Volkswagen's Q1 2026: The Painful Molting of a Giant

05/15 2026

05/15 2026

475

475

Amid an extremely volatile global automotive market, Volkswagen Group became the first traditional powerhouse to release its Q1 2026 results.

However, this report evokes mixed feelings. Some say Volkswagen has "held the line against the headwinds," while others argue it's merely "masking profit collapse with cash flow." Both views hold merit. From halved operating profits to sustained pressure in the Chinese market, and the ambitious launch of 'Vision 2030,' Volkswagen is not just explaining its past to Wall Street but declaring to the world: This slow-moving giant is shifting gears.

This article delves into Volkswagen's Q1 2026 financial performance, transformation strategy, and global competitive landscape to understand where this automotive empire selling nearly 9 million vehicles annually has stumbled and how it plans to recover.

01 Q1 Financial Performance

Face saved, but underwear showing

[Three Core Figures]

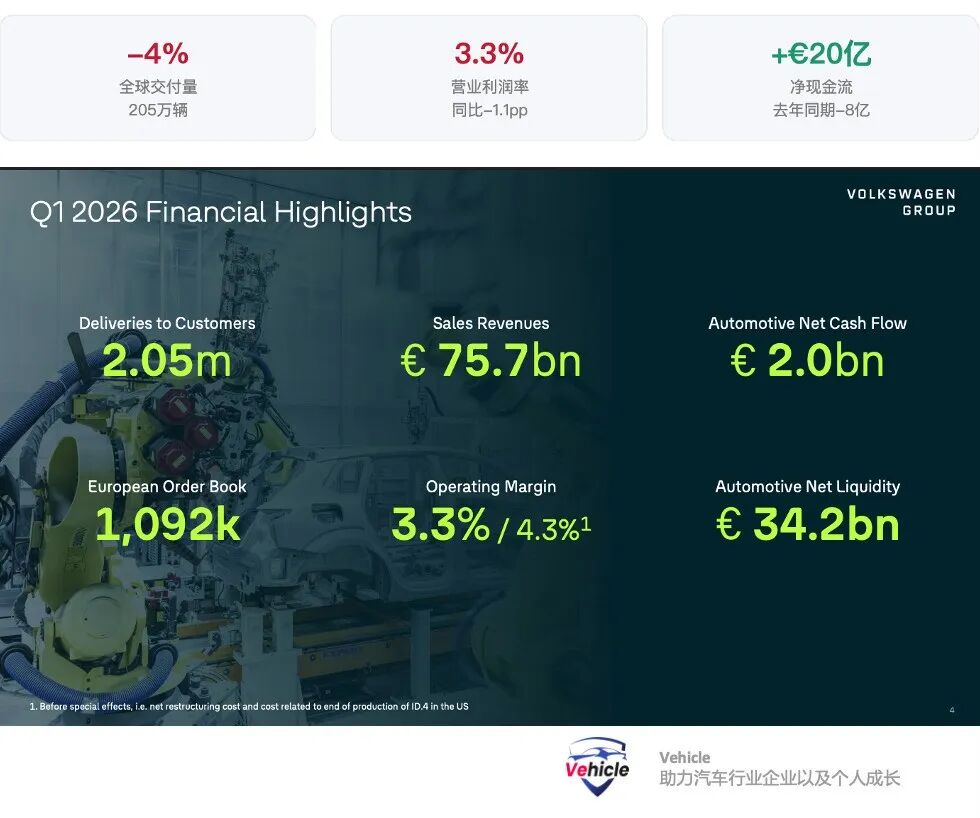

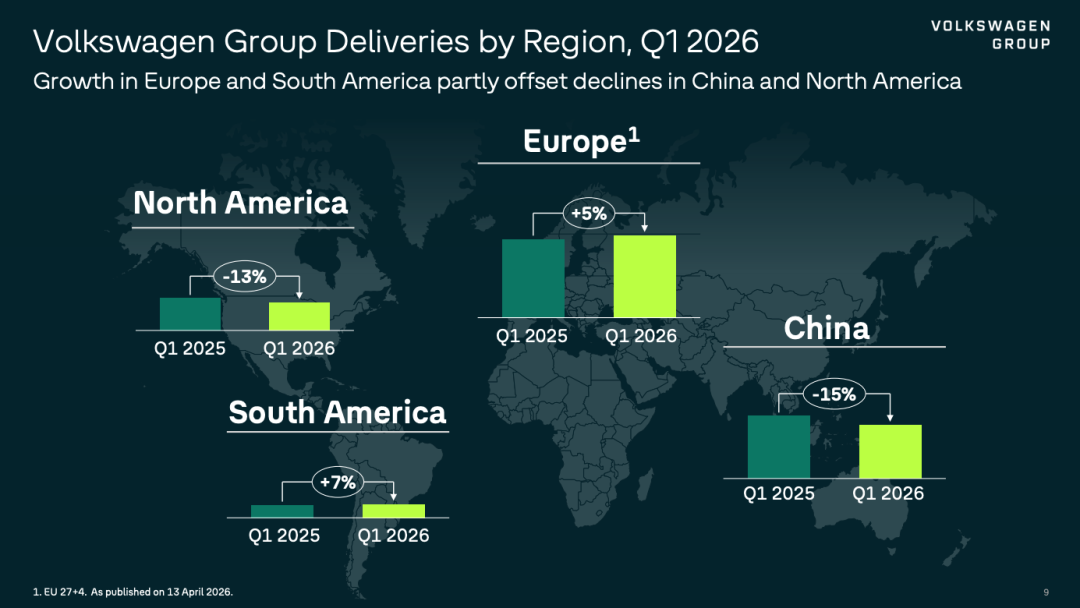

▌Global Deliveries: 2.05 million units, YoY -4%

▌Operating Profit Margin: 3.3%, down 1.1 percentage points YoY

▌Net Cash Flow: +€2 billion (Last year same period: -€800 million)

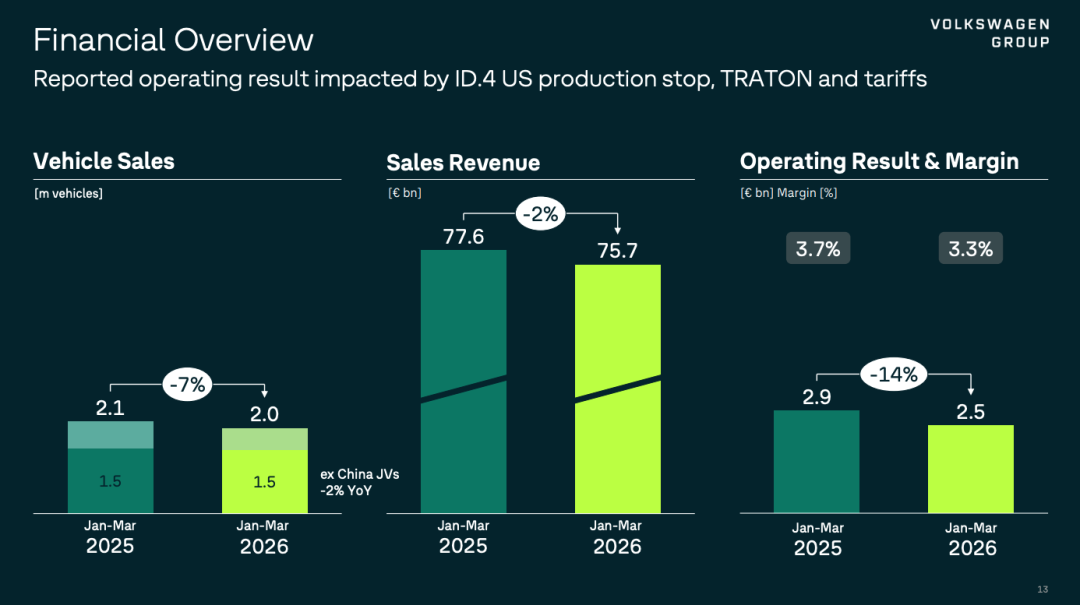

Global deliveries stood at 2.05 million units in Q1, down 4% YoY. The decline came from two main directions: North America fell 13% due to tariff impacts, while China dropped 15%. However, Europe saw a 5% increase, and South America grew 7%, partially offsetting the declines.

Consider that Volkswagen delivered approximately 2.69 million units in China in 2025, down 8% YoY—marking the second consecutive year of decline in China. Continuing this trend in Q1 was unsurprising but by no means relaxed (a Chinese term meaning 'not easy').

Operating profit stood at €2.5 billion, down 14% YoY, with a profit margin of 3.3%.

