BMW Didn't Bet on the Wrong Path, But Lacks a Toyota-Style Solution

05/18 2026

05/18 2026

486

486

Making fewer mistakes does not equal finding the answer.

Original content from Autopix (ID: autopix)

Zipse could have exited gracefully.

On May 13, at BMW's 106th Annual General Meeting, he stood beside the new 7 Series for his final public speech as CEO. The next day, Production Director Neukirchen took over.

Following the conventional farewell speech script, Zipse could have reflected on achievements and regrets over the past seven years. Instead, he spoke for over 40 minutes, dedicating substantial time to criticizing the EU.

"Tariffs are like boomerangs. Who pays the price? Customers," he said.

He criticized the EU's anti-subsidy taxes on Chinese electric vehicles as "one of the highest tariffs we have to pay, which cannot possibly align with EU interests."

He criticized the 2035 combustion engine ban as "neither beneficial to customers, nor to European industry, nor to the environment."

He criticized the EU for "replacing effective market mechanisms with bans and protectionism," directly naming the European Commission and European Council.

This was a CEO's industry manifesto delivered a day before handing over the reins. Yet viewed alongside financial results, the declaration's undertone was anxiety.

In Q1 2026, BMW's net profit fell 23% to €1.67 billion. For the full year 2025, BMW's automotive segment EBIT dropped 20.7% year-on-year, with the profit margin declining from 6.3% to 5.3%.

Zipse summarized his career as "anti-fragile," a term he repeated throughout his speech. It meant BMW not only withstood external shocks but grew stronger amid volatility.

But BMW didn't grow stronger. It simply fell less than Mercedes-Benz and Volkswagen. While it recognized the risks of a pure EV-only approach, avoiding risks doesn't equate to finding a solution.

01

Under Zipse, BMW at least avoided self-destruction

2021 marked the peak of electrification narratives in Germany's auto industry.

That year, Mercedes-Benz announced "readiness for full electrification by 2030," interpreted as a de facto phase-out timeline for combustion engines. Volkswagen targeted ending combustion engine production in Europe by 2033. Volvo pledged 100% electric vehicles by 2030. Stellantis committed to 100% electric passenger car sales in Europe by 2030.

BMW was the only major European automaker refusing to set a combustion engine phase-out deadline. Zipse repeatedly stated: "We won't let regulations or political narratives dictate our product mix—customers will."

At the time, this was mocked as backwardness. Greenpeace's 2021 report labeled BMW a "climate transition laggard." Capital markets consistently undervalued BMW for lacking a "sexy" story.

BMW simultaneously iterated internal combustion versions of the 3 Series, 5 Series, 7 Series, X3, and X5 while launching electric variants, maintained PHEV lineups, and added hydrogen fuel cell vehicles by 2028.

A single vehicle platform supported multiple powertrains, with the same production line manufacturing products with different propulsion systems. Zipse dubbed this approach "technology-open."

In his May 13 speech, Zipse continued defending this strategy.

"For over 90% of EU vehicles, de facto bans will remain... After supply-side bans, they now want demand-side restrictions," he said, asserting BMW had demonstrated "a technology-neutral path" as an alternative.

▍Zipse's farewell speech

▍Zipse's farewell speech

The strategy's true value only emerged after 2024.

Mercedes' EQS became an iconic failure. Launched in 2021 as a flagship electric sedan priced over RMB 1 million, it lagged Tesla and Chinese EVs in range and smart features. Sales collapsed by more than half from peak levels in 2024-2025, forcing Mercedes to quietly retract its 2030 all-electric pledge in 2024, revising it to "up to 50% electric by 2030." Volvo also withdrew its 2030 all-electric target.

Volkswagen faced greater troubles. Its ID. series failed in both Europe and China, while prematurely canceling iterations of combustion models like Golf and Polo left it unanchored in both markets.

In 2025, Porsche booked €2.7 billion in goodwill impairment and €2 billion in product strategy adjustment expenses. As Volkswagen's brand most reliant on pure EV narratives, Porsche retracted its electrification timeline, contributing €5.9 billion to Volkswagen's special items expenses alone.

Comparing the 2025 financials clarifies the differences.

BMW Group's net profit reached €7.5 billion, down 3% year-on-year, with an automotive segment EBIT margin of ~6.3%. Mercedes-Benz Group's net profit fell 48.8% to €5.3 billion; Volkswagen AG's operating profit dropped 53% to €8.9 billion.

This ordering persisted in Q1 2026. BMW's automotive EBIT margin was 5%, Mercedes 4.1%, and Volkswagen in the 3-4% range.

The Chinese market represented the greatest divergence. Mercedes' Q1 China sales plunged 27%, Audi's 12%, while BMW's fell 10%.

Relative to Mercedes and Audi, BMW suffered less. It avoided errors on the scale of its rivals and didn't fully align strategies with EU guidance. In the 2024-2026 systemic crisis, this alone required management discipline.

Zipse attributed these results to "anti-fragility," a term from Taleb's 2012 book meaning "growing stronger through volatility." But strictly speaking, BMW hasn't achieved anti-fragility. Its 2025 China deliveries of 625,000 units marked a 12.5% decline.

Its performance is declining in step-type (stepwise) fashion, just slower than rivals. This hardly counts as victory.

02

BMW lacks a profitable middle path

Toyota demonstrated superior anti-fragility in its financials.

Toyota's FY2026 operating profit (ending March 2026) hit ¥3.77 trillion (~€23 billion), triple BMW's 2025 net profit of €7.5 billion. Meanwhile, Toyota's sales grew to 9.595 million units globally.

The two companies share superficial product philosophies. Toyota also opposes "pure EV-only routes," with former CEO Akio Toyoda expressing even stronger criticism than Zipse of EU and California BEV mandates. Both emphasize technology openness, multi-powertrain parallelism, and customer choice.

But their financial results diverge sharply. The reason lies not in strategic stance but execution.

Toyota's diversification (diversified) approach features a true protagonist: HEV hybrid electric vehicles. The Prius, Corolla Hybrid, RAV4 Hybrid, and Camry Hybrid contributed nearly half of Toyota's global sales in FY2025. Toyota's cumulative HEV sales worldwide have surpassed 27 million units.

HEVs sustain the transition period as profit engines due to four attributes:

They don't rely on infrastructure—no charging stations, grid upgrades, or consumer behavior changes are needed—enabling sales in all markets. They offer painless adoption for consumers, with nearly unchanged experience but 30-40% lower fuel consumption. Their mature cost structure, iterated since 1997 to the fifth generation, has reduced per-unit HEV premiums to $1,500-2,000, yielding higher gross margins per vehicle sold than ICE equivalents. They've passed the J-curve trough into pure harvest phase.

BMW's portfolio lacks this segment.

