Joint Venture’s New Energy Counterattack 2.0: A Turning Point, Not a Total Reversal

05/28 2026

05/28 2026

461

461

“Volkswagen, Toyota, Nissan, and Buick have all made their moves, but declaring victory is premature.”

Author | Zhen Yao Editor | Li Guozheng Produced by | Bangning Studio (gbngzs)

“Once a trend is established, reversing it is difficult.” This is a cardinal rule, repeatedly confirmed by the capital market, highlighting the importance of aligning with market trends.

Over the past five years, three definitive trends have emerged in China's auto market: the rise of electric vehicles (EVs) over fuel-powered cars, the ascent of domestic brands, and the acceleration of automotive intelligence.

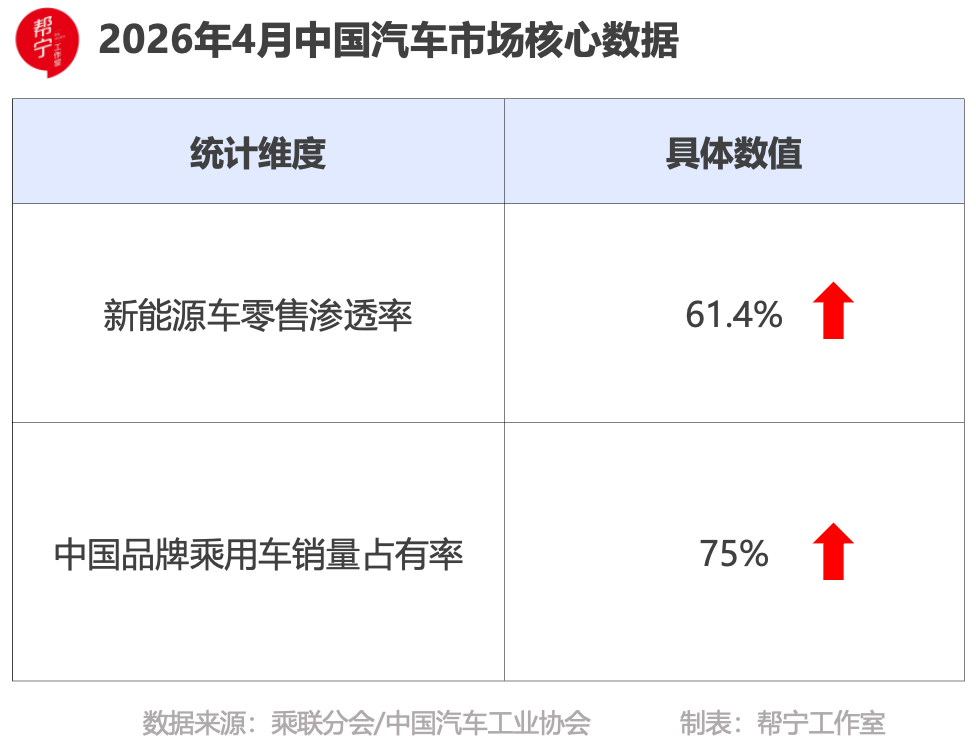

Data underscores these transformations. In April 2026, the retail penetration rate of new energy vehicles (NEVs) surpassed 60% for the first time, reaching 61.4%. The market share of Chinese-brand passenger vehicles climbed to a record high of 75%, leaving joint ventures with a mere 25% share. German, Japanese, American, and Korean brands have all lost ground.

However, it would be premature to conclude that “joint ventures are obsolete.”

On May 24, during the Buick Ultium brand night, news broke that the Ultium E7 had delivered over 10,000 units in its first month on the market. This set a new record for the fastest joint venture NEV to reach 10,000 deliveries, marking the “first true breakthrough of 10,000 units for joint venture NEVs.”

This marks a critical turning point in the joint venture new energy counterattack, proving that joint venture brands can still secure a foothold in the mainstream home-use NEV market. It may drive a collective recovery for joint venture NEV portfolios, including Buick’s Ultium series, Volkswagen’s ID series, Nissan’s N series, and Toyota’s bZ series, definitively ending the narrative of their “complete defeat.”