This 3.3% would have been unthinkable two years ago:

2022 ▓▓▓▓▓▓▓▓ 8%+

2023 ▓▓▓▓▓▓▓ 7%

2024 ▓▓▓▓▓▓ 5.9%

2025 ▓▓▓ 2.8% (Full-year profit down over €10 billion)

2026Q1 ▓▓▓ 3.3% (Slight rebound post-restructuring)

CFO Arno Antlitz stated bluntly on the earnings call: "Excluding special items, our profit margin is only 4.3%, which is clearly insufficient."

Of course, the CFO also noted during the call that the group's profit decline this quarter was primarily dragged down by €800 million in special impacts—including €500 million in costs related to halting ID.4 production in Chattanooga, €500 million in impairments from TRATON restructuring and the cessation of certain battery projects, and €600 million in North American tariff expenses. Excluding these, the operating profit margin would be 4.3%.

Thus, Volkswagen maintained its full-year 2026 outlook: an operating return on sales between 4% and 5.5%, and automotive net cash flow between €3 billion and €6 billion.

The quarter's brightest spot was net cash flow—reaching €2 billion in the automotive division, compared to -€800 million last year. Volkswagen spent a full year rebuilding its working capital management system, and this figure shows the hard work paid off.

02 Horizontal Comparison

Volkswagen vs. Global Rivals: Who's Laughing, Who's Crying?

Volkswagen is struggling, but it's not alone. Expanding the view, you'll find nearly the entire foreign-brand automotive industry's earnings season has been a tale of "finding joy in bitterness."

The most alarming gap: BYD's 2024 R&D investment exceeded ¥54 billion, roughly half of Volkswagen's total group R&D spending—but Volkswagen's sales volume is twice that of BYD. This R&D intensity gap is truly concerning.

The conclusion is clear: The global automotive market is forming new tiers.

One tier consists of China's BYD and Geely, redefining price benchmarks with scale and efficiency; another is Tesla, maintaining valuation through software premiums but facing profitability pressure; another is Toyota, buying more time for transformation with hybrid technology; and then there's Volkswagen, standing at the toughest crossroads—too large to shed weight easily, burdened by history, yet compelled to move.

03 Transformation Strategy

Vision 2030: Ambitious Goals, Execution is Key

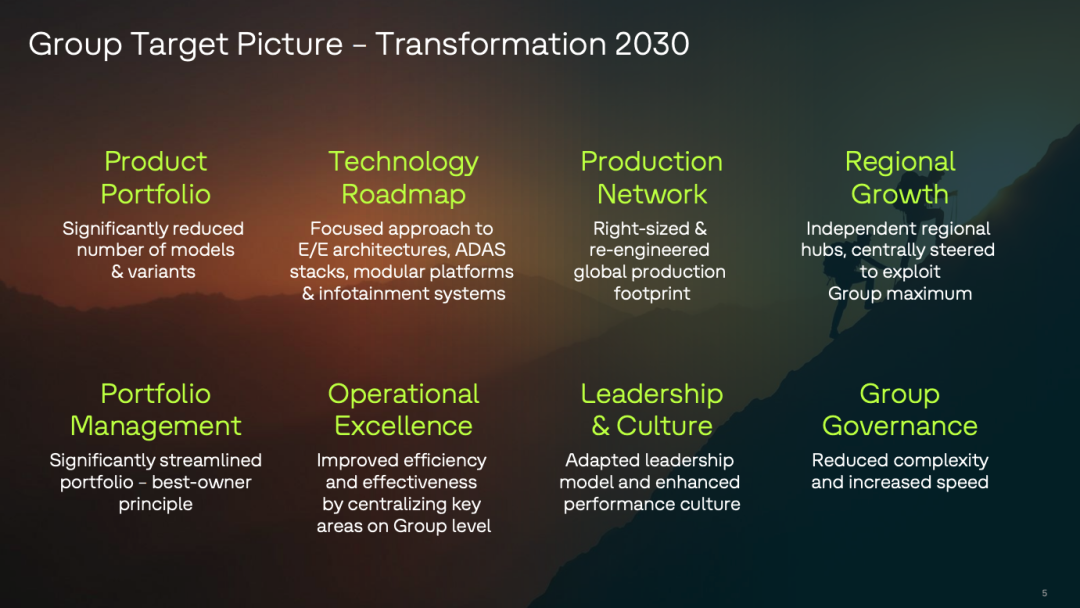

The most significant part of Volkswagen's earnings call was not the financial figures but a transformation roadmap called "Volkswagen Group Vision 2030." CEO Oliver Blume stated: "Our current business model cannot generate sufficient returns in this environment and must be fundamentally reshaped."