▍BMW's Neue Klasse iX3 concept

▍BMW's Neue Klasse iX3 concept

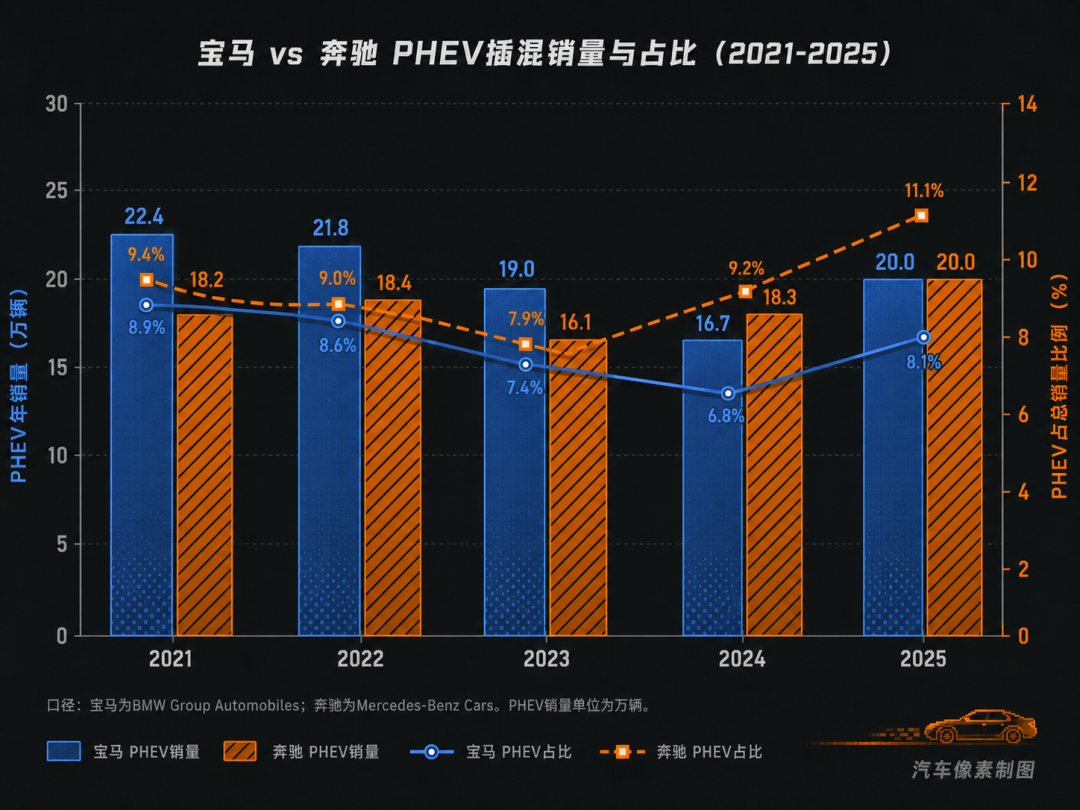

BMW has continued investing in internal combustion engines, hydrogen, and plug-in hybrid electric vehicles (PHEVs) in recent years.

Take PHEVs as an example: their product form (form) and business models differ completely outside China.

The EU is tightening PHEV fleet CO₂ discount coefficients, reducing them from 2025 and again in 2027. Multiple independent studies show PHEVs' actual electric driving ratios overseas fall far below laboratory assumptions.

Corporate users are particularly egregious—many company vehicles never charge, effectively becoming heavier, more fuel-hungry ICE cars. They're environmentally unfriendly, worsening their public perception.

In 2025, BMW's U.S. PHEV sales surged 30.7% year-on-year to 25,351 units, while BEV sales dropped 16.7%. When customers hesitated between BEVs and ICEs, they naturally chose PHEVs.

This was passive demand fulfillment, not a proactive BMW strategy. BMW has yet to develop a dedicated PHEV platform—all PHEVs are retrofits of existing models.

Zipse barely mentioned PHEVs in his AGM speech, knowing they don't make a compelling capital markets story.

Chinese domestic players offer a third solution. BYD's DM-i redefined PHEVs as low-cost products covering the entire price spectrum from RMB 80,000 to 250,000, with plug-in hybrid sales soaring from 270,000 units three years ago to 2.49 million in 2024. Li Auto's extended-range electric vehicles (EREVs) satisfied customers wanting EV experiences without range anxiety, growing from zero to 500,000 annual sales in three years.

These solutions share a common trait: they created independent, scalable, and profitable product categories rather than retrofitting existing models. BMW lacks such an offering.

Zipse's transition strategy relied on ICE engines as a safety net, PHEVs as a stopgap, and BEVs as the future. Each layer could hold temporarily but not sustainably. Combustion engines face the 2035 regulatory deadline. PHEVs are retrofits with low margins and poor public perception. BEVs remain in the investment phase, with Neue Klasse models not achieving true mass-market scale until 2027-2028.

This strategy essentially trades time for space, delaying competition until the 2027-2028 Neue Klasse arrival and betting on its success. It's a disciplined transition plan but lacks a robust interim solution.

03

What Neukirchen inherits isn't victory

At its March 12 event, Honda presented a new narrative.

Zipse's greatest regret is BMW's failure to create a powerful product category during seven years of transition.

This isn't entirely his fault. Luxury brand positioning inherently limits product innovation space—BMW can't make an RMB 80,000 large-battery PHEV or a family vehicle packed with fridges and TVs without diluting its brand. BMW's R&D resources are also fully occupied by the Neue Klasse, leaving no capacity for a second product line.

Structural constraints may be unsolvable, but they remain problems—now passed to his successor.

On May 14, Neukirchen officially became CEO. He faces pressure to deliver on a defensive strategy.

▍Neukirchen

▍Neukirchen

Neukirchen and Zipse share remarkably similar backgrounds. Zipse joined BMW in 1991 with an industrial engineering degree, became production director, and ascended to CEO in 2019. Neukirchen joined in 1993 with a PhD in mechanical engineering, served as production director, and became CEO in 2026.

Among BMW's last four CEOs over two decades, all came from production. This is unique among European luxury automakers. Mercedes' Ola Källenius started in sales; Volkswagen's Oliver Blume has a hybrid engineering-management background. But BMW insists on promoting CEOs from factory roles.

The Quandt family, holding 46% of BMW's shares, reflects majority shareholder will in personnel decisions. Not relying on stock sales for profits, they prioritize CEOs who build good cars, keep factories running, and avoid strategic blunders. Production-background executives best meet these criteria.

Yet this profile suggests Neukirchen will likely not rewrite Zipse's strategy.

His task list is specific: the Neue Klasse iX3 is already ramping up production at Debrecen and Shenyang factories, with the i3 slated for August mass production (mass production). Dozens of models will launch by 2027, coinciding with synchronized commissioning of five battery factories across three continents.

The Neue Klasse must establish BMW's missing growth narrative—the true challenge.

European Q1 new orders hit a record seasonal high, with BEV orders up 62% year-on-year and iX3 orders alone exceeding 50,000. But in China, 625,000 units in 2025 represent an emergency defense line. Smart EV newcomers like Seres, Li Auto, Xiaomi, and NIO in the RMB 300,000-500,000 price range are rapidly encroaching on BMW's core market.

The pure EV track (segment) is now a red ocean. BMW's Neue Klasse iX3, i3, and long-wheelbase iX3L face not just the 2020 Tesla market but a 2026 landscape where all price points are covered by domestic players.

BMW has developed a long-wheelbase Neue Klasse version and adopted Chinese supplier solutions like Momenta's intelligent driving. Mercedes did the same with its all-new CLA late last year—and still failed. China's competition is too fierce.

Observing Neukirchen's public remarks in recent days, his keywords are "profitability and speed are critical." His contract runs through 2031. He may reduce BMW's bleeding during the transition but won't necessarily achieve successful transformation and renewed growth.

BMW must confront its real long-term issue: whether luxury brand premiums can persist in the electrification and smart era.

Thus, BMW needs external environment improvements more than ever.

Zipse concluded his speech: "Thank you, BMW, for 35 fulfilling, intense, and thrilling years." What he didn't say was that he leaves Neukirchen a BMW with half the profit, stressed market share, and untested transformation results compared to when he took over.

Whether it can switch from defense to offense is a question that BMW has not answered.

-

![]()

BYD’s European Aspirations: Negotiating with Stellantis for European Factory Acquisitions

-

On World Telecommunication Day (May 17), Three Major Operators Launch 'Token-Based Computing Power Packages'—Here’s How to Avoid Overpaying for the 'AI Premium'

-

![]()

Ali's Global Expansion: AliExpress Steps Out of the Shadows

-

![]()

This Week in Home Appliances: Rising Costs! Haier, Hisense, Meiling, Daikin, BSH Take Action as Samsung, JD.com, Pinduoduo Face Pressure

-

![]()

Honda Corrects Course, Restructures Its 'New Four-Wheeled' Strategy

-

![]()

Don't Be Fooled by Your Home AI Again! D Lab Community's Latest Method, TraceLift, Exposes 'Fake Reasoning' and Ensures Model Thinking Processes Are Truly Reliable

-

![]()

Is Detroit Being Sidelined Amid Trump's China Focus?

-

![]()

19% Layoff Rate: Detroit's Big Three Bet on Future with Drastic Measures