NIO's Q1 2026 Performance: Has China's Most Hard-Pressed New Energy Vehicle (NEV) Manufacturer Finally Turned the Corner?

05/28 2026

05/28 2026

409

409

Firstly, this is not an article tailored for NIO enthusiasts. Rather, it scrutinizes whether the fundamental logic underpinning NIO's business model as a new energy vehicle manufacturer can lead to success. Nevertheless, it will profoundly shape your perspective on the competitive landscape of China's entire NEV sector—be it analyzing the competitive advantages of high-end brands, the commercialization trajectory of battery-swapping models, or the marginal efficiency of R&D investments.

Grasping its essence may aid you in comprehending the diverse survival strategies of China's NEV makers; it may help you decipher the true connotation of a 'high-end brand' in the Chinese market; it may assist you in understanding the genuine rationale behind R&D investments and their returns. Perhaps, you will glean fresh insights for your business, investment, and career endeavors.

Presented here is the Q1 financial report unveiled by NIO on May 27, 2026, showcasing deliveries of 83,465 vehicles (a 98.3% YoY surge), a vehicle gross profit margin of 18.8% (improving for four consecutive quarters), a positive non-GAAP operating profit, and cash reserves amounting to RMB 48.2 billion. This NEV manufacturer, once the most loss-making and frequently criticized, with its founder repeatedly 'schooled' on CEO duties, has now signaled to the market its first tangible sign of a 'viable business model'.

The ensuing analysis is grounded in NIO's Q1 2026 financial report core data, coupled with highlights from the management Q&A during the earnings call, aiming to furnish you with valuable information and inspiration.

1. First Glance at the Report Card: The 'Bottomless Pit' of Losses Reveals Profitability

NIO delivered 83,465 vehicles in Q1, marking a staggering 98.3% YoY increase—a figure likely to make any analyst who has tracked NIO's financials over the past three years rub their eyes in disbelief. Consider that NIO delivered merely around 30,000 vehicles in Q1 2024 and 42,000 in Q1 2025, only to double that in Q1 2026. All three brands contributed: NIO's main brand delivered 58,543 vehicles, ONVO 13,339, and Firefly 11,583.

Q1 Core Financial Highlights:

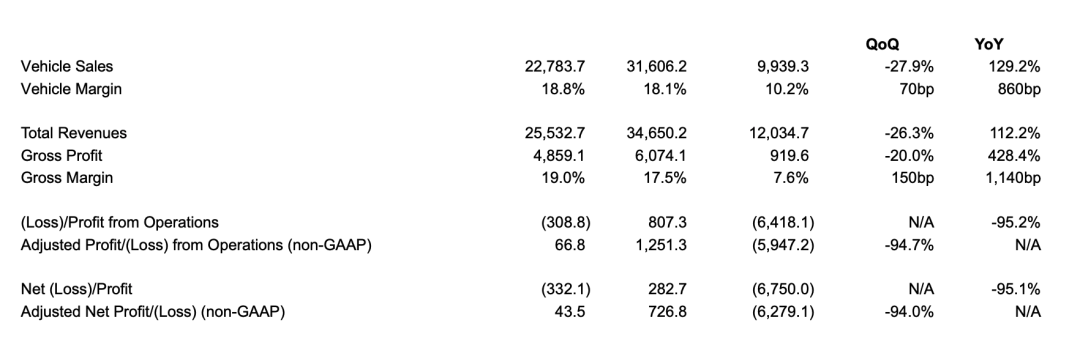

· Total Revenue: RMB 25.5 billion (+112.2% YoY, -26.3% QoQ)

· Vehicle Sales Revenue: RMB 22.8 billion (+129.2% YoY)

· Other Sales Revenue: RMB 2.7 billion (+31.2% YoY)

· Overall Gross Margin: 19% (7.6% YoY, 17.5% QoQ)

· Vehicle Gross Margin: 18.8% (10.2% YoY, 18.1% QoQ)

· Other Sales Gross Margin: 20.6% (Four-year high)

· Operating Loss: -RMB 300 million (Loss of RMB 6.4 billion YoY)

· Non-GAAP Operating Profit: +RMB 66.8 million (First positive)

· Cash Reserves: RMB 48.2 billion (New high)

The most noteworthy figure in this report card is the non-GAAP operating profit of RMB 66.8 million. Although seemingly modest, its significance far outweighs the number itself: after 11 years, NIO has demonstrated for the first time that the business model of 'high-end electric vehicle brand + battery-swapping ecosystem + full-stack technology' can succeed in the Chinese market.