This plan has seven core levers, dissected one by one:

① Product Streamlining

Drastically reducing from ~150 models to far fewer, with significantly fewer configurations. Volkswagen finally admits: Too many SKUs are poison. More brands, platforms, and versions mean higher fixed costs.

② Technology Platform Convergence

Unifying electronic architectures, autonomous driving tech stacks, and cockpit systems into a limited number of solutions. The RVT architecture (a tech JV between Volkswagen and Rivian) will be used in Europe and America (Europe and America), while the CEA architecture will be used in China—two clear, separate systems.

③ Production Capacity Target of 9 Million Units

Reducing global technical capacity from 12 million units to 9 million, aligning with the average actual sales volume over the past five years. Lowering the breakeven point signals a shift from growth stories to resilience stories.

④ Regional Empowerment

North America and the "Global South" (Southeast Asia, South America, Africa) are defined as growth opportunities. Headquarters sets direction, regions execute. This acknowledges that Volkswagen's past model of a central brain directing global limbs was too slow.

⑤ Layoffs and Restructuring

In Q1 alone, operating costs were compressed by nearly €1 billion, down 70 basis points YoY. From the end of 2023 to now, ~18,000 layoffs have occurred in Germany, with ~29,000 across the group. By 2030, Germany will see ~50,000 job cuts.

⑥ Portfolio Restructuring

Bugatti was sold (to Porsche), Everance Auto Finance is negotiating to sell a majority stake, and Traton reduced its stake in Sinotruk to cash out. Volkswagen has 1,500 consolidated/non-consolidated entities. Blume said: "Everyone asks about Ducati and Lamborghini, but we have 1,500 entities to sort out."

⑦ Culture and Governance

Reducing reporting layers, linking performance to incentives, and preventing the entrepreneurial spirit at the brand level from being smothered by group bureaucracy.

Another aspect is group governance.

Volkswagen hopes to achieve an operating profit margin of 8-10% through this Combination Fist (combined strategy)—returning to pre-2022 levels.

The strategic framework is reasonable, but the issue is: Volkswagen isn't telling this story for the first time. A similar narrative was presented at the 2023 Capital Markets Day, yet the 2025 profit margin still dropped to 2.8%. The credibility of "Vision 2030" depends on execution pace, not PPT thickness.

04 China Market

From "Volkswagen's China" to "China's Volkswagen"

The topic of China dominated the earnings call, recurring every few questions. This frequency speaks volumes.

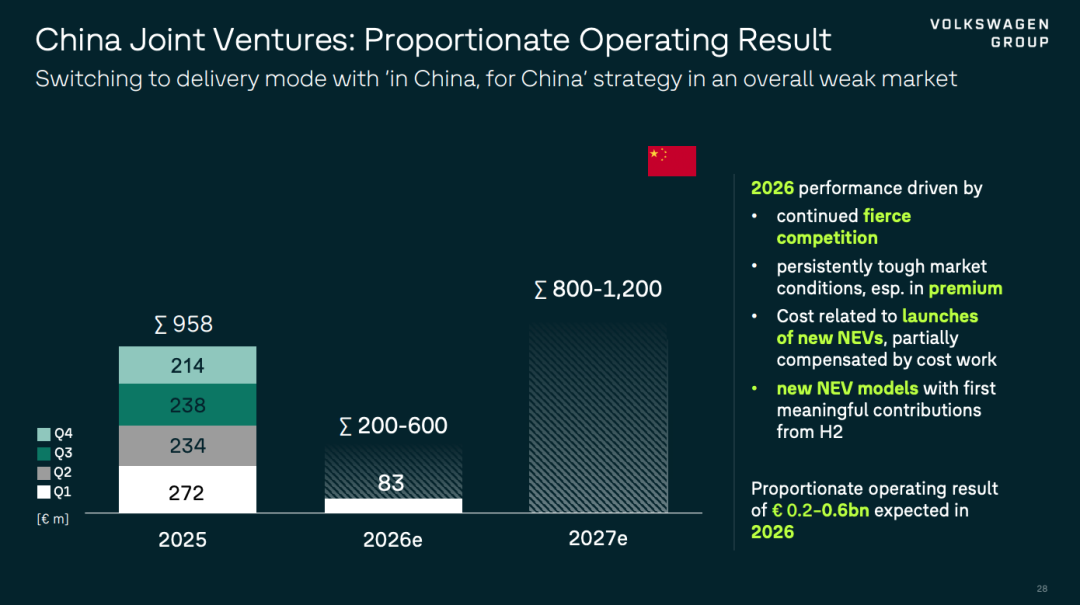

Profits from Volkswagen's Chinese JVs have halved in three years:

2023 ██████████ €2.62 billion

2024 ███████ €1.74 billion

2025 ████ €960 million

After two years of price wars, average prices have dropped ~15%, and Blume stated directly: "Prices won't recover; profit improvement can only come from costs."

