BYD’s European Aspirations: Negotiating with Stellantis for European Factory Acquisitions

05/18 2026

05/18 2026

436

436

By 2025, global automotive sales had surged to nearly 100 million vehicles, reaching a precise figure of 99.8 million. China, Europe, and the United States emerged as the top three automotive markets worldwide.

Together, these three markets accounted for over half of the global automotive sales volume.

The U.S. market is notably insular; apart from domestic automakers, only Japanese, South Korean, and select European manufacturers have managed to maintain a foothold, often facing exploitative conditions (Volkswagen: It’s a tough road). Chinese automakers have largely struggled to break in (Jia Yueting: We’re ready to compete!);

While the European market appears open and fair on the surface, so-called EU standards act as significant barriers to entry. In the era of new energy vehicles (NEVs), these standards have lost their effectiveness against leading Chinese automakers, prompting the EU to introduce the “New Battery Law” to restrict the influx of Chinese NEVs;

In contrast, the Chinese market welcomes overseas brands through joint ventures and even allows Tesla to establish wholly-owned factories.

For Chinese automakers, until their global presence reaches a critical mass, the U.S. market can be set aside; the focus should be on Europe.

So, how can entry barriers be permanently overcome?

By establishing local factories.

1

From Building a Factory in Hungary to Negotiating with Stellantis: BYD’s European Dream

On December 22, 2023, BYD announced plans to construct a new energy passenger vehicle production base in Szeged, Hungary, marking the first instance of a Chinese automaker establishing a passenger vehicle factory in the EU.

With a total investment of €4 billion (approximately RMB 35 billion), the factory is projected to achieve an annual production capacity of 300,000 vehicles at its peak, primarily manufacturing passenger vehicle models for the European market. For BYD, this factory represents not just a production site but a cornerstone of its “Made in Europe, Sold in Europe” strategy.

On May 15, 2025, BYD established its European headquarters in Hungary, tasked with three core functions: sales and after-sales service, vehicle certification and testing, and local design and feature development for models. In terms of R&D, BYD’s European headquarters will initially focus on in-depth research into intelligent assisted driving technologies and next-generation automotive electrification technologies. Moving forward, BYD plans to collaborate with at least three Hungarian universities on joint research and work with local suppliers and enterprises to drive upgrades in the NEV industrial chain.

On January 30, 2026, the Mayor of Szeged announced that trial production had commenced at the factory, with mass production scheduled for the second quarter. BYD stated that the factory’s construction progress was fully on track and that it was currently conducting qualification certifications for 150 European suppliers to further strengthen the local supply chain system.

However, a single factory in Hungary is insufficient to support BYD’s ambitious European goals.

According to data from the European Automobile Manufacturers Association (ACEA), BYD’s cumulative sales in the European market reached 187,657 vehicles in 2025, a 268.6% increase from 50,912 vehicles in 2024, making it the fastest-growing automotive brand in the region. In December 2025, BYD registered 27,678 vehicles in Europe, a 229.7% year-on-year increase.

Such rapid growth clearly cannot be sustained by a single factory in Hungary.

On May 13, 2026, BYD Executive Vice President Li Ke revealed that the company was in negotiations with Stellantis NV and other European automakers to acquire idle production capacity factories in the region, currently in the consultation phase.

Who is Stellantis?

Nicknamed the “League of Losers,” it is a “living fossil” of Europe’s century-old automotive culture.

Formed through continuous mergers and acquisitions of underperforming automotive enterprises by Italy’s Fiat and France’s Peugeot,

it owns brands such as Peugeot, Citroën, Fiat, Jeep, Alfa Romeo, and Maserati. In recent years, due to slow electric vehicle transformation and shrinking demand for fuel vehicles in Europe, several Stellantis factories have faced idle production capacity.

It is reported that Stellantis has informed the French and Italian governments that its remaining manufacturing capacity in Europe involves four factories, including the Rennes factory in France and the Cassino factory in central Italy. These factories originally produced fuel vehicles for brands like Peugeot and Citroën, but with delayed electrification transformation, capacity utilization has continued to decline.

BYD’s intention is clear: by acquiring or taking over these idle factories, it can swiftly gain local production capacity in Europe, avoid tariff barriers, and shorten market response times.

Li Ke stated that BYD aims to utilize existing idle capacity locally rather than building new factories from scratch, thereby rapidly enhancing its local supply capacity in Europe. The rationale behind this strategy is that idle factories of European automakers already possess mature production lines, skilled workers, and a complete supply chain. BYD only needs to carry out electrification transformations to commence production, which is far more time- and labor-saving than building new factories.

However, the complexity of the negotiations cannot be underestimated. Powerful European trade unions, employee placement issues, labor-management negotiations, and adaptation to environmental standards may all pose obstacles to the deal. Additionally, whether the Italian government will approve the sale of its domestic factories to a Chinese automaker is a politically sensitive issue.

If the negotiations with Stellantis succeed, BYD will gain additional idle production capacity in Europe, further solidifying its strategic layout of “Made in Europe, Sold in Europe.”

This model of acquiring idle capacity is reminiscent of the path taken by Japanese automakers when they entered the U.S. market in the 1980s. Toyota and Honda successfully avoided trade frictions and tariff barriers by building factories in the United States and eventually established a strong foothold in the U.S. market. BYD is replicating this successful path, but the stage has shifted from North America to Europe.

2

A Mixed Q1 Financial Report

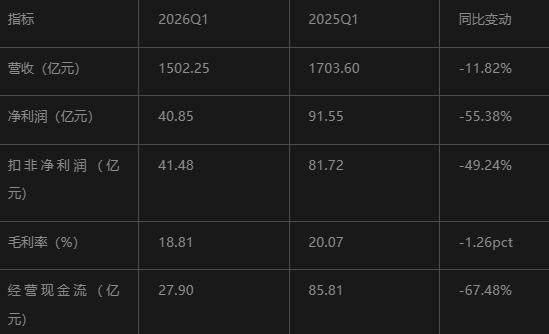

In the first quarter of 2026, BYD delivered a mixed financial performance: revenue reached RMB 150.225 billion, a year-on-year decrease of 11.82%. Net profit was RMB 4.085 billion, a sharp decline of 55.38% year-on-year. Non-recurring profit and loss net profit was RMB 4.148 billion, a year-on-year decrease of 49.24%. Operating cash flow was RMB 2.790 billion, a year-on-year narrowing of 67.48%.

In the first quarter of 2025, BYD’s net profit was still RMB 9.155 billion. Within a year, net profit more than halved.

In the first quarter of 2024, net profit was RMB 4.569 billion. It surged to RMB 9.155 billion in the first quarter of 2025, doubling. In the first quarter of 2026, it fell back to RMB 4.085 billion.

This reflects the brutal elimination race in the NEV industry. It is the pain of the domestic market shifting from incremental competition to stock competition.

To understand this financial report, one must first answer a question: when the domestic market is trapped in stock competition, where is BYD’s second growth curve?

The answer lies in the 320,000 overseas sales volume.

Hidden within this seemingly dismal financial report are signals of structural differentiation:

Data Source: iFind

The core reason for the 55.38% decline in net profit is not operational deterioration but dual fluctuations in the financial and investment ends:

Exchange Losses: Affected by exchange losses in the current period (compared to exchange gains in the same period last year), financial expenses shifted from a net gain of RMB 1.908 billion in the same period last year to a net expense of RMB 2.099 billion, a variation exceeding 200%. This fluctuation was primarily due to sharp fluctuations in the RMB exchange rates against the euro and the U.S. dollar, as well as the impact of diversified settlement currencies in overseas business.

Shrinking Investment Gains: Investment gains shrank significantly by 87.68%, and losses from changes in fair value further eroded profit margins. This is related to capital market fluctuations and declining yields on wealth management products.

Reduced Sales Receipts: Operating cash flow was RMB 2.790 billion, a year-on-year narrowing of 67.48%, primarily due to reduced sales receipts. The first quarter is typically a slow season for automotive sales, compounded by intensified competition in the domestic market, leading to longer receipt cycles for dealers.

However, it is noteworthy that BYD’s gross profit margin climbed to 18.81% in the first quarter, up 1.4 percentage points sequentially, reaching its highest level in nearly a year. This was driven by the optimization of the overseas sales structure—an increase in the proportion of high-gross-margin overseas models.

3

Between 705,000 Sales and 320,000 Exports

In the first quarter of 2026, BYD cumulatively sold approximately 705,000 new energy vehicles.

Among them, cumulative overseas sales approached 320,000 vehicles, a year-on-year increase of 55%, accounting for over 45% of total sales.

In March 2026, BYD’s total monthly sales reached 300,222 vehicles, strongly surpassing the 300,000-unit mark and maintaining its position as China’s top-selling NEV brand for 58 consecutive months. Among them, overseas sales of passenger vehicles and pickups reached 119,591 vehicles, a year-on-year increase of 65.2%, setting a new annual high. Cumulative overseas sales in the first quarter were 319,700 vehicles, with a continuously rising proportion, becoming an important pillar of growth.

The explosion in overseas markets has become BYD’s brightest growth pole.

In the European market, annual sales reached 187,657 vehicles in 2025, a staggering year-on-year increase of 268.6%, making it the fastest-growing automotive brand in the region.

In the first quarter of 2026, BYD’s registrations in Germany surged by 644% year-on-year, with its market share rising to 1.3%. In major markets such as the UK, France, and Italy, BYD’s growth was equally remarkable.

Globally, BYD’s sales footprint spans 120 countries, with cumulative exports exceeding 2.08 million vehicles. From Southeast Asia to South America, from the Middle East to Europe, BYD’s global presence is rapidly expanding.

BYD has raised its full-year overseas export target for 2026 from 1.3 million vehicles by 15% to 1.5 million vehicles. The confidence behind this target comes from the continuously exceeding expectations performance of overseas sales.

The rapid growth of overseas sales is transforming BYD’s profit structure.

An increase in the proportion of high-gross-margin overseas models is driving the company’s gross profit margin upward against the trend. For example, BYD’s Tang EV sold in Norway is priced at approximately NOK 600,000 (approximately RMB 400,000), while its domestic price is around RMB 300,000. The overseas premium space provides BYD with valuable profit buffers.

More importantly, the success in overseas markets is reshaping BYD’s brand image. From being seen as a manufacturer of cheap electric vehicles to a technology leader, BYD is undergoing a brand upgrade in overseas markets. In Germany, BYD’s electric vehicles are priced similarly to Volkswagen’s ID series; in Norway, the price of BYD’s Tang EV is even higher than some European domestic brands.

But on this early summer evening, the R&D center at BYD’s headquarters in Shenzhen is ablaze with light, the assembly line at the Szeged factory in Hungary is undergoing trial runs, and the negotiation table at the Cassino factory in Italy is piled high with documents.

At the crossroads of globalization and de-globalization, BYD’s wheels keep rolling forward.

-END-

Disclaimer: This article is based on the public company attributes of listed companies and the information disclosed by them in accordance with their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms) as the core basis for analysis and research; Shiyu Xingkong strives for fairness in the content and viewpoints presented in the article but does not guarantee its accuracy, completeness, or timeliness; the information or opinions expressed in this article do not constitute any investment advice, and Shiyu Xingkong is not responsible for any actions taken based on the use of this article. Copyright Notice: The content of this article is original to Shiyu Xingkong and may not be reproduced without authorization.

-

![]()

Launching 7 New Products in May, Laifen Still Needs to Master the Art of "Simplification"

-

![]()

Defying the Cost Tsunami: Why is Apple Daring to Cut Prices Amid Industry-Wide Hikes?

-

Top 10 Most Profitable Enterprises in Computing Power Leasing

-

![]()

The Early Riser Who Has Led Apple for Years Is Finally Stepping Down

-

![]()

Can China's Auto Companies Open the Door to the U.S. Market by Expanding Cooperation Paths?

-

AI Falls Behind, Tencent Rushes to Catch Up

-

![]()

BYD’s European Aspirations: Negotiating with Stellantis for European Factory Acquisitions

-

On World Telecommunication Day (May 17), Three Major Operators Launch 'Token-Based Computing Power Packages'—Here’s How to Avoid Overpaying for the 'AI Premium'