Even more remarkable is that R&D expenses decreased by 40.7% YoY, from RMB 3.2 billion in Q1 last year to RMB 1.9 billion this Q1, yet the product development pace accelerated. CFO Qu Yu remarked on the call: 'Today, every RMB 2 billion in R&D investment yields results equivalent to RMB 3.5 billion in the past.' This underscores the harvest of NIO's past investments.

2. ES8 + ES9: NIO's High-End Brand Makes a Breakthrough

If there was a standout product in NIO's Q1, it was the all-new ES8. Deliveries commenced in late September 2025, and it reached 100,000 units delivered in just 215 days, setting the fastest record for all passenger vehicles priced above RMB 400,000 in the Chinese market. As of April, the ES8 had claimed the top spot in sales for five consecutive months in both the large SUV and passenger vehicle markets above RMB 400,000 (across all powertrain types).

'In the large three-row SUV market above RMB 400,000, the ES8 commands a 49.7% market share. This achievement reflects our 11 years of systematic capability building.'

— William Li, Founder of NIO

On May 27 (today), NIO officially launched and delivered its flagship executive SUV, the ES9, priced above RMB 500,000. Initially, there were concerns that the ES9 would cannibalize ES8 orders—after all, both are large SUVs in similar price brackets.

Li's response on the call was surprising: ES9 pre-orders not only failed to cannibalize ES8 orders but instead spurred a 30% week-on-week increase in ES8 orders. In the first 20 days of May, ES8 orders reached a new all-time high since its launch in October 2025. The reason is straightforward—the ES9 attracted many 'on-the-fence' customers who were originally considering BBA ICE vehicles to NIO stores. comparisons After, some found the ES8 better suited their size and usage needs. New models are not just competing with old ones but also driving traffic to them—a subtle yet invaluable phenomenon.

Li accurately positioned the ES9: 'It competes directly with traditional ICE flagship SUVs like the BMW X7 and Mercedes-Benz GLS.' This marks the first time a Chinese NEV brand has explicitly targeted the most fortified segment of German luxury SUVs above RMB 500,000 in the ICE era.

3. ONVO: The 'Unsellable' Sub-Brand Stages a Quiet Recovery

The ONVO L90 was initially deemed a 'flop' after its launch in the second half of 2025—sales figures in its initial months were lackluster, and doubts emerged regarding ONVO's brand positioning. However, Q1 data tells a different story:

ONVO Q1 Key Highlights:

· L90 ranked first in the large SUV market priced between RMB 200,000-300,000

· All-new L80 (launched May 15): Boasts the largest cargo space among Chinese five-seater SUVs, featuring an innovative 'frunk + trunk' layout

· ONVO average selling price: ~RMB 240,000 (competing with second-tier luxury brands)

· Brand awareness: Equivalent to a new brand in 2020 (still requires significant improvement)

Li acknowledged that ONVO's primary challenge is brand awareness. 'ONVO has only been delivering for 20 months; its awareness is roughly on par with a new brand in 2020,' he stated on the call. To enhance awareness, ONVO has significantly revamped its marketing strategy—engaging celebrity endorsements, grassroots promotion teams, and in-store events.

ONVO's narrative essentially revolves around 'how to create a best-selling family SUV priced between RMB 200,000-300,000 leveraging battery-swapping and brand parent advantages.' If it succeeds, it proves NIO Group can forge a second growth curve; if not, NIO's high-end foundation remains stable but faces a clear ceiling.

4. Other Sales (Services & Community): The Hidden Profit Goldmine, Gross Margin Hits 20.6%

The biggest 'pleasant surprise' in this financial report is that the gross margin on other sales reached 20.6%, a four-year high for NIO. Other sales encompass after-sales services, parts, energy services (battery swapping/charging), and NIO Life products. Q1 other sales revenue was RMB 2.7 billion, with a gross profit of RMB 560 million.

Why is this figure pivotal? It signifies that NIO's investments over the past 11 years in user community, battery-swapping networks, and parts e-commerce—long perceived as heavy-asset 'cost centers'—are now transforming into profitable 'profit centers.'

'Other sales have reached a profitability inflection point and entered a new phase. Our full-year 2026 gross margin target for other sales is 20%. Long-term, besides new car sales, other sales will become a key driver of NIO's sustainable growth.'

— Qu Yu, CFO of NIO

Three key drivers underpin this:

Firstly, high user stickiness and strong willingness to pay—NIO's user base inherently possesses high purchasing power and brand loyalty;

Secondly, optimized battery-swapping station operational efficiency—average daily swaps per station stabilized at 30-45, combined with peak-shaving arbitrage and grid interaction trading;

Thirdly, NIO Life's cultural and creative products have evolved into a profitable side business.

This marks another successful instance of an automaker leveraging 'full-lifecycle services' for profit, alongside Ford Pro service subscriptions (+30%), Toyota KINTO subscriptions (JPY 2.1 trillion), and Kia's PBV one-billing system. Selling a car once for a one-time profit is no longer sufficient; ensuring users pay continuously throughout the vehicle's lifecycle is the real barrier for the next decade.

5. Intelligent Driving + Self-Developed Chips: NIO's True 'Technological Ace'

NIO disclosed a set of self-developed intelligent driving data during the call, the most information-dense segment:

NIO World Model (NWM) Real-World Data:

· Urban NOP mileage increased by 92% QoQ within one quarter of the new version's launch

· Intelligent driving usage time ratio increased by 116% QoQ

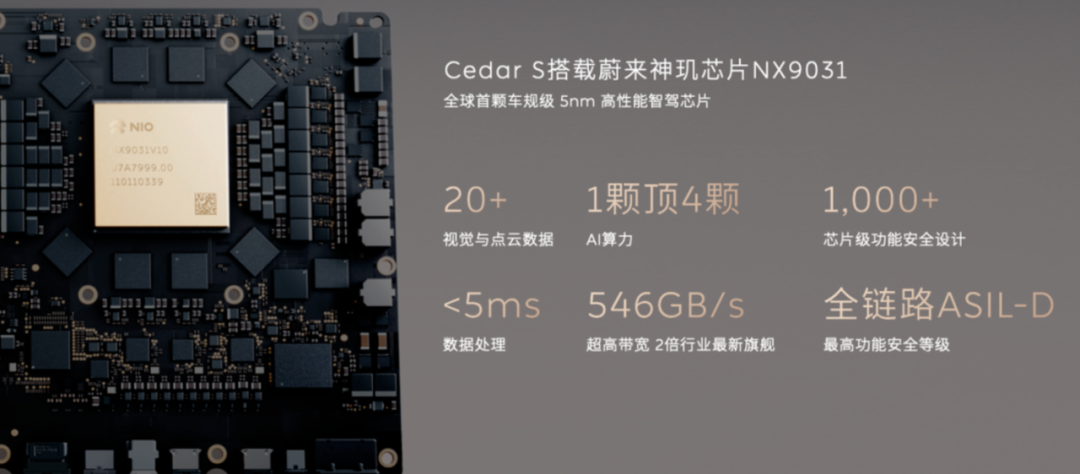

· Self-developed NX9031 intelligent driving chip (world's first 5nm automotive-grade chip): Over 250,000 units shipped

· Next major NWM upgrade slated for June

· 80-85% of models to be equipped with self-developed chips in H2

· NIO achieves equal or superior intelligent driving experience with just 20% of industry-average cloud computing power

'Achieving the same experience with 20% of cloud computing power'—if accurate, this statement carries profound implications. It means NIO's intelligent driving architecture (World Model + closed-loop reinforcement learning) has achieved significant efficiency leadership. In the AI era where computing power incurs costs, this efficiency gap will only widen over time.

Notably, NIO's semiconductor subsidiary 'Shenji' secured RMB 2 billion in funding in Q1. Li remarked: 'This funding provides us with more resources to develop even more cost-effective chips.' In essence, NIO is not only developing flagship intelligent driving chips but also 'economy chips' for models priced around RMB 200,000—aiming to capture Horizon Robotics' market share as well.

6. Gross Margin Target of 17-18% vs Industry Price Hikes: NIO's Coping Strategy

During the Q&A session, analyst Paul Gong posed a pointed question: With rising prices for chips (especially memory), lithium battery materials, and copper/aluminum raw materials—expected to increase average vehicle costs by over RMB 10,000 per unit—how will NIO cope?

Li's response can be encapsulated as 'walking on three legs':

First leg: Product mix upgrade. Increase the proportion of high-gross-margin models like the ES8 and ES9. The ES8 alone contributed over 20% gross margin per unit in Q1, accounting for 50% of total vehicle gross profit. In other words, NIO doesn't rely on volume for profit but on selling high-end models effectively.

Second leg: Stable pricing, reduced promotions. Li made it clear: 'We won't sacrifice gross margins for volume.' This stance is rare among Chinese automakers amid fierce price wars. Li Auto, Seres, and XPeng are all cutting prices or adding features, while NIO chooses to 'hold firm.'

Third leg: Supply chain refinement and operation. Li revealed a figure—NIO's 'transparent supply chain + primary & preferred partners' mechanism, implemented since last year, is expected to squeeze out 5-10% cost optimization space on the supply side. This approach involves long-term risk-sharing and improvement dividend-sharing with suppliers, essentially a Chinese version of Toyota's TPS (continuous improvement) logic.

NIO's Q2 and full-year vehicle gross margin guidance is 17-18%. In China's generally declining NEV gross margin environment, this is an ambitious but not unattainable target.

In Closing

NIO's Q1 2026 financial report marks the most pivotal milestone in the company's 11-year history—not because the numbers are dazzlingly impressive (absolute values are still not 'eye-catching'), but because it demonstrates, for the first time, that a new energy vehicle manufacturer has established a complete, self-sustaining business closed loop: high-end brand positioning + full-stack technology R&D + battery-swapping ecosystem moat + user community stickiness + multi-brand matrix coverage. These five components have finally begun to interlock and reinforce each other.

The NIO of yore was a tale of love and hate—brimming with passion but lacking execution, burning cash faster than generating profits. The NIO of today is assuming a different guise: it will still err, still face fierce competition, but its underlying business model logic has finally traversed the first kilometer.

The real test now is whether this 'first kilometer' can replicate and extend to the second, third, and beyond—can ONVO truly scale? Can Firefly establish a solid foothold in the small car market? When will overseas markets contribute a second growth curve? Can the ES9 and ET9 above RMB 50

-

![]()

DeepSeek Raises the Query, Xiaomi Provides the Solution

-

![]()

The Story Behind Honor's IPO 'Difficulties': Lost Market Share and a Hanging Future

-

High R&D Investment ≠ High Barriers: Decoding Insta360's 'Technology Story'

-

![]()

Over 400 Mercedes-Benz EQC Owners Gear Up for Legal Action! ‘Battery Capacity Degradation’ Dispute Intensifies

-

![]()

The 'Enclosure Movement' in the AI Era: When Operators Start Selling Tokens

-

Domestic Mobile Phone Makers Navigate Challenging Times

-

![]()

NIO's Q1 2026 Performance: Has China's Most Hard-Pressed New Energy Vehicle (NEV) Manufacturer Finally Turned the Corner?

-

![]()

Jensen Huang Now Shares a 'Brotherly' Bond with Richard Liu