The three-year-long 'price war' is considered the core driver of the decline in automotive industry profits.

In recent years, automakers have generally adopted a strategy of 'trading price for volume' to seize market share, leading to a continuous decline in the terminal selling prices of mainstream models. Some models have seen price reductions exceeding 30%, directly causing a sustained contraction in gross profit per vehicle. As the 'price war' intensifies, the increase in volume can no longer offset the profit losses caused by price reductions.

Moreover, the stimulating effect of price reductions on sales is weakening. Data shows that from January to March this year, passenger vehicle production and sales reached 5.909 million and 5.934 million units, respectively, down 9.3% and 7.6% year-on-year. From a profit perspective, the first quarter of 2026 saw a further decline to 3.2%. In the previous January-February period, this figure was as low as 2.9%, a near-decade low.

Chart source: Cui Dongshu, Secretary-General of the China Passenger Car Association

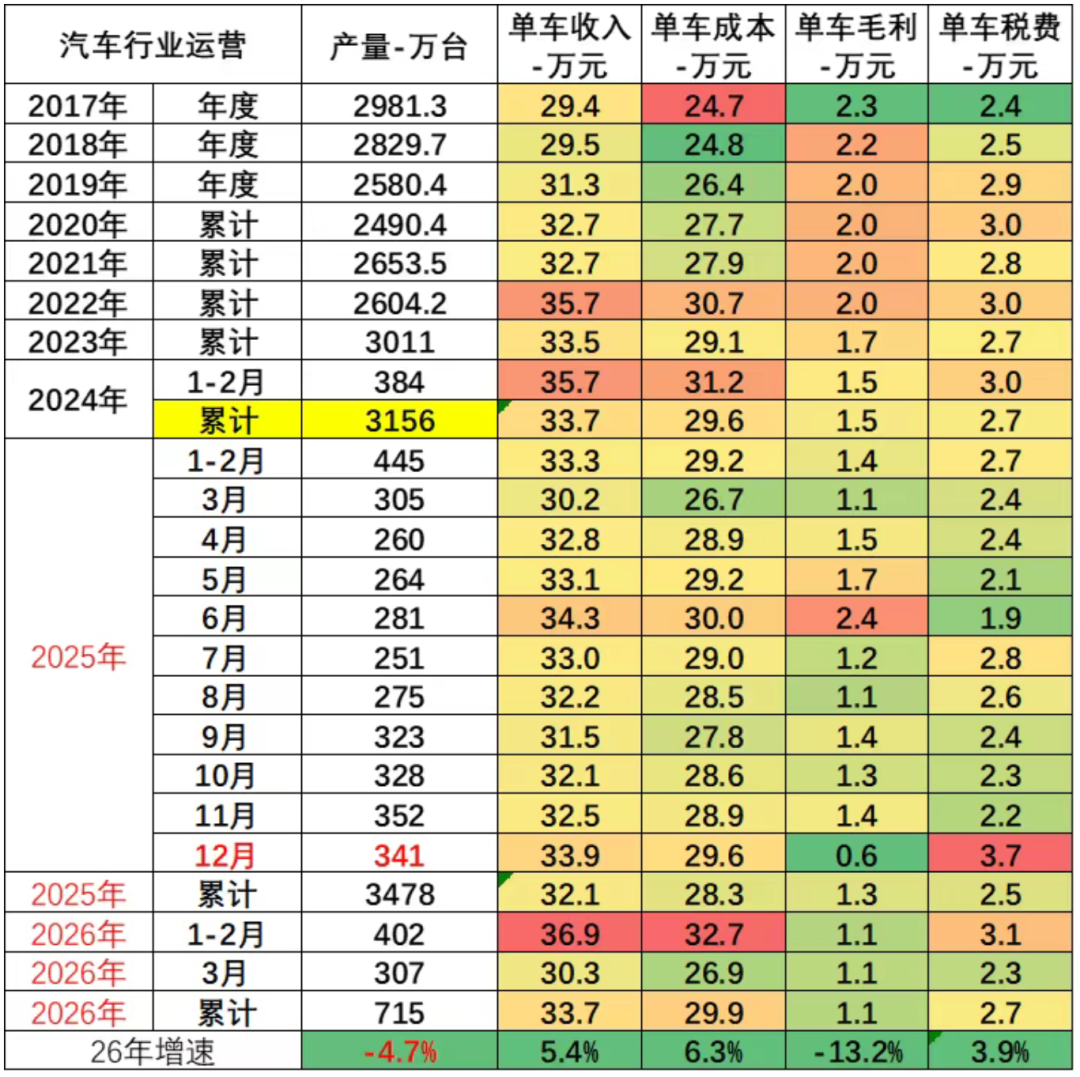

From the perspective of per-vehicle economic indicators, in the first quarter, the overall per-vehicle revenue of the automotive industry supply chain was 337,000 yuan, up 5.4% year-on-year; per-vehicle cost was 299,000 yuan, up 6.3% year-on-year; and the per-vehicle gross profit of the supply chain was 11,000 yuan, down 13.2% year-on-year. Although per-vehicle revenue has increased, cost growth has been faster, squeezing profit margins.

For small and medium-sized automakers, unrestricted price reductions have led to expanding losses, making price increases an inevitable choice to maintain normal production and operations. While leading automakers have scale advantages, they also face significant cost pressures. Precise price adjustments to transfer some of the cost pressures have become an important measure to balance profits.

Comprehensive Upstream Cost Increases

The industry's profits hitting rock bottom is a key reason for automakers to halt price reductions and opt for price adjustments. Meanwhile, the sustained rise in costs across the entire upstream supply chain has become a direct driver of the current round of price increases in the automotive market. Currently, from the core raw materials of power batteries and essential chips for intelligent vehicles to basic metal raw materials and automotive components, multiple cost pressures are superposition and transmitted downwards to the terminal market for complete vehicles.

The price of lithium carbonate, a core raw material for power batteries, is on a strong upward trajectory. Data shows that the average price of battery-grade lithium carbonate surged from 75,000 yuan per ton in July 2025 to approximately 170,000 yuan per ton in March 2026, a increase (increase) of over 125%. Power batteries account for 30%-50% of the cost of new energy vehicles. Calculating based on 600 grams of lithium carbonate needed per 1kWh of battery, for a medium-sized pure electric vehicle with an 80kWh battery, the increase in lithium carbonate prices alone adds about 4,500 yuan to the battery cost.

At the same time, the shortage and price hikes of automotive-grade chips have further exacerbated cost pressures. With the increasing penetration of automotive intelligence, configurations such as high-level auxiliary driving and intelligent cockpits have led to a surge in demand for chips. However, global semiconductor capacity has been heavily occupied by the AI computing power industry, resulting in longer supply cycles and soaring prices for automotive-grade chips. Data shows that in the past three months, automotive-grade DRAM prices have increased by 180% overall, with DDR5 prices rising by 300%. The increase in memory chip costs alone adds 1,000-3,000 yuan to the per-vehicle cost of medium-sized intelligent electric vehicles. Companies like NIO have revealed that chip costs for high-end models have increased by 3,000-5,000 yuan.

In addition, prices of basic commodities such as copper and aluminum have also fluctuated upwards. Producing a medium-sized electric vehicle requires 200 kilograms of aluminum and 80 kilograms of copper. Since 2026, aluminum prices have exceeded 25,000 yuan per ton, and copper prices have surpassed 100,000 yuan per ton. These two raw materials alone add about 1,800 yuan to the per-vehicle cost. Under the combined impact of multiple costs, the cost of medium-sized intelligent electric vehicles in 2026 has increased by 4,000-7,000 yuan compared to 2025, directly eroding the already thin profit margins of automakers.

Li Bin, founder, chairman, and CEO of NIO, stated at the High-Level Forum on Intelligent Electric Vehicle Development (2026): 'All chips, semiconductors, and batteries combined account for more than 50% of the cost of intelligent electric vehicles. A cost exceeding 50% for an automotive product is an uncontrollable situation.'

The cost pressures in the supply chain have also extended to automotive components such as tires. Since mid-April, the domestic tire industry has witnessed the second round of collective price hikes this year, with over 70 tire companies officially announcing price increases. The mainstream price increases for passenger car tires generally range from 2% to 5%. The reasons include drought in the main producing areas of natural rubber, which has limited production, and the surge in international crude oil prices, which has driven up the prices of synthetic rubber, with some varieties doubling in price. The price of carbon black and other chemical raw materials has increased by 13% in a single month due to environmental protection and production restriction policies. These multiple factors have pushed up the production cost of all-steel tires by nearly 7% in March compared to January. As high-consumption automotive components, tire price increases will also indirectly be transmitted to the production and after-sales links of complete vehicles, further aggravate (increasing) the industry's cost burden.

'Now, with the rapid increase in raw material prices, including chip and memory prices, it has indeed caused significant trouble for the entire supply chain and posed a huge challenge for cost control by vehicle manufacturers,' said Lu Fang, chairman and party secretary of VOYAH Automobile, in a media interview during the High-Level Forum on Intelligent Electric Vehicle Development (2026). 'The automotive industry or the entire value chain must ultimately generate profits, even if they are meager, to sustain operations. Therefore, I predict that if prices continue to rise, they will eventually be passed on to the terminal market, leading to an overall increase in car prices.'

From the current landscape, it will take time for the upstream lithium resource capacity to be released and for chip supply and demand to balance, making it difficult to reverse the high-cost trend in the short term. Meanwhile, industry profit recovery will also take time, leaving automakers with no room for further price reductions. As a result, the domestic automotive market may gradually bid farewell to disorderly low-price 'involution' and enter a new development phase characterized by price stabilization and localized moderate increases.

-

![]()

Exploring the Distinctions Between Alibaba and ByteDance in AI-Driven E-commerce: The Comprehensive Integration of Qianwen with Taobao

-

![]()

Qianwen Revolutionizes Taobao: Alibaba's Bold Self-Transformation

-

![]()

What’s the Real Story? China Leads in 5G Patents but Pays More in Royalties!

-

![]()

8 Auto Companies Unanimously Deny 'Summons for Talks' Rumors, but OTA Battery Locking is Real

-

![]()

China’s Premier AI Infrastructure Provider Launches IPO, with Zhipu AI and SenseTime as Key Backers

-

![]()

Have car prices gone up?

-

![]()

Samsung Withdraws, Joint Venture Automakers Brace for Battle

-

![]()

Nvidia Starts Adding Soap to the Bubble