This is also a localization transformation manifesto from joint venture brands—targeting family users, led by local R&D, and refining product portfolios, abandoning the old approach of “importing global models to China.”

2026 can be called the inaugural year of strategic transformation for the joint venture new energy counterattack.

The Beijing Auto Show held at the end of April epitomized this shift—over a dozen joint venture NEV products, including SAIC Volkswagen’s ID.ERA 9X, FAW-Volkswagen’s ID.AURA T6, Volkswagen Anhui’s Zony 08, Dongfeng Nissan’s NX8, GAC Toyota’s bZ7, and Buick’s Ultium E7, made their debut. All were tailored localization pure electric products designed for Chinese road conditions, user habits, and consumer preferences, marking a new phase of large-scale counterattacks by joint venture NEVs.

Trends are resilient, but the participants in the automotive industry's trends are evolving.

▍01 Who Cracked the Joint Venture 2.0 Code

The joint venture new energy counterattack did not awaken simultaneously; rather, each was roused by the market one after another.

In April 2021, Volkswagen launched the ID.4 CROZZ and ID.4 X in China, firing the first shot in the joint venture counterattack. However, this initial move was conservative, as it was still a direct replication of global models with minimal localization.

For the next two years, joint ventures remained largely silent. It wasn’t until November 2023 that GAC Toyota launched the bZ brand, breaking the stalemate. Toyota did not rush to introduce new products but spent two years refining a localized product system in China.

In 2024, Dongfeng Nissan’s N series made its debut, followed by the N7’s launch in April of the following year, priced starting at 119,900 yuan. In April 2025, Buick unveiled the Ultium brand and showcased three concept cars at the Chengdu Auto Show. In 2026, Hyundai’s IONIQ entered the fray.

By then, German, Japanese, American, and Korean joint venture forces were fully engaged in the new energy race.

The true turning point came in April 2025 with the launch of GAC Toyota’s bZ3X. Orders surpassed 10,000 in one hour, overwhelming servers.

This marked the watershed moment when joint venture NEVs transitioned from the 1.0 model (retrofitting fuel cars to electric) to the 2.0 model (deep localization and collaboration with the Chinese supply chain).

A year later, in April 2026, the bZ brand sold 14,664 units in a single month: the bZ7 sold 4,637 units in its first month, ranking first among joint venture pure electric sedans; the bZ3X reached 10,027 units, topping the joint venture NEV sales charts for eight consecutive months.

Toyota’s automotive manufacturing logic is clear: it prioritizes stability, reliability, and mainstream choices over specifications, targeting the general public rather than tech enthusiasts.

Now, let’s examine Volkswagen’s ID series. It boasts the largest portfolio and faces significant pressure, yet it is severely underestimated.

The ID.3 was once Volkswagen’s hope for NEVs, reaching 13,000 monthly sales in December 2023 with a “fixed price” of 119,800 yuan. But reality was harsh: by 2025, its average monthly sales dropped to 3,200 units; in January 2026, it sold 2,265 units, and in March, only 945 units—a 70% decline in less than two years.

Many seized on the ID.3’s sales figures, arguing that its plunge from 13,000 to 945 units signaled a collapse of Volkswagen’s NEV ambitions.

This judgment was premature.

At the 2026 Beijing Auto Show, Volkswagen revealed its full counterattack strategy, unveiling three products—ID.ERA 9X, ID.AURA T6, and Zony 08—covering the high-end market (200,000-300,000 yuan), the mainstream intelligent track, and entirely new localized models, reconstructing its product layout across three parallel dimensions.

In fact, Dongfeng Nissan’s N series is the fastest-moving pursuer in the joint venture segment. From the N7 and N6 to the NX8, it covers pure electric, plug-in hybrid, and extended-range technologies, all launched within 18 months and targeting the core 90,000-200,000 yuan NEV market segments. Dongfeng Nissan’s strategy is to trade speed for space, prioritizing portfolio completion over perfection before iteration.

However, in China’s NEV market, whether joint ventures or domestic brands, the drawbacks of a fast-paced rollout are evident: new car hype peaks early and fades quickly, making it hard to sustain stable sales.

Compared to Volkswagen and Nissan, Buick may be the true enabler of Joint Venture 2.0.

The Ultium E7 delivered over 10,000 units in its first month, setting a new record for the fastest joint venture NEV to reach 10,000 deliveries. Note that this was not 10,000 orders but 10,000 deliveries, marking the “first true breakthrough of 10,000 units for joint venture NEVs.”

Previously, while the GAC Toyota bZ3X exceeded 10,000 orders, it took much longer to reach 10,000 deliveries. In contrast, the Buick Ultium E7 achieved this milestone in one go.

This demonstrates that the core of Joint Venture 2.0 is not about who launches first but who simultaneously delivers product strength and fulfillment capabilities. With one model, Buick Ultium preempted the narrative that other joint venture automakers took two years to build.

After five years of counterattacks, the joint venture NEV landscape is gradually clarifying—the era of rough expansion is over, and refined localization competition has just begun.

▍02 No Winner Yet

For years, the strategy of joint venture automotive brands in China can be summed up in one sentence: defined abroad, executed in China. Product development was dictated by headquarters, with China only responsible for production and sales.

The result was slow product definition, sluggish NEV transitions, and reliance on price cuts and specification inflation to survive.

Now, this logic is being rewritten.

For example, Buick’s “Ultium Model” centers on relocating R&D decision-making from Detroit to Shanghai. Leveraging Panasia Technical Automotive Center’s self-developed system, SAIC-GM Buick empowers local teams with full decision-making authority from product definition to mass production, abandoning headquarters directives and transforming “global models adapted for China” into “Chinese needs defining global standards.”

GAC Toyota has gone even further. It implements a China Chief Engineer system and a ONE R&D framework, with Chinese teams leading the entire process—from product planning and technology selection to development and validation. Simultaneously, it deeply binds with leading Chinese supply chain enterprises like Hesai, Momenta, Qualcomm, and iFLYTEK, using incubator-style procurement to bring advanced intelligent driving and smart cockpit technologies to models priced at 100,000 yuan.

Dongfeng Nissan’s N series GLOCAL model can be distilled into three keywords: global standards, Chinese speed, and local ecosystems.

Global standards form the foundation—Nissan’s 11-time champion factory system and 17 million-user base continue to demand the highest standards for local manufacturing. Chinese speed drives breakthroughs—the N7, N6, and NX8’s timeline from project initiation to market launch now aligns with new forces. Local ecosystems serve as leverage—integrating CATL’s batteries, Momenta’s intelligent driving, and iFLYTEK’s voice technology into product architectures, creating a “big factory quality + Chinese ecosystem” combination.

Three automakers, three models, but one consensus: joint venture NEVs can only turn the tide not through nostalgia but by entrusting R&D and supply chains to Chinese teams.

Yet challenges persist.

“The entire Chinese automotive market still holds biases against joint venture brands,” said Xue Haitao, Deputy General Manager of SAIC-GM, in a candid remark.

This explains why Buick’s MPV family enlisted Jay Chou, a superstar in Chinese-language music, as a spokesperson. The goal is not to sell cars through Jay Chou but to leverage a national-level IP to swiftly position Buick’s NEVs on consumers’ consideration lists.

This is not unique to Buick but a common dilemma across joint ventures. In the past, few considered domestic brands when buying fuel-powered cars; now, the reverse is true for NEVs.

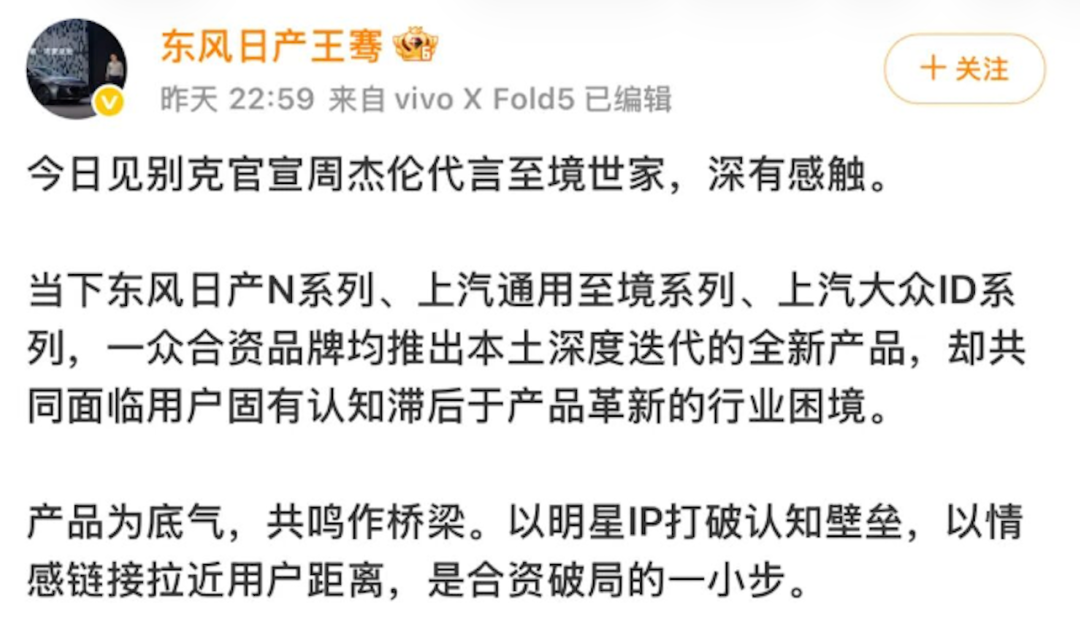

“The product side has completed deep localization iterations, but user perceptions remain stuck in the fuel car era,” Wang Qian, Deputy General Manager of Dongfeng Nissan Sales, wrote on his personal Weibo, highlighting a shared challenge in the joint venture segment.

He believes that while Nissan’s N series, Buick’s Ultium series, and Volkswagen’s ID series are rapidly upgrading technologically and in product strength, consumers still perceive joint venture brands as “fuel-efficient but unintelligent.” Joint venture products have “renewed,” but user impressions have not “caught up.”

This is the biggest obstacle to the joint venture counterattack—not the inadequacy of joint venture products but the rigidity of user perceptions.

How to break through? Synthesizing insights from industry insiders, the core lies in two strategies:

First, superior localized products are the foundation. Without strong localized offerings, all marketing is built on sand. Whether it’s GLOCAL or the Ultium Model, the essence is solving the fundamental issue of product strength.

Second, emotional resonance is the lever. Celebrity endorsements and emotional marketing use IPs to break cognitive barriers, reintroducing users to the “new joint venture.”

With product strength as the backbone and emotional resonance as the bridge, joint venture NEVs can find their breakthrough.

2026 is a “turning point year” for joint venture NEVs, not a “reversal year.” Transformation will not happen overnight; shifting user perceptions takes time, and 2026 may not see a complete turnaround.

But the direction is clear—when product and perception upgrade simultaneously, the upward path for joint venture NEVs opens.

Those joint venture brands that first entrust R&D to China and bind supply chains to local ecosystems have already secured their tickets for the next round of competition.

The remaining question is: When will users realize that joint ventures are no longer what they used to be?

-

![]()

From 'Frequent New Car Launches' to 'Safety Crucible': The Rising Value of Millimeter-Wave Radar Under L2 Mandatory Standards

-

![]()

Kuaishou’s Financial Report: The True Standout Isn’t Short Videos, But Kling AI Beginning to Drive Revenue

-

![]()

Sino-Foreign AI Showdown: Top Three Domestic Models Compete Only for Fifth Place Globally

-

![]()

Joint Venture’s New Energy Counterattack 2.0: A Turning Point, Not a Total Reversal

-

![]()

Is Tesla Coming to China? Are Chinese Automakers Ready? Actually, These Are False Propositions

-

![]()

Alibaba’s Trillion-Yuan Revenue Struggles to Mask Decline as Profits and Cash Flow Tumble

-

![]()

How Did Anthropic, the World's Most Profitable AI Company, Achieve Its Success?

-

![]()

Kuaishou's Q1 Revenue Increases But Profits Decline: 26% Profit Drop, Kling AI Revenue Surges 300% to Become Second Growth Engine