Volkswagen's response is to deepen its "In China, For China" strategy:

• Joint venture with Horizon Robotics to establish Coretree for local chip and autonomous driving R&D

• Launching locally developed models at the Beijing Auto Show, garnering more media coverage than all Chinese domestic brands

• Launching over 20 new models in China in 2026, covering BEV, PHEV, and range-extended EVs

• Gradually seeking a turnaround post-2027

However, the competitive reality is: BYD, Geely, and Huawei's Aito are using software capabilities, end-to-end autonomous driving, and extreme cost control to compress the premium space for joint-venture vehicles inch by inch. Volkswagen's brand recognition in China remains strong, but converting that into sales takes time—and Chinese consumers' patience for Volkswagen is running thin.

05 U.S. Market

€4 Billion in Annual Tariff Losses: Is Scout the Only Way Out?

Annualized losses from U.S. tariffs amount to ~€4 billion, directly suppressing Volkswagen's full-year 2026 profit ceiling.

Volkswagen's localization path hinges on the Scout brand—a new pickup and SUV brand for North America, with a factory in Chattanooga, South Carolina, representing massive investment.

Blume's statement was telling: "We're paying high tariffs while investing heavily in new capacity. Doing both simultaneously is too costly, so we need support from state governments."

The subtext: The U.S. political environment is uncertain, and Volkswagen is still wait and see (waiting and seeing), but the direction is to go local. The software-defined vehicle architecture developed with Rivian has completed winter testing—this is Volkswagen's other leg in Western technology routes. If the China route relies on "speed for cost," the Western route relies on "software for premiums."

Final Thoughts

Volkswagen's Q1 report is an ugly but honest scorecard.

Behind the numbers lies the toughest species transformation for an automotive empire with nearly 90 years of history:

• From "scale-driven" to "resilience-driven"

• From "global uniformity" to "regional autonomy"

• From "hardware-first" to "software-enabled"

Few examples exist of elephants turning successfully, but they do exist. Volkswagen has capital, brands, and product reserves—what it lacks is speed and cultural DNA.

Meanwhile, China's Geely and BYD are sprinting forward at a pace exceeding market expectations every quarter, Tesla is adjusting, and Toyota is buying time. The global automotive market's new order is being rewritten.

Will Volkswagen's Vision 2030 be Oliver Blume's moment of glory or another unfulfilled strategic PPT?

The answer lies in the coming quarterly reports. Welcome to leave comments discussing your views on Volkswagen's future.

References and Images

Volkswagen AG Investor, Analyst and Media Call Q1/2026 pdf - Volkswagen Group

Volkswagen AG China Investor Update pdf - Ralf Brandstätter, Volkswagen Group

*Unauthorized reproduction or excerpting strictly prohibited-

-

![]()

Five Emerging Golden Entrepreneurial Pathways in the Agent Ecosystem: A Deep Dive into the Report (Part 2)

-

![]()

GEM-TIPS Makes Its Debut at Shenzhen International AI Expo: “Octopus AI Brain” + Intelligent Agent Cluster Pave New Ways for Industrial Intelligence

-

![]()

'China's Pioneer Domestic GPU Stock' Moore Threads Posts Profit in Q1, Yet True Profitability Unverified

-

![]()

Hynix Employees Await 3 Million Won in Bonuses, Samsung Employees Go on Strike: A Dramatic Clash Between Korea's Memory Giants

-

![]()

Twelve Years On, Can Cheng Yixiao Steer Kling to Another Victory?

-

![]()

From Data Scarcity to Open Source Boom: How China's Embodied AI Data Industry Can Break Through

-

Trend丨Indium Phosphide (InP) Prices Soar Amid AI Boom, with Cycles and Disruptions Set to Continue

-

![]()

One Article to Decode 'Computing Power Inflation': Why AI Costs Less for You While Computing Power Firms Rake in Profits