The Story Behind Honor's IPO 'Difficulties': Lost Market Share and a Hanging Future

05/28 2026

05/28 2026

634

634

Author|Haotian

The long-delayed IPO has led Honor to press the 'exit button' for employee shareholdings.

On May 22, 2026, according to Jiemian News, Honor held an internal employee shareholding meeting in the afternoon after failing to complete its IPO within one year of its share reform. Considering the financial pressure on some employees, Honor's management committee decided to open a share reduction and exit channel, allowing employees to sell back their shares at the original subscription price.

Notably, at this meeting, Honor's senior executives also directly addressed rumors of the 'termination of Honor's IPO,' clarifying that the IPO had not been terminated but did not mention a specific listing timeline.

It is reported that in June 2025, Honor completed its listing tutoring (tutoring) filing (filing) with the Shenzhen Securities Regulatory Bureau. The filing report indicated that the tutoring period would be divided into three stages, with the latest completion scheduled for March 2026 and an application for tutoring acceptance. However, as of May 2026, Honor's listing tutoring had not yet passed acceptance, naturally raising concerns about its IPO prospects.

Despite Honor's continued efforts to advance its IPO, the situation it faces is becoming increasingly severe (severe). Currently, the smartphone industry has entered a mature phase, and memory prices continue to rise. Against this backdrop, Honor, which is highly dependent on its smartphone business, finds it difficult to instill confidence in the capital market.

01 Honor's Valuation Has Shrunk by About 35% Since Independence

As is widely known, Honor was originally a sub-brand under Huawei focused on internet channels, with its core strategic goal being to compete directly with internet-focused smartphone brands like Xiaomi and help Huawei's smartphones achieve a breakthrough into the high-end market.

At the end of 2020, under pressure from sanctions, Huawei sold Honor to the Shenzhen State-owned Assets Supervision and Administration Commission (SASAC) and dozens of distributors and agents. Since the core objectives of local state-owned assets and financial investors are capital appreciation and exit, an IPO became a critical task that Honor must accomplish.

In November 2023, Honor's board of directors announced, 'To achieve the company's next-stage strategic development, the company will continuously optimize its equity structure, attract diversified capital, and drive the company to list on the capital market through an initial public offering.'

Image source: Honor

In the following years, Honor actively pursued share reform, introducing shareholders such as China Mobile, China Telecom, and BOE, forming a community of interests among 'state-owned assets + industrial chain + channels' and preparing for its IPO.

However, somewhat unusually, despite being endorsed by central enterprises and industrial capital, with a more stable capital structure, Honor's valuation has been on a downward trajectory.

Image source: Hurun Research Institute

According to Caixin, citing sources from buyer channels, Huawei sold Honor for approximately $40 billion (about RMB 260 billion at the then-current exchange rate) at the end of 2020. The '2025 Global Unicorn List' released by Hurun Research Institute in June 2025 showed Honor's value at RMB 170 billion. In less than five years, Honor's valuation has shrunk by about 34.62%.

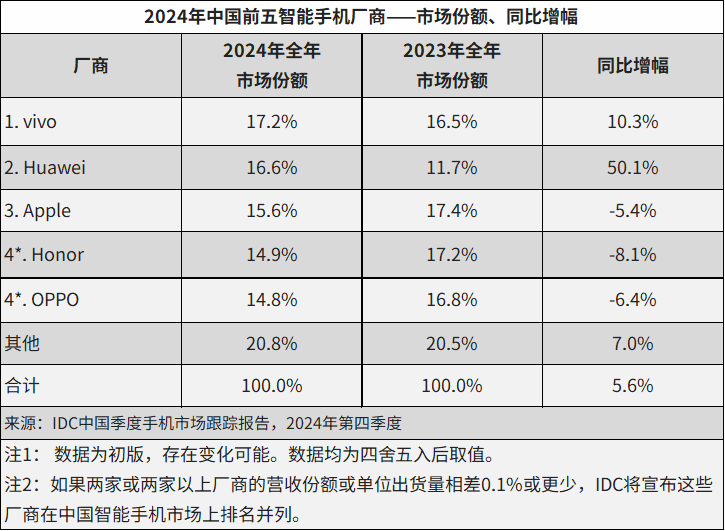

Image source: IDC

The reason is that Honor's smartphone shipments have been declining. IDC data shows that from 2023 to 2024, in the Chinese smartphone market, Honor's shipments fell by 10.3% and 8.1% year-over-year, ranking second and fourth, respectively. In 2025, Honor even fell out of the TOP 5 list.

Unlike Xiaomi, which has built strong growth drivers such as IoT and new energy vehicles beyond its smartphone business, Honor's shrinking smartphone base naturally weakens its valuation.

Given the continuous decline in the company's valuation, which significantly harmed shareholders' interests, despite Zhao Ming's significant contributions to Honor's development, Honor's senior leadership still chose to 'change the commander.' In January 2025, Zhao Ming stepped down as Honor's CEO, and former Huawei executive Li Jian took over.

02 Huawei's Return Erodes Honor's Market Share

In recent years, Honor's smartphone shipments have continued to decline, partly due to the Chinese smartphone industry entering a mature phase and partly due to Huawei's strong return.

As mentioned earlier, Huawei sold Honor primarily because its smartphone business was struggling under sanctions. Due to its deep ties with Huawei, in its early days of independence, Honor emphasized business, office, and high-end 'Huawei concepts,' significantly filling the market vacuum left by Huawei's smartphone hiatus.

Official data shows that in Q1 2021, Honor's market share in the Chinese smartphone market was only 3%. IDC data indicates that from 2021 to 2022, Honor's market share rebounded to 11.7% and 18.1%, respectively.

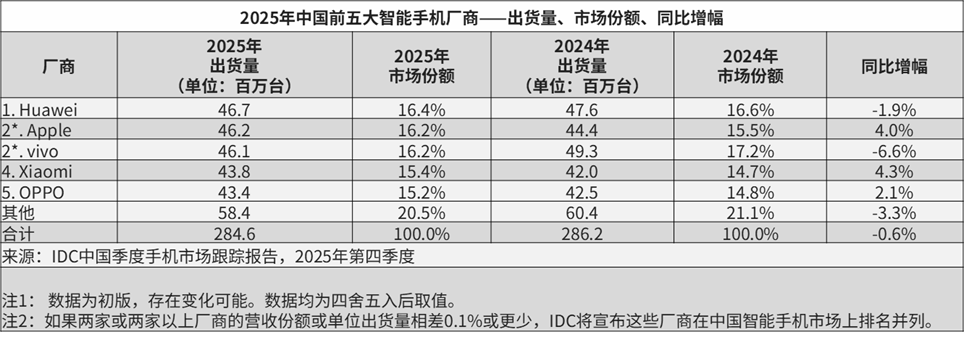

Image source: IDC

However, Huawei's smartphones did not collapse. After August 2023, with the restart of Kirin chip production, Huawei's smartphones staged a strong recovery. IDC data shows that in the Chinese smartphone market in 2024, Huawei's smartphone shipments surged by 50.1% year-over-year, ranking second; in 2025, Huawei's smartphone shipments reached 46.7 million units, ranking first.

A comprehensive comparison of the market trends of Huawei and Honor smartphones in the past two years reveals a clear 'zero-sum' dynamic. With Huawei's full return, Honor's brand narrative as a 'Huawei alternative' has gradually collapsed, making it increasingly difficult to persuade consumers to buy its products.

Through specific products, Honor's weak position is evident. Data disclosed by digital blogger 'RD Observation' shows that as of the 20th week of 2026, sales of the Honor Magic8 series reached 1.1707 million units, not only far below the 6.0935 million units of the Huawei Mate 80 series but also ranking last among the flagship models of the six major brands.

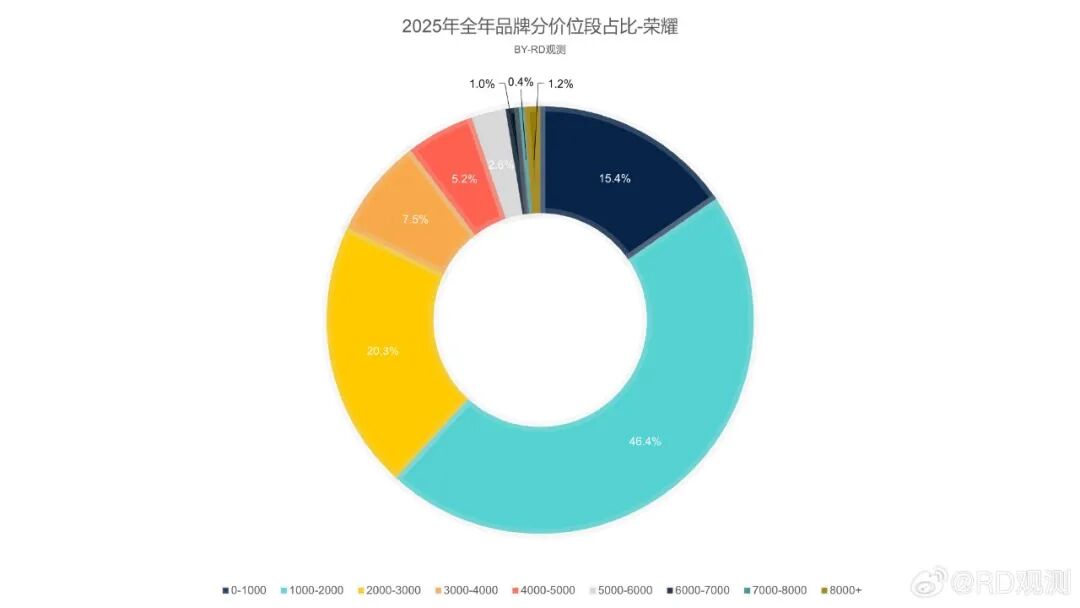

Image source: RD Observation

Against the backdrop of sluggish flagship smartphone sales, to stabilize its market position, Honor has become increasingly reliant on mid-to-low-end products. 'RD Observation' data shows that in 2025, products priced below RMB 2,000 accounted for as much as 61.8% of Honor's smartphone sales structure.

Although Honor has not yet disclosed its prospectus, referencing the financial reports disclosed by Xiaomi, which has a similar positioning, provides insight into the pressure faced by Honor's smartphone business. In Q1 2026, Xiaomi's smartphone shipments were 33.8 million units, down 19.14% year-over-year; its smartphone business gross margin was 10.1%, down 2.3 percentage points year-over-year.

It is worth noting that in 2025, products priced below RMB 2,000 accounted for 50.4% of Xiaomi's smartphone sales structure, 11.4 percentage points lower than Honor's.

Even so, under the pressure of rising memory prices, Xiaomi's smartphone profit margins have been significantly squeezed. Given its greater reliance on mid-to-low-end models, Honor's smartphone profits may face even greater downward pressure.

03 Telling a Grand AI Story, Honor Lacks Transitional Products

Given that its smartphone business has reached a growth bottleneck and struggles to instill confidence in the capital market, with Li Jian assuming the CEO role, Honor has begun to embrace the AI trend and construct a new capital narrative.

Image source: Honor

At MWC 2025 held in March 2025, Li Jian announced the 'Alpha Strategy,' declaring Honor's transformation from a smartphone manufacturer to a globally leading AI terminal ecosystem company. Li Jian revealed that Honor would invest $10 billion over the next five years to establish an open and collaborative AI device ecosystem with global partners.

Image source: Honor

A year later, at MWC, Honor proposed the concept of Augmented Human Intelligence, driving AI advancements in intelligence and lifelikeness, and showcased phased (phased) achievement such as the Robot Phone and embodied AI humanoid robots.

From a market perspective, with the gradual maturation of AI technology, the 'AI terminal ecosystem' targeted by Honor indeed has broad development prospects.

Image source: 36Kr Research Institute

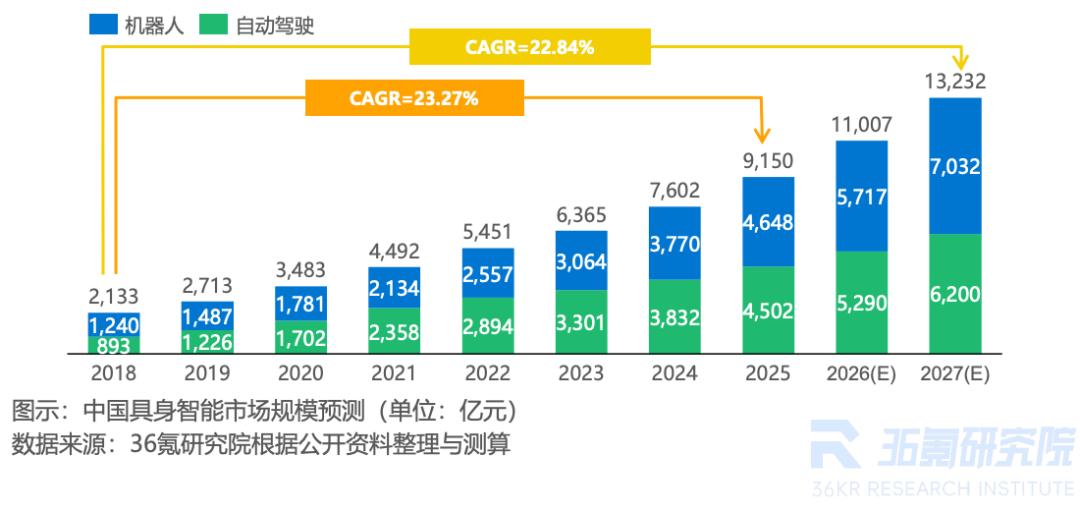

Taking the embodied AI sector as an example, data disclosed by 36Kr Research Institute shows that from 2018 to 2025, the Chinese embodied AI market size grew from RMB 213.3 billion to RMB 915 billion, with a compound annual growth rate of 23.27%. It is expected that by 2027, the relevant market size will reach RMB 1.32 trillion.

Against this backdrop, not only Honor but also tech companies such as Li Auto, XPeng, and Tesla are actively increasing their investments in embodied AI-related businesses.

However, as He Xiaopeng, Chairman and CEO of XPeng Group, said, 'Cars and robots share the same origins. We believe that all AI automotive companies will become robotics companies in the future.' Since autonomous driving and general-purpose humanoid robots originate from the same technological framework, automakers' layout (layout) in embodied AI has strong continuity and foresight.

In contrast, although Honor is also a leading Chinese tech company, its core smartphone business lacks a strong internal connection with embodied AI.

This means that Honor will find it difficult to rapidly iterate embodied AI-related technologies in real-world scenarios like automakers, relying on new energy vehicles to provide sufficient deployment scenarios, data feedback, and shipment volumes for new technologies, thereby forming the scale effects required for industrialization.

In other words, on this new, capital-intensive, and long-cycle track of embodied AI, Honor faces a significant industry gap.

For the capital market, only companies with a solid core business and high growth potential can be considered quality investment targets.

Today, Honor faces the real pressure of declining smartphone shipments, and its newly proposed AI terminal ecosystem strategy has not yet formed a sufficiently close synergistic relationship with its existing core business, making it difficult to quickly grow into a second growth engine.

All these factors suggest that even if Honor successfully lists on the capital market, it may struggle to meet shareholders' high premium expectations in the short term.

END

This article is original content from Shijiao Farsight and is prohibited from reproduction without authorization